Key Insights

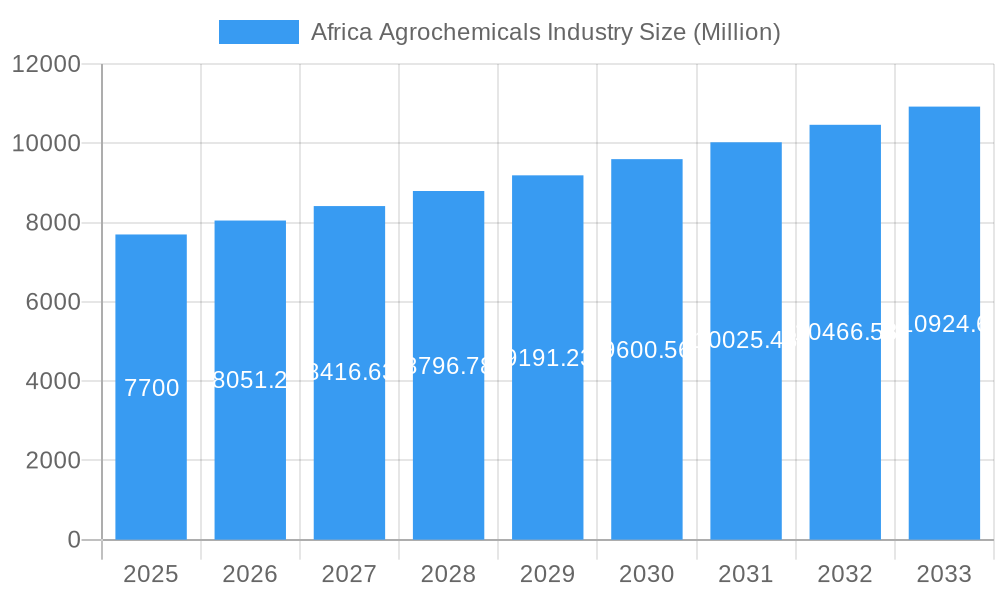

The Africa agrochemicals market, valued at $7.70 billion in 2025, is projected to experience robust growth, driven by factors such as rising agricultural production to meet food security needs of a rapidly growing population, increasing adoption of modern farming techniques, and government initiatives promoting agricultural development across the continent. The market's Compound Annual Growth Rate (CAGR) of 4.60% from 2025 to 2033 indicates a significant expansion. Key segments contributing to this growth include fertilizers, pesticides, and plant growth regulators, with grains and cereals, pulses and oilseeds, and fruits and vegetables representing major application areas. Growth is particularly strong in regions with expanding agricultural land and investment in irrigation, such as East Africa (Kenya, Tanzania, Uganda). However, challenges remain, including limited access to advanced agricultural technologies in certain regions, climate change impacting crop yields, and concerns regarding the environmental impact of agrochemical use, necessitating a focus on sustainable and responsible agricultural practices. Major players like Sumitomo, Syngenta, Bayer, BASF, and Corteva are actively investing in the region, expanding their product portfolios and distribution networks to capitalize on the market’s potential. This competitive landscape fosters innovation and drives the development of more efficient and environmentally friendly agrochemical solutions.

Africa Agrochemicals Industry Market Size (In Billion)

The market segmentation reveals varied growth trajectories across product types and applications. The fertilizer market is expected to dominate due to the high demand for improved soil fertility, while the pesticides market is anticipated to see substantial growth owing to the increasing prevalence of crop pests and diseases. The adoption of plant growth regulators is likely to accelerate as farmers increasingly seek to enhance crop yields and quality. Geographically, countries like South Africa, with its relatively advanced agricultural sector, and Kenya, with its expanding horticultural industry, are major contributors to market growth. However, untapped potential exists in other African nations, presenting opportunities for market expansion through improved infrastructure, farmer education, and access to credit. The long-term outlook for the African agrochemicals market is optimistic, contingent upon sustained investment, policy support, and the adoption of environmentally sustainable practices.

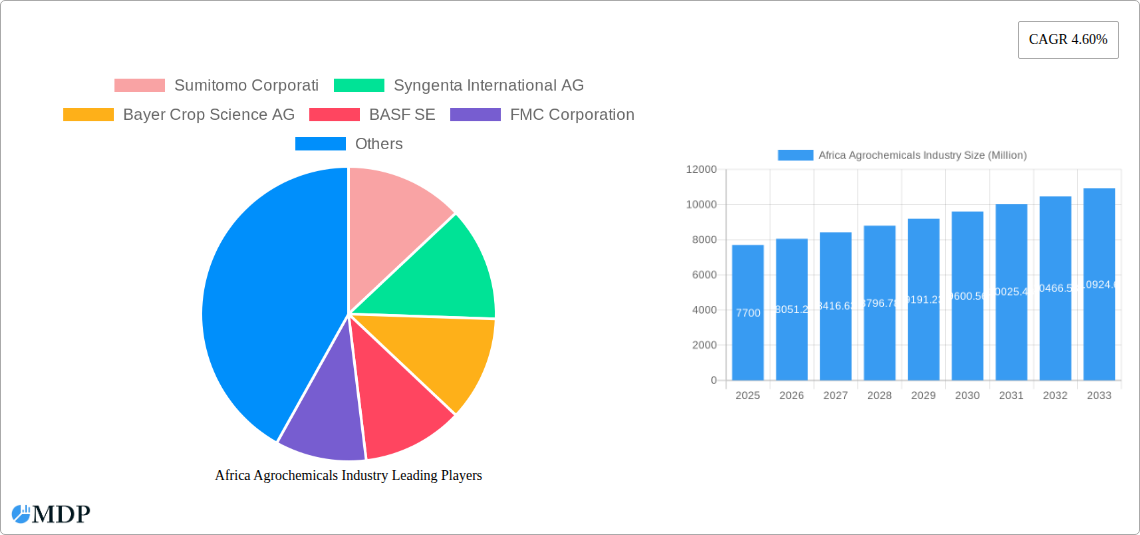

Africa Agrochemicals Industry Company Market Share

Africa Agrochemicals Industry: A Comprehensive Market Report (2019-2033)

This comprehensive report provides an in-depth analysis of the Africa agrochemicals industry, offering valuable insights for stakeholders across the value chain. Covering the period 2019-2033, with a focus on 2025, this report unveils market dynamics, trends, leading players, and future growth opportunities. Maximize your understanding of this dynamic market and make informed strategic decisions.

Africa Agrochemicals Industry Market Dynamics & Concentration

The African agrochemicals market is characterized by moderate concentration, with several multinational corporations holding significant market share. While precise figures for market share are difficult to obtain due to data limitations, estimates suggest that companies like Sumitomo Corporation, Syngenta International AG, Bayer Crop Science AG, BASF SE, FMC Corporation, Corteva Agrisciences, UPL, Yara International, Nufar, and Adama Agricultural Solutions collectively account for a significant portion (estimated at xx%) of the total market.

Innovation is a key driver, with companies investing heavily in developing new formulations to address specific pest and disease challenges in the region. Regulatory frameworks vary across African nations, posing both challenges and opportunities. The presence of bio-pesticides and other sustainable alternatives is increasing, presenting competitive pressures. End-user trends reveal a growing demand for high-yielding, disease-resistant crop varieties which fuels demand for advanced agrochemicals. The market has witnessed a moderate number of M&A activities (xx deals) in the historical period (2019-2024), primarily focused on expanding product portfolios and geographical reach.

Africa Agrochemicals Industry Industry Trends & Analysis

The African agrochemicals market exhibits robust growth, driven by factors such as rising agricultural output, increasing adoption of modern farming techniques, and government initiatives aimed at boosting food security. The market is projected to experience a Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025-2033). Technological disruptions, such as the increased use of precision agriculture and digital tools, are reshaping the landscape, improving efficiency, and reducing chemical usage. Consumer preferences are shifting towards sustainable and environmentally friendly products, creating opportunities for bio-pesticides and other eco-friendly solutions. Competitive dynamics are intense, with both multinational and regional players vying for market share. Market penetration remains relatively low compared to global averages, indicating substantial growth potential. Increased access to credit and improved infrastructure is also a major driver, contributing to increased adoption of advanced crop management practices.

Leading Markets & Segments in Africa Agrochemicals Industry

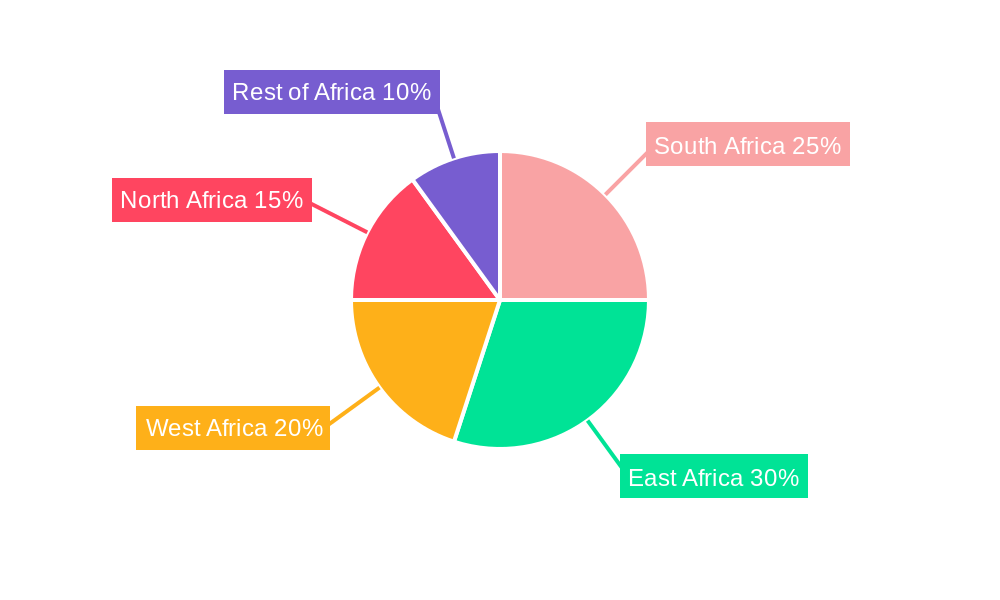

While data limitations make precise identification of the single dominant market challenging, the analysis suggests a substantial market across several regions. Key markets are showing growth in regions like East Africa (Kenya, Ethiopia, Tanzania), Southern Africa (South Africa) and West Africa (Nigeria, Ghana). The Pesticides Market holds the largest share within the product type segment (estimated at xx Million), reflecting the prevalence of pest and disease pressure on crops. Within applications, the Grains and Cereals segment demonstrates consistent dominance.

Key Drivers for Grains and Cereals dominance: Large cultivated area, high demand, and government support for staple crop production.

Key Drivers for Pesticides Market dominance: Growing awareness of pest and disease management, increased crop yields, and the efficacy of chemical pesticides.

South Africa's Dominance: South Africa stands out as the leading national market due to its advanced agricultural sector, strong infrastructure, and favorable regulatory environment. Other major markets include Nigeria, Kenya and Ethiopia.

Other significant segments include Pulses and Oilseeds, driven by rising demand for dietary protein and vegetable oils. Fruits and Vegetables show significant growth potential, linked to increasing urbanization and changing consumer preferences. The Commercial Crops segment is also experiencing growth, particularly for export-oriented commodities like coffee and tea.

Africa Agrochemicals Industry Product Developments

Recent years have witnessed significant advancements in agrochemical product development, focusing on improved efficacy, reduced environmental impact, and enhanced crop protection solutions. Companies are emphasizing the development of biological pesticides and integrated pest management solutions. The integration of digital technologies, such as precision spraying and remote sensing, is transforming application methods, leading to more targeted and efficient pesticide use. This focus on innovative products provides both cost savings and improved yields for farmers.

Key Drivers of Africa Agrochemicals Industry Growth

Several factors contribute to the growth of the African agrochemicals market. Technological advancements, including the introduction of precision agriculture tools and data-driven decision-making, significantly improve efficiency and yield. Economic growth and rising disposable incomes boost farmers’ investment in improved crop management practices. Government policies aimed at boosting agricultural production, including subsidies and extension services, significantly support market expansion. Furthermore, the increasing adoption of high-yielding crop varieties necessitates the use of tailored agrochemical solutions, driving market growth.

Challenges in the Africa Agrochemicals Industry Market

The African agrochemicals market faces several challenges. Regulatory hurdles and varying standards across different nations complicate product registration and market access. Supply chain constraints, including infrastructure limitations and logistical bottlenecks, impact product availability and affordability. The competitiveness of the market, with both multinational and local players, puts pressure on pricing and profitability. Furthermore, concerns about environmental impact and the potential health risks associated with certain agrochemicals pose significant barriers. These challenges result in an estimated xx Million loss in revenue annually.

Emerging Opportunities in Africa Agrochemicals Industry

The long-term growth potential of the African agrochemicals market is considerable. Technological breakthroughs, particularly in biopesticides and precision agriculture, present significant opportunities for innovation and expansion. Strategic partnerships between multinational companies and local distributors can enhance market access and product distribution. Market expansion strategies, focusing on untapped regions and underserved farming communities, create significant growth opportunities. This expansion is predicted to add xx Million to the market value by 2033.

Leading Players in the Africa Agrochemicals Industry Sector

- Sumitomo Corporation

- Syngenta International AG

- Bayer Crop Science AG

- BASF SE

- FMC Corporation

- Corteva Agrisciences

- UPL

- Yara International

- Nufar

- Adama Agricultural Solutions

Key Milestones in Africa Agrochemicals Industry Industry

- March 2022: Corteva Agrisciences launched Aubaine 518 SC herbicide in South Africa, addressing a specific weed control need in wheat farming.

- February 2022: Bayer launched Flipper and Serenade, expanding its organic crop protection offerings.

- February 2022: Bayer and Kimitec partnered to develop and commercialize biological crop protection products, signifying a shift towards sustainable solutions.

- January 2023: Bayer partnered with M2i Group to integrate pheromone-based technology into its crop protection products, enhancing digital capabilities.

Strategic Outlook for Africa Agrochemicals Industry Market

The future of the African agrochemicals market is promising, driven by increasing demand for food security, supportive government policies, and technological advancements. Strategic opportunities lie in investing in sustainable and environmentally friendly solutions, expanding into underserved markets, and leveraging digital technologies to enhance efficiency. The market's growth trajectory is expected to continue, presenting lucrative opportunities for both established and emerging players to capture significant market share. By 2033, the market is projected to reach xx Million, representing substantial growth potential.

Africa Agrochemicals Industry Segmentation

- 1. Production Analysis

- 2. Consumption Analysis

- 3. Import Market Analysis (Value & Volume)

- 4. Export Market Analysis (Value & Volume)

- 5. Price Trend Analysis

Africa Agrochemicals Industry Segmentation By Geography

-

1. Africa

- 1.1. Nigeria

- 1.2. South Africa

- 1.3. Egypt

- 1.4. Kenya

- 1.5. Ethiopia

- 1.6. Morocco

- 1.7. Ghana

- 1.8. Algeria

- 1.9. Tanzania

- 1.10. Ivory Coast

Africa Agrochemicals Industry Regional Market Share

Geographic Coverage of Africa Agrochemicals Industry

Africa Agrochemicals Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.60% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Adoption of Organic and Eco-friendly Farming Practices; Declining Area of Arable Land and Rising Food Security Concerns

- 3.3. Market Restrains

- 3.3.1. High Demand for Conventional and Synthetic Products; Lack of Awareness and Other Factors Limiting the Adoption of Agricultural Inoculants

- 3.4. Market Trends

- 3.4.1. Growing Food Demand Due to High Population Growth

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Africa Agrochemicals Industry Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Production Analysis

- 5.2. Market Analysis, Insights and Forecast - by Consumption Analysis

- 5.3. Market Analysis, Insights and Forecast - by Import Market Analysis (Value & Volume)

- 5.4. Market Analysis, Insights and Forecast - by Export Market Analysis (Value & Volume)

- 5.5. Market Analysis, Insights and Forecast - by Price Trend Analysis

- 5.6. Market Analysis, Insights and Forecast - by Region

- 5.6.1. Africa

- 5.1. Market Analysis, Insights and Forecast - by Production Analysis

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2025

- 6.2. Company Profiles

- 6.2.1 Sumitomo Corporati

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Syngenta International AG

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Bayer Crop Science AG

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 BASF SE

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 FMC Corporation

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Corteva Agrisciences

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 UPL

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Yara International

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Nufar

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 Adama Agricultural Solutions

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.1 Sumitomo Corporati

List of Figures

- Figure 1: Africa Agrochemicals Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Africa Agrochemicals Industry Share (%) by Company 2025

List of Tables

- Table 1: Africa Agrochemicals Industry Revenue Million Forecast, by Production Analysis 2020 & 2033

- Table 2: Africa Agrochemicals Industry Revenue Million Forecast, by Consumption Analysis 2020 & 2033

- Table 3: Africa Agrochemicals Industry Revenue Million Forecast, by Import Market Analysis (Value & Volume) 2020 & 2033

- Table 4: Africa Agrochemicals Industry Revenue Million Forecast, by Export Market Analysis (Value & Volume) 2020 & 2033

- Table 5: Africa Agrochemicals Industry Revenue Million Forecast, by Price Trend Analysis 2020 & 2033

- Table 6: Africa Agrochemicals Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 7: Africa Agrochemicals Industry Revenue Million Forecast, by Production Analysis 2020 & 2033

- Table 8: Africa Agrochemicals Industry Revenue Million Forecast, by Consumption Analysis 2020 & 2033

- Table 9: Africa Agrochemicals Industry Revenue Million Forecast, by Import Market Analysis (Value & Volume) 2020 & 2033

- Table 10: Africa Agrochemicals Industry Revenue Million Forecast, by Export Market Analysis (Value & Volume) 2020 & 2033

- Table 11: Africa Agrochemicals Industry Revenue Million Forecast, by Price Trend Analysis 2020 & 2033

- Table 12: Africa Agrochemicals Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: Nigeria Africa Agrochemicals Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: South Africa Africa Agrochemicals Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: Egypt Africa Agrochemicals Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Kenya Africa Agrochemicals Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: Ethiopia Africa Agrochemicals Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Morocco Africa Agrochemicals Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: Ghana Africa Agrochemicals Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Algeria Africa Agrochemicals Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: Tanzania Africa Agrochemicals Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Ivory Coast Africa Agrochemicals Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Africa Agrochemicals Industry?

The projected CAGR is approximately 4.60%.

2. Which companies are prominent players in the Africa Agrochemicals Industry?

Key companies in the market include Sumitomo Corporati, Syngenta International AG, Bayer Crop Science AG, BASF SE, FMC Corporation, Corteva Agrisciences, UPL, Yara International, Nufar, Adama Agricultural Solutions.

3. What are the main segments of the Africa Agrochemicals Industry?

The market segments include Production Analysis, Consumption Analysis, Import Market Analysis (Value & Volume), Export Market Analysis (Value & Volume), Price Trend Analysis.

4. Can you provide details about the market size?

The market size is estimated to be USD 7.70 Million as of 2022.

5. What are some drivers contributing to market growth?

Adoption of Organic and Eco-friendly Farming Practices; Declining Area of Arable Land and Rising Food Security Concerns.

6. What are the notable trends driving market growth?

Growing Food Demand Due to High Population Growth.

7. Are there any restraints impacting market growth?

High Demand for Conventional and Synthetic Products; Lack of Awareness and Other Factors Limiting the Adoption of Agricultural Inoculants.

8. Can you provide examples of recent developments in the market?

January 2023: Bayer announced its Partnership with French company M2i Group which will provide Pheromone-based biological Crop Protection products. Bayer will integrate M2i's innovative press application technology into the product to form a digitally enabled solution.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Africa Agrochemicals Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Africa Agrochemicals Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Africa Agrochemicals Industry?

To stay informed about further developments, trends, and reports in the Africa Agrochemicals Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence