Key Insights

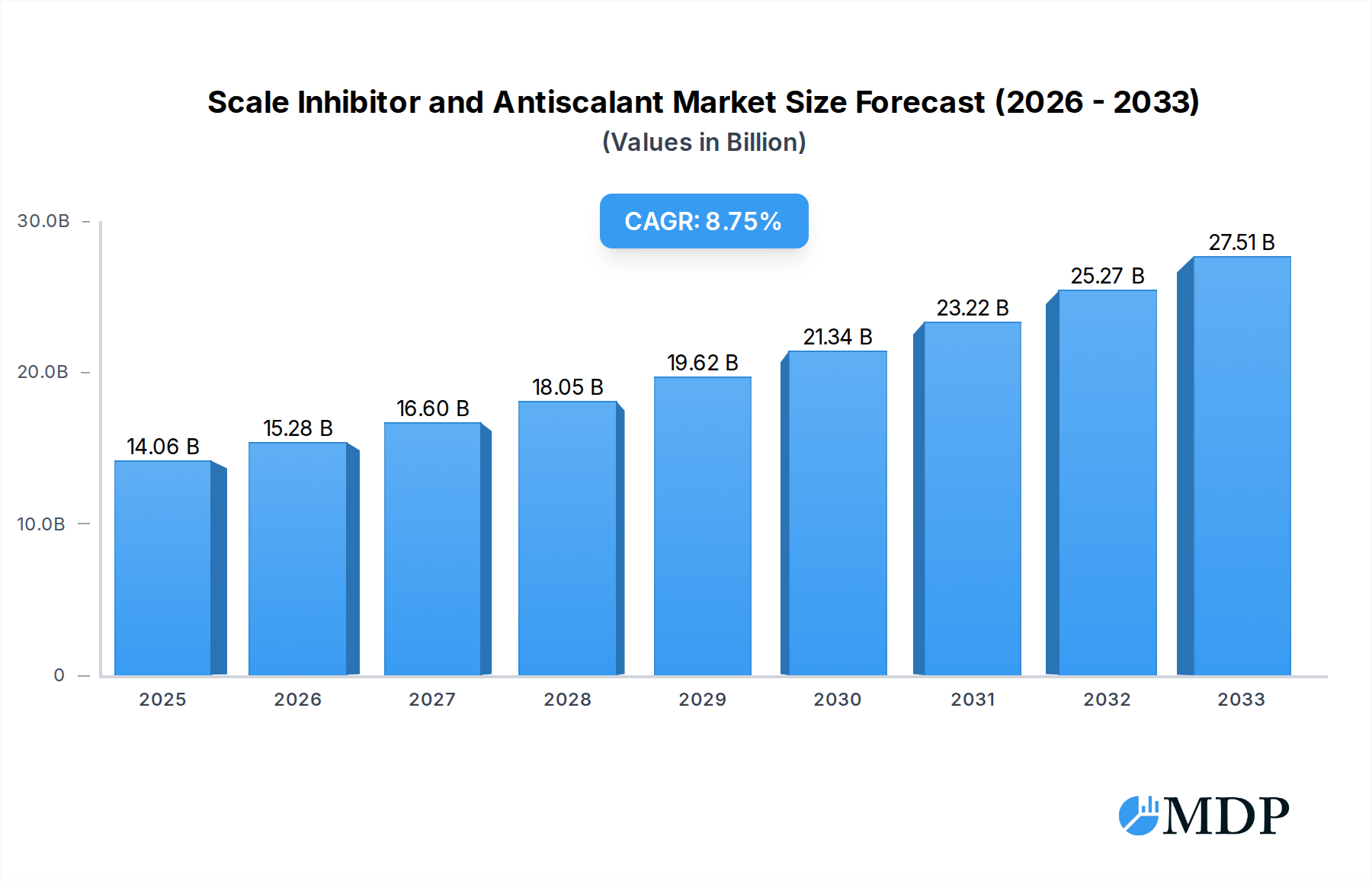

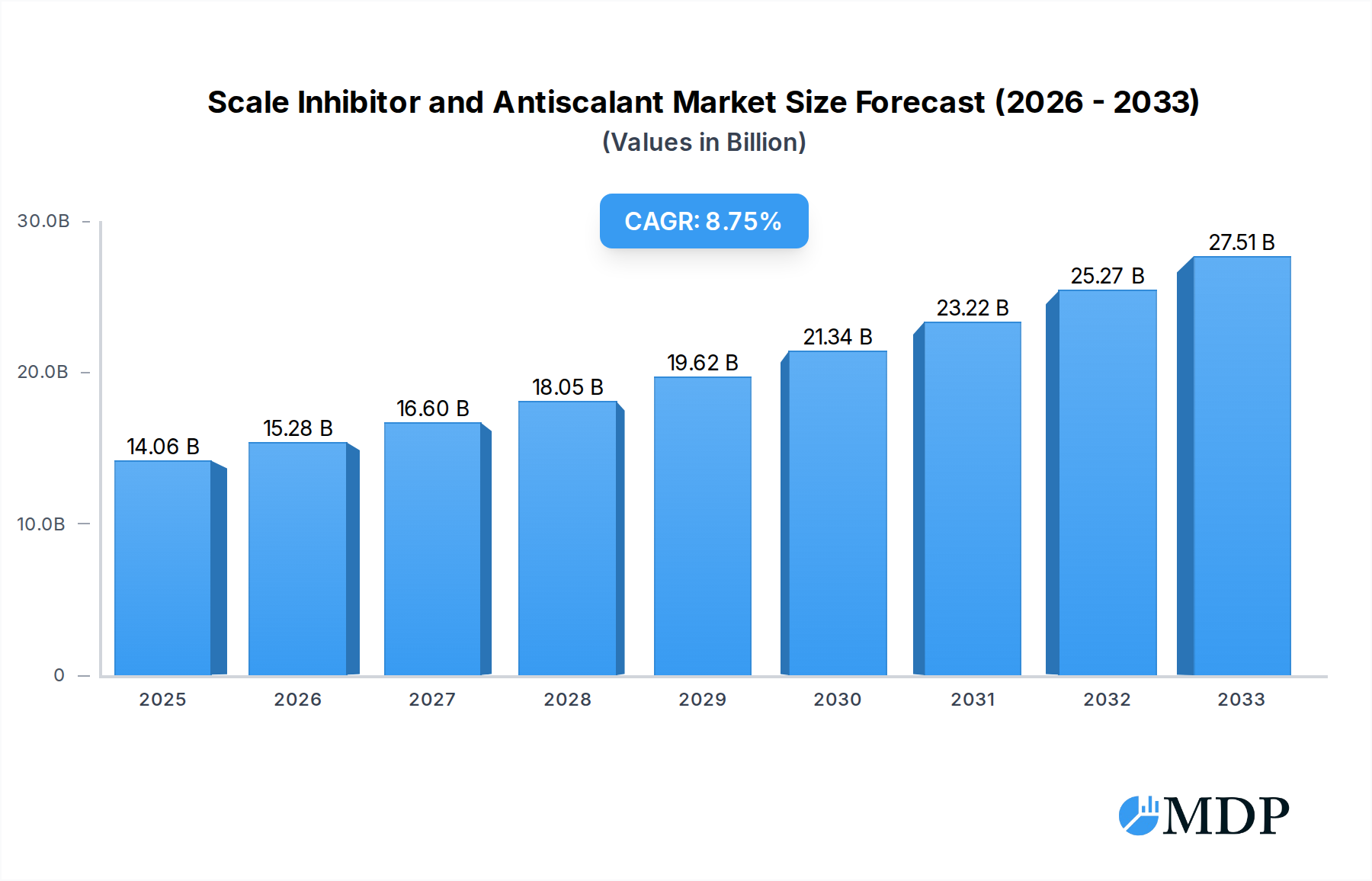

The global Scale Inhibitor and Antiscalant market is poised for substantial growth, projected to reach $14.06 billion in 2025 and expand at a robust Compound Annual Growth Rate (CAGR) of 8.7% through 2033. This upward trajectory is primarily fueled by the escalating demand for efficient water management solutions across diverse industrial sectors, including the burgeoning oil and gas industry, critical water and wastewater treatment facilities, and the power generation sector. The increasing need to protect vital infrastructure from the damaging effects of mineral scale formation, which can lead to reduced efficiency, increased maintenance costs, and premature equipment failure, is a paramount driver. Furthermore, stringent environmental regulations promoting sustainable water usage and minimizing industrial discharge are compelling industries to adopt advanced scale inhibition technologies. The market is witnessing significant innovation in product development, with a growing emphasis on eco-friendly and highly effective formulations.

Scale Inhibitor and Antiscalant Market Size (In Billion)

Key segments contributing to this market expansion include the widespread adoption of phosphonates and carboxylate-based scale inhibitors due to their superior performance and cost-effectiveness. The oil and gas sector, particularly in upstream exploration and production activities, represents a significant application area, driven by the challenging operational environments and the need to maintain flow assurance. The water and wastewater treatment segment is also a major consumer, as municipalities and industries strive to meet water quality standards and conserve precious water resources. While the market demonstrates strong growth, potential restraints such as the high initial investment cost for advanced treatment systems and fluctuations in raw material prices could present challenges. However, the overwhelming benefits of scale prevention in terms of operational efficiency, asset longevity, and regulatory compliance are expected to outweigh these limitations, driving sustained market expansion.

Scale Inhibitor and Antiscalant Company Market Share

Here's an SEO-optimized and engaging report description for "Scale Inhibitor and Antiscalant," incorporating high-traffic keywords and structured as requested:

Report Title: Global Scale Inhibitor and Antiscalant Market: Growth, Trends, and Forecast 2025-2033

Report Description:

Unlock comprehensive insights into the global Scale Inhibitor and Antiscalant market, a critical sector for industrial water management. This in-depth report provides a detailed analysis of market dynamics, key trends, leading applications, and future growth prospects, covering the period from 2019 to 2033. With a base year of 2025 and a forecast period extending to 2033, this research offers actionable intelligence for stakeholders seeking to capitalize on the evolving demands for efficient water treatment solutions.

The scale inhibitor market is experiencing significant expansion driven by increasing industrialization, stringent environmental regulations, and the growing need for optimized operational efficiency across diverse sectors. This report delves into the intricate interplay of market forces, highlighting innovation drivers, competitive landscapes, and the strategic moves of major players. Whether you are involved in oil and gas water treatment, pulp and paper manufacturing, mining operations, or wastewater management, understanding the nuances of scale prevention is paramount.

Explore the dominance of specific chemical types, such as carboxylate, sulfonates, and phosphonates, and their adoption across various applications including power generation, construction, and the chemical industry. This report dissects technological advancements, product developments, and emerging opportunities that are shaping the future of scale and corrosion control. Gain a competitive edge with data-driven analysis on market penetration, CAGR, and the strategic imperatives for sustained growth.

Key Report Segments:

Key Companies Covered: Avista Technologies, BASF SE, Dow Inc., General Electric, Ashland, Solenis, Kemira Oyg, Lenntech B.V., Clariant AG, Solvay, PWT Chemicals.

- Study Period: 2019–2033

- Base Year: 2025

- Estimated Year: 2025

- Forecast Period: 2025–2033

- Historical Period: 2019–2024

Scale Inhibitor and Antiscalant Market Dynamics & Concentration

The global scale inhibitor and antiscalant market exhibits a moderate to high concentration, with a few key players dominating a significant portion of the market share. Innovation drivers are primarily focused on developing eco-friendly and high-performance formulations, addressing increasingly stringent environmental regulations globally. Regulatory frameworks are becoming more demanding, pushing for sustainable and biodegradable chemical solutions, which in turn influences product development and market entry barriers. Product substitutes, such as physical water treatment methods, pose a growing challenge but often lack the comprehensive protection offered by chemical inhibitors in high-demand industrial settings. End-user trends are leaning towards integrated water management solutions that combine scale inhibition with corrosion control and other water treatment functionalities. Mergers and acquisition (M&A) activities have been observed, aimed at consolidating market presence, expanding product portfolios, and gaining access to new geographical regions. For instance, in the historical period, there were approximately 10-15 significant M&A deals each year, valued at an estimated one billion to five billion dollars collectively, reflecting strategic consolidation within the industry. The market share of leading companies ranges from approximately 15% to 25% for the top three players.

Scale Inhibitor and Antiscalant Industry Trends & Analysis

The scale inhibitor and antiscalant industry is on a robust growth trajectory, projected to witness a Compound Annual Growth Rate (CAGR) of approximately 5.5% over the forecast period. This expansion is propelled by a confluence of factors, including the ever-increasing global demand for clean water, the persistent need to protect industrial infrastructure from the damaging effects of scale formation, and the continuous industrialization and economic development across emerging economies. The water and wastewater treatment sector represents a substantial market segment, driven by regulatory mandates for improved water quality and the growing scarcity of potable water resources. In the oil and gas industry, scale inhibitors are indispensable for maintaining the flow assurance and operational efficiency of wells and pipelines, especially with the increasing exploitation of challenging reserves. Technological disruptions are shaping the industry, with a growing emphasis on developing advanced polymeric antiscalants and multi-functional additives that offer superior performance at lower dosages. These innovations are crucial for meeting the performance expectations of industries like pulp and paper and mining, where large volumes of water are processed, and scale deposition can lead to significant operational downtime and increased maintenance costs. Consumer preferences are shifting towards environmentally benign and sustainable chemical solutions. Manufacturers are investing heavily in R&D to create bio-based or biodegradable scale inhibitors that minimize environmental impact, aligning with corporate sustainability goals and stringent environmental policies. This trend also influences the adoption of specific chemical types, with a rising interest in formulations that offer a better environmental profile alongside effective scale prevention. The competitive dynamics within the market are characterized by intense price competition, a focus on product differentiation through performance and sustainability, and strategic partnerships aimed at market penetration and technology dissemination. The market penetration for advanced antiscalant technologies is estimated to grow from approximately 50% to 70% by 2033, indicating a significant shift towards higher-efficacy solutions. The ongoing development of smart water treatment systems also presents an opportunity for integrated scale inhibitor solutions that can adapt to changing water chemistry in real-time, further enhancing operational efficiency and reducing the need for manual intervention. The overall market size is expected to reach over one hundred billion dollars by the end of the forecast period.

Leading Markets & Segments in Scale Inhibitor and Antiscalant

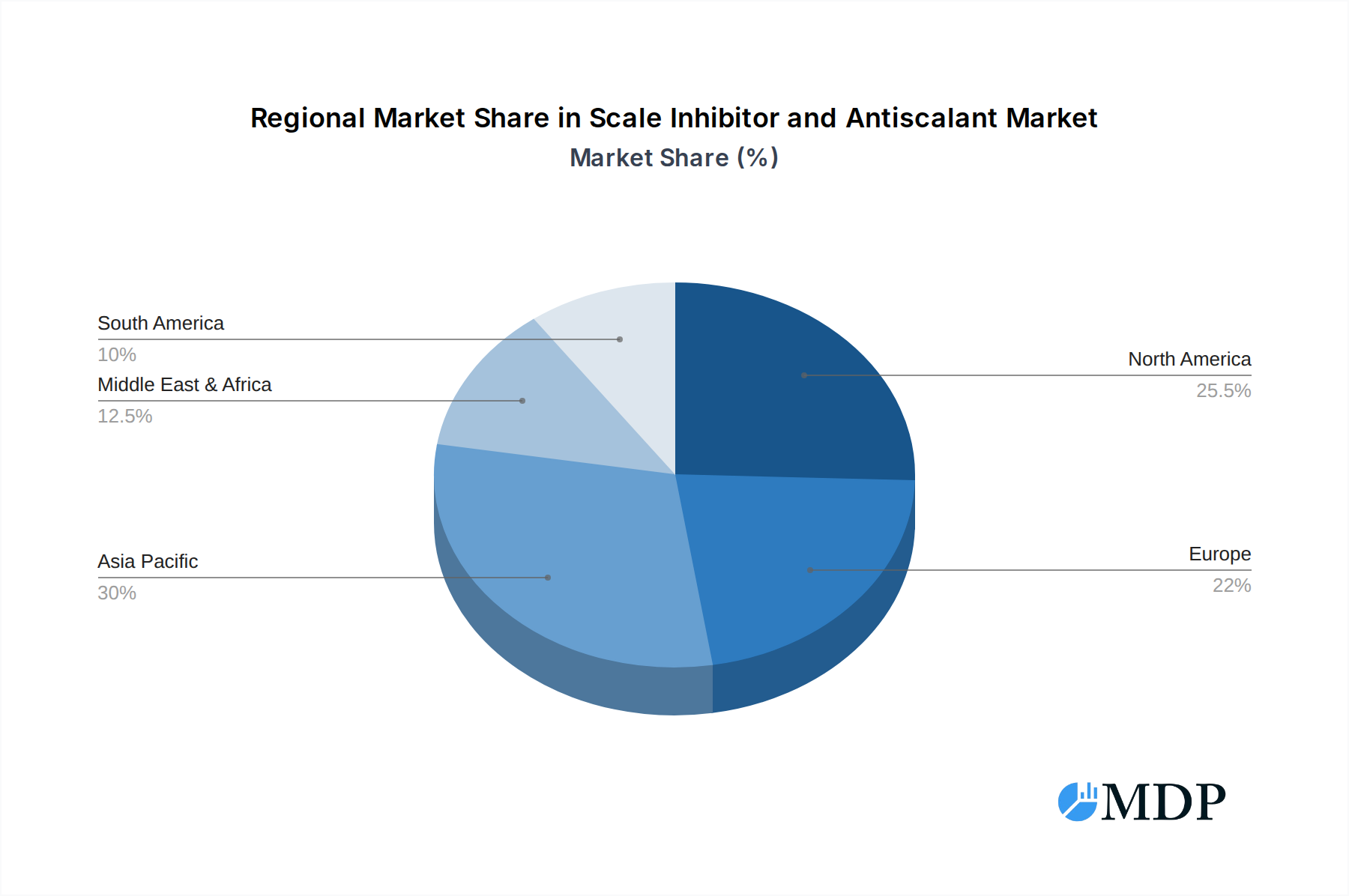

The Water and Wastewater Treatment application segment is undeniably the dominant force within the global scale inhibitor and antiscalant market, driven by escalating global water scarcity, stringent environmental regulations mandating improved water quality, and the continuous need for efficient industrial water management. This segment alone is estimated to account for over 30% of the total market share. Geographically, North America and Europe currently lead in terms of market penetration due to well-established industrial bases and robust regulatory frameworks. However, the Asia-Pacific region is exhibiting the fastest growth, fueled by rapid industrialization, urbanization, and significant investments in water infrastructure projects.

Within the Water and Wastewater Treatment segment, municipal water treatment plants and industrial wastewater facilities are major consumers. Key drivers for this dominance include:

- Regulatory Compliance: Strict government mandates on discharge limits and water quality necessitate effective scale and corrosion control.

- Infrastructure Protection: Preventing scale buildup in distribution networks, treatment equipment, and boilers extends asset lifespan and reduces maintenance costs, saving billions annually.

- Water Reuse and Recycling: As water resources become scarcer, increasing emphasis on water reuse requires advanced treatment methods, where scale inhibitors play a vital role.

Among the Types of scale inhibitors, Carboxylate and Sulfonates currently hold the largest market share, estimated at approximately 30% and 25% respectively, due to their proven efficacy, cost-effectiveness, and broad applicability across various water chemistries. Phosphonates are also significant, particularly in high-temperature and high-salinity environments, while Fluorids and other novel chemistries are gaining traction for specialized applications.

The Oil and Gas application segment is the second-largest contributor, driven by the imperative to maintain production efficiency and prevent costly downtime in exploration, extraction, and refining processes. Key drivers include:

- Flow Assurance: Preventing scale deposition in pipelines and production equipment is critical to maintaining optimal flow rates and preventing blockages, saving billions in potential lost production.

- Asset Integrity: Protecting offshore platforms, onshore facilities, and processing plants from scale-induced corrosion extends their operational life.

The Pulp and Paper industry relies heavily on scale inhibitors to prevent deposition on machinery, which can lead to reduced product quality and significant operational disruptions. The Mining sector utilizes these chemicals to manage scale in process water, tailings ponds, and processing equipment. The Power and Construction sectors, particularly in cooling tower operations and boiler systems, also represent substantial markets. The Chemical Industry employs scale inhibitors to maintain process efficiency and protect sensitive equipment in various chemical synthesis and processing applications.

Scale Inhibitor and Antiscalant Product Developments

Recent product developments in the scale inhibitor and antiscalant market are centered on creating highly effective, environmentally sustainable, and cost-efficient solutions. Innovations include advanced polymeric antiscalants with enhanced dispersion capabilities for complex water chemistries and higher temperatures. There is a significant push towards bio-based and biodegradable formulations, addressing growing regulatory pressure and corporate sustainability mandates. These new products offer competitive advantages by providing superior scale prevention at lower dosage rates, reducing chemical consumption and associated environmental impacts. Furthermore, the development of multi-functional additives that combine scale inhibition with corrosion control and microbial inhibition is gaining momentum, offering integrated water management solutions for end-users.

Key Drivers of Scale Inhibitor and Antiscalant Growth

The growth of the scale inhibitor and antiscalant market is primarily driven by several key factors. Increasing global demand for clean water, coupled with the growing scarcity of potable water resources, necessitates efficient water treatment solutions, including effective scale prevention. Stringent environmental regulations worldwide are pushing industries to adopt advanced water management practices, favoring chemicals that are both high-performing and environmentally responsible. Technological advancements in chemical formulations, leading to more effective and sustainable antiscalants, are also a significant growth catalyst. Furthermore, the continuous industrialization and economic development in emerging economies are expanding the customer base and increasing the demand for industrial water treatment chemicals. The need to protect critical infrastructure, such as pipelines, boilers, and cooling systems, from scale-induced damage and maintain operational efficiency, further fuels market expansion.

Challenges in the Scale Inhibitor and Antiscalant Market

The scale inhibitor and antiscalant market faces several challenges that could impede its growth. Increasingly stringent environmental regulations, while a driver for innovation, can also create barriers to market entry for new formulations and require significant investment in compliance and R&D, costing billions in R&D and testing. Supply chain disruptions, exacerbated by geopolitical instability and raw material price volatility, can impact production costs and availability, potentially affecting market stability. Intense competition among established players and the emergence of new entrants lead to price pressures, squeezing profit margins. The development and adoption of alternative, non-chemical water treatment technologies, though currently niche, represent a potential long-term threat by offering different approaches to scale management.

Emerging Opportunities in Scale Inhibitor and Antiscalant

Several emerging opportunities are poised to drive long-term growth in the scale inhibitor and antiscalant market. The increasing global focus on water conservation and reuse presents a significant opportunity for advanced antiscalants that enable higher cycles of concentration in industrial water systems, minimizing water discharge and consumption, potentially saving billions in water costs. Technological breakthroughs in nanotechnology and smart materials are paving the way for the development of novel, highly efficient scale inhibitors with targeted delivery mechanisms. Strategic partnerships between chemical manufacturers and industrial end-users are crucial for co-developing tailored solutions that address specific operational challenges. Furthermore, the expansion of industrial activities in developing regions offers substantial untapped market potential for scale inhibitor and antiscalant solutions.

Leading Players in the Scale Inhibitor and Antiscalant Sector

- Avista Technologies

- BASF SE

- Dow Inc.

- General Electric

- Ashland

- Solenis

- Kemira Oyg

- Lenntech B.V.

- Clariant AG

- Solvay

- PWT Chemicals

Key Milestones in Scale Inhibitor and Antiscalant Industry

- 2019: Introduction of several new biodegradable scale inhibitor formulations, responding to growing environmental concerns.

- 2020: Increased R&D investment in phosphonate-free antiscalants by major players, anticipating future regulatory shifts.

- 2021: Several strategic acquisitions focused on expanding product portfolios in high-performance and specialty antiscalants, involving hundreds of millions of dollars in deals.

- 2022: Launch of advanced polymeric scale inhibitors offering superior performance in challenging oilfield applications, commanding premium pricing.

- 2023: Growing adoption of digital monitoring and control systems for water treatment, influencing the demand for integrated scale inhibition solutions.

- 2024 (Estimated): Increased focus on circular economy principles, driving innovation in scale inhibitor recycling and reuse technologies.

Strategic Outlook for Scale Inhibitor and Antiscalant Market

The strategic outlook for the scale inhibitor and antiscalant market is exceptionally positive, characterized by robust growth accelerators. The escalating global demand for sustainable water management solutions will continue to be a primary growth engine, driving innovation in eco-friendly chemistries and bio-based alternatives. Advancements in material science and nanotechnology are expected to unlock new frontiers in antiscalant efficacy, offering tailored solutions for increasingly complex industrial challenges. Strategic collaborations and partnerships between technology providers and industrial users will be crucial for market penetration and the development of customized solutions. Furthermore, the ongoing expansion of industrial sectors in emerging economies presents significant opportunities for market players to extend their geographical reach and capitalize on unmet demand, contributing to an estimated market growth of tens of billions of dollars.

Scale Inhibitor and Antiscalant Segmentation

-

1. Application

- 1.1. Pulp and Paper

- 1.2. Mining

- 1.3. Others

- 1.4. Oil and Gas

- 1.5. Water and Wastewater Treatment

- 1.6. Power and Construction

- 1.7. Chemical Industry

-

2. Types

- 2.1. Carboxylate

- 2.2. Sulfonates

- 2.3. Phosphonates

- 2.4. Fluorids

- 2.5. Others

Scale Inhibitor and Antiscalant Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Scale Inhibitor and Antiscalant Regional Market Share

Geographic Coverage of Scale Inhibitor and Antiscalant

Scale Inhibitor and Antiscalant REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.7% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Scale Inhibitor and Antiscalant Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Pulp and Paper

- 5.1.2. Mining

- 5.1.3. Others

- 5.1.4. Oil and Gas

- 5.1.5. Water and Wastewater Treatment

- 5.1.6. Power and Construction

- 5.1.7. Chemical Industry

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Carboxylate

- 5.2.2. Sulfonates

- 5.2.3. Phosphonates

- 5.2.4. Fluorids

- 5.2.5. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Scale Inhibitor and Antiscalant Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Pulp and Paper

- 6.1.2. Mining

- 6.1.3. Others

- 6.1.4. Oil and Gas

- 6.1.5. Water and Wastewater Treatment

- 6.1.6. Power and Construction

- 6.1.7. Chemical Industry

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Carboxylate

- 6.2.2. Sulfonates

- 6.2.3. Phosphonates

- 6.2.4. Fluorids

- 6.2.5. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Scale Inhibitor and Antiscalant Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Pulp and Paper

- 7.1.2. Mining

- 7.1.3. Others

- 7.1.4. Oil and Gas

- 7.1.5. Water and Wastewater Treatment

- 7.1.6. Power and Construction

- 7.1.7. Chemical Industry

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Carboxylate

- 7.2.2. Sulfonates

- 7.2.3. Phosphonates

- 7.2.4. Fluorids

- 7.2.5. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Scale Inhibitor and Antiscalant Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Pulp and Paper

- 8.1.2. Mining

- 8.1.3. Others

- 8.1.4. Oil and Gas

- 8.1.5. Water and Wastewater Treatment

- 8.1.6. Power and Construction

- 8.1.7. Chemical Industry

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Carboxylate

- 8.2.2. Sulfonates

- 8.2.3. Phosphonates

- 8.2.4. Fluorids

- 8.2.5. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Scale Inhibitor and Antiscalant Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Pulp and Paper

- 9.1.2. Mining

- 9.1.3. Others

- 9.1.4. Oil and Gas

- 9.1.5. Water and Wastewater Treatment

- 9.1.6. Power and Construction

- 9.1.7. Chemical Industry

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Carboxylate

- 9.2.2. Sulfonates

- 9.2.3. Phosphonates

- 9.2.4. Fluorids

- 9.2.5. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Scale Inhibitor and Antiscalant Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Pulp and Paper

- 10.1.2. Mining

- 10.1.3. Others

- 10.1.4. Oil and Gas

- 10.1.5. Water and Wastewater Treatment

- 10.1.6. Power and Construction

- 10.1.7. Chemical Industry

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Carboxylate

- 10.2.2. Sulfonates

- 10.2.3. Phosphonates

- 10.2.4. Fluorids

- 10.2.5. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Avista Technologies

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 BASF SE

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Dow Inc.

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 General Electric

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Ashland

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Solenis

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Kemira Oyg

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Lenntech B.V.

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Clariant AG

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Solvay

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 PWT Chemicals

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.1 Avista Technologies

List of Figures

- Figure 1: Global Scale Inhibitor and Antiscalant Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Scale Inhibitor and Antiscalant Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Scale Inhibitor and Antiscalant Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Scale Inhibitor and Antiscalant Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Scale Inhibitor and Antiscalant Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Scale Inhibitor and Antiscalant Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Scale Inhibitor and Antiscalant Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Scale Inhibitor and Antiscalant Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Scale Inhibitor and Antiscalant Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Scale Inhibitor and Antiscalant Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Scale Inhibitor and Antiscalant Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Scale Inhibitor and Antiscalant Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Scale Inhibitor and Antiscalant Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Scale Inhibitor and Antiscalant Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Scale Inhibitor and Antiscalant Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Scale Inhibitor and Antiscalant Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Scale Inhibitor and Antiscalant Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Scale Inhibitor and Antiscalant Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Scale Inhibitor and Antiscalant Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Scale Inhibitor and Antiscalant Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Scale Inhibitor and Antiscalant Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Scale Inhibitor and Antiscalant Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Scale Inhibitor and Antiscalant Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Scale Inhibitor and Antiscalant Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Scale Inhibitor and Antiscalant Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Scale Inhibitor and Antiscalant Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Scale Inhibitor and Antiscalant Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Scale Inhibitor and Antiscalant Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Scale Inhibitor and Antiscalant Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Scale Inhibitor and Antiscalant Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Scale Inhibitor and Antiscalant Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Scale Inhibitor and Antiscalant Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Scale Inhibitor and Antiscalant Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Scale Inhibitor and Antiscalant Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Scale Inhibitor and Antiscalant Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Scale Inhibitor and Antiscalant Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Scale Inhibitor and Antiscalant Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Scale Inhibitor and Antiscalant Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Scale Inhibitor and Antiscalant Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Scale Inhibitor and Antiscalant Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Scale Inhibitor and Antiscalant Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Scale Inhibitor and Antiscalant Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Scale Inhibitor and Antiscalant Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Scale Inhibitor and Antiscalant Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Scale Inhibitor and Antiscalant Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Scale Inhibitor and Antiscalant Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Scale Inhibitor and Antiscalant Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Scale Inhibitor and Antiscalant Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Scale Inhibitor and Antiscalant Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Scale Inhibitor and Antiscalant Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Scale Inhibitor and Antiscalant Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Scale Inhibitor and Antiscalant Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Scale Inhibitor and Antiscalant Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Scale Inhibitor and Antiscalant Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Scale Inhibitor and Antiscalant Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Scale Inhibitor and Antiscalant Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Scale Inhibitor and Antiscalant Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Scale Inhibitor and Antiscalant Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Scale Inhibitor and Antiscalant Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Scale Inhibitor and Antiscalant Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Scale Inhibitor and Antiscalant Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Scale Inhibitor and Antiscalant Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Scale Inhibitor and Antiscalant Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Scale Inhibitor and Antiscalant Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Scale Inhibitor and Antiscalant Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Scale Inhibitor and Antiscalant Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Scale Inhibitor and Antiscalant Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Scale Inhibitor and Antiscalant Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Scale Inhibitor and Antiscalant Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Scale Inhibitor and Antiscalant Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Scale Inhibitor and Antiscalant Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Scale Inhibitor and Antiscalant Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Scale Inhibitor and Antiscalant Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Scale Inhibitor and Antiscalant Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Scale Inhibitor and Antiscalant Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Scale Inhibitor and Antiscalant Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Scale Inhibitor and Antiscalant Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Scale Inhibitor and Antiscalant?

The projected CAGR is approximately 8.7%.

2. Which companies are prominent players in the Scale Inhibitor and Antiscalant?

Key companies in the market include Avista Technologies, BASF SE, Dow Inc., General Electric, Ashland, Solenis, Kemira Oyg, Lenntech B.V., Clariant AG, Solvay, PWT Chemicals.

3. What are the main segments of the Scale Inhibitor and Antiscalant?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 14.06 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Scale Inhibitor and Antiscalant," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Scale Inhibitor and Antiscalant report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Scale Inhibitor and Antiscalant?

To stay informed about further developments, trends, and reports in the Scale Inhibitor and Antiscalant, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence