Key Insights

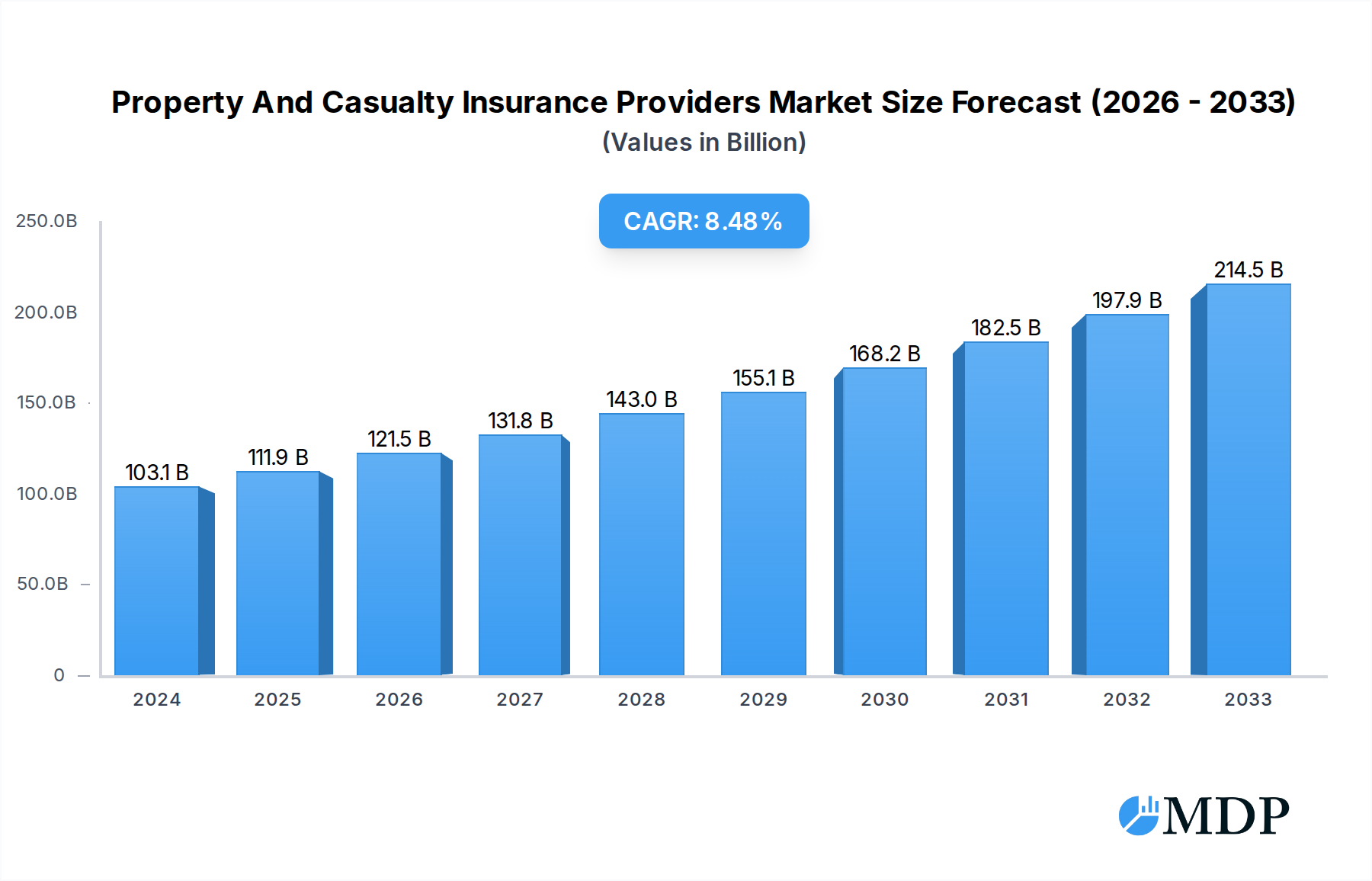

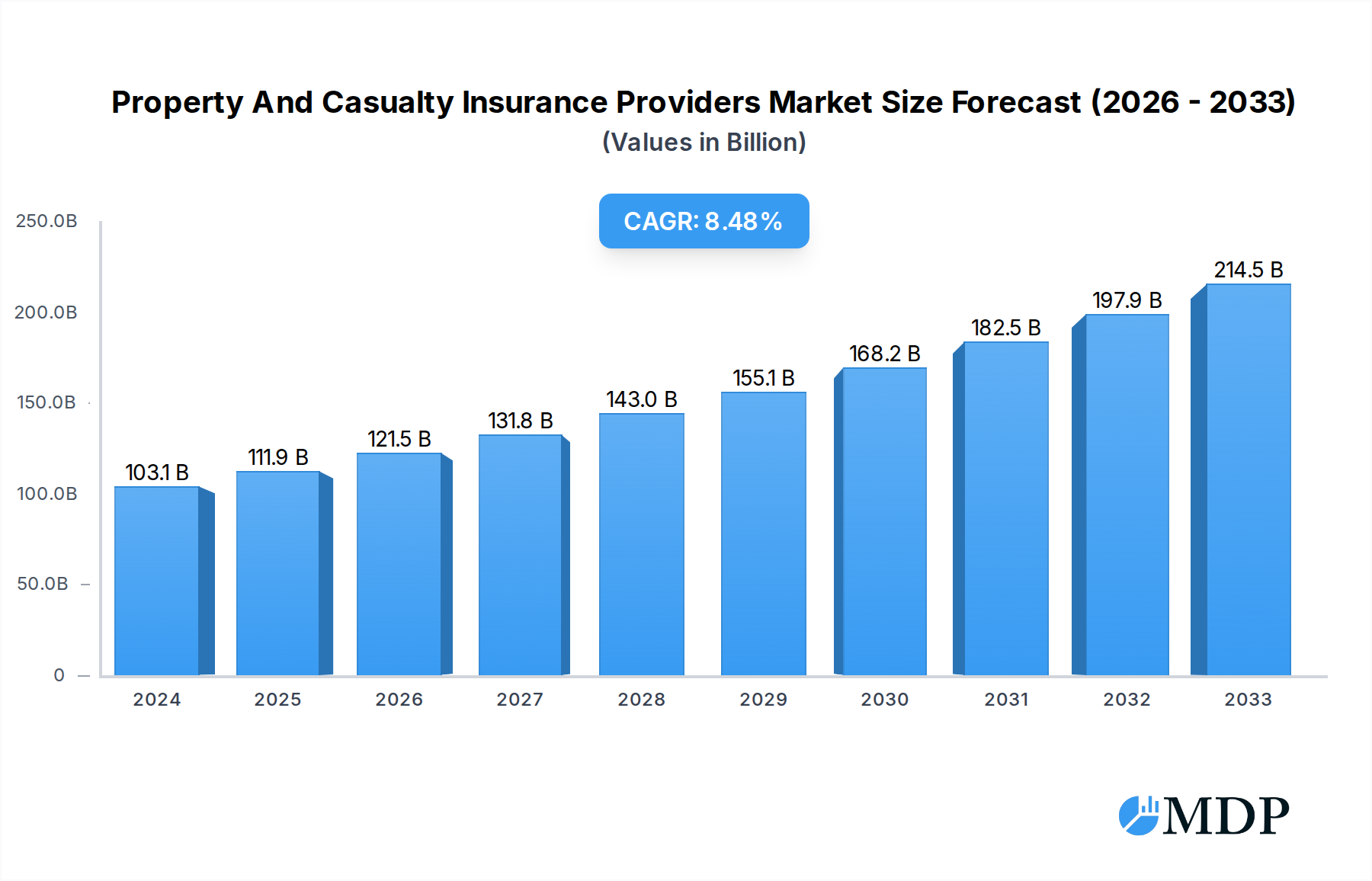

The Property and Casualty (P&C) insurance sector is poised for robust expansion, with the global market size estimated at $103.1 billion in 2024. Driven by escalating global economic activity, increasing awareness of risk management, and the growing adoption of digital technologies in claims processing and customer service, the industry is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.8%. This significant growth is fueled by the increasing complexity of risks faced by businesses and individuals, necessitating comprehensive P&C insurance solutions. Key drivers include the rising prevalence of natural disasters, cyber threats, and evolving regulatory landscapes that mandate certain types of coverage. Furthermore, the expanding middle class in emerging economies and increased disposable income are boosting demand for homeowner and auto insurance, directly contributing to market expansion. The competitive landscape is characterized by prominent players like Allstate, Berkshire Hathaway, Liberty Mutual, and Travelers Companies, all actively investing in innovation and customer-centric approaches to capture market share.

Property And Casualty Insurance Providers Market Size (In Billion)

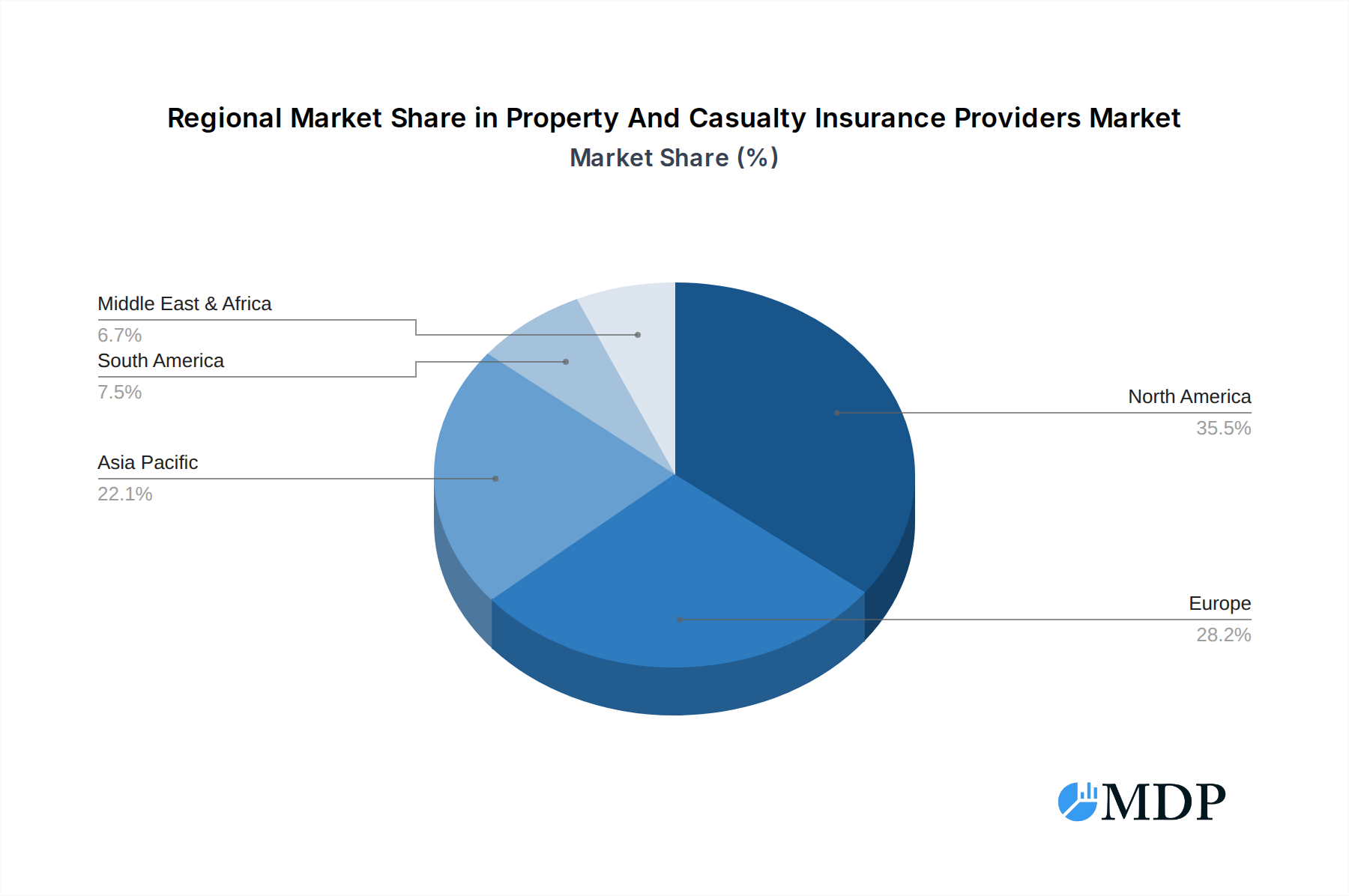

The P&C insurance market is segmented across various applications, including intermediary and direct selling channels, catering to diverse customer needs. Key insurance types within this market encompass automobile, malpractice/indemnity, fidelity, mortgage guaranty, homeowners, surety, and liability insurance. Each segment presents unique growth opportunities and challenges, influenced by specific industry dynamics and regulatory frameworks. For instance, the growing sophistication of cyberattacks is driving demand for specialized cyber liability insurance, while increasing infrastructure development worldwide is spurring growth in surety and construction-related insurance. Geographically, North America currently holds a significant market share, with the United States leading the way. However, the Asia Pacific region is anticipated to exhibit the fastest growth due to rapid industrialization, urbanization, and a burgeoning middle class. Europe also represents a mature yet substantial market, with ongoing digital transformation efforts enhancing efficiency and customer experience.

Property And Casualty Insurance Providers Company Market Share

Here is the SEO-optimized, engaging report description for Property and Casualty Insurance Providers:

This comprehensive report offers an in-depth analysis of the global Property and Casualty (P&C) Insurance Providers market, providing critical insights for stakeholders navigating this dynamic industry. With a study period spanning 2019 to 2033, a base year of 2025, and a forecast period from 2025 to 2033, this report delves into historical trends, current market conditions, and future projections. We analyze key segments including Application: Intermediary, Direct Selling and delve into critical Types: Automobile Insurance Carriers, Malpractice/Indemnity Insurance Carriers, Fidelity Insurance Carriers, Mortgage Guaranty Insurance Carriers, Homeowners Insurance Carriers, Surety Insurance Carriers, Liability Insurance Carriers. The report highlights significant industry developments and provides actionable intelligence on market concentration, innovation drivers, and regulatory frameworks. Prepare to gain a competitive edge with data-driven strategies and a clear understanding of the forces shaping the P&C insurance landscape. This report is essential for insurers, reinsurers, brokers, investors, and regulatory bodies seeking to optimize their strategies in a multi-billion dollar market projected for substantial growth.

Property And Casualty Insurance Providers Market Dynamics & Concentration

The Property and Casualty (P&C) Insurance Providers market is characterized by a moderate to high level of concentration, with key players like Allstate, Berkshire Hathaway, Liberty Mutual, and Travelers Companies holding significant market shares. In the historical period (2019-2024), the market has seen ongoing consolidation and strategic M&A activities aimed at expanding geographic reach and product portfolios. For instance, M&A deal counts in the P&C sector have averaged 500+ deals annually during this period, with deal values often in the billions of dollars. Innovation drivers are increasingly centered on digital transformation, with providers investing heavily in AI-powered underwriting, personalized customer experiences, and advanced risk assessment tools to gain a competitive advantage. Regulatory frameworks remain a critical aspect, with evolving compliance requirements impacting solvency, data privacy, and consumer protection. Product substitutes, such as self-insurance and alternative risk transfer mechanisms, are gaining traction, forcing P&C providers to enhance their value propositions. End-user trends highlight a growing demand for integrated, digital-first insurance solutions and a greater emphasis on risk mitigation services.

Property And Casualty Insurance Providers Industry Trends & Analysis

The Property and Casualty Insurance Providers market is poised for robust expansion, driven by a confluence of economic, technological, and societal factors. The Compound Annual Growth Rate (CAGR) is projected to be 6.5% for the forecast period (2025-2033), signifying a multi-billion dollar industry experiencing sustained momentum. This growth is fueled by increasing disposable incomes, a rising global population, and a growing awareness of the need for financial protection against unforeseen events. Technological disruptions are at the forefront of this evolution. Insurtech innovations, including artificial intelligence (AI) for claims processing and underwriting, telematics for personalized auto insurance, and blockchain for enhanced transparency and security, are fundamentally reshaping operational efficiency and customer engagement. The market penetration of digital insurance platforms has seen a significant surge, with an estimated 70% of new policy purchases initiated online by 2025. Consumer preferences are shifting towards more personalized and accessible insurance products. Customers now expect seamless digital onboarding, real-time policy management, and proactive risk advice. The competitive dynamics are intensifying, with traditional insurers facing pressure from agile insurtech startups and non-traditional players entering the market. This necessitates a strategic focus on customer-centricity, data analytics, and the development of innovative, value-added services beyond basic coverage. The market size is expected to reach over $7 trillion by 2033.

Leading Markets & Segments in Property And Casualty Insurance Providers

The Property and Casualty Insurance Providers market exhibits distinct regional dominance and segment performance. North America continues to be a leading market, driven by a mature insurance infrastructure, robust economic policies, and a high level of consumer demand for various insurance types. Within North America, the United States represents a significant portion of the global P&C market, with an estimated market size of $1.8 trillion in 2025.

Key segment analysis reveals:

- Automobile Insurance Carriers: This segment remains a cornerstone of the P&C market, with its dominance driven by high vehicle ownership rates and the mandatory nature of auto insurance in most jurisdictions. The growth in this segment is further propelled by advancements in telematics and the increasing adoption of electric vehicles.

- Homeowners Insurance Carriers: Experiencing steady growth, this segment is influenced by real estate market trends, urbanization, and the increasing frequency of natural disasters, which underscores the critical need for property protection. Infrastructure development and government initiatives promoting homeownership also contribute significantly.

- Liability Insurance Carriers: This segment is crucial for businesses across all sectors, driven by increasing litigation and evolving regulatory landscapes. Growing awareness of corporate responsibility and product liability fuels demand.

- Malpractice/Indemnity Insurance Carriers: Essential for healthcare professionals and other service providers, this segment's growth is linked to the expansion of the healthcare industry and the complex legal environments professionals operate within.

- Mortgage Guaranty Insurance Carriers: While closely tied to the real estate market, this segment plays a vital role in facilitating homeownership by insuring lenders against borrower default.

- Fidelity Insurance Carriers: Protecting businesses against financial losses due to employee dishonesty and fraud, this segment's relevance grows with the complexity of financial transactions and the increasing threat of cyber-enabled fraud.

- Surety Insurance Carriers: Essential for construction projects and government contracts, this segment's performance is closely aligned with infrastructure spending and economic development initiatives.

The Direct Selling application channel is witnessing accelerated growth due to advancements in digital platforms and a preference for end-to-end online customer journeys. Conversely, the Intermediary channel, comprising agents and brokers, continues to hold substantial sway, particularly for complex insurance needs and for customers seeking personalized advice.

Property And Casualty Insurance Providers Product Developments

Product innovation in the P&C insurance sector is rapidly evolving, focusing on enhanced customer value and competitive differentiation. Key developments include the integration of AI and IoT for real-time risk assessment and personalized pricing, especially in automobile insurance carriers through telematics, and in homeowners insurance carriers via smart home devices. Cyber insurance products are gaining significant traction as businesses increasingly face digital threats, offering tailored protection against data breaches and cyberattacks. Insurers are also developing parametric insurance solutions for quicker payouts in cases of natural disasters. The competitive advantage lies in offering agile, digital-first products with embedded services that go beyond traditional coverage, such as preventative risk management advice and seamless claims processing.

Key Drivers of Property And Casualty Insurance Providers Growth

Several key drivers are propelling the growth of the Property and Casualty Insurance Providers market. Technological advancements, particularly in AI, machine learning, and big data analytics, are enabling more accurate risk assessment, personalized pricing, and efficient claims processing. Economic growth, including rising disposable incomes and increased business activity, translates to greater demand for insurance products across various sectors. Evolving regulatory frameworks, while presenting challenges, can also spur growth by creating new markets for compliance-related insurance. Furthermore, increasing awareness of climate change and natural disasters is driving demand for comprehensive homeowners insurance carriers and specialized liability insurance carriers. The expansion of the gig economy and new business models also necessitates tailored insurance solutions.

Challenges in the Property And Casualty Insurance Providers Market

The Property and Casualty Insurance Providers market faces several significant challenges that could hinder growth. Stringent and evolving regulatory hurdles across different jurisdictions can increase compliance costs and complexity. Persistent supply chain issues, particularly in sectors like automotive and construction, can impact claims costs and lead times for repairs. Intense competitive pressures from established players and agile insurtech startups demand continuous innovation and cost optimization. The increasing frequency and severity of natural disasters, exacerbated by climate change, are leading to higher claims payouts and impacting the profitability of homeowners insurance carriers and automobile insurance carriers. Furthermore, the growing threat of cyberattacks poses a substantial risk to insurers, necessitating significant investments in cybersecurity and specialized fidelity insurance carriers and liability insurance carriers.

Emerging Opportunities in Property And Casualty Insurance Providers

Emerging opportunities within the Property and Casualty Insurance Providers market are vast and primarily driven by technological breakthroughs and evolving societal needs. The pervasive adoption of IoT devices, from smart homes to connected vehicles, presents an immense opportunity for data-driven underwriting and personalized insurance offerings. Strategic partnerships between traditional insurers and insurtech companies are creating innovative solutions and expanding market reach. The growing awareness of environmental, social, and governance (ESG) factors is also creating new product development avenues, such as coverage for renewable energy projects and climate resilience initiatives. Market expansion into emerging economies with growing middle classes and increasing demand for financial protection offers significant long-term growth potential.

Leading Players in the Property And Casualty Insurance Providers Sector

- Allstate

- Berkshire Hathaway

- Liberty Mutual

- Travelers Companies

Key Milestones in Property And Casualty Insurance Providers Industry

- 2019: Increased investment in AI and machine learning for underwriting and claims processing across major providers.

- 2020: Surge in demand for cyber insurance due to the rise of remote work and increased cyber threats.

- 2021: Significant M&A activity as larger insurers acquire insurtech startups to enhance digital capabilities.

- 2022: Growing focus on parametric insurance solutions for faster payouts following natural disasters.

- 2023: Expansion of usage-based insurance (UBI) programs in the automobile insurance carriers segment.

- 2024: Heightened awareness and product development for climate-related risks, impacting homeowners insurance carriers.

Strategic Outlook for Property And Casualty Insurance Providers Market

The strategic outlook for the Property and Casualty Insurance Providers market is one of dynamic evolution and significant growth. The focus will increasingly be on leveraging advanced analytics and AI to personalize customer experiences and optimize operational efficiency. Insurers that embrace digital transformation, invest in innovative product development for emerging risks like cyber threats and climate change, and forge strategic partnerships will be best positioned for success. Market expansion into underserved regions and a continued emphasis on customer-centricity will be crucial growth accelerators. The industry is moving towards a more proactive, service-oriented model, where insurance providers act as risk mitigation partners rather than just payers of claims.

Property And Casualty Insurance Providers Segmentation

-

1. Application

- 1.1. Intermediary

- 1.2. Direct Selling

-

2. Types

- 2.1. Automobile Insurance Carriers

- 2.2. Malpractice/Indemnity Insurance Carriers

- 2.3. Fidelity Insurance Carriers

- 2.4. Mortgage Guaranty Insurance Carriers

- 2.5. Homeowners Insurance Carriers

- 2.6. Surety Insurance Carriers

- 2.7. Liability Insurance Carriers

Property And Casualty Insurance Providers Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Property And Casualty Insurance Providers Regional Market Share

Geographic Coverage of Property And Casualty Insurance Providers

Property And Casualty Insurance Providers REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.8% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Intermediary

- 5.1.2. Direct Selling

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Automobile Insurance Carriers

- 5.2.2. Malpractice/Indemnity Insurance Carriers

- 5.2.3. Fidelity Insurance Carriers

- 5.2.4. Mortgage Guaranty Insurance Carriers

- 5.2.5. Homeowners Insurance Carriers

- 5.2.6. Surety Insurance Carriers

- 5.2.7. Liability Insurance Carriers

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Property And Casualty Insurance Providers Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Intermediary

- 6.1.2. Direct Selling

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Automobile Insurance Carriers

- 6.2.2. Malpractice/Indemnity Insurance Carriers

- 6.2.3. Fidelity Insurance Carriers

- 6.2.4. Mortgage Guaranty Insurance Carriers

- 6.2.5. Homeowners Insurance Carriers

- 6.2.6. Surety Insurance Carriers

- 6.2.7. Liability Insurance Carriers

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Property And Casualty Insurance Providers Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Intermediary

- 7.1.2. Direct Selling

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Automobile Insurance Carriers

- 7.2.2. Malpractice/Indemnity Insurance Carriers

- 7.2.3. Fidelity Insurance Carriers

- 7.2.4. Mortgage Guaranty Insurance Carriers

- 7.2.5. Homeowners Insurance Carriers

- 7.2.6. Surety Insurance Carriers

- 7.2.7. Liability Insurance Carriers

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Property And Casualty Insurance Providers Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Intermediary

- 8.1.2. Direct Selling

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Automobile Insurance Carriers

- 8.2.2. Malpractice/Indemnity Insurance Carriers

- 8.2.3. Fidelity Insurance Carriers

- 8.2.4. Mortgage Guaranty Insurance Carriers

- 8.2.5. Homeowners Insurance Carriers

- 8.2.6. Surety Insurance Carriers

- 8.2.7. Liability Insurance Carriers

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Property And Casualty Insurance Providers Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Intermediary

- 9.1.2. Direct Selling

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Automobile Insurance Carriers

- 9.2.2. Malpractice/Indemnity Insurance Carriers

- 9.2.3. Fidelity Insurance Carriers

- 9.2.4. Mortgage Guaranty Insurance Carriers

- 9.2.5. Homeowners Insurance Carriers

- 9.2.6. Surety Insurance Carriers

- 9.2.7. Liability Insurance Carriers

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Property And Casualty Insurance Providers Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Intermediary

- 10.1.2. Direct Selling

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Automobile Insurance Carriers

- 10.2.2. Malpractice/Indemnity Insurance Carriers

- 10.2.3. Fidelity Insurance Carriers

- 10.2.4. Mortgage Guaranty Insurance Carriers

- 10.2.5. Homeowners Insurance Carriers

- 10.2.6. Surety Insurance Carriers

- 10.2.7. Liability Insurance Carriers

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Property And Casualty Insurance Providers Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Intermediary

- 11.1.2. Direct Selling

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. Automobile Insurance Carriers

- 11.2.2. Malpractice/Indemnity Insurance Carriers

- 11.2.3. Fidelity Insurance Carriers

- 11.2.4. Mortgage Guaranty Insurance Carriers

- 11.2.5. Homeowners Insurance Carriers

- 11.2.6. Surety Insurance Carriers

- 11.2.7. Liability Insurance Carriers

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Allstate

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Berkshire Hathaway

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Liberty Mutual

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Travelers Companies

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.1 Allstate

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Property And Casualty Insurance Providers Revenue Breakdown (billion, %) by Region 2025 & 2033

- Figure 2: North America Property And Casualty Insurance Providers Revenue (billion), by Application 2025 & 2033

- Figure 3: North America Property And Casualty Insurance Providers Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Property And Casualty Insurance Providers Revenue (billion), by Types 2025 & 2033

- Figure 5: North America Property And Casualty Insurance Providers Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Property And Casualty Insurance Providers Revenue (billion), by Country 2025 & 2033

- Figure 7: North America Property And Casualty Insurance Providers Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Property And Casualty Insurance Providers Revenue (billion), by Application 2025 & 2033

- Figure 9: South America Property And Casualty Insurance Providers Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Property And Casualty Insurance Providers Revenue (billion), by Types 2025 & 2033

- Figure 11: South America Property And Casualty Insurance Providers Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Property And Casualty Insurance Providers Revenue (billion), by Country 2025 & 2033

- Figure 13: South America Property And Casualty Insurance Providers Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Property And Casualty Insurance Providers Revenue (billion), by Application 2025 & 2033

- Figure 15: Europe Property And Casualty Insurance Providers Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Property And Casualty Insurance Providers Revenue (billion), by Types 2025 & 2033

- Figure 17: Europe Property And Casualty Insurance Providers Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Property And Casualty Insurance Providers Revenue (billion), by Country 2025 & 2033

- Figure 19: Europe Property And Casualty Insurance Providers Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Property And Casualty Insurance Providers Revenue (billion), by Application 2025 & 2033

- Figure 21: Middle East & Africa Property And Casualty Insurance Providers Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Property And Casualty Insurance Providers Revenue (billion), by Types 2025 & 2033

- Figure 23: Middle East & Africa Property And Casualty Insurance Providers Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Property And Casualty Insurance Providers Revenue (billion), by Country 2025 & 2033

- Figure 25: Middle East & Africa Property And Casualty Insurance Providers Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Property And Casualty Insurance Providers Revenue (billion), by Application 2025 & 2033

- Figure 27: Asia Pacific Property And Casualty Insurance Providers Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Property And Casualty Insurance Providers Revenue (billion), by Types 2025 & 2033

- Figure 29: Asia Pacific Property And Casualty Insurance Providers Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Property And Casualty Insurance Providers Revenue (billion), by Country 2025 & 2033

- Figure 31: Asia Pacific Property And Casualty Insurance Providers Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Property And Casualty Insurance Providers Revenue billion Forecast, by Application 2020 & 2033

- Table 2: Global Property And Casualty Insurance Providers Revenue billion Forecast, by Types 2020 & 2033

- Table 3: Global Property And Casualty Insurance Providers Revenue billion Forecast, by Region 2020 & 2033

- Table 4: Global Property And Casualty Insurance Providers Revenue billion Forecast, by Application 2020 & 2033

- Table 5: Global Property And Casualty Insurance Providers Revenue billion Forecast, by Types 2020 & 2033

- Table 6: Global Property And Casualty Insurance Providers Revenue billion Forecast, by Country 2020 & 2033

- Table 7: United States Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 8: Canada Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 9: Mexico Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 10: Global Property And Casualty Insurance Providers Revenue billion Forecast, by Application 2020 & 2033

- Table 11: Global Property And Casualty Insurance Providers Revenue billion Forecast, by Types 2020 & 2033

- Table 12: Global Property And Casualty Insurance Providers Revenue billion Forecast, by Country 2020 & 2033

- Table 13: Brazil Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 14: Argentina Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 16: Global Property And Casualty Insurance Providers Revenue billion Forecast, by Application 2020 & 2033

- Table 17: Global Property And Casualty Insurance Providers Revenue billion Forecast, by Types 2020 & 2033

- Table 18: Global Property And Casualty Insurance Providers Revenue billion Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 20: Germany Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 21: France Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 22: Italy Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 23: Spain Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 24: Russia Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 25: Benelux Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 26: Nordics Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 28: Global Property And Casualty Insurance Providers Revenue billion Forecast, by Application 2020 & 2033

- Table 29: Global Property And Casualty Insurance Providers Revenue billion Forecast, by Types 2020 & 2033

- Table 30: Global Property And Casualty Insurance Providers Revenue billion Forecast, by Country 2020 & 2033

- Table 31: Turkey Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 32: Israel Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 33: GCC Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 34: North Africa Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 35: South Africa Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 37: Global Property And Casualty Insurance Providers Revenue billion Forecast, by Application 2020 & 2033

- Table 38: Global Property And Casualty Insurance Providers Revenue billion Forecast, by Types 2020 & 2033

- Table 39: Global Property And Casualty Insurance Providers Revenue billion Forecast, by Country 2020 & 2033

- Table 40: China Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 41: India Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 42: Japan Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 43: South Korea Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 45: Oceania Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Property And Casualty Insurance Providers Revenue (billion) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Property And Casualty Insurance Providers?

The projected CAGR is approximately 8.8%.

2. Which companies are prominent players in the Property And Casualty Insurance Providers?

Key companies in the market include Allstate, Berkshire Hathaway, Liberty Mutual, Travelers Companies.

3. What are the main segments of the Property And Casualty Insurance Providers?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD 103.1 billion as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3350.00, USD 5025.00, and USD 6700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Property And Casualty Insurance Providers," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Property And Casualty Insurance Providers report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Property And Casualty Insurance Providers?

To stay informed about further developments, trends, and reports in the Property And Casualty Insurance Providers, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence