Key Insights

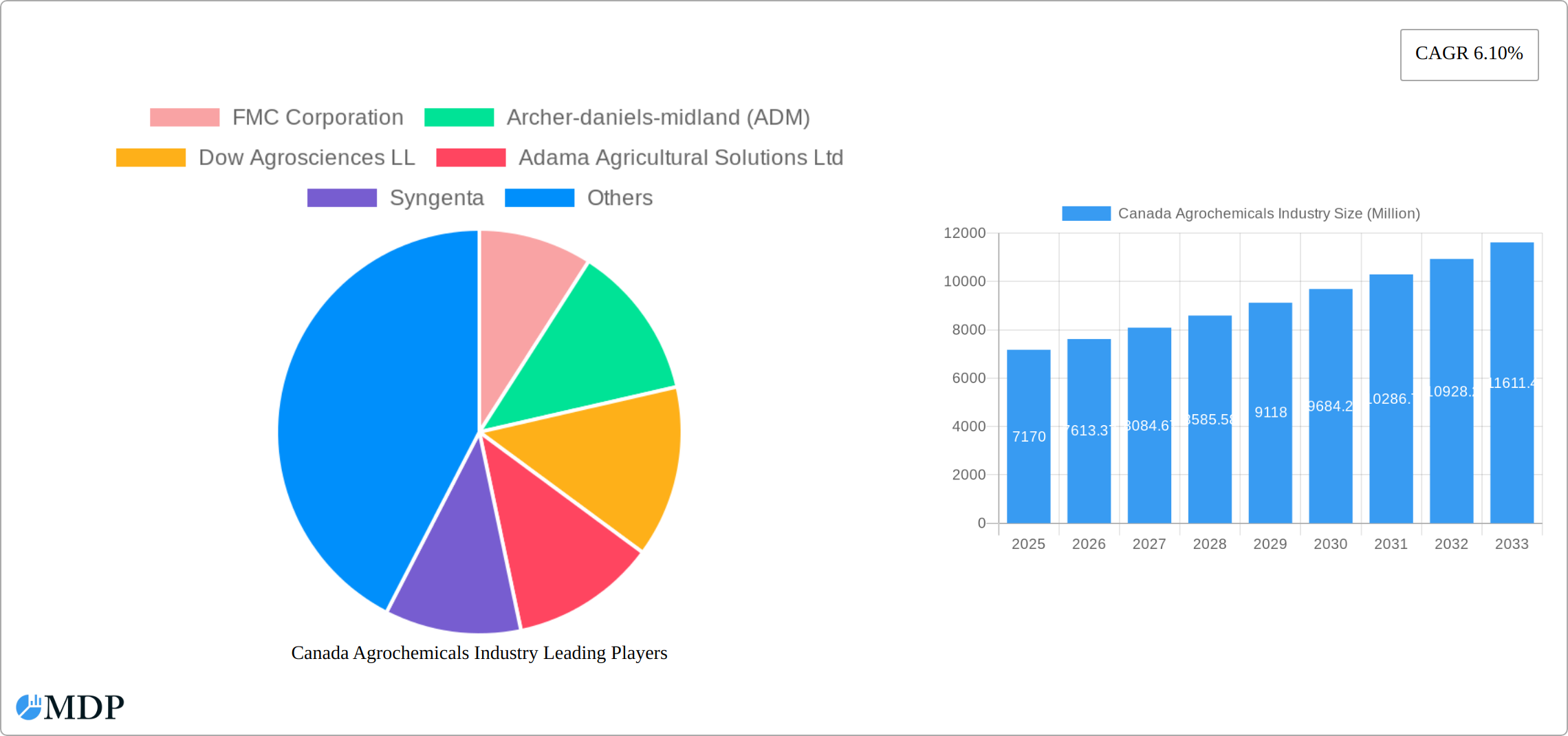

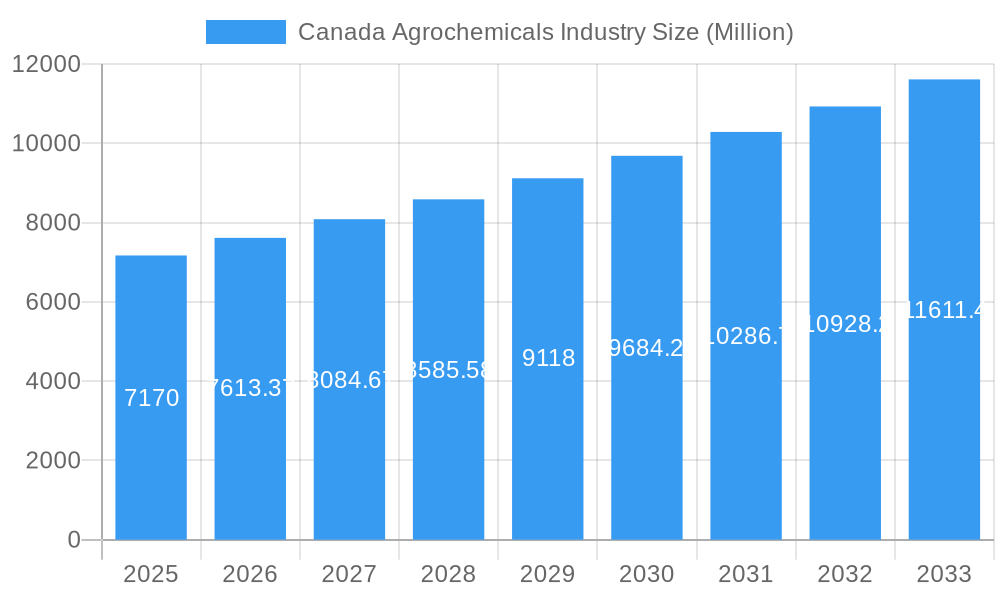

The Canadian agrochemicals market, valued at $7.17 billion in 2025, is projected to experience robust growth, driven by a compound annual growth rate (CAGR) of 6.10% from 2025 to 2033. This expansion is fueled by several key factors. Increasing demand for food security and the rising adoption of advanced farming techniques, including precision agriculture and crop protection strategies, are significant contributors. Furthermore, the growing prevalence of crop diseases and pest infestations necessitates the increased usage of agrochemicals to ensure high crop yields. Government initiatives promoting sustainable agricultural practices, while posing some constraints initially, also indirectly stimulate market growth by fostering the development and adoption of more efficient and environmentally friendly agrochemical solutions. The market is segmented by product type (fertilizers, pesticides, adjuvants, plant growth regulators) and application (grains and cereals, pulses and oilseeds, fruits and vegetables, turf and ornamental grass). Regional variations exist, with potentially higher growth rates in regions like Western Canada due to its extensive agricultural lands. Leading companies such as FMC Corporation, ADM, Dow Agrosciences, Adama, Syngenta, UPL, Corteva, Bayer, Nufarm, and BASF are actively shaping the market through innovation and strategic partnerships.

Canada Agrochemicals Industry Market Size (In Billion)

The competitive landscape is characterized by both established multinational corporations and regional players. The market's future trajectory will depend on factors such as government regulations regarding pesticide usage, fluctuating commodity prices, and the ongoing development of biopesticides and other sustainable alternatives. Further research into specific regional dynamics within Canada (Eastern, Western, and Central Canada) would provide a more granular understanding of market opportunities and challenges. The consistent demand for higher crop yields in the face of climate change and a growing global population will likely sustain the positive growth trajectory of the Canadian agrochemicals market. While some restraints exist related to environmental concerns and regulatory hurdles, innovation and a focus on sustainable solutions within the industry will mitigate these challenges and drive future growth.

Canada Agrochemicals Industry Company Market Share

Canada Agrochemicals Industry: A Comprehensive Market Report (2019-2033)

This comprehensive report provides a detailed analysis of the Canada agrochemicals industry, covering market dynamics, leading players, key trends, and future growth prospects. The study period spans from 2019 to 2033, with 2025 serving as both the base and estimated year. This report is essential for industry stakeholders, investors, and anyone seeking to understand this dynamic market. The report utilizes data in Millions ($).

Canada Agrochemicals Industry Market Dynamics & Concentration

The Canadian agrochemicals market exhibits a moderately concentrated structure, with dominant multinational corporations holding substantial market shares. Key industry players include FMC Corporation, Archer-Daniels-Midland (ADM), Dow Agrosciences LL, Adama Agricultural Solutions Ltd, Syngenta, UPL Limited, Corteva Agriscience, Bayer CropScience AG, Nufarm Ltd, and BASF SE. These entities collectively are estimated to command approximately **[Insert Specific Market Share Percentage]**% of the market in 2025. Market share dynamics are intricately linked to continuous innovation, evolving regulatory landscapes, and strategic Mergers & Acquisitions (M&A) activity. The historical period (2019-2024) saw around **[Insert Number]** significant M&A deals, largely driven by the strategic imperative to broaden product portfolios and expand geographical footprints. Major innovation drivers encompass the persistent need to achieve higher crop yields, enhance pest and disease resistance, and respond to the escalating demand for sustainable agricultural methodologies. Stringent regulatory frameworks governing the registration and application of pesticides significantly influence product availability and market entry barriers. While still in its nascent stages, the presence of alternative solutions, such as biopesticides, is showing a gradual upward trend. Furthermore, evolving end-user trends, notably the widespread adoption of precision agriculture, are fundamentally reshaping demand patterns within the sector.

Canada Agrochemicals Industry Industry Trends & Analysis

The Canadian agrochemicals market is anticipated to experience a robust Compound Annual Growth Rate (CAGR) of **[Insert Specific CAGR Percentage]**% during the forecast period spanning 2025-2033. This projected growth is propelled by a confluence of key factors. The imperative to augment agricultural production to satisfy escalating global food demand serves as a primary catalyst. Significant technological advancements, including the development of more efficacious and precisely targeted pesticides and fertilizers, are instrumental in driving higher yields and optimizing operational efficiency. Shifting consumer preferences towards sustainably produced food are increasingly influencing the demand for biopesticides and other environmentally conscious agrochemical solutions. The competitive landscape is characterized by a continuous cycle of innovation, the formation of strategic alliances, and dynamic M&A activities, all of which contribute to intensifying market dynamics. The gradual but increasing penetration of novel technologies, such as precision spraying and drone-based application systems, is enhancing application efficacy and minimizing environmental footprints. The overarching trend towards the adoption of sustainable agricultural practices is also a significant driver for specific product segments within the market.

Leading Markets & Segments in Canada Agrochemicals Industry

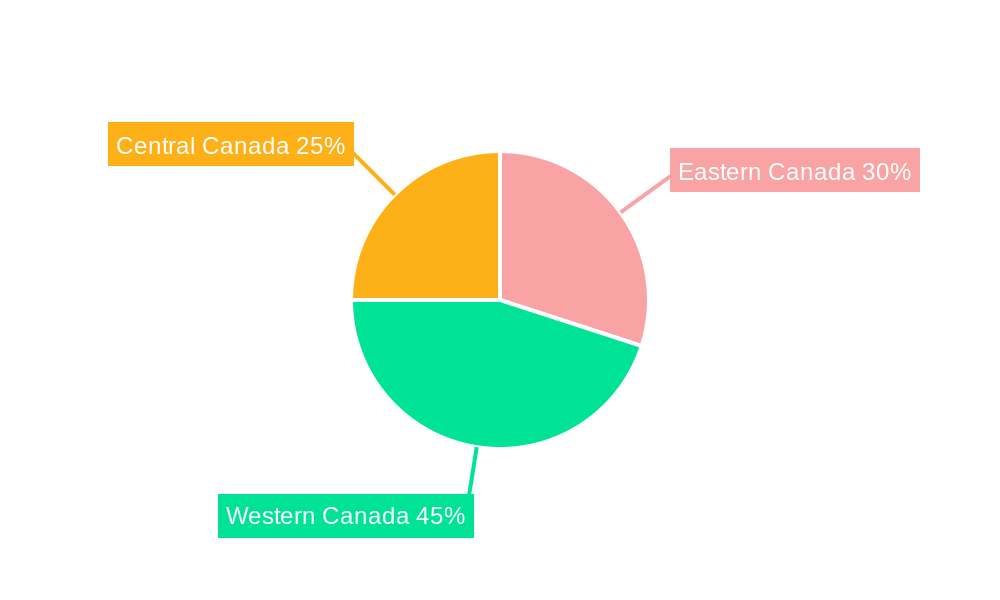

The Canadian agrochemicals market is geographically diverse, demonstrating strong performance across various regions. However, the Prairie provinces, encompassing Alberta, Saskatchewan, and Manitoba, stand out as the most significant market segment, largely attributed to their substantial contribution to Canada's grain and oilseed production.

Key Drivers for Dominant Segments:

- Grains and Cereals: Extensive cultivation areas, intensive farming practices, and inherent susceptibility to pests and diseases collectively fuel a robust demand for fertilizers and pesticides in this segment.

- Pulses and Oilseeds: The escalating global demand for pulses and oilseeds, coupled with the expanding acreage dedicated to these crops in Canada, provides a strong impetus for market growth within this segment.

- Fruits and Vegetables: A growing consumer appetite for fresh produce directly translates into an increased demand for specialized agrochemicals tailored for horticultural crops.

- Turf and Ornamental Grass: The robust landscaping and golf course industries sustain a consistent demand for herbicides and fertilizers in the turf and ornamental segment.

Dominance Analysis: Currently, the fertilizers segment commands the largest market share, closely followed by pesticides. However, the adjuvants and plant growth regulators segments are experiencing accelerated growth, largely driven by the increasing adoption of precision agriculture techniques. Favorable economic policies designed to foster agricultural expansion and advancements in infrastructure, including enhanced transportation networks, further contribute to the overall market's upward trajectory.

Canada Agrochemicals Industry Product Developments

Recent product innovations focus on improving efficacy, reducing environmental impact, and enhancing convenience for farmers. The launch of new herbicides, such as Gowan Canada and ISK Biosciences' Insight 339SC, exemplifies this trend towards more targeted and effective solutions. These developments reflect a shift towards sustainable and precision agriculture practices, meeting the needs of environmentally conscious consumers and addressing regulatory pressures.

Key Drivers of Canada Agrochemicals Industry Growth

Several pivotal factors are contributing to the sustained growth of the Canadian agrochemicals market. These include the intensification of agricultural production to meet burgeoning global food requirements, significant technological advancements that lead to higher crop yields and improved operational efficiency, and proactive government initiatives championing sustainable agricultural practices. The widespread adoption of precision agriculture techniques is a key enabler, enhancing the efficiency of agrochemical applications, thereby reducing waste and mitigating environmental impact. Furthermore, favorable macroeconomic conditions and substantial investments in agricultural infrastructure serve as crucial supports for ongoing market expansion.

Challenges in the Canada Agrochemicals Industry Market

The Canadian agrochemicals industry faces several challenges, including stringent regulatory hurdles for pesticide registration, potential supply chain disruptions impacting raw material availability and pricing, and increased competition from both domestic and international players. These challenges result in increased production costs and potential market volatility. The overall impact of these restraints is a projected xx% reduction in market growth compared to a scenario without these challenges.

Emerging Opportunities in Canada Agrochemicals Industry

The Canadian agrochemicals market presents significant long-term growth opportunities. Technological advancements, such as the development of biopesticides and precision agriculture technologies, create new market segments and enhance sustainability. Strategic partnerships between agrochemical companies and agricultural technology firms facilitate innovation and market expansion. The increasing emphasis on sustainable and environmentally friendly agricultural practices creates new opportunities for bio-based products and services.

Leading Players in the Canada Agrochemicals Industry Sector

Key Milestones in Canada Agrochemicals Industry Industry

- September 2022: Gowan Canada and ISK BioSciences launched 'Insight 339SC', a new group 14 herbicide, impacting pre-seed burnoff applications and weed control strategies.

- July 2022: Pivot Bio's expansion into Canada signals a shift toward sustainable nitrogen solutions and potentially alters fertilizer market dynamics.

- May 2022: Protein Industries Canada's USD 19 million project for micronutrient fertilizer commercialization promotes sustainability and reduces carbon emissions, influencing fertilizer market composition.

Strategic Outlook for Canada Agrochemicals Industry Market

The Canadian agrochemicals market is strategically positioned for continued and substantial growth, underpinned by ongoing technological advancements, an increasing emphasis on sustainable agricultural practices, and a supportive economic environment. Strategic partnerships and significant investments in research and development (R&D) will play a critical role in shaping the future trajectory of market dynamics. Companies that prioritize the development and offering of innovative, sustainable, and highly efficient solutions will be best equipped to capitalize on the considerable growth potential inherent in the Canadian agrochemicals market.

Canada Agrochemicals Industry Segmentation

- 1. Production Analysis

- 2. Consumption Analysis

- 3. Import Market Analysis (Value & Volume)

- 4. Export Market Analysis (Value & Volume)

- 5. Price Trend Analysis

Canada Agrochemicals Industry Segmentation By Geography

- 1. Canada

Canada Agrochemicals Industry Regional Market Share

Geographic Coverage of Canada Agrochemicals Industry

Canada Agrochemicals Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 6.10% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Decreasing Per Capita Arable Land; Increased Demand for Food

- 3.3. Market Restrains

- 3.3.1. High Initial Investments; Requirement of Precision Agriculture

- 3.4. Market Trends

- 3.4.1. Need for Improving Productivity by Limiting the Crop Damage

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Canada Agrochemicals Industry Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Production Analysis

- 5.2. Market Analysis, Insights and Forecast - by Consumption Analysis

- 5.3. Market Analysis, Insights and Forecast - by Import Market Analysis (Value & Volume)

- 5.4. Market Analysis, Insights and Forecast - by Export Market Analysis (Value & Volume)

- 5.5. Market Analysis, Insights and Forecast - by Price Trend Analysis

- 5.6. Market Analysis, Insights and Forecast - by Region

- 5.6.1. Canada

- 5.1. Market Analysis, Insights and Forecast - by Production Analysis

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2025

- 6.2. Company Profiles

- 6.2.1 FMC Corporation

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Archer-daniels-midland (ADM)

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Dow Agrosciences LL

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Adama Agricultural Solutions Ltd

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Syngenta

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 UPL Limited

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Corteva Agriscience

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Bayer CropScience AG

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Nufarm Ltd

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 BASF SE

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.1 FMC Corporation

List of Figures

- Figure 1: Canada Agrochemicals Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Canada Agrochemicals Industry Share (%) by Company 2025

List of Tables

- Table 1: Canada Agrochemicals Industry Revenue Million Forecast, by Production Analysis 2020 & 2033

- Table 2: Canada Agrochemicals Industry Revenue Million Forecast, by Consumption Analysis 2020 & 2033

- Table 3: Canada Agrochemicals Industry Revenue Million Forecast, by Import Market Analysis (Value & Volume) 2020 & 2033

- Table 4: Canada Agrochemicals Industry Revenue Million Forecast, by Export Market Analysis (Value & Volume) 2020 & 2033

- Table 5: Canada Agrochemicals Industry Revenue Million Forecast, by Price Trend Analysis 2020 & 2033

- Table 6: Canada Agrochemicals Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 7: Canada Agrochemicals Industry Revenue Million Forecast, by Production Analysis 2020 & 2033

- Table 8: Canada Agrochemicals Industry Revenue Million Forecast, by Consumption Analysis 2020 & 2033

- Table 9: Canada Agrochemicals Industry Revenue Million Forecast, by Import Market Analysis (Value & Volume) 2020 & 2033

- Table 10: Canada Agrochemicals Industry Revenue Million Forecast, by Export Market Analysis (Value & Volume) 2020 & 2033

- Table 11: Canada Agrochemicals Industry Revenue Million Forecast, by Price Trend Analysis 2020 & 2033

- Table 12: Canada Agrochemicals Industry Revenue Million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Canada Agrochemicals Industry?

The projected CAGR is approximately 6.10%.

2. Which companies are prominent players in the Canada Agrochemicals Industry?

Key companies in the market include FMC Corporation, Archer-daniels-midland (ADM), Dow Agrosciences LL, Adama Agricultural Solutions Ltd, Syngenta, UPL Limited, Corteva Agriscience, Bayer CropScience AG, Nufarm Ltd, BASF SE.

3. What are the main segments of the Canada Agrochemicals Industry?

The market segments include Production Analysis, Consumption Analysis, Import Market Analysis (Value & Volume), Export Market Analysis (Value & Volume), Price Trend Analysis.

4. Can you provide details about the market size?

The market size is estimated to be USD 7.17 Million as of 2022.

5. What are some drivers contributing to market growth?

Decreasing Per Capita Arable Land; Increased Demand for Food.

6. What are the notable trends driving market growth?

Need for Improving Productivity by Limiting the Crop Damage.

7. Are there any restraints impacting market growth?

High Initial Investments; Requirement of Precision Agriculture.

8. Can you provide examples of recent developments in the market?

September 2022: Gowan Canada and ISK BioSciences launched 'Insight 339SC', a new group 14 herbicide for pre-seed burnoff applications in wheat, corn, and soybean. Insight 339SC provides rapid and effective pre-seed burndown of important broadleaf weeds like kochia, redroot pigweed, common lamb's quarters, and wild buckwheat.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Canada Agrochemicals Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Canada Agrochemicals Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Canada Agrochemicals Industry?

To stay informed about further developments, trends, and reports in the Canada Agrochemicals Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence