Key Insights

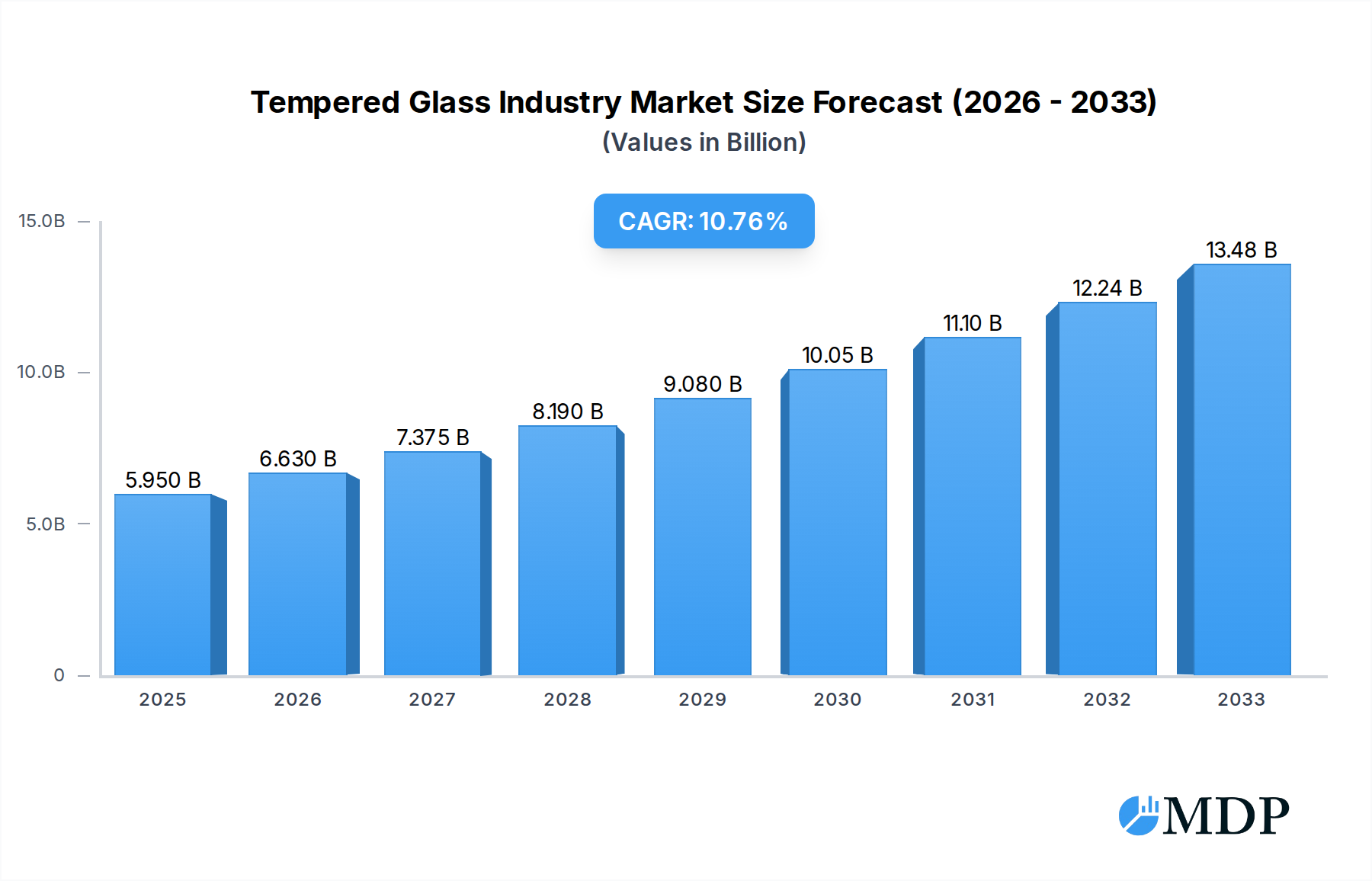

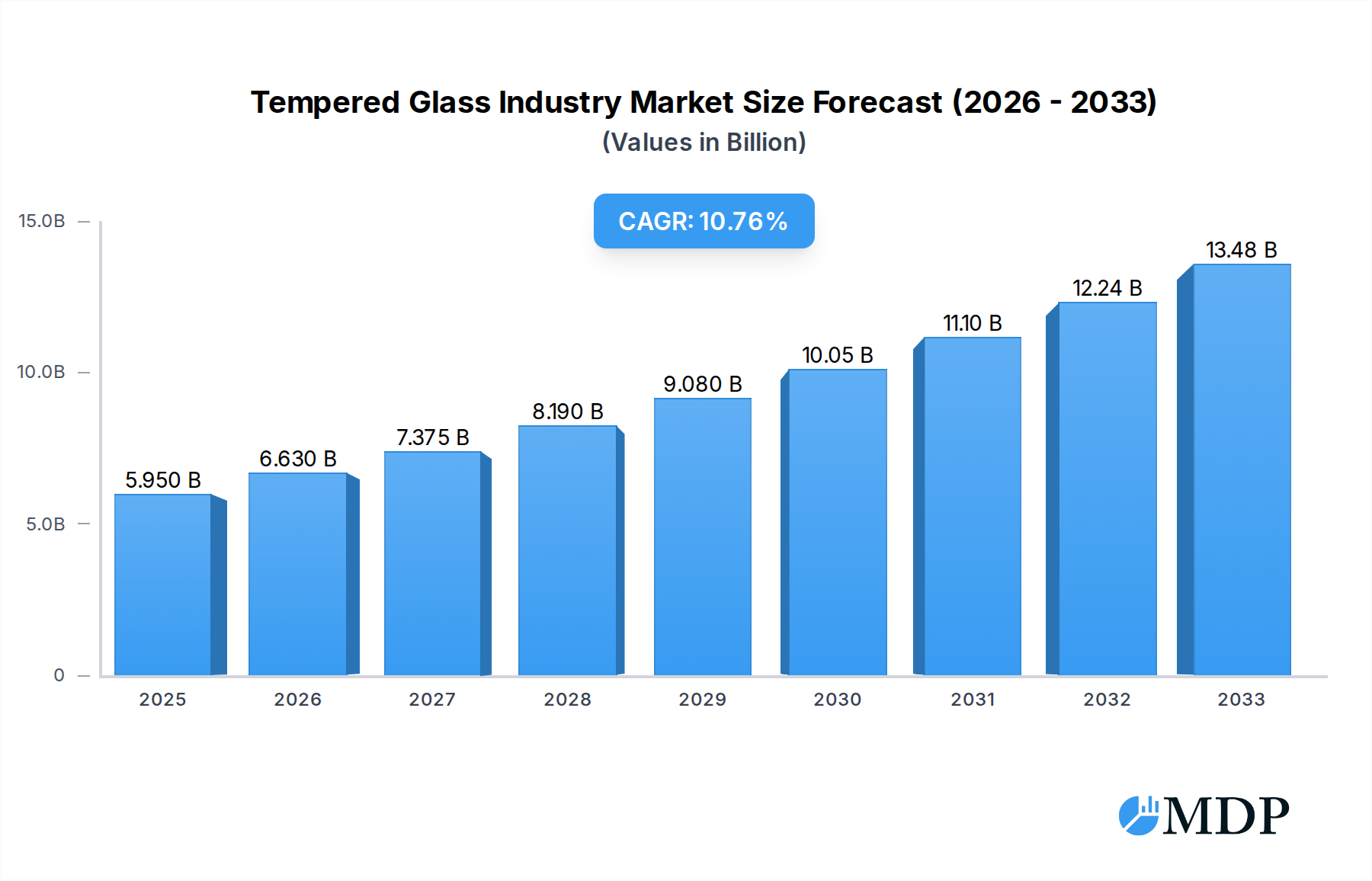

The global Tempered Glass market is poised for significant expansion, projected to reach $5.95 billion by 2025, demonstrating robust growth fueled by a compound annual growth rate (CAGR) of 11.51%. This impressive trajectory is driven by increasing demand across key end-user industries such as automotive, construction, and electronics, where the enhanced safety, durability, and aesthetic appeal of tempered glass are highly valued. In the automotive sector, the rising adoption of advanced driver-assistance systems (ADAS) necessitates the use of specialized glass for sensor integration, while the construction industry's focus on energy-efficient and secure buildings further propels demand. The electronics industry's continuous innovation in display technology also contributes to market growth, with tempered glass serving as a critical component for screens in smartphones, tablets, and other devices. Emerging applications in renewable energy, particularly in solar panels, also represent a nascent yet promising growth avenue.

Tempered Glass Industry Market Size (In Billion)

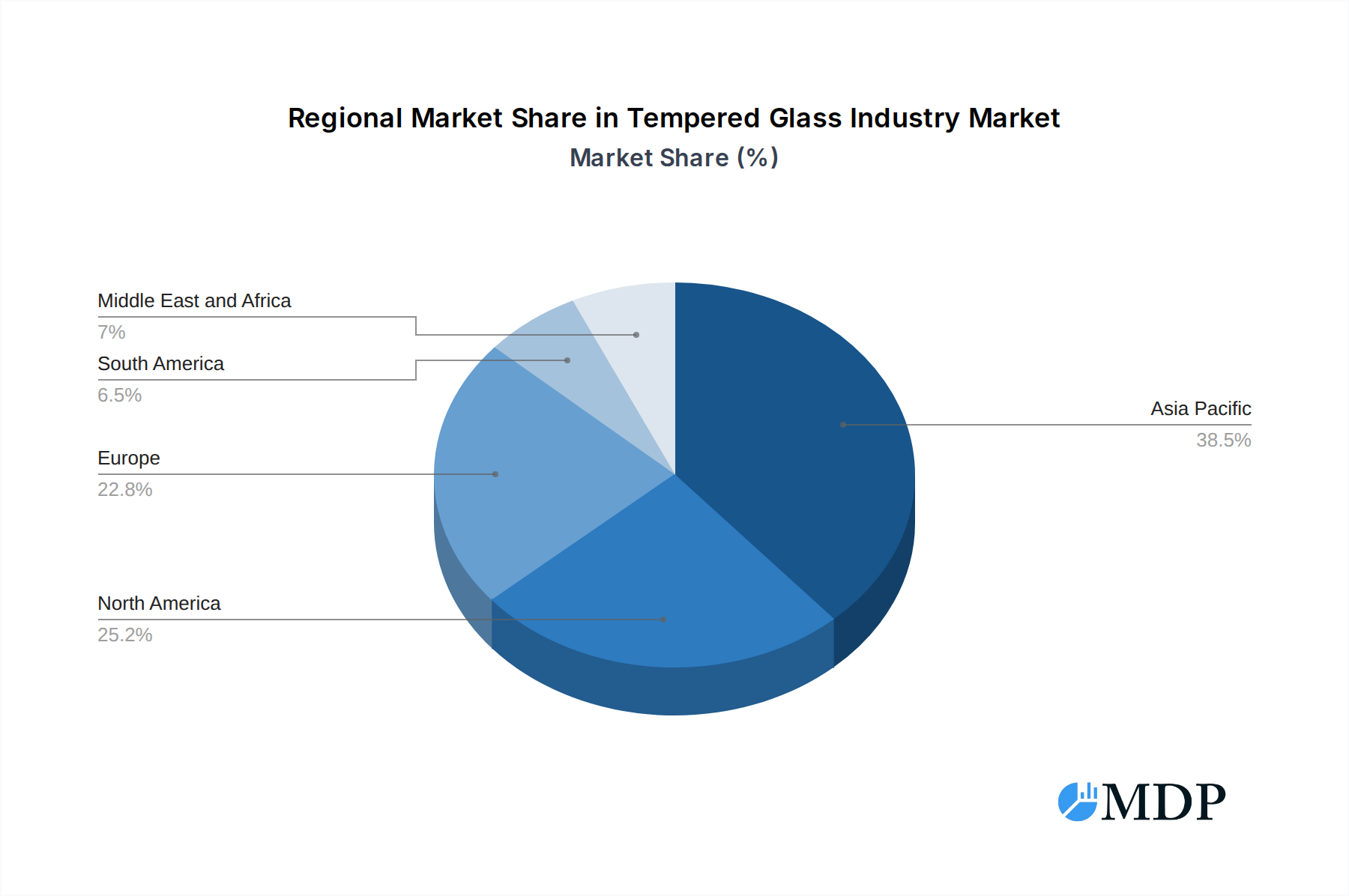

However, the market is not without its challenges. Fluctuations in raw material prices, particularly for high-purity silica, can impact manufacturing costs and profitability. Stringent environmental regulations concerning manufacturing processes and waste management can also pose compliance hurdles for industry players. Despite these restraints, the overarching trend towards enhanced safety standards and the increasing preference for high-performance materials are expected to outweigh these challenges. The Asia Pacific region, led by China and India, is anticipated to be a major growth engine due to rapid industrialization and increasing disposable incomes, further boosting the adoption of tempered glass across various applications. Key industry players like Nippon Sheet Glass Co Ltd, Saint-Gobain, and AGC Inc. are actively investing in research and development to innovate and expand their product portfolios to meet evolving market demands.

Tempered Glass Industry Company Market Share

Tempered Glass Industry Market Dynamics & Concentration

The tempered glass industry exhibits a moderate to high market concentration, with key players like Nippon Sheet Glass Co Ltd, Saint-Gobain, AGC Inc., and Guardian Glass LLC commanding significant market shares, estimated to be over 60% collectively in the historical period. Innovation remains a primary driver, fueled by advancements in safety standards, energy efficiency, and aesthetic appeal. Regulatory frameworks, particularly concerning building codes and automotive safety, are pivotal, often mandating the use of tempered glass. The threat of product substitutes, while present in some low-demand applications, is diminishing as tempered glass's superior strength and safety characteristics become increasingly recognized. End-user trends show a robust demand from the construction sector for architectural glazing and from the automotive industry for enhanced vehicle safety. Mergers and acquisitions (M&A) activity, with an estimated XX number of significant deals in the historical period, has played a crucial role in market consolidation, allowing larger entities to expand their product portfolios and geographical reach.

Tempered Glass Industry Industry Trends & Analysis

The global tempered glass market is poised for substantial growth, projected to expand at a Compound Annual Growth Rate (CAGR) of approximately 7.5% from the base year of 2025 through 2033. This impressive trajectory is driven by a confluence of factors, including escalating demand for safety-compliant materials across various end-user industries, particularly construction and automotive. Technological advancements are revolutionizing tempered glass production, leading to thinner, stronger, and more specialized variants that cater to sophisticated applications. For instance, the development of advanced coating technologies enhances thermal insulation and solar control properties, making tempered glass a preferred choice for energy-efficient buildings. Consumer preferences are increasingly leaning towards aesthetics and durability, further bolstering the adoption of tempered glass in residential and commercial spaces. The competitive landscape is characterized by intense innovation, with companies investing heavily in research and development to differentiate their offerings. Market penetration is high in developed economies, while emerging markets present significant untapped potential due to rapid urbanization and infrastructure development. The market size is projected to reach over USD 80 billion by 2033.

Leading Markets & Segments in Tempered Glass Industry

The construction segment stands as the dominant force within the tempered glass industry, accounting for an estimated 55% of the market share in the forecast period. This dominance is underpinned by global urbanization trends, increasing investments in infrastructure projects, and stringent building safety regulations that mandate the use of tempered glass for windows, doors, facades, and interior partitions. Economic policies promoting sustainable building practices and the adoption of energy-efficient materials further amplify this demand. Within the construction sector, architectural glazing, including curtain walls and skylights, represents a significant application.

The automotive sector emerges as the second-largest segment, driven by the continuous evolution of vehicle safety standards and the growing popularity of panoramic sunroofs and advanced driver-assistance systems (ADAS) that often incorporate tempered glass. Stringent safety regulations worldwide require the use of tempered glass for side and rear windows due to its shatter-resistant properties. The increasing production of electric vehicles (EVs), which often feature advanced designs and larger glass surfaces, also contributes to market expansion.

The electronics segment, while smaller, is experiencing robust growth, fueled by the proliferation of touch-screen devices such as smartphones, tablets, and smart displays. The demand for durable, scratch-resistant, and aesthetically pleasing display covers makes tempered glass an indispensable material.

Key Drivers for Dominance:

- Construction:

- Global population growth and urbanization.

- Government initiatives for infrastructure development and renovation.

- Increasing demand for energy-efficient and sustainable building materials.

- Stringent safety regulations in residential and commercial construction.

- Automotive:

- Mandatory automotive safety standards globally.

- Growing consumer preference for advanced vehicle features like panoramic roofs.

- The burgeoning electric vehicle market with its unique design requirements.

- Electronics:

- Ubiquitous adoption of smartphones, tablets, and other smart devices.

- Demand for durable and aesthetically superior display interfaces.

Tempered Glass Industry Product Developments

Recent product developments in the tempered glass industry focus on enhancing performance and expanding application versatility. Innovations include the development of ultra-thin tempered glass for flexible electronic displays and advanced anti-reflective coatings for improved optical clarity in architectural and automotive applications. Companies are also investing in toughened glass with enhanced thermal resistance and impact absorption capabilities, catering to specialized industrial and high-risk environments. The integration of smart functionalities, such as embedded heating elements for defogging or sensor integration, is also a growing trend, offering competitive advantages and opening new market niches.

Key Drivers of Tempered Glass Industry Growth

The tempered glass industry's growth is propelled by several key factors. Foremost is the unwavering emphasis on safety and security regulations across automotive and construction sectors, mandating its use for accident prevention and structural integrity. Technological advancements in glass manufacturing processes, leading to stronger, lighter, and more specialized tempered glass products, are also significant. Furthermore, the rising disposable incomes and urbanization in emerging economies are driving demand for enhanced building materials and modern vehicle designs. The increasing adoption of smart devices, requiring durable and aesthetically pleasing screens, also contributes substantially to market expansion.

Challenges in the Tempered Glass Industry Market

Despite robust growth, the tempered glass industry faces several challenges. Fluctuations in raw material prices, particularly for high-purity silica, can impact profitability. Intense competition among manufacturers leads to price pressures, potentially affecting profit margins. Evolving regulatory landscapes, while often driving demand, can also impose additional compliance costs. Furthermore, supply chain disruptions, as witnessed in recent global events, can hinder production and timely delivery, impacting customer satisfaction. The high energy consumption associated with the tempering process also presents an ongoing environmental and cost consideration for manufacturers.

Emerging Opportunities in Tempered Glass Industry

The tempered glass industry is ripe with emerging opportunities. The burgeoning renewable energy sector presents a significant avenue through increased demand for tempered glass in solar panels, requiring enhanced durability and light transmission. The rapid growth of the smart home and building automation markets offers opportunities for integrating sensors and smart functionalities into architectural glass. Furthermore, advancements in nanotechnology are enabling the development of self-cleaning and anti-microbial tempered glass surfaces, catering to hygiene-conscious applications. Strategic partnerships between glass manufacturers and technology providers can unlock innovative solutions for sectors like aerospace and advanced defense.

Leading Players in the Tempered Glass Industry Sector

- Nippon Sheet Glass Co Ltd

- Saint-Gobain

- Airxcel Inc

- Asahimas Flat Glass

- Asahi India Glass Limited

- TOMAKK GLASS PARTNERS LLC

- GUARDIAN GLASS LLC

- GSC GLASS LTD

- KIBING GROUP

- AGC Inc

- CARDINAL GLASS INDUSTRIES INC

- Abrisa Technologies

- SCHOTT AG

Key Milestones in Tempered Glass Industry Industry

- January 2023: AGC develops digital twin technology (CADTANK Online Computation and Optimization Assistant (COCOA)) for the glass melting process and starts flotation furnace operational verification. This technology makes it easy to get a quick and detailed understanding of how glass is melted and a first look at the manufacturing conditions, enhancing process efficiency and quality control.

- December 2022: The Guardian Glass Company launched the new Guardian Glass Resource Hub, which offers 24/7 online access to technical information, analytical tools, and training. It provides critical information on dealing with thermal stress, glass bending, condensation, and cleaning, empowering industry professionals and improving product application.

Strategic Outlook for Tempered Glass Industry Market

The strategic outlook for the tempered glass industry is exceptionally promising, driven by sustained demand from its core sectors and the emergence of new application areas. Companies are focusing on innovation to develop high-performance, value-added products that meet stringent safety and sustainability requirements. Expansion into emerging markets, particularly in Asia-Pacific and Latin America, represents a significant growth lever. Strategic collaborations and vertical integration are expected to further solidify market positions. Embracing digital transformation and Industry 4.0 principles will be crucial for optimizing manufacturing processes, enhancing customer service, and maintaining a competitive edge in this dynamic global market.

Tempered Glass Industry Segmentation

-

1. End-user Industry

- 1.1. Automotive

- 1.2. Construction

- 1.3. Electronics

- 1.4. Other End-user Industries

Tempered Glass Industry Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. India

- 1.3. Japan

- 1.4. South Korea

- 1.5. Rest of Asia Pacific

-

2. North America

- 2.1. United States

- 2.2. Canada

- 2.3. Mexico

-

3. Europe

- 3.1. Germany

- 3.2. United Kingdom

- 3.3. France

- 3.4. Italy

- 3.5. Rest of Europe

-

4. South America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Rest of South America

-

5. Middle East and Africa

- 5.1. Saudi Arabia

- 5.2. South Africa

- 5.3. Rest of Middle East and Africa

Tempered Glass Industry Regional Market Share

Geographic Coverage of Tempered Glass Industry

Tempered Glass Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 11.51% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by End-user Industry

- 5.1.1. Automotive

- 5.1.2. Construction

- 5.1.3. Electronics

- 5.1.4. Other End-user Industries

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Asia Pacific

- 5.2.2. North America

- 5.2.3. Europe

- 5.2.4. South America

- 5.2.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by End-user Industry

- 6. Global Tempered Glass Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by End-user Industry

- 6.1.1. Automotive

- 6.1.2. Construction

- 6.1.3. Electronics

- 6.1.4. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by End-user Industry

- 7. Asia Pacific Tempered Glass Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by End-user Industry

- 7.1.1. Automotive

- 7.1.2. Construction

- 7.1.3. Electronics

- 7.1.4. Other End-user Industries

- 7.1. Market Analysis, Insights and Forecast - by End-user Industry

- 8. North America Tempered Glass Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by End-user Industry

- 8.1.1. Automotive

- 8.1.2. Construction

- 8.1.3. Electronics

- 8.1.4. Other End-user Industries

- 8.1. Market Analysis, Insights and Forecast - by End-user Industry

- 9. Europe Tempered Glass Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by End-user Industry

- 9.1.1. Automotive

- 9.1.2. Construction

- 9.1.3. Electronics

- 9.1.4. Other End-user Industries

- 9.1. Market Analysis, Insights and Forecast - by End-user Industry

- 10. South America Tempered Glass Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by End-user Industry

- 10.1.1. Automotive

- 10.1.2. Construction

- 10.1.3. Electronics

- 10.1.4. Other End-user Industries

- 10.1. Market Analysis, Insights and Forecast - by End-user Industry

- 11. Middle East and Africa Tempered Glass Industry Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by End-user Industry

- 11.1.1. Automotive

- 11.1.2. Construction

- 11.1.3. Electronics

- 11.1.4. Other End-user Industries

- 11.1. Market Analysis, Insights and Forecast - by End-user Industry

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Nippon Sheet Glass Co Ltd

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Saint-Gobain

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Airxcel Inc

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Asahimas Flat Glass

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 Asahi India Glass Limited

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 TOMAKK GLASS PARTNERS LLC*List Not Exhaustive

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 GUARDIAN GLASS LLC

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 GSC GLASS LTD

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 KIBING GROUP

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 AGC Inc

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 CARDINAL GLASS INDUSTRIES INC

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 Abrisa Technologies

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 SCHOTT AG

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.1 Nippon Sheet Glass Co Ltd

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Tempered Glass Industry Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: Asia Pacific Tempered Glass Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 3: Asia Pacific Tempered Glass Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 4: Asia Pacific Tempered Glass Industry Revenue (billion), by Country 2025 & 2033

- Figure 5: Asia Pacific Tempered Glass Industry Revenue Share (%), by Country 2025 & 2033

- Figure 6: North America Tempered Glass Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 7: North America Tempered Glass Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 8: North America Tempered Glass Industry Revenue (billion), by Country 2025 & 2033

- Figure 9: North America Tempered Glass Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Tempered Glass Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 11: Europe Tempered Glass Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 12: Europe Tempered Glass Industry Revenue (billion), by Country 2025 & 2033

- Figure 13: Europe Tempered Glass Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: South America Tempered Glass Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 15: South America Tempered Glass Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 16: South America Tempered Glass Industry Revenue (billion), by Country 2025 & 2033

- Figure 17: South America Tempered Glass Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Middle East and Africa Tempered Glass Industry Revenue (billion), by End-user Industry 2025 & 2033

- Figure 19: Middle East and Africa Tempered Glass Industry Revenue Share (%), by End-user Industry 2025 & 2033

- Figure 20: Middle East and Africa Tempered Glass Industry Revenue (billion), by Country 2025 & 2033

- Figure 21: Middle East and Africa Tempered Glass Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Tempered Glass Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 2: Global Tempered Glass Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 3: Global Tempered Glass Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 4: Global Tempered Glass Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 5: China Tempered Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 6: India Tempered Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 7: Japan Tempered Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: South Korea Tempered Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Rest of Asia Pacific Tempered Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Tempered Glass Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 11: Global Tempered Glass Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 12: United States Tempered Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 13: Canada Tempered Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Mexico Tempered Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Global Tempered Glass Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 16: Global Tempered Glass Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 17: Germany Tempered Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 18: United Kingdom Tempered Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 19: France Tempered Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Italy Tempered Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: Rest of Europe Tempered Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Global Tempered Glass Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 23: Global Tempered Glass Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 24: Brazil Tempered Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Argentina Tempered Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Rest of South America Tempered Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Global Tempered Glass Industry Revenue billion Forecast, by End-user Industry 2020 & 2033

- Table 28: Global Tempered Glass Industry Revenue billion Forecast, by Country 2020 & 2033

- Table 29: Saudi Arabia Tempered Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 30: South Africa Tempered Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

- Table 31: Rest of Middle East and Africa Tempered Glass Industry Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Tempered Glass Industry?

The projected CAGR is approximately 11.51%.

2. Which companies are prominent players in the Tempered Glass Industry?

Key companies in the market include Nippon Sheet Glass Co Ltd, Saint-Gobain, Airxcel Inc, Asahimas Flat Glass, Asahi India Glass Limited, TOMAKK GLASS PARTNERS LLC*List Not Exhaustive, GUARDIAN GLASS LLC, GSC GLASS LTD, KIBING GROUP, AGC Inc, CARDINAL GLASS INDUSTRIES INC, Abrisa Technologies, SCHOTT AG.

3. What are the main segments of the Tempered Glass Industry?

The market segments include End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD 5.95 billion as of 2022.

5. What are some drivers contributing to market growth?

Growing Demand from the Construction Industry; Other Drivers.

6. What are the notable trends driving market growth?

Growing Demand from the Construction Industry.

7. Are there any restraints impacting market growth?

Increasing Use of Other Light Weight Products; Other Restraints.

8. Can you provide examples of recent developments in the market?

January 2023: AGC develops digital twin technology (CADTANK Online Computation and Optimization Assistant (COCOA)) for the glass melting process and starts flotation furnace operational verification. This technology makes it easy to get a quick and detailed understanding of how glass is melted and a first look at the manufacturing conditions.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Tempered Glass Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Tempered Glass Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Tempered Glass Industry?

To stay informed about further developments, trends, and reports in the Tempered Glass Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence