Key Insights

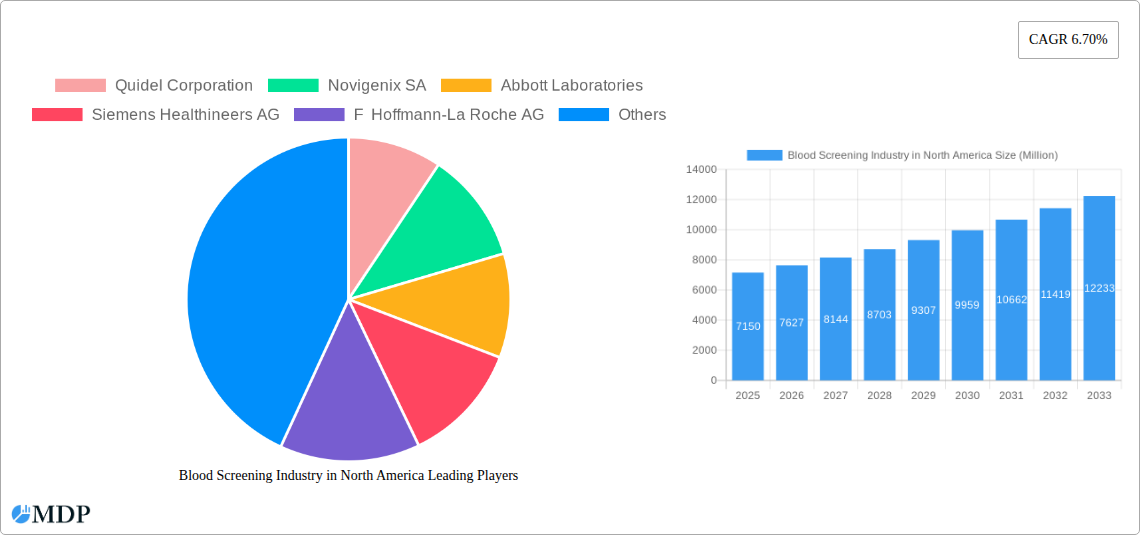

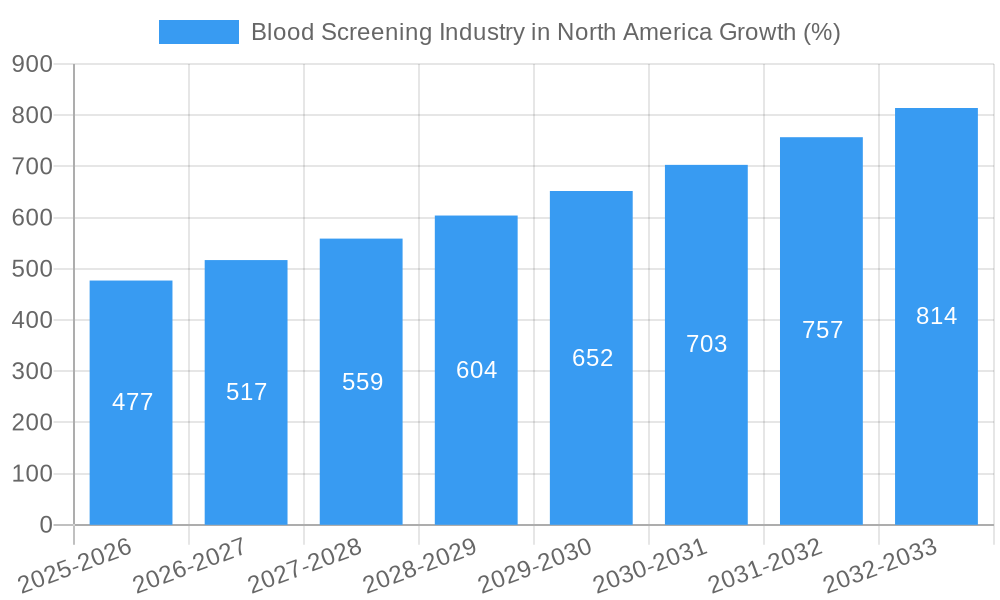

The North American blood screening market, valued at approximately $7.15 billion in 2025, is projected to experience robust growth, driven by factors such as an aging population, increasing prevalence of chronic diseases like colorectal cancer and cardiovascular diseases, and rising awareness about preventive healthcare. The market's Compound Annual Growth Rate (CAGR) of 6.70% from 2025 to 2033 indicates a significant expansion, reaching an estimated market value exceeding $12 billion by 2033. This growth is further fueled by technological advancements in screening tests, such as the increasing adoption of stool DNA tests offering higher sensitivity and specificity compared to traditional stool-based tests. The shift toward non-invasive screening methods and the growing availability of advanced diagnostic equipment in hospitals and diagnostic centers are also contributing factors. However, high costs associated with advanced screening technologies and the potential for false-positive results, leading to unnecessary follow-up procedures, act as market restraints. The market segmentation reveals significant contributions from stool-based tests and colonoscopy within the screening tests segment and a considerable market share held by hospitals and diagnostic centers within the end-user segment.

The competitive landscape is characterized by a mix of established multinational corporations like Abbott Laboratories, Roche, and Siemens Healthineers, and specialized companies focusing on innovative blood screening technologies. The increasing adoption of telehealth and remote patient monitoring may further accelerate market growth by expanding access to screening services. Regulatory approvals for new and improved screening tests, and increasing insurance coverage for these tests, will play a crucial role in shaping market dynamics. Furthermore, the ongoing research and development efforts focused on improving test accuracy and reducing costs will be key to sustaining the market's growth trajectory. The North American market is expected to maintain its dominance due to factors including high healthcare expenditure, advanced infrastructure, and strong regulatory support for medical innovation.

Blood Screening Industry in North America: 2019-2033 Market Report

This comprehensive report provides a detailed analysis of the North American blood screening industry, covering market dynamics, leading players, technological advancements, and future growth prospects from 2019 to 2033. The study period spans 2019-2033, with 2025 as the base and estimated year. The forecast period is 2025-2033, and the historical period covers 2019-2024. This in-depth analysis is crucial for investors, industry stakeholders, and strategic decision-makers seeking to navigate this rapidly evolving market. Key segments analyzed include stool-based tests, stool DNA tests, colonoscopy, CT colonography, flexible sigmoidoscopy, other products, and end-users (hospitals, diagnostic centers/laboratories, and other end-users). Leading companies such as Quidel Corporation, Abbott Laboratories, and Exact Sciences Corporation are profiled, providing valuable competitive intelligence.

Blood Screening Industry in North America Market Dynamics & Concentration

The North American blood screening market exhibits a moderately concentrated landscape, with a few major players holding significant market share. The market's dynamics are shaped by several key factors. Innovation is a primary driver, with continuous advancements in technologies like ctDNA analysis pushing the boundaries of early disease detection. Stringent regulatory frameworks, particularly from the FDA, influence product approvals and market entry. The presence of substitute diagnostic methods, such as traditional colonoscopies, creates competitive pressures. End-user trends, including increasing demand for minimally invasive procedures and early detection, fuel market growth. Finally, mergers and acquisitions (M&A) activity is frequent, reflecting consolidation within the industry.

- Market Concentration: The top 5 players collectively hold an estimated xx% market share in 2025.

- Innovation Drivers: Advancements in molecular diagnostics, AI-powered analysis, and liquid biopsy technologies.

- Regulatory Landscape: Stringent FDA regulations for blood tests drive product development and validation.

- Product Substitutes: Traditional colonoscopy and other imaging techniques compete with blood-based screenings.

- End-User Trends: Growing preference for non-invasive screening methods among the aging population.

- M&A Activity: An average of xx M&A deals per year were observed during the historical period (2019-2024).

Blood Screening Industry in North America Industry Trends & Analysis

The North American blood screening market is experiencing robust growth, driven by several factors. The market is expected to witness a Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025-2033). Technological disruptions, particularly in next-generation sequencing and artificial intelligence, are enhancing diagnostic accuracy and efficiency. Consumer preferences are shifting towards minimally invasive and convenient screening methods, boosting demand for blood-based tests. Competitive dynamics are intense, with companies investing heavily in R&D and strategic partnerships to gain a market edge. Market penetration of blood-based colorectal cancer screening is projected to reach xx% by 2033. This growth is further fueled by increasing awareness of early detection's importance and government initiatives promoting preventative healthcare. The increasing prevalence of chronic diseases also fuels market expansion.

Leading Markets & Segments in Blood Screening Industry in North America

The United States dominates the North American blood screening market, owing to its advanced healthcare infrastructure, higher disposable incomes, and increased awareness of preventative healthcare. Within screening tests, stool-based tests currently hold the largest market share, followed by stool DNA tests. However, the market for blood-based tests, including ctDNA analysis, is anticipated to experience significant growth.

- Dominant Region: United States

- Key Drivers for US Dominance:

- Advanced healthcare infrastructure and technological capabilities.

- High prevalence of colorectal cancer and other target diseases.

- Robust government funding for healthcare research and development.

- High consumer awareness of preventative healthcare and early detection.

- Segment Analysis: Stool-based tests maintain a larger market share due to established usage and familiarity. However, the stool DNA test segment is growing rapidly due to improved accuracy and technological advancements. Blood-based tests like ctDNA assays show the highest growth potential. Hospitals and diagnostic centers/laboratories are the primary end-users.

Blood Screening Industry in North America Product Developments

Significant advancements are transforming the blood screening landscape. The development of more sensitive and specific blood-based tests utilizing advanced technologies like next-generation sequencing (NGS) and digital PCR is a major trend. These innovations provide earlier and more accurate detection of various cancers and other diseases, resulting in improved patient outcomes. The integration of artificial intelligence (AI) and machine learning (ML) further enhances diagnostic accuracy and efficiency. The market is witnessing a transition towards multi-cancer early detection (MCED) blood tests, offering simultaneous screening for a range of cancers, improving screening efficiency and cost-effectiveness.

Key Drivers of Blood Screening Industry in North America Growth

Several factors contribute to the market’s growth. Technological advancements, such as improved sensitivity and specificity of blood tests, coupled with declining costs, are making blood screening more accessible and affordable. Favorable regulatory environments and reimbursement policies support wider adoption. Furthermore, increasing public awareness of the benefits of early disease detection and proactive healthcare contributes significantly to market expansion. Government initiatives promoting preventative healthcare further fuel growth.

Challenges in the Blood Screening Industry in North America Market

Despite significant growth potential, the blood screening industry faces challenges. High initial costs associated with the development and validation of new assays create barriers to entry. Complex regulatory pathways and reimbursement policies can delay product approvals and market access. Moreover, competition among established players and emerging biotech firms is fierce, potentially impacting profitability. Supply chain disruptions and fluctuations in raw material prices can impact production costs. Lastly, ensuring patient access and affordability remains a persistent challenge.

Emerging Opportunities in Blood Screening Industry in North America

The market presents several exciting opportunities. Advancements in liquid biopsy technologies and AI-driven diagnostics promise significant improvements in early cancer detection and personalized medicine. Strategic collaborations between diagnostic companies and pharmaceutical firms can accelerate product development and market penetration. Expansion into underserved markets and the development of cost-effective screening solutions will create further growth avenues. The development of multi-cancer early detection tests (MCED) will broaden market accessibility and affordability.

Leading Players in the Blood Screening Industry in North America Sector

- Quidel Corporation

- Novigenix SA

- Abbott Laboratories

- Siemens Healthineers AG

- F Hoffmann-La Roche AG

- Exact Sciences Corporation

- Clinical Genomics Technologies Pty Ltd

- EKF Diagnostics

- MAINZ BIOMED N V

- Sysmex Corporation

- Epigenomics Inc

- Hemosure Inc

Key Milestones in Blood Screening Industry in North America Industry

- December 2022: Guardant Health, Inc. announced positive results from the ECLIPSE study, demonstrating the potential of its blood test for detecting colorectal cancer in average-risk adults. This significantly boosts the credibility and adoption of blood-based CRC screening.

- February 2022: The FDA approved QIAGEN Manchester Ltd.'s Therascreen KRAS RGQ PCR Kit for colorectal cancer screening, expanding the available tools for targeted cancer detection.

Strategic Outlook for Blood Screening Industry in North America Market

The North American blood screening market is poised for continued expansion, driven by technological innovation, increasing awareness of early detection, and supportive regulatory environments. Strategic partnerships, investments in R&D, and expansion into new markets are critical for success. Companies focused on developing highly sensitive, specific, and cost-effective blood-based tests will be well-positioned to capitalize on this growing opportunity. The market holds significant potential for players who can effectively integrate advanced technologies such as AI and ML into their diagnostic platforms.

Blood Screening Industry in North America Segmentation

-

1. Screening Tests

-

1.1. Stool-based Tests

- 1.1.1. Fecal Immunochemical Test (FIT)

- 1.1.2. Guaiac-based Fecal Occult Blood Test (gFOBT)

- 1.1.3. Stool DNA Test

- 1.2. Colonoscopy

- 1.3. CT Colonography (Virtual Colonoscopy)

- 1.4. Flexible Sigmoidoscopy

- 1.5. Other Screening Tests

-

1.1. Stool-based Tests

-

2. End User

- 2.1. Hospitals

- 2.2. Diagnostic Centers/Laboratories

- 2.3. Other End Users

-

3. Geography

- 3.1. United States

- 3.2. Canada

- 3.3. Mexico

Blood Screening Industry in North America Segmentation By Geography

- 1. United States

- 2. Canada

- 3. Mexico

Blood Screening Industry in North America REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 6.70% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Prevalence of Colorectal Cancer; Technological advancements and Increasing Cancer Prevention Initiatives

- 3.3. Market Restrains

- 3.3.1. High Screening Tests Costs

- 3.4. Market Trends

- 3.4.1. Guaiac Fecal Occult Blood Test (gFOBT) is Expected to be Hold a Significant Market Share Over the Forecast Period

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Blood Screening Industry in North America Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Screening Tests

- 5.1.1. Stool-based Tests

- 5.1.1.1. Fecal Immunochemical Test (FIT)

- 5.1.1.2. Guaiac-based Fecal Occult Blood Test (gFOBT)

- 5.1.1.3. Stool DNA Test

- 5.1.2. Colonoscopy

- 5.1.3. CT Colonography (Virtual Colonoscopy)

- 5.1.4. Flexible Sigmoidoscopy

- 5.1.5. Other Screening Tests

- 5.1.1. Stool-based Tests

- 5.2. Market Analysis, Insights and Forecast - by End User

- 5.2.1. Hospitals

- 5.2.2. Diagnostic Centers/Laboratories

- 5.2.3. Other End Users

- 5.3. Market Analysis, Insights and Forecast - by Geography

- 5.3.1. United States

- 5.3.2. Canada

- 5.3.3. Mexico

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. United States

- 5.4.2. Canada

- 5.4.3. Mexico

- 5.1. Market Analysis, Insights and Forecast - by Screening Tests

- 6. United States Blood Screening Industry in North America Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Screening Tests

- 6.1.1. Stool-based Tests

- 6.1.1.1. Fecal Immunochemical Test (FIT)

- 6.1.1.2. Guaiac-based Fecal Occult Blood Test (gFOBT)

- 6.1.1.3. Stool DNA Test

- 6.1.2. Colonoscopy

- 6.1.3. CT Colonography (Virtual Colonoscopy)

- 6.1.4. Flexible Sigmoidoscopy

- 6.1.5. Other Screening Tests

- 6.1.1. Stool-based Tests

- 6.2. Market Analysis, Insights and Forecast - by End User

- 6.2.1. Hospitals

- 6.2.2. Diagnostic Centers/Laboratories

- 6.2.3. Other End Users

- 6.3. Market Analysis, Insights and Forecast - by Geography

- 6.3.1. United States

- 6.3.2. Canada

- 6.3.3. Mexico

- 6.1. Market Analysis, Insights and Forecast - by Screening Tests

- 7. Canada Blood Screening Industry in North America Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Screening Tests

- 7.1.1. Stool-based Tests

- 7.1.1.1. Fecal Immunochemical Test (FIT)

- 7.1.1.2. Guaiac-based Fecal Occult Blood Test (gFOBT)

- 7.1.1.3. Stool DNA Test

- 7.1.2. Colonoscopy

- 7.1.3. CT Colonography (Virtual Colonoscopy)

- 7.1.4. Flexible Sigmoidoscopy

- 7.1.5. Other Screening Tests

- 7.1.1. Stool-based Tests

- 7.2. Market Analysis, Insights and Forecast - by End User

- 7.2.1. Hospitals

- 7.2.2. Diagnostic Centers/Laboratories

- 7.2.3. Other End Users

- 7.3. Market Analysis, Insights and Forecast - by Geography

- 7.3.1. United States

- 7.3.2. Canada

- 7.3.3. Mexico

- 7.1. Market Analysis, Insights and Forecast - by Screening Tests

- 8. Mexico Blood Screening Industry in North America Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Screening Tests

- 8.1.1. Stool-based Tests

- 8.1.1.1. Fecal Immunochemical Test (FIT)

- 8.1.1.2. Guaiac-based Fecal Occult Blood Test (gFOBT)

- 8.1.1.3. Stool DNA Test

- 8.1.2. Colonoscopy

- 8.1.3. CT Colonography (Virtual Colonoscopy)

- 8.1.4. Flexible Sigmoidoscopy

- 8.1.5. Other Screening Tests

- 8.1.1. Stool-based Tests

- 8.2. Market Analysis, Insights and Forecast - by End User

- 8.2.1. Hospitals

- 8.2.2. Diagnostic Centers/Laboratories

- 8.2.3. Other End Users

- 8.3. Market Analysis, Insights and Forecast - by Geography

- 8.3.1. United States

- 8.3.2. Canada

- 8.3.3. Mexico

- 8.1. Market Analysis, Insights and Forecast - by Screening Tests

- 9. United States Blood Screening Industry in North America Analysis, Insights and Forecast, 2019-2031

- 10. Canada Blood Screening Industry in North America Analysis, Insights and Forecast, 2019-2031

- 11. Mexico Blood Screening Industry in North America Analysis, Insights and Forecast, 2019-2031

- 12. Rest of North America Blood Screening Industry in North America Analysis, Insights and Forecast, 2019-2031

- 13. Competitive Analysis

- 13.1. Market Share Analysis 2024

- 13.2. Company Profiles

- 13.2.1 Quidel Corporation

- 13.2.1.1. Overview

- 13.2.1.2. Products

- 13.2.1.3. SWOT Analysis

- 13.2.1.4. Recent Developments

- 13.2.1.5. Financials (Based on Availability)

- 13.2.2 Novigenix SA

- 13.2.2.1. Overview

- 13.2.2.2. Products

- 13.2.2.3. SWOT Analysis

- 13.2.2.4. Recent Developments

- 13.2.2.5. Financials (Based on Availability)

- 13.2.3 Abbott Laboratories

- 13.2.3.1. Overview

- 13.2.3.2. Products

- 13.2.3.3. SWOT Analysis

- 13.2.3.4. Recent Developments

- 13.2.3.5. Financials (Based on Availability)

- 13.2.4 Siemens Healthineers AG

- 13.2.4.1. Overview

- 13.2.4.2. Products

- 13.2.4.3. SWOT Analysis

- 13.2.4.4. Recent Developments

- 13.2.4.5. Financials (Based on Availability)

- 13.2.5 F Hoffmann-La Roche AG

- 13.2.5.1. Overview

- 13.2.5.2. Products

- 13.2.5.3. SWOT Analysis

- 13.2.5.4. Recent Developments

- 13.2.5.5. Financials (Based on Availability)

- 13.2.6 Exact Sciences Corporation

- 13.2.6.1. Overview

- 13.2.6.2. Products

- 13.2.6.3. SWOT Analysis

- 13.2.6.4. Recent Developments

- 13.2.6.5. Financials (Based on Availability)

- 13.2.7 Clinical Genomics Technologies Pty Ltd

- 13.2.7.1. Overview

- 13.2.7.2. Products

- 13.2.7.3. SWOT Analysis

- 13.2.7.4. Recent Developments

- 13.2.7.5. Financials (Based on Availability)

- 13.2.8 EKF Diagnostics

- 13.2.8.1. Overview

- 13.2.8.2. Products

- 13.2.8.3. SWOT Analysis

- 13.2.8.4. Recent Developments

- 13.2.8.5. Financials (Based on Availability)

- 13.2.9 MAINZ BIOMED N V

- 13.2.9.1. Overview

- 13.2.9.2. Products

- 13.2.9.3. SWOT Analysis

- 13.2.9.4. Recent Developments

- 13.2.9.5. Financials (Based on Availability)

- 13.2.10 Sysmex Corporation

- 13.2.10.1. Overview

- 13.2.10.2. Products

- 13.2.10.3. SWOT Analysis

- 13.2.10.4. Recent Developments

- 13.2.10.5. Financials (Based on Availability)

- 13.2.11 Epigenomics Inc

- 13.2.11.1. Overview

- 13.2.11.2. Products

- 13.2.11.3. SWOT Analysis

- 13.2.11.4. Recent Developments

- 13.2.11.5. Financials (Based on Availability)

- 13.2.12 Hemosure Inc

- 13.2.12.1. Overview

- 13.2.12.2. Products

- 13.2.12.3. SWOT Analysis

- 13.2.12.4. Recent Developments

- 13.2.12.5. Financials (Based on Availability)

- 13.2.1 Quidel Corporation

List of Figures

- Figure 1: Blood Screening Industry in North America Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Blood Screening Industry in North America Share (%) by Company 2024

List of Tables

- Table 1: Blood Screening Industry in North America Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Blood Screening Industry in North America Volume K Unit Forecast, by Region 2019 & 2032

- Table 3: Blood Screening Industry in North America Revenue Million Forecast, by Screening Tests 2019 & 2032

- Table 4: Blood Screening Industry in North America Volume K Unit Forecast, by Screening Tests 2019 & 2032

- Table 5: Blood Screening Industry in North America Revenue Million Forecast, by End User 2019 & 2032

- Table 6: Blood Screening Industry in North America Volume K Unit Forecast, by End User 2019 & 2032

- Table 7: Blood Screening Industry in North America Revenue Million Forecast, by Geography 2019 & 2032

- Table 8: Blood Screening Industry in North America Volume K Unit Forecast, by Geography 2019 & 2032

- Table 9: Blood Screening Industry in North America Revenue Million Forecast, by Region 2019 & 2032

- Table 10: Blood Screening Industry in North America Volume K Unit Forecast, by Region 2019 & 2032

- Table 11: Blood Screening Industry in North America Revenue Million Forecast, by Country 2019 & 2032

- Table 12: Blood Screening Industry in North America Volume K Unit Forecast, by Country 2019 & 2032

- Table 13: United States Blood Screening Industry in North America Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: United States Blood Screening Industry in North America Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 15: Canada Blood Screening Industry in North America Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: Canada Blood Screening Industry in North America Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 17: Mexico Blood Screening Industry in North America Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: Mexico Blood Screening Industry in North America Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 19: Rest of North America Blood Screening Industry in North America Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Rest of North America Blood Screening Industry in North America Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 21: Blood Screening Industry in North America Revenue Million Forecast, by Screening Tests 2019 & 2032

- Table 22: Blood Screening Industry in North America Volume K Unit Forecast, by Screening Tests 2019 & 2032

- Table 23: Blood Screening Industry in North America Revenue Million Forecast, by End User 2019 & 2032

- Table 24: Blood Screening Industry in North America Volume K Unit Forecast, by End User 2019 & 2032

- Table 25: Blood Screening Industry in North America Revenue Million Forecast, by Geography 2019 & 2032

- Table 26: Blood Screening Industry in North America Volume K Unit Forecast, by Geography 2019 & 2032

- Table 27: Blood Screening Industry in North America Revenue Million Forecast, by Country 2019 & 2032

- Table 28: Blood Screening Industry in North America Volume K Unit Forecast, by Country 2019 & 2032

- Table 29: Blood Screening Industry in North America Revenue Million Forecast, by Screening Tests 2019 & 2032

- Table 30: Blood Screening Industry in North America Volume K Unit Forecast, by Screening Tests 2019 & 2032

- Table 31: Blood Screening Industry in North America Revenue Million Forecast, by End User 2019 & 2032

- Table 32: Blood Screening Industry in North America Volume K Unit Forecast, by End User 2019 & 2032

- Table 33: Blood Screening Industry in North America Revenue Million Forecast, by Geography 2019 & 2032

- Table 34: Blood Screening Industry in North America Volume K Unit Forecast, by Geography 2019 & 2032

- Table 35: Blood Screening Industry in North America Revenue Million Forecast, by Country 2019 & 2032

- Table 36: Blood Screening Industry in North America Volume K Unit Forecast, by Country 2019 & 2032

- Table 37: Blood Screening Industry in North America Revenue Million Forecast, by Screening Tests 2019 & 2032

- Table 38: Blood Screening Industry in North America Volume K Unit Forecast, by Screening Tests 2019 & 2032

- Table 39: Blood Screening Industry in North America Revenue Million Forecast, by End User 2019 & 2032

- Table 40: Blood Screening Industry in North America Volume K Unit Forecast, by End User 2019 & 2032

- Table 41: Blood Screening Industry in North America Revenue Million Forecast, by Geography 2019 & 2032

- Table 42: Blood Screening Industry in North America Volume K Unit Forecast, by Geography 2019 & 2032

- Table 43: Blood Screening Industry in North America Revenue Million Forecast, by Country 2019 & 2032

- Table 44: Blood Screening Industry in North America Volume K Unit Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Blood Screening Industry in North America?

The projected CAGR is approximately 6.70%.

2. Which companies are prominent players in the Blood Screening Industry in North America?

Key companies in the market include Quidel Corporation, Novigenix SA, Abbott Laboratories, Siemens Healthineers AG, F Hoffmann-La Roche AG, Exact Sciences Corporation, Clinical Genomics Technologies Pty Ltd, EKF Diagnostics, MAINZ BIOMED N V , Sysmex Corporation, Epigenomics Inc, Hemosure Inc.

3. What are the main segments of the Blood Screening Industry in North America?

The market segments include Screening Tests, End User, Geography.

4. Can you provide details about the market size?

The market size is estimated to be USD 7.15 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Prevalence of Colorectal Cancer; Technological advancements and Increasing Cancer Prevention Initiatives.

6. What are the notable trends driving market growth?

Guaiac Fecal Occult Blood Test (gFOBT) is Expected to be Hold a Significant Market Share Over the Forecast Period.

7. Are there any restraints impacting market growth?

High Screening Tests Costs.

8. Can you provide examples of recent developments in the market?

December 2022: Guardant Health, Inc., a United States based Company, produced positive results from ECLIPSE (Evaluation of ctDNA LUNAR Assay In an Average Patient Screening Episode), an over 20,000 patient study for evaluating the performance of its blood test for detecting colorectal cancer (CRC) in average-risk adults.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Blood Screening Industry in North America," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Blood Screening Industry in North America report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Blood Screening Industry in North America?

To stay informed about further developments, trends, and reports in the Blood Screening Industry in North America, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence