Key Insights

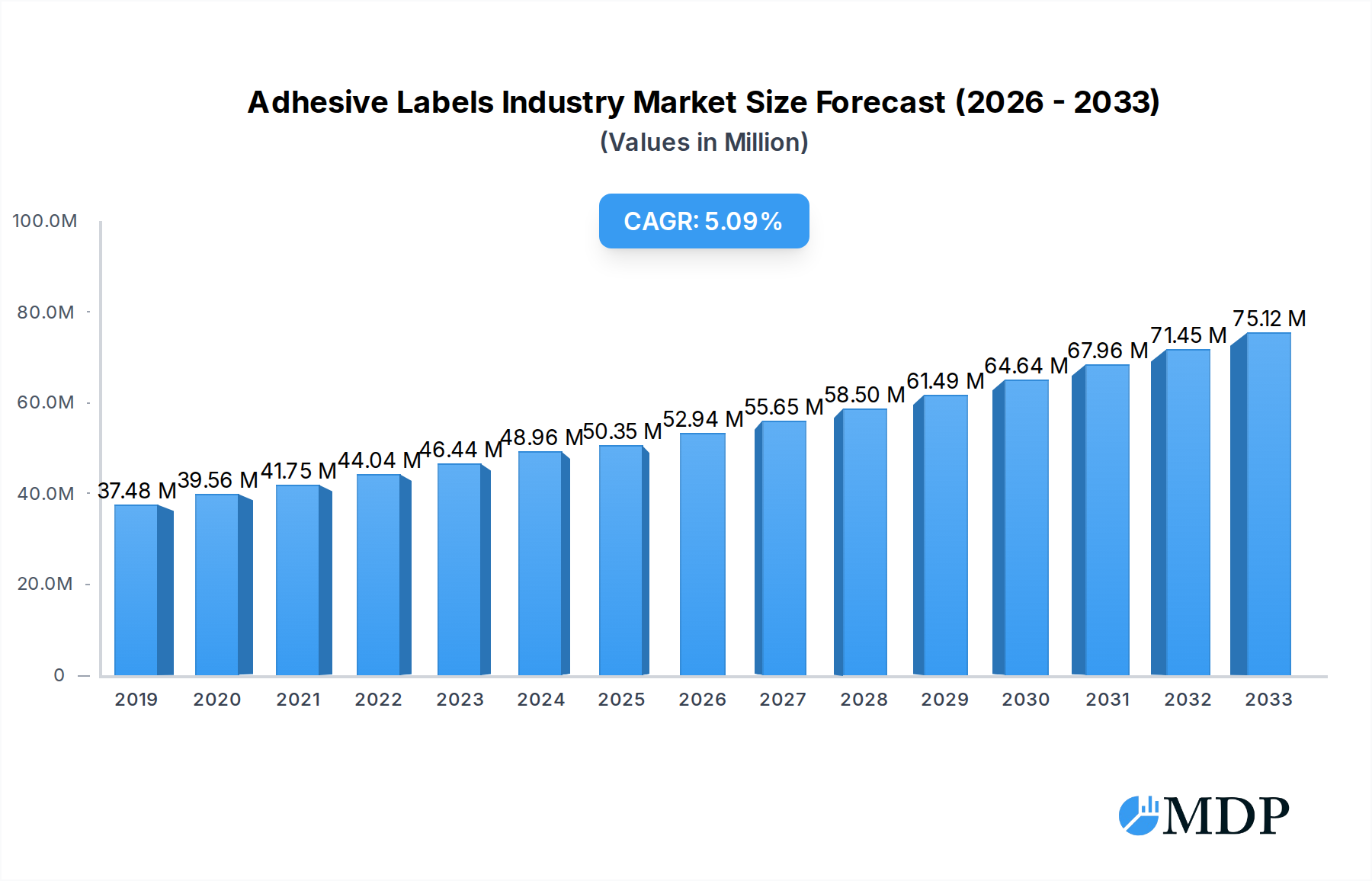

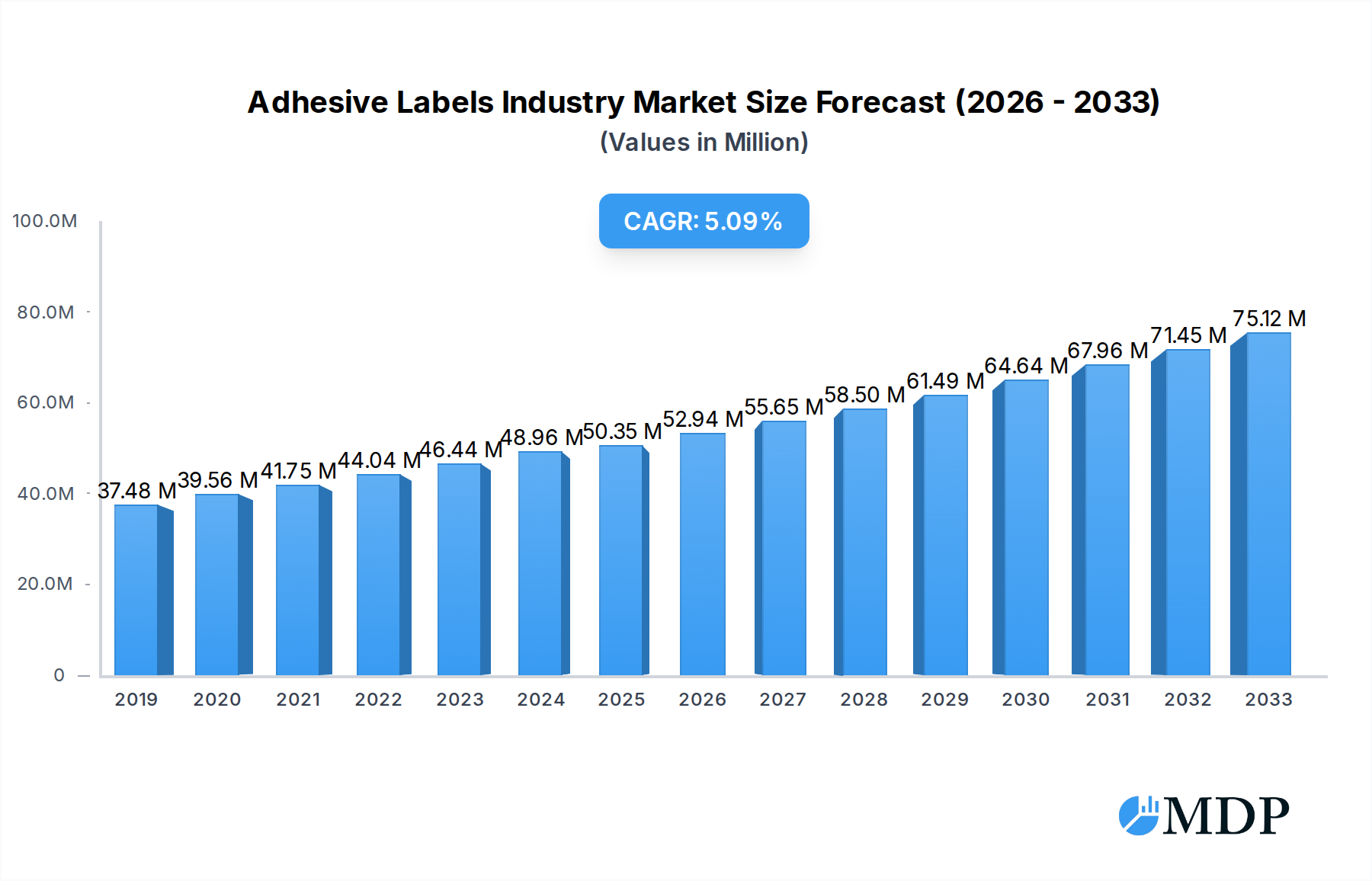

The global Adhesive Labels market is poised for robust growth, projected to reach $50.35 million by 2025, expanding at a Compound Annual Growth Rate (CAGR) of 5.47% from 2019 to 2033. This significant market expansion is primarily propelled by the escalating demand across diverse end-use industries, notably Food and Beverage, Pharmaceutical, and Consumer Durables. The burgeoning e-commerce sector, coupled with increasing consumer awareness regarding product information and branding, is a key driver for the adoption of high-quality adhesive labels. Furthermore, advancements in printing technologies, such as digital printing, are enabling greater customization and shorter run lengths, catering to niche market demands and contributing to market growth. The convenience and versatility offered by adhesive labels, from product identification and branding to tamper-evidence and regulatory compliance, further solidify their indispensable role in modern commerce.

Adhesive Labels Industry Market Size (In Million)

The market landscape is characterized by a dynamic interplay of trends and restraints. Key trends include the rising adoption of sustainable and eco-friendly label materials, such as recyclable and biodegradable options, driven by increasing environmental regulations and consumer preferences. The growing emphasis on supply chain visibility and traceability is also fueling the demand for smart labels with integrated RFID or NFC technology. However, volatile raw material prices, particularly for paper and plastic, along with stringent regulatory frameworks governing labeling in specific industries like pharmaceuticals, can present challenges to market growth. The competitive environment is shaped by major players like Avery Dennison Corporation, UPM, and Mondi, who are focusing on product innovation, strategic collaborations, and expanding their geographical presence to capitalize on emerging opportunities.

Adhesive Labels Industry Company Market Share

Adhesive Labels Industry: Market Dynamics, Trends, and Strategic Outlook 2024-2033

Unlock comprehensive insights into the global Adhesive Labels Industry with this in-depth market research report. Spanning from 2019 to 2033, with a base and estimated year of 2025, this study delivers granular analysis of market dynamics, emerging trends, leading segments, and strategic opportunities. Leveraging high-traffic keywords such as "adhesive labels market," "labeling solutions," "packaging industry," "food and beverage labels," "pharmaceutical labels," and "logistics labeling," this report is essential for stakeholders seeking to navigate this dynamic sector. With a forecast period from 2025 to 2033 and historical data from 2019-2024, gain a complete understanding of market evolution and future potential. The report quantifies the market size in excess of one million units for various metrics, providing actionable data for strategic decision-making.

Adhesive Labels Industry Market Dynamics & Concentration

The global Adhesive Labels Industry exhibits a moderate to high market concentration, with a few dominant players holding significant market share, estimated at over 70% combined. Innovation is a key driver, propelled by advancements in material science, printing technologies, and sustainable solutions. Regulatory frameworks surrounding food safety, pharmaceutical traceability, and environmental impact are increasingly shaping product development and market entry strategies. While direct product substitutes are limited, the rise of alternative packaging formats and digital information solutions presents an indirect competitive challenge. End-user trends indicate a strong demand for high-performance, customizable, and sustainable labeling solutions across diverse applications. Mergers and acquisitions (M&A) activity remains robust, with an estimated xx M&A deals annually, driven by the pursuit of market expansion, technological integration, and economies of scale. Companies like Avery Dennison Corporation and UPM consistently lead in M&A activities, solidifying their market positions.

Adhesive Labels Industry Industry Trends & Analysis

The Adhesive Labels Industry is experiencing robust growth, projected to witness a Compound Annual Growth Rate (CAGR) of approximately 6.5% over the forecast period. This expansion is primarily fueled by the burgeoning global packaging sector, with a market penetration rate steadily increasing across all end-use industries. Technological disruptions, including the adoption of digital printing, variable data printing (VDP), and advanced material functionalities like tamper-evidence and anti-counterfeiting features, are transforming product offerings. Consumer preferences are increasingly leaning towards aesthetically appealing, informative, and eco-friendly labels, driving demand for sustainable face materials and adhesives. Competitive dynamics are characterized by intense price competition, product differentiation strategies, and a growing emphasis on supply chain efficiency. The food and beverage sector continues to be a dominant application, representing over 35% of the global market share, due to its high volume consumption and stringent labeling requirements. The pharmaceutical industry also contributes significantly, driven by the need for serialization and track-and-trace capabilities, accounting for approximately 20% of the market. Advancements in plastic face materials, particularly polypropylene and polyester, are gaining traction due to their durability and versatility, chipping away at paper-based label dominance. The hot-melt adhesive segment remains a cornerstone due to its cost-effectiveness and broad applicability, although emulsion acrylics are gaining ground for their eco-friendly profiles and performance in specific applications.

Leading Markets & Segments in Adhesive Labels Industry

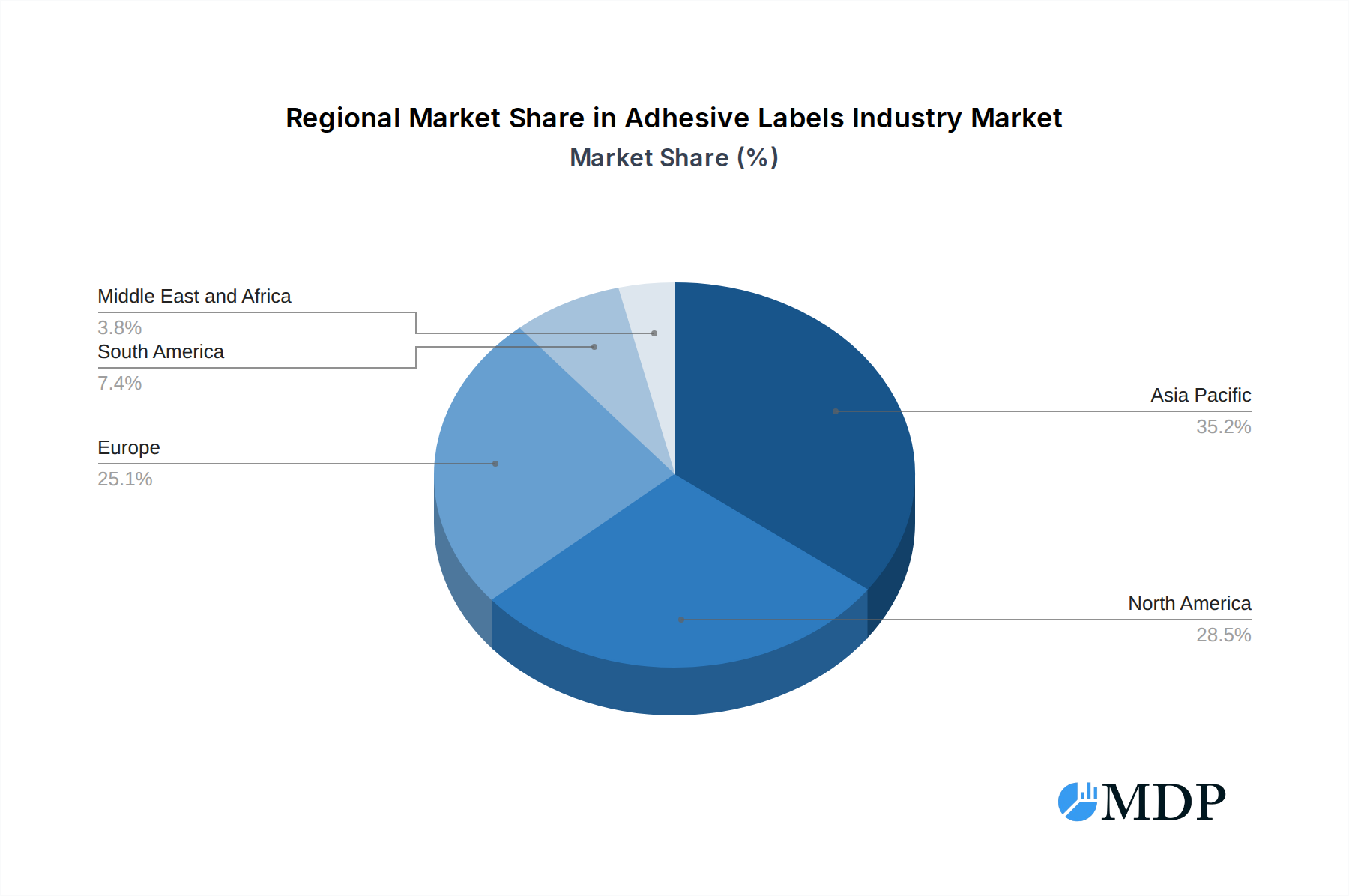

The Asia-Pacific region stands as the dominant market for adhesive labels, driven by its rapidly expanding manufacturing base, burgeoning middle class, and increasing demand from the food and beverage, pharmaceutical, and consumer goods sectors. Within this region, countries like China and India are at the forefront of growth, supported by favorable government policies and significant investments in infrastructure.

Dominant Application:

- Food and Beverage: This segment continues its reign, constituting over 35% of the global market. Key drivers include the immense volume of packaged food and beverages, stringent food safety regulations, and the growing demand for visually appealing and informative product labeling. Economic growth and evolving consumer lifestyles in emerging economies further bolster this segment.

- Pharmaceutical: Representing approximately 20% of the market, this segment is propelled by global healthcare demands, the increasing prevalence of chronic diseases, and strict regulatory mandates for drug traceability, serialization, and patient safety. The need for high-security and tamper-evident labels is paramount.

- Logistics and Transport: This segment is experiencing significant growth due to the expansion of e-commerce and global supply chains. Efficient labeling for shipping, tracking, and inventory management is crucial, driving demand for durable and scannable labels.

Dominant Face Material:

- Plastic (Polypropylene and Polyester): These materials are increasingly favored over paper due to their superior durability, resistance to moisture and chemicals, and enhanced printability. Polypropylene labels are widely used in food and beverage and personal care, while polyester labels offer higher temperature resistance and clarity, making them ideal for demanding applications like automotive and electronics.

Dominant Adhesive Type:

- Hot-melt: This adhesive type remains the most widely used due to its fast setting times, strong initial tack, and cost-effectiveness. It is suitable for a broad range of applications and substrates, particularly in high-speed packaging lines.

Adhesive Labels Industry Product Developments

Product innovations in the Adhesive Labels Industry are focused on enhancing functionality, sustainability, and digital integration. Advancements in pressure-sensitive adhesive formulations are yielding improved adhesion to challenging surfaces and enhanced durability. The development of eco-friendly liners and facestocks, including compostable and recyclable materials, is a key trend. Smart labeling solutions, incorporating RFID technology and QR codes, are gaining traction for supply chain traceability and consumer engagement. These innovations offer competitive advantages by meeting evolving regulatory demands and consumer preferences for sustainable and technologically advanced packaging.

Key Drivers of Adhesive Labels Industry Growth

The Adhesive Labels Industry's growth is propelled by several interconnected factors. Technological advancements in printing, such as digital and flexographic printing, enable higher quality, faster production, and greater customization. The expanding global packaging market, driven by rising consumption and urbanization, directly translates to increased demand for labels. Stringent regulatory requirements for product safety, traceability (especially in pharmaceuticals and food), and environmental impact necessitate advanced labeling solutions. Furthermore, the growth of e-commerce and the logistics sector relies heavily on efficient and accurate labeling for shipment tracking and inventory management.

Challenges in the Adhesive Labels Industry Market

Despite robust growth, the Adhesive Labels Industry faces several challenges. Fluctuating raw material prices, particularly for paper pulp and petroleum-based plastics, can impact profit margins. Intense competition from both established players and new entrants leads to price pressures and the need for continuous innovation. Supply chain disruptions, as witnessed in recent years, can affect the availability and cost of raw materials and finished goods. Increasing environmental regulations regarding waste and recyclability require manufacturers to invest in sustainable alternatives, which can be costly.

Emerging Opportunities in Adhesive Labels Industry

The Adhesive Labels Industry is poised for significant growth driven by emerging opportunities. The increasing demand for sustainable and eco-friendly labeling solutions presents a major avenue for innovation and market differentiation. The expansion of the pharmaceutical and healthcare sectors, coupled with stringent track-and-trace regulations, fuels demand for high-security and functional labels. The growth of the e-commerce sector continues to drive the need for robust and versatile labeling for shipping and fulfillment. Furthermore, technological integration, such as the adoption of RFID and smart label technologies, offers opportunities for added value and enhanced supply chain visibility.

Leading Players in the Adhesive Labels Industry Sector

- LECTA

- Optimum Group

- HERMA

- H B Fuller Company

- Avery Dennison Corporation

- Asteria Group

- Fuji Seal International Inc

- Thai KK Group

- LINTEC Corporation

- Mondi

- UPM

- 3M

- Symbio Inc

- CPC Haferkamp GmbH & Co KG

Key Milestones in Adhesive Labels Industry Industry

- May 2022: Mondi announced switching glassine-based liners to certified base paper. It is to move to an environmentally benign supply chain and get a stronghold in European markets.

- May 2022: UPM acquired AMC AG, a German-based company. This move will expand the product base of UPM Raflatac in the coming years and in expanding economies.

Strategic Outlook for Adhesive Labels Industry Market

The strategic outlook for the Adhesive Labels Industry is positive, driven by continued innovation and market expansion. Focus on sustainable materials and manufacturing processes will be crucial for long-term success and meeting regulatory and consumer demands. Investments in digital printing technologies will enhance customization capabilities and production efficiency. The growth of emerging economies presents significant untapped market potential. Companies that can effectively leverage strategic partnerships and M&A activities will be well-positioned to consolidate market share and expand their product portfolios, particularly in niche and high-growth segments like pharmaceutical and specialty labels.

Adhesive Labels Industry Segmentation

-

1. Adhesive Type

- 1.1. Hot-melt

- 1.2. Emulsion Acrylic

- 1.3. Solvent

-

2. Face Material

- 2.1. Paper

-

2.2. Plastic

- 2.2.1. Polypropylene

- 2.2.2. Polyester

- 2.2.3. Vinyl

- 2.2.4. Other Plastics

-

3. Application

- 3.1. Food and Beverage

- 3.2. Pharmaceutical

- 3.3. Logistics and Transport

- 3.4. Personal Care

- 3.5. Consumer Durables

- 3.6. Other Applications

Adhesive Labels Industry Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. India

- 1.3. Japan

- 1.4. South Korea

- 1.5. Rest of Asia Pacific

-

2. North America

- 2.1. United States

- 2.2. Canada

- 2.3. Mexico

-

3. Europe

- 3.1. Germany

- 3.2. United Kingdom

- 3.3. France

- 3.4. Italy

- 3.5. Rest of Europe

-

4. South America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Rest of South America

-

5. Middle East and Africa

- 5.1. South Africa

- 5.2. Saudi Arabia

- 5.3. Rest of Middle East and Africa

Adhesive Labels Industry Regional Market Share

Geographic Coverage of Adhesive Labels Industry

Adhesive Labels Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 5.47% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Adhesive Type

- 5.1.1. Hot-melt

- 5.1.2. Emulsion Acrylic

- 5.1.3. Solvent

- 5.2. Market Analysis, Insights and Forecast - by Face Material

- 5.2.1. Paper

- 5.2.2. Plastic

- 5.2.2.1. Polypropylene

- 5.2.2.2. Polyester

- 5.2.2.3. Vinyl

- 5.2.2.4. Other Plastics

- 5.3. Market Analysis, Insights and Forecast - by Application

- 5.3.1. Food and Beverage

- 5.3.2. Pharmaceutical

- 5.3.3. Logistics and Transport

- 5.3.4. Personal Care

- 5.3.5. Consumer Durables

- 5.3.6. Other Applications

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Asia Pacific

- 5.4.2. North America

- 5.4.3. Europe

- 5.4.4. South America

- 5.4.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Adhesive Type

- 6. Global Adhesive Labels Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Adhesive Type

- 6.1.1. Hot-melt

- 6.1.2. Emulsion Acrylic

- 6.1.3. Solvent

- 6.2. Market Analysis, Insights and Forecast - by Face Material

- 6.2.1. Paper

- 6.2.2. Plastic

- 6.2.2.1. Polypropylene

- 6.2.2.2. Polyester

- 6.2.2.3. Vinyl

- 6.2.2.4. Other Plastics

- 6.3. Market Analysis, Insights and Forecast - by Application

- 6.3.1. Food and Beverage

- 6.3.2. Pharmaceutical

- 6.3.3. Logistics and Transport

- 6.3.4. Personal Care

- 6.3.5. Consumer Durables

- 6.3.6. Other Applications

- 6.1. Market Analysis, Insights and Forecast - by Adhesive Type

- 7. Asia Pacific Adhesive Labels Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Adhesive Type

- 7.1.1. Hot-melt

- 7.1.2. Emulsion Acrylic

- 7.1.3. Solvent

- 7.2. Market Analysis, Insights and Forecast - by Face Material

- 7.2.1. Paper

- 7.2.2. Plastic

- 7.2.2.1. Polypropylene

- 7.2.2.2. Polyester

- 7.2.2.3. Vinyl

- 7.2.2.4. Other Plastics

- 7.3. Market Analysis, Insights and Forecast - by Application

- 7.3.1. Food and Beverage

- 7.3.2. Pharmaceutical

- 7.3.3. Logistics and Transport

- 7.3.4. Personal Care

- 7.3.5. Consumer Durables

- 7.3.6. Other Applications

- 7.1. Market Analysis, Insights and Forecast - by Adhesive Type

- 8. North America Adhesive Labels Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Adhesive Type

- 8.1.1. Hot-melt

- 8.1.2. Emulsion Acrylic

- 8.1.3. Solvent

- 8.2. Market Analysis, Insights and Forecast - by Face Material

- 8.2.1. Paper

- 8.2.2. Plastic

- 8.2.2.1. Polypropylene

- 8.2.2.2. Polyester

- 8.2.2.3. Vinyl

- 8.2.2.4. Other Plastics

- 8.3. Market Analysis, Insights and Forecast - by Application

- 8.3.1. Food and Beverage

- 8.3.2. Pharmaceutical

- 8.3.3. Logistics and Transport

- 8.3.4. Personal Care

- 8.3.5. Consumer Durables

- 8.3.6. Other Applications

- 8.1. Market Analysis, Insights and Forecast - by Adhesive Type

- 9. Europe Adhesive Labels Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Adhesive Type

- 9.1.1. Hot-melt

- 9.1.2. Emulsion Acrylic

- 9.1.3. Solvent

- 9.2. Market Analysis, Insights and Forecast - by Face Material

- 9.2.1. Paper

- 9.2.2. Plastic

- 9.2.2.1. Polypropylene

- 9.2.2.2. Polyester

- 9.2.2.3. Vinyl

- 9.2.2.4. Other Plastics

- 9.3. Market Analysis, Insights and Forecast - by Application

- 9.3.1. Food and Beverage

- 9.3.2. Pharmaceutical

- 9.3.3. Logistics and Transport

- 9.3.4. Personal Care

- 9.3.5. Consumer Durables

- 9.3.6. Other Applications

- 9.1. Market Analysis, Insights and Forecast - by Adhesive Type

- 10. South America Adhesive Labels Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Adhesive Type

- 10.1.1. Hot-melt

- 10.1.2. Emulsion Acrylic

- 10.1.3. Solvent

- 10.2. Market Analysis, Insights and Forecast - by Face Material

- 10.2.1. Paper

- 10.2.2. Plastic

- 10.2.2.1. Polypropylene

- 10.2.2.2. Polyester

- 10.2.2.3. Vinyl

- 10.2.2.4. Other Plastics

- 10.3. Market Analysis, Insights and Forecast - by Application

- 10.3.1. Food and Beverage

- 10.3.2. Pharmaceutical

- 10.3.3. Logistics and Transport

- 10.3.4. Personal Care

- 10.3.5. Consumer Durables

- 10.3.6. Other Applications

- 10.1. Market Analysis, Insights and Forecast - by Adhesive Type

- 11. Middle East and Africa Adhesive Labels Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Adhesive Type

- 11.1.1. Hot-melt

- 11.1.2. Emulsion Acrylic

- 11.1.3. Solvent

- 11.2. Market Analysis, Insights and Forecast - by Face Material

- 11.2.1. Paper

- 11.2.2. Plastic

- 11.2.2.1. Polypropylene

- 11.2.2.2. Polyester

- 11.2.2.3. Vinyl

- 11.2.2.4. Other Plastics

- 11.3. Market Analysis, Insights and Forecast - by Application

- 11.3.1. Food and Beverage

- 11.3.2. Pharmaceutical

- 11.3.3. Logistics and Transport

- 11.3.4. Personal Care

- 11.3.5. Consumer Durables

- 11.3.6. Other Applications

- 11.1. Market Analysis, Insights and Forecast - by Adhesive Type

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 LECTA

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Optimum Group

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 HERMA

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 H B Fuller Company

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Avery Dennison Corporation

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Asteria Group

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Fuji Seal International Inc

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Thai KK Group

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 LINTEC Corporation

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 Mondi

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 UPM*List Not Exhaustive

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 3M

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Symbio Inc

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 CPC Haferkamp GmbH & Co KG

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.1 LECTA

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Adhesive Labels Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: Asia Pacific Adhesive Labels Industry Revenue (Million), by Adhesive Type 2025 & 2033

- Figure 3: Asia Pacific Adhesive Labels Industry Revenue Share (%), by Adhesive Type 2025 & 2033

- Figure 4: Asia Pacific Adhesive Labels Industry Revenue (Million), by Face Material 2025 & 2033

- Figure 5: Asia Pacific Adhesive Labels Industry Revenue Share (%), by Face Material 2025 & 2033

- Figure 6: Asia Pacific Adhesive Labels Industry Revenue (Million), by Application 2025 & 2033

- Figure 7: Asia Pacific Adhesive Labels Industry Revenue Share (%), by Application 2025 & 2033

- Figure 8: Asia Pacific Adhesive Labels Industry Revenue (Million), by Country 2025 & 2033

- Figure 9: Asia Pacific Adhesive Labels Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: North America Adhesive Labels Industry Revenue (Million), by Adhesive Type 2025 & 2033

- Figure 11: North America Adhesive Labels Industry Revenue Share (%), by Adhesive Type 2025 & 2033

- Figure 12: North America Adhesive Labels Industry Revenue (Million), by Face Material 2025 & 2033

- Figure 13: North America Adhesive Labels Industry Revenue Share (%), by Face Material 2025 & 2033

- Figure 14: North America Adhesive Labels Industry Revenue (Million), by Application 2025 & 2033

- Figure 15: North America Adhesive Labels Industry Revenue Share (%), by Application 2025 & 2033

- Figure 16: North America Adhesive Labels Industry Revenue (Million), by Country 2025 & 2033

- Figure 17: North America Adhesive Labels Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Europe Adhesive Labels Industry Revenue (Million), by Adhesive Type 2025 & 2033

- Figure 19: Europe Adhesive Labels Industry Revenue Share (%), by Adhesive Type 2025 & 2033

- Figure 20: Europe Adhesive Labels Industry Revenue (Million), by Face Material 2025 & 2033

- Figure 21: Europe Adhesive Labels Industry Revenue Share (%), by Face Material 2025 & 2033

- Figure 22: Europe Adhesive Labels Industry Revenue (Million), by Application 2025 & 2033

- Figure 23: Europe Adhesive Labels Industry Revenue Share (%), by Application 2025 & 2033

- Figure 24: Europe Adhesive Labels Industry Revenue (Million), by Country 2025 & 2033

- Figure 25: Europe Adhesive Labels Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: South America Adhesive Labels Industry Revenue (Million), by Adhesive Type 2025 & 2033

- Figure 27: South America Adhesive Labels Industry Revenue Share (%), by Adhesive Type 2025 & 2033

- Figure 28: South America Adhesive Labels Industry Revenue (Million), by Face Material 2025 & 2033

- Figure 29: South America Adhesive Labels Industry Revenue Share (%), by Face Material 2025 & 2033

- Figure 30: South America Adhesive Labels Industry Revenue (Million), by Application 2025 & 2033

- Figure 31: South America Adhesive Labels Industry Revenue Share (%), by Application 2025 & 2033

- Figure 32: South America Adhesive Labels Industry Revenue (Million), by Country 2025 & 2033

- Figure 33: South America Adhesive Labels Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Middle East and Africa Adhesive Labels Industry Revenue (Million), by Adhesive Type 2025 & 2033

- Figure 35: Middle East and Africa Adhesive Labels Industry Revenue Share (%), by Adhesive Type 2025 & 2033

- Figure 36: Middle East and Africa Adhesive Labels Industry Revenue (Million), by Face Material 2025 & 2033

- Figure 37: Middle East and Africa Adhesive Labels Industry Revenue Share (%), by Face Material 2025 & 2033

- Figure 38: Middle East and Africa Adhesive Labels Industry Revenue (Million), by Application 2025 & 2033

- Figure 39: Middle East and Africa Adhesive Labels Industry Revenue Share (%), by Application 2025 & 2033

- Figure 40: Middle East and Africa Adhesive Labels Industry Revenue (Million), by Country 2025 & 2033

- Figure 41: Middle East and Africa Adhesive Labels Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Adhesive Labels Industry Revenue Million Forecast, by Adhesive Type 2020 & 2033

- Table 2: Global Adhesive Labels Industry Revenue Million Forecast, by Face Material 2020 & 2033

- Table 3: Global Adhesive Labels Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 4: Global Adhesive Labels Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 5: Global Adhesive Labels Industry Revenue Million Forecast, by Adhesive Type 2020 & 2033

- Table 6: Global Adhesive Labels Industry Revenue Million Forecast, by Face Material 2020 & 2033

- Table 7: Global Adhesive Labels Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 8: Global Adhesive Labels Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 9: China Adhesive Labels Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: India Adhesive Labels Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: Japan Adhesive Labels Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: South Korea Adhesive Labels Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 13: Rest of Asia Pacific Adhesive Labels Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: Global Adhesive Labels Industry Revenue Million Forecast, by Adhesive Type 2020 & 2033

- Table 15: Global Adhesive Labels Industry Revenue Million Forecast, by Face Material 2020 & 2033

- Table 16: Global Adhesive Labels Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 17: Global Adhesive Labels Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 18: United States Adhesive Labels Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: Canada Adhesive Labels Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Mexico Adhesive Labels Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: Global Adhesive Labels Industry Revenue Million Forecast, by Adhesive Type 2020 & 2033

- Table 22: Global Adhesive Labels Industry Revenue Million Forecast, by Face Material 2020 & 2033

- Table 23: Global Adhesive Labels Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 24: Global Adhesive Labels Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 25: Germany Adhesive Labels Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 26: United Kingdom Adhesive Labels Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 27: France Adhesive Labels Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 28: Italy Adhesive Labels Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 29: Rest of Europe Adhesive Labels Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: Global Adhesive Labels Industry Revenue Million Forecast, by Adhesive Type 2020 & 2033

- Table 31: Global Adhesive Labels Industry Revenue Million Forecast, by Face Material 2020 & 2033

- Table 32: Global Adhesive Labels Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 33: Global Adhesive Labels Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 34: Brazil Adhesive Labels Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 35: Argentina Adhesive Labels Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 36: Rest of South America Adhesive Labels Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 37: Global Adhesive Labels Industry Revenue Million Forecast, by Adhesive Type 2020 & 2033

- Table 38: Global Adhesive Labels Industry Revenue Million Forecast, by Face Material 2020 & 2033

- Table 39: Global Adhesive Labels Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 40: Global Adhesive Labels Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 41: South Africa Adhesive Labels Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 42: Saudi Arabia Adhesive Labels Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 43: Rest of Middle East and Africa Adhesive Labels Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Adhesive Labels Industry?

The projected CAGR is approximately 5.47%.

2. Which companies are prominent players in the Adhesive Labels Industry?

Key companies in the market include LECTA, Optimum Group, HERMA, H B Fuller Company, Avery Dennison Corporation, Asteria Group, Fuji Seal International Inc, Thai KK Group, LINTEC Corporation, Mondi, UPM*List Not Exhaustive, 3M, Symbio Inc, CPC Haferkamp GmbH & Co KG.

3. What are the main segments of the Adhesive Labels Industry?

The market segments include Adhesive Type, Face Material, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD 50.35 Million as of 2022.

5. What are some drivers contributing to market growth?

Rapidly Growing E-commerce Industry; Increasing Demand for Packed Foods from Food and Beverage Industry; Other Drivers.

6. What are the notable trends driving market growth?

Increasing Demand from the Food and Beverage Industry.

7. Are there any restraints impacting market growth?

Increasing Government Regulations; Other Restraints.

8. Can you provide examples of recent developments in the market?

May 2022: Mondi announced switching glassine-based liners to certified base paper. It is to move to an environmentally benign supply chain and get a stronghold in European markets.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Adhesive Labels Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Adhesive Labels Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Adhesive Labels Industry?

To stay informed about further developments, trends, and reports in the Adhesive Labels Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence