Key Insights

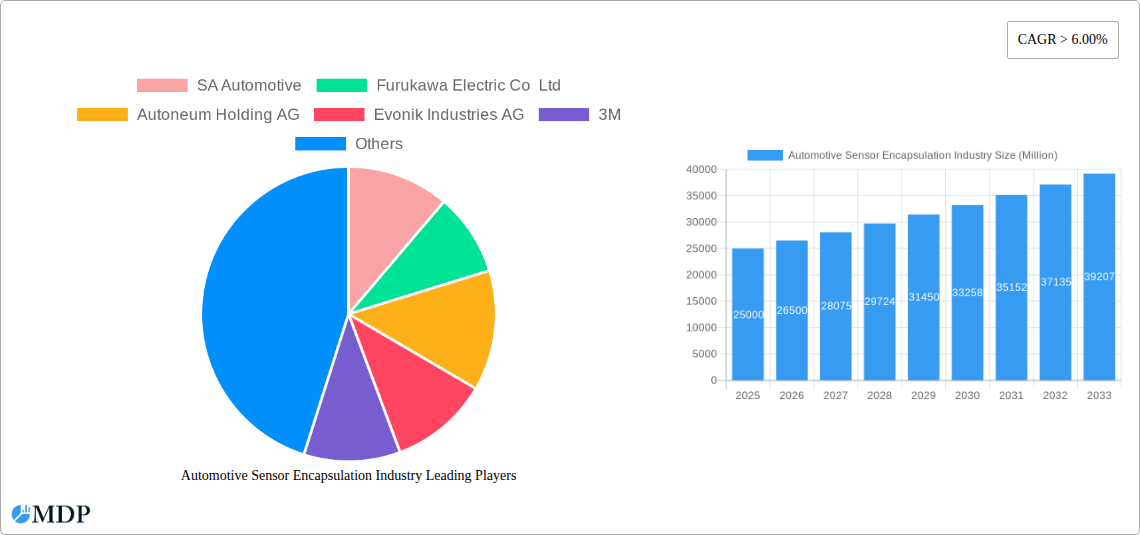

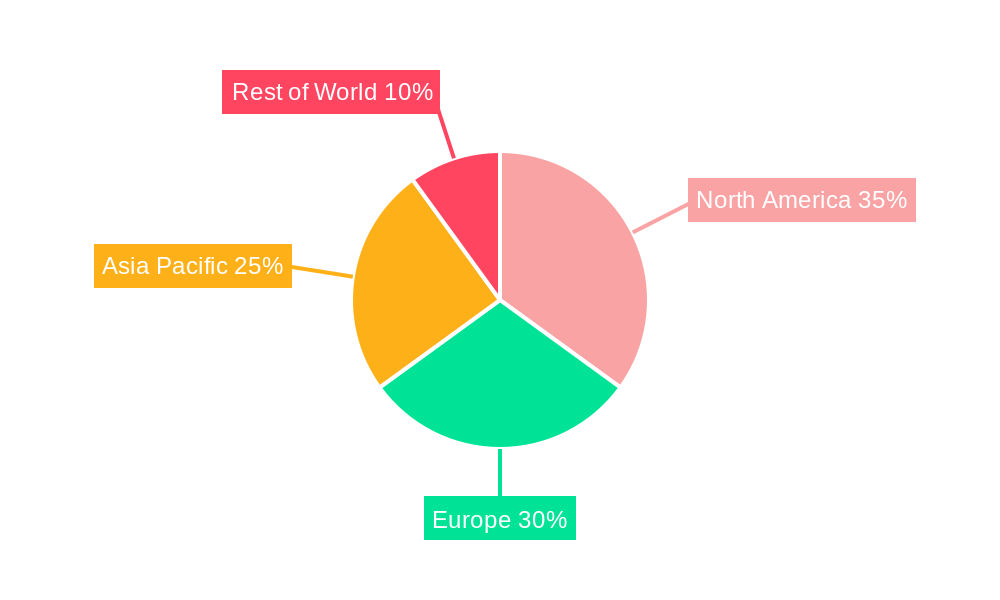

The automotive sensor encapsulation market is experiencing robust growth, driven by the increasing integration of advanced driver-assistance systems (ADAS) and the proliferation of electric vehicles (EVs). The market's expansion is fueled by the rising demand for enhanced vehicle safety and fuel efficiency. A Compound Annual Growth Rate (CAGR) exceeding 6% indicates significant market potential. Segmentation reveals a diverse landscape, with engine-mounted and body-mounted encapsulations leading the product type segment. Gasoline and diesel fuel types dominate the fuel type segment, while materials such as carbon fiber, polyurethane, polypropylene, and polyamide are commonly used, reflecting the industry's focus on lightweighting and durability. The geographical distribution of the market is widespread, with North America and Europe representing established markets, and the Asia-Pacific region experiencing rapid growth due to increasing vehicle production and technological advancements in countries like China and India. Key players like SA Automotive, Furukawa Electric, Autoneum, and others are actively competing in this market, continuously innovating to improve encapsulation technologies and cater to the evolving demands of the automotive industry.

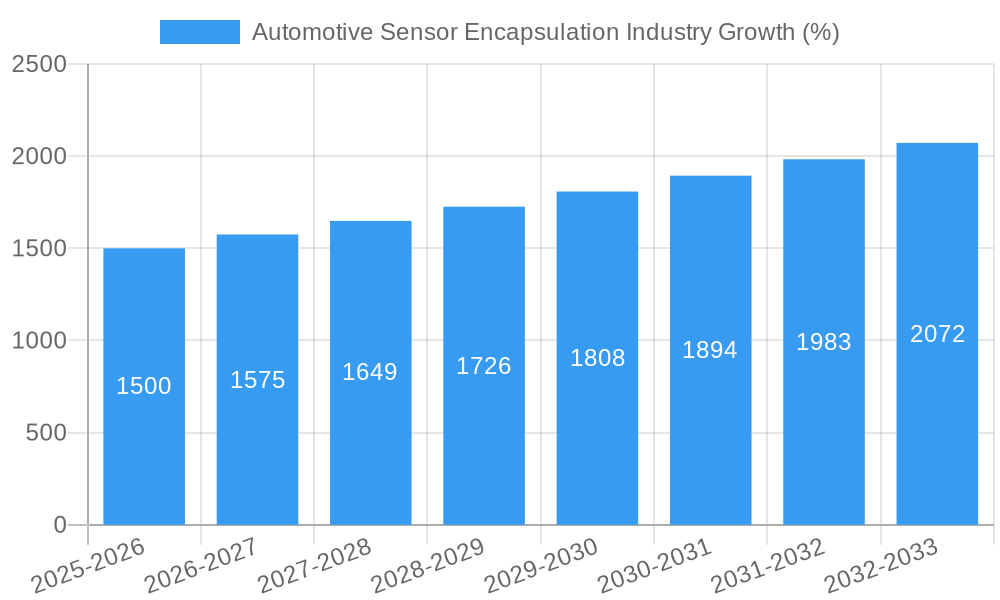

The market's growth trajectory is expected to remain positive throughout the forecast period (2025-2033), driven by continued technological advancements in sensor technology and the increasing demand for sophisticated automotive electronics. However, challenges remain. The cost of advanced materials and stringent regulatory compliance requirements pose potential restraints. The market will likely witness increased consolidation among key players, with mergers and acquisitions becoming more prevalent as companies strive to expand their product portfolios and geographic reach. Further growth will hinge upon the successful integration of new sensor technologies into vehicles, coupled with the development of cost-effective and durable encapsulation solutions that meet the diverse needs of various vehicle types. The focus on sustainability and environmentally friendly materials will also play a significant role in shaping future market trends.

Automotive Sensor Encapsulation Industry Market Report: 2019-2033

This comprehensive report provides a detailed analysis of the Automotive Sensor Encapsulation Industry, offering invaluable insights for stakeholders seeking to navigate this dynamic market. The study period covers 2019-2033, with a base year of 2025 and a forecast period of 2025-2033. We project a xx Million USD market value by 2033, exhibiting a CAGR of xx% during the forecast period. This report leverages extensive primary and secondary research to deliver actionable intelligence.

Automotive Sensor Encapsulation Industry Market Dynamics & Concentration

The Automotive Sensor Encapsulation market exhibits a moderately concentrated landscape, with key players like SA Automotive, 3M, and BASF SE holding significant market share. Market concentration is influenced by factors including economies of scale, technological expertise, and established distribution networks. Innovation in materials, particularly lightweight and high-performance polymers like Polyurethane and Polyamide, is a significant driver. Stringent automotive safety and emission regulations are pushing the adoption of advanced encapsulation techniques. Product substitution is limited, primarily driven by the pursuit of improved performance and cost-effectiveness. The increasing integration of sensors across vehicle platforms fuels market demand. M&A activity has been moderate in recent years, with approximately xx deals recorded between 2019 and 2024, driven largely by companies seeking to expand their product portfolios and geographical reach. Leading companies are focusing on strategic collaborations to access specialized technologies and enhance their market position. The global market share distribution among the top 5 players is estimated at approximately xx% in 2025.

Automotive Sensor Encapsulation Industry Industry Trends & Analysis

The Automotive Sensor Encapsulation market is witnessing robust growth, driven by the proliferation of Advanced Driver-Assistance Systems (ADAS) and the rise of autonomous vehicles. Technological advancements in sensor technology, miniaturization, and improved encapsulation materials are contributing to higher performance and reliability. Consumer demand for enhanced safety features and fuel efficiency is a significant market driver. The increasing adoption of electric vehicles (EVs) is also impacting the market, as EVs require a greater number of sensors compared to internal combustion engine (ICE) vehicles. The competitive landscape is marked by intense rivalry among established players and the emergence of new entrants specializing in niche technologies. Market penetration of advanced materials like carbon fiber is increasing gradually, while traditional materials like polyurethane maintain significant market share due to their cost-effectiveness and established manufacturing processes. The market is expected to maintain a healthy growth trajectory, driven by increasing vehicle production and the continuous adoption of advanced sensor technologies. This translates to a projected market value of xx Million USD by 2033, with a CAGR of xx% during the forecast period.

Leading Markets & Segments in Automotive Sensor Encapsulation Industry

The Asia-Pacific region currently dominates the Automotive Sensor Encapsulation market, driven by substantial automotive production, robust economic growth, and supportive government policies promoting vehicle electrification. Within this region, China holds the largest market share due to its massive automotive production base.

- Product Type: Engine-mounted sensors hold a larger market share compared to body-mounted sensors due to the critical nature of engine control systems.

- Fuel Type: Gasoline-powered vehicles currently account for a larger segment than diesel-powered vehicles, but the market share for diesel is expected to slightly increase given the regulatory trends in certain regions.

- Material Type: Polyurethane currently dominates due to its cost-effectiveness and suitable properties. However, the adoption of lightweight materials such as carbon fiber and polypropylene is steadily rising due to their performance advantages.

These segments are experiencing varying growth rates. For example, the demand for engine-mounted sensors in EVs is projected to grow at a faster rate than that for body-mounted sensors, while the utilization of carbon fiber is expected to increase significantly in the coming years because of increasing environmental concerns. Government initiatives promoting the use of lightweight materials and stringent emission regulations are influencing the adoption of different material types. Further, cost-effective and robust production processes of specific materials in certain geographical regions influence the overall material adoption in that region.

Automotive Sensor Encapsulation Industry Product Developments

Recent innovations include the development of highly durable, waterproof, and temperature-resistant encapsulation materials that enhance sensor reliability and longevity. Miniaturization of sensor packaging is also a significant trend, enabling better integration within vehicles and increased functionality. The integration of sensors with advanced communication protocols, such as CAN bus, is another key development. These product improvements enhance safety, reduce costs and improve fuel efficiency thus increasing market adoption.

Key Drivers of Automotive Sensor Encapsulation Industry Growth

Several factors drive market growth: the increasing integration of advanced driver-assistance systems (ADAS) and autonomous driving features in vehicles, stringent government regulations mandating improved vehicle safety and emissions, technological advancements resulting in higher-performing and cost-effective encapsulation materials, and the global expansion of the automotive industry, particularly in emerging economies.

Challenges in the Automotive Sensor Encapsulation Industry Market

Key challenges include the fluctuating cost of raw materials, intense competition among established players and new entrants, stringent industry regulations and quality standards, and complexities associated with the integration of sophisticated sensor systems into vehicles. Supply chain disruptions caused by global events can also significantly impact market stability. The combined effect of these challenges could lead to a xx% decrease in growth potential in specific regions within the forecast period.

Emerging Opportunities in Automotive Sensor Encapsulation Industry

The integration of sensors with 5G and IoT technologies presents significant opportunities. Expansion into niche automotive segments like commercial vehicles and off-highway vehicles offers potential for growth. Strategic partnerships between sensor manufacturers and automotive component suppliers will unlock synergistic opportunities for innovation and market expansion. The incorporation of more sustainable and recyclable materials also presents a growing avenue for product differentiation and environmental compliance.

Leading Players in the Automotive Sensor Encapsulation Industry Sector

- SA Automotive

- Furukawa Electric Co Ltd

- Autoneum Holding AG

- Evonik Industries AG

- 3M

- Roechling Group

- Woco Group

- BASF SE

- Continental AG

- Trocellen Automotive

- Compagnie de Saint-Gobain SA

- Adler Pelzer

- Erlingklinger AG

- Charlotte Baur Formschaumtechnik Gmb

Key Milestones in Automotive Sensor Encapsulation Industry Industry

- 2020: Increased focus on developing eco-friendly encapsulation materials.

- 2021: Several key players announced strategic partnerships to enhance their technological capabilities.

- 2022: Introduction of miniaturized sensor encapsulation solutions.

- 2023: Significant investments in R&D for improved sensor performance and reliability.

- 2024: Several mergers and acquisitions occurred, consolidating market share.

Strategic Outlook for Automotive Sensor Encapsulation Industry Market

The Automotive Sensor Encapsulation market is poised for sustained growth, driven by technological innovation, increasing vehicle electrification, and the expansion of ADAS and autonomous driving technologies. Strategic investments in R&D, strategic partnerships, and expansion into new markets are crucial for capturing significant market share. Companies should focus on developing sustainable and cost-effective encapsulation solutions to cater to the growing demand while maintaining a strong competitive position. The long-term outlook is positive, with continuous technological advancement and growing regulatory pressure further fueling market growth.

Automotive Sensor Encapsulation Industry Segmentation

-

1. Product Type

- 1.1. Engine Mounted

- 1.2. Body Mounted

-

2. Fuel Type

- 2.1. Gasoline

- 2.2. Diesel

-

3. Material Type

- 3.1. Carbon Fiber

- 3.2. Polyurethane

- 3.3. Polypropylene

- 3.4. Polyamide

- 3.5. Glasswool

Automotive Sensor Encapsulation Industry Segmentation By Geography

-

1. North America

- 1.1. US

- 1.2. Canada

- 1.3. Rest of North America

-

2. Europe

- 2.1. Germany

- 2.2. UK

- 2.3. France

- 2.4. Italy

- 2.5. Rest of Europe

-

3. Asia Pacific

- 3.1. India

- 3.2. China

- 3.3. Japan

- 3.4. South Korea

- 3.5. Rest of Asia Pacific

-

4. Rest of the World

- 4.1. Latin America

- 4.2. Middle East and Africa

Automotive Sensor Encapsulation Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of > 6.00% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increased Safety Awareness is Driving the Market Growth

- 3.3. Market Restrains

- 3.3.1. Cybersecurity Concerns is Anticipated to Restrain the Market Growth

- 3.4. Market Trends

- 3.4.1. Stringent Government Regulations to Drive Market Growth

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Automotive Sensor Encapsulation Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Engine Mounted

- 5.1.2. Body Mounted

- 5.2. Market Analysis, Insights and Forecast - by Fuel Type

- 5.2.1. Gasoline

- 5.2.2. Diesel

- 5.3. Market Analysis, Insights and Forecast - by Material Type

- 5.3.1. Carbon Fiber

- 5.3.2. Polyurethane

- 5.3.3. Polypropylene

- 5.3.4. Polyamide

- 5.3.5. Glasswool

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. North America Automotive Sensor Encapsulation Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 6.1.1. Engine Mounted

- 6.1.2. Body Mounted

- 6.2. Market Analysis, Insights and Forecast - by Fuel Type

- 6.2.1. Gasoline

- 6.2.2. Diesel

- 6.3. Market Analysis, Insights and Forecast - by Material Type

- 6.3.1. Carbon Fiber

- 6.3.2. Polyurethane

- 6.3.3. Polypropylene

- 6.3.4. Polyamide

- 6.3.5. Glasswool

- 6.1. Market Analysis, Insights and Forecast - by Product Type

- 7. Europe Automotive Sensor Encapsulation Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 7.1.1. Engine Mounted

- 7.1.2. Body Mounted

- 7.2. Market Analysis, Insights and Forecast - by Fuel Type

- 7.2.1. Gasoline

- 7.2.2. Diesel

- 7.3. Market Analysis, Insights and Forecast - by Material Type

- 7.3.1. Carbon Fiber

- 7.3.2. Polyurethane

- 7.3.3. Polypropylene

- 7.3.4. Polyamide

- 7.3.5. Glasswool

- 7.1. Market Analysis, Insights and Forecast - by Product Type

- 8. Asia Pacific Automotive Sensor Encapsulation Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 8.1.1. Engine Mounted

- 8.1.2. Body Mounted

- 8.2. Market Analysis, Insights and Forecast - by Fuel Type

- 8.2.1. Gasoline

- 8.2.2. Diesel

- 8.3. Market Analysis, Insights and Forecast - by Material Type

- 8.3.1. Carbon Fiber

- 8.3.2. Polyurethane

- 8.3.3. Polypropylene

- 8.3.4. Polyamide

- 8.3.5. Glasswool

- 8.1. Market Analysis, Insights and Forecast - by Product Type

- 9. Rest of the World Automotive Sensor Encapsulation Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 9.1.1. Engine Mounted

- 9.1.2. Body Mounted

- 9.2. Market Analysis, Insights and Forecast - by Fuel Type

- 9.2.1. Gasoline

- 9.2.2. Diesel

- 9.3. Market Analysis, Insights and Forecast - by Material Type

- 9.3.1. Carbon Fiber

- 9.3.2. Polyurethane

- 9.3.3. Polypropylene

- 9.3.4. Polyamide

- 9.3.5. Glasswool

- 9.1. Market Analysis, Insights and Forecast - by Product Type

- 10. North America Automotive Sensor Encapsulation Industry Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 10.1.1 US

- 10.1.2 Canada

- 10.1.3 Rest of North America

- 11. Europe Automotive Sensor Encapsulation Industry Analysis, Insights and Forecast, 2019-2031

- 11.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 11.1.1 Germany

- 11.1.2 UK

- 11.1.3 France

- 11.1.4 Italy

- 11.1.5 Rest of Europe

- 12. Asia Pacific Automotive Sensor Encapsulation Industry Analysis, Insights and Forecast, 2019-2031

- 12.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 12.1.1 India

- 12.1.2 China

- 12.1.3 Japan

- 12.1.4 South Korea

- 12.1.5 Rest of Asia Pacific

- 13. Rest of the World Automotive Sensor Encapsulation Industry Analysis, Insights and Forecast, 2019-2031

- 13.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 13.1.1 Latin America

- 13.1.2 Middle East and Africa

- 14. Competitive Analysis

- 14.1. Global Market Share Analysis 2024

- 14.2. Company Profiles

- 14.2.1 SA Automotive

- 14.2.1.1. Overview

- 14.2.1.2. Products

- 14.2.1.3. SWOT Analysis

- 14.2.1.4. Recent Developments

- 14.2.1.5. Financials (Based on Availability)

- 14.2.2 Furukawa Electric Co Ltd

- 14.2.2.1. Overview

- 14.2.2.2. Products

- 14.2.2.3. SWOT Analysis

- 14.2.2.4. Recent Developments

- 14.2.2.5. Financials (Based on Availability)

- 14.2.3 Autoneum Holding AG

- 14.2.3.1. Overview

- 14.2.3.2. Products

- 14.2.3.3. SWOT Analysis

- 14.2.3.4. Recent Developments

- 14.2.3.5. Financials (Based on Availability)

- 14.2.4 Evonik Industries AG

- 14.2.4.1. Overview

- 14.2.4.2. Products

- 14.2.4.3. SWOT Analysis

- 14.2.4.4. Recent Developments

- 14.2.4.5. Financials (Based on Availability)

- 14.2.5 3M

- 14.2.5.1. Overview

- 14.2.5.2. Products

- 14.2.5.3. SWOT Analysis

- 14.2.5.4. Recent Developments

- 14.2.5.5. Financials (Based on Availability)

- 14.2.6 Roechling Group

- 14.2.6.1. Overview

- 14.2.6.2. Products

- 14.2.6.3. SWOT Analysis

- 14.2.6.4. Recent Developments

- 14.2.6.5. Financials (Based on Availability)

- 14.2.7 Woco Group

- 14.2.7.1. Overview

- 14.2.7.2. Products

- 14.2.7.3. SWOT Analysis

- 14.2.7.4. Recent Developments

- 14.2.7.5. Financials (Based on Availability)

- 14.2.8 BASF SE

- 14.2.8.1. Overview

- 14.2.8.2. Products

- 14.2.8.3. SWOT Analysis

- 14.2.8.4. Recent Developments

- 14.2.8.5. Financials (Based on Availability)

- 14.2.9 Continental AG

- 14.2.9.1. Overview

- 14.2.9.2. Products

- 14.2.9.3. SWOT Analysis

- 14.2.9.4. Recent Developments

- 14.2.9.5. Financials (Based on Availability)

- 14.2.10 Trocellen Automotive

- 14.2.10.1. Overview

- 14.2.10.2. Products

- 14.2.10.3. SWOT Analysis

- 14.2.10.4. Recent Developments

- 14.2.10.5. Financials (Based on Availability)

- 14.2.11 Compagnie de Saint-Gobain SA

- 14.2.11.1. Overview

- 14.2.11.2. Products

- 14.2.11.3. SWOT Analysis

- 14.2.11.4. Recent Developments

- 14.2.11.5. Financials (Based on Availability)

- 14.2.12 Adler Pelzer

- 14.2.12.1. Overview

- 14.2.12.2. Products

- 14.2.12.3. SWOT Analysis

- 14.2.12.4. Recent Developments

- 14.2.12.5. Financials (Based on Availability)

- 14.2.13 Erlingklinger AG

- 14.2.13.1. Overview

- 14.2.13.2. Products

- 14.2.13.3. SWOT Analysis

- 14.2.13.4. Recent Developments

- 14.2.13.5. Financials (Based on Availability)

- 14.2.14 Charlotte Baur Formschaumtechnik Gmb

- 14.2.14.1. Overview

- 14.2.14.2. Products

- 14.2.14.3. SWOT Analysis

- 14.2.14.4. Recent Developments

- 14.2.14.5. Financials (Based on Availability)

- 14.2.1 SA Automotive

List of Figures

- Figure 1: Global Automotive Sensor Encapsulation Industry Revenue Breakdown (Million, %) by Region 2024 & 2032

- Figure 2: North America Automotive Sensor Encapsulation Industry Revenue (Million), by Country 2024 & 2032

- Figure 3: North America Automotive Sensor Encapsulation Industry Revenue Share (%), by Country 2024 & 2032

- Figure 4: Europe Automotive Sensor Encapsulation Industry Revenue (Million), by Country 2024 & 2032

- Figure 5: Europe Automotive Sensor Encapsulation Industry Revenue Share (%), by Country 2024 & 2032

- Figure 6: Asia Pacific Automotive Sensor Encapsulation Industry Revenue (Million), by Country 2024 & 2032

- Figure 7: Asia Pacific Automotive Sensor Encapsulation Industry Revenue Share (%), by Country 2024 & 2032

- Figure 8: Rest of the World Automotive Sensor Encapsulation Industry Revenue (Million), by Country 2024 & 2032

- Figure 9: Rest of the World Automotive Sensor Encapsulation Industry Revenue Share (%), by Country 2024 & 2032

- Figure 10: North America Automotive Sensor Encapsulation Industry Revenue (Million), by Product Type 2024 & 2032

- Figure 11: North America Automotive Sensor Encapsulation Industry Revenue Share (%), by Product Type 2024 & 2032

- Figure 12: North America Automotive Sensor Encapsulation Industry Revenue (Million), by Fuel Type 2024 & 2032

- Figure 13: North America Automotive Sensor Encapsulation Industry Revenue Share (%), by Fuel Type 2024 & 2032

- Figure 14: North America Automotive Sensor Encapsulation Industry Revenue (Million), by Material Type 2024 & 2032

- Figure 15: North America Automotive Sensor Encapsulation Industry Revenue Share (%), by Material Type 2024 & 2032

- Figure 16: North America Automotive Sensor Encapsulation Industry Revenue (Million), by Country 2024 & 2032

- Figure 17: North America Automotive Sensor Encapsulation Industry Revenue Share (%), by Country 2024 & 2032

- Figure 18: Europe Automotive Sensor Encapsulation Industry Revenue (Million), by Product Type 2024 & 2032

- Figure 19: Europe Automotive Sensor Encapsulation Industry Revenue Share (%), by Product Type 2024 & 2032

- Figure 20: Europe Automotive Sensor Encapsulation Industry Revenue (Million), by Fuel Type 2024 & 2032

- Figure 21: Europe Automotive Sensor Encapsulation Industry Revenue Share (%), by Fuel Type 2024 & 2032

- Figure 22: Europe Automotive Sensor Encapsulation Industry Revenue (Million), by Material Type 2024 & 2032

- Figure 23: Europe Automotive Sensor Encapsulation Industry Revenue Share (%), by Material Type 2024 & 2032

- Figure 24: Europe Automotive Sensor Encapsulation Industry Revenue (Million), by Country 2024 & 2032

- Figure 25: Europe Automotive Sensor Encapsulation Industry Revenue Share (%), by Country 2024 & 2032

- Figure 26: Asia Pacific Automotive Sensor Encapsulation Industry Revenue (Million), by Product Type 2024 & 2032

- Figure 27: Asia Pacific Automotive Sensor Encapsulation Industry Revenue Share (%), by Product Type 2024 & 2032

- Figure 28: Asia Pacific Automotive Sensor Encapsulation Industry Revenue (Million), by Fuel Type 2024 & 2032

- Figure 29: Asia Pacific Automotive Sensor Encapsulation Industry Revenue Share (%), by Fuel Type 2024 & 2032

- Figure 30: Asia Pacific Automotive Sensor Encapsulation Industry Revenue (Million), by Material Type 2024 & 2032

- Figure 31: Asia Pacific Automotive Sensor Encapsulation Industry Revenue Share (%), by Material Type 2024 & 2032

- Figure 32: Asia Pacific Automotive Sensor Encapsulation Industry Revenue (Million), by Country 2024 & 2032

- Figure 33: Asia Pacific Automotive Sensor Encapsulation Industry Revenue Share (%), by Country 2024 & 2032

- Figure 34: Rest of the World Automotive Sensor Encapsulation Industry Revenue (Million), by Product Type 2024 & 2032

- Figure 35: Rest of the World Automotive Sensor Encapsulation Industry Revenue Share (%), by Product Type 2024 & 2032

- Figure 36: Rest of the World Automotive Sensor Encapsulation Industry Revenue (Million), by Fuel Type 2024 & 2032

- Figure 37: Rest of the World Automotive Sensor Encapsulation Industry Revenue Share (%), by Fuel Type 2024 & 2032

- Figure 38: Rest of the World Automotive Sensor Encapsulation Industry Revenue (Million), by Material Type 2024 & 2032

- Figure 39: Rest of the World Automotive Sensor Encapsulation Industry Revenue Share (%), by Material Type 2024 & 2032

- Figure 40: Rest of the World Automotive Sensor Encapsulation Industry Revenue (Million), by Country 2024 & 2032

- Figure 41: Rest of the World Automotive Sensor Encapsulation Industry Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Automotive Sensor Encapsulation Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Global Automotive Sensor Encapsulation Industry Revenue Million Forecast, by Product Type 2019 & 2032

- Table 3: Global Automotive Sensor Encapsulation Industry Revenue Million Forecast, by Fuel Type 2019 & 2032

- Table 4: Global Automotive Sensor Encapsulation Industry Revenue Million Forecast, by Material Type 2019 & 2032

- Table 5: Global Automotive Sensor Encapsulation Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 6: Global Automotive Sensor Encapsulation Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 7: US Automotive Sensor Encapsulation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Canada Automotive Sensor Encapsulation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Rest of North America Automotive Sensor Encapsulation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Global Automotive Sensor Encapsulation Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 11: Germany Automotive Sensor Encapsulation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: UK Automotive Sensor Encapsulation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: France Automotive Sensor Encapsulation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Italy Automotive Sensor Encapsulation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 15: Rest of Europe Automotive Sensor Encapsulation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: Global Automotive Sensor Encapsulation Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 17: India Automotive Sensor Encapsulation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: China Automotive Sensor Encapsulation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: Japan Automotive Sensor Encapsulation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: South Korea Automotive Sensor Encapsulation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 21: Rest of Asia Pacific Automotive Sensor Encapsulation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: Global Automotive Sensor Encapsulation Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 23: Latin America Automotive Sensor Encapsulation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: Middle East and Africa Automotive Sensor Encapsulation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 25: Global Automotive Sensor Encapsulation Industry Revenue Million Forecast, by Product Type 2019 & 2032

- Table 26: Global Automotive Sensor Encapsulation Industry Revenue Million Forecast, by Fuel Type 2019 & 2032

- Table 27: Global Automotive Sensor Encapsulation Industry Revenue Million Forecast, by Material Type 2019 & 2032

- Table 28: Global Automotive Sensor Encapsulation Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 29: US Automotive Sensor Encapsulation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 30: Canada Automotive Sensor Encapsulation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 31: Rest of North America Automotive Sensor Encapsulation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 32: Global Automotive Sensor Encapsulation Industry Revenue Million Forecast, by Product Type 2019 & 2032

- Table 33: Global Automotive Sensor Encapsulation Industry Revenue Million Forecast, by Fuel Type 2019 & 2032

- Table 34: Global Automotive Sensor Encapsulation Industry Revenue Million Forecast, by Material Type 2019 & 2032

- Table 35: Global Automotive Sensor Encapsulation Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 36: Germany Automotive Sensor Encapsulation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 37: UK Automotive Sensor Encapsulation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 38: France Automotive Sensor Encapsulation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 39: Italy Automotive Sensor Encapsulation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 40: Rest of Europe Automotive Sensor Encapsulation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 41: Global Automotive Sensor Encapsulation Industry Revenue Million Forecast, by Product Type 2019 & 2032

- Table 42: Global Automotive Sensor Encapsulation Industry Revenue Million Forecast, by Fuel Type 2019 & 2032

- Table 43: Global Automotive Sensor Encapsulation Industry Revenue Million Forecast, by Material Type 2019 & 2032

- Table 44: Global Automotive Sensor Encapsulation Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 45: India Automotive Sensor Encapsulation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 46: China Automotive Sensor Encapsulation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 47: Japan Automotive Sensor Encapsulation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 48: South Korea Automotive Sensor Encapsulation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 49: Rest of Asia Pacific Automotive Sensor Encapsulation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 50: Global Automotive Sensor Encapsulation Industry Revenue Million Forecast, by Product Type 2019 & 2032

- Table 51: Global Automotive Sensor Encapsulation Industry Revenue Million Forecast, by Fuel Type 2019 & 2032

- Table 52: Global Automotive Sensor Encapsulation Industry Revenue Million Forecast, by Material Type 2019 & 2032

- Table 53: Global Automotive Sensor Encapsulation Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 54: Latin America Automotive Sensor Encapsulation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 55: Middle East and Africa Automotive Sensor Encapsulation Industry Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Sensor Encapsulation Industry?

The projected CAGR is approximately > 6.00%.

2. Which companies are prominent players in the Automotive Sensor Encapsulation Industry?

Key companies in the market include SA Automotive, Furukawa Electric Co Ltd, Autoneum Holding AG, Evonik Industries AG, 3M, Roechling Group, Woco Group, BASF SE, Continental AG, Trocellen Automotive, Compagnie de Saint-Gobain SA, Adler Pelzer, Erlingklinger AG, Charlotte Baur Formschaumtechnik Gmb.

3. What are the main segments of the Automotive Sensor Encapsulation Industry?

The market segments include Product Type, Fuel Type, Material Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Increased Safety Awareness is Driving the Market Growth.

6. What are the notable trends driving market growth?

Stringent Government Regulations to Drive Market Growth.

7. Are there any restraints impacting market growth?

Cybersecurity Concerns is Anticipated to Restrain the Market Growth.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automotive Sensor Encapsulation Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automotive Sensor Encapsulation Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automotive Sensor Encapsulation Industry?

To stay informed about further developments, trends, and reports in the Automotive Sensor Encapsulation Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence