Key Insights

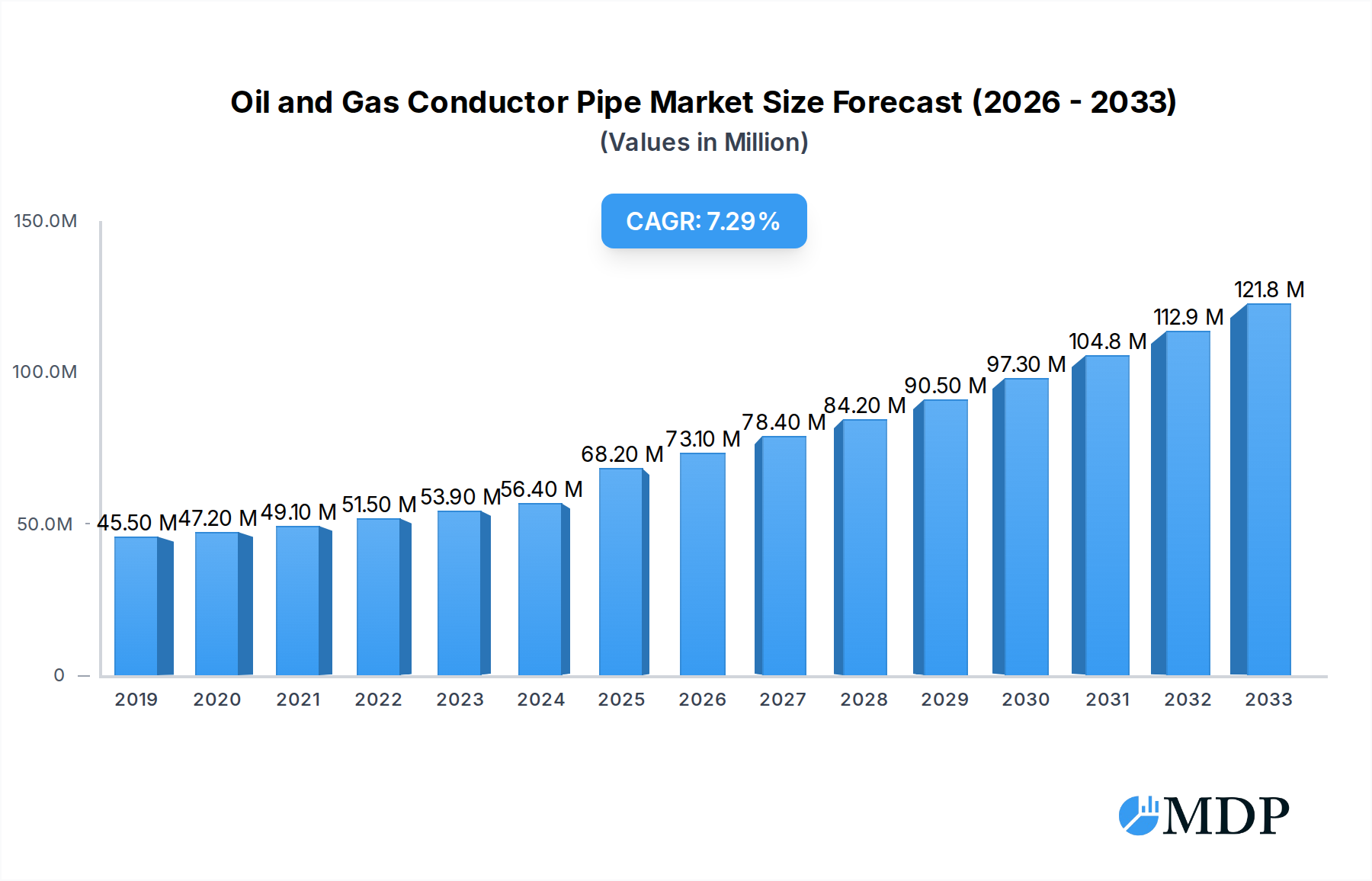

The global Oil and Gas Conductor Pipe market is poised for significant expansion, projected to reach an estimated USD 68.2 billion in 2025 and grow at a robust Compound Annual Growth Rate (CAGR) of 7.2% through 2033. This growth is primarily fueled by the sustained global demand for energy, necessitating continuous exploration and production activities, particularly in deep-sea and challenging onshore environments. The increasing need for robust and reliable infrastructure to transport oil and gas safely and efficiently, coupled with ongoing investments in pipeline networks across developing and developed economies, are key drivers. Furthermore, technological advancements in pipe manufacturing, leading to enhanced durability and performance, are also contributing to market momentum. The market is segmented by application into Onshore and Offshore, with Offshore applications expected to witness substantial growth due to the increasing complexity and scale of deepwater exploration projects.

Oil and Gas Conductor Pipe Market Size (In Million)

The market is broadly categorized into types including Electric Resistance Welding (ERW) Pipes, Spiral Submerged Arc Welded (SSAW) Pipes, and Longitudinally Submerged Arc Welding (LSAW) Pipes. LSAW pipes, known for their large diameter and high strength, are expected to dominate the market, particularly for large-scale oil and gas transportation projects. However, the market also faces certain restraints, including stringent environmental regulations, the volatile nature of oil and gas prices, and the growing global emphasis on renewable energy sources, which may influence future investment in hydrocarbon infrastructure. Despite these challenges, the essential role of oil and gas in the global energy mix ensures a sustained demand for conductor pipes. Key players like Tenaris, TMK, JFE, and Nippon Steel & Sumitomo Metal are actively investing in research and development, expanding their production capacities, and focusing on strategic collaborations to maintain a competitive edge in this dynamic market.

Oil and Gas Conductor Pipe Company Market Share

Here is the SEO-optimized, engaging report description for the Oil and Gas Conductor Pipe market, incorporating high-traffic keywords and adhering to all specified guidelines:

Report Description: Oil and Gas Conductor Pipe Market Analysis 2019-2033

Unlock critical insights into the global Oil and Gas Conductor Pipe market with this comprehensive report. Covering the historical period of 2019–2024 and extending through a detailed forecast from 2025–2033, with a base and estimated year of 2025, this analysis provides an in-depth understanding of market dynamics, trends, and future projections. We meticulously examine key segments including Onshore and Offshore applications, and delve into the dominant pipe types: Electric Resistance Welding (ERW) Pipes, Spiral Submerged Arc Welded (SSAW) Pipes, Longitudinally Submerged Arc Welding (LSAW) Pipes, and Others. Our research is built upon a foundation of extensive data, projecting a market size exceeding XX billion by 2033, with a projected Compound Annual Growth Rate (CAGR) of XX%. This report is an indispensable resource for stakeholders seeking to navigate the evolving landscape of the oil and gas industry, from upstream exploration to midstream transportation.

Oil and Gas Conductor Pipe Market Dynamics & Concentration

The global Oil and Gas Conductor Pipe market, projected to exceed XX billion in value by 2033, exhibits a moderate to high concentration, with key players like Tenaris, TMK, and JFE Steel Corporation holding significant market shares. Innovation drivers are primarily focused on enhancing pipe durability, corrosion resistance, and efficiency in extreme environments, spurred by the increasing complexity of exploration and production activities. Regulatory frameworks globally mandate stringent safety and environmental standards, influencing material selection and manufacturing processes. Product substitutes, while present in niche applications, struggle to match the reliability and cost-effectiveness of conductor pipes in core oil and gas operations. End-user trends indicate a growing demand for larger diameter pipes and specialized coatings to support deepwater and unconventional resource extraction. Merger and acquisition (M&A) activities, though moderate, have seen strategic consolidations aimed at expanding geographical reach and technological capabilities, with an estimated XX significant M&A deals recorded during the historical period.

Oil and Gas Conductor Pipe Industry Trends & Analysis

The Oil and Gas Conductor Pipe industry is undergoing a transformative phase, driven by a confluence of technological advancements, evolving energy demands, and evolving operational landscapes. The market is witnessing robust growth, anticipated to expand at a CAGR of XX% from XX billion in 2025 to over XX billion by 2033. This expansion is underpinned by the escalating global demand for oil and gas, necessitating continuous investment in exploration and production infrastructure, particularly in challenging offshore and remote onshore locations. Technological disruptions are playing a pivotal role, with advancements in welding techniques, material science, and coating technologies leading to the development of more durable, corrosion-resistant, and high-strength conductor pipes. These innovations are crucial for withstanding the extreme pressures and corrosive environments encountered in deepwater drilling and complex geological formations.

Consumer preferences are shifting towards customized solutions that offer enhanced longevity and reduced maintenance costs. Operators are increasingly seeking pipes that can withstand higher operating temperatures and pressures, thereby optimizing extraction efficiency. The competitive dynamics within the market are characterized by a blend of established global players and emerging regional manufacturers, each vying for market share through product differentiation, cost leadership, and strategic partnerships. The penetration of advanced manufacturing technologies, such as automated welding and non-destructive testing, is also a key trend, ensuring superior product quality and reliability. Furthermore, the increasing focus on environmental sustainability is driving the demand for pipes made from recycled materials and those with longer service lives, minimizing the need for premature replacements. The exploration of unconventional reserves, including shale gas and oil sands, further propels the demand for specialized conductor pipes capable of withstanding unique operational challenges. The ongoing digitalization of the energy sector is also influencing the industry, with a growing emphasis on smart pipelines equipped with sensor technology for real-time monitoring and predictive maintenance.

Leading Markets & Segments in Oil and Gas Conductor Pipe

The global Oil and Gas Conductor Pipe market is characterized by significant regional variations and segment dominance. The Onshore application segment is a dominant force, driven by extensive oil and gas exploration and production activities across established reserves and emerging unconventional fields worldwide. Key drivers for this dominance include substantial investments in pipeline infrastructure for the transportation of crude oil and natural gas from wellheads to processing facilities and refineries. Economic policies encouraging domestic energy production and the need for robust energy security further bolster the onshore segment.

In terms of pipe types, Longitudinally Submerged Arc Welding (LSAW) Pipes currently hold a substantial market share. This is attributed to their superior strength and ability to handle high pressures, making them ideal for large-diameter onshore pipelines and critical offshore applications. The manufacturing process for LSAW pipes allows for precise control over pipe dimensions and material properties, ensuring compliance with stringent industry standards.

Geographically, North America stands out as a leading market, fueled by the prolific shale oil and gas revolution in the United States and Canada. Significant investments in both onshore and offshore exploration, coupled with extensive pipeline network expansion, contribute to its market leadership. Government initiatives supporting energy independence and technological innovation in extraction processes further stimulate demand.

The Offshore segment, while currently smaller than onshore, presents a significant growth trajectory. This is driven by the increasing depletion of onshore reserves and the necessity to tap into deeper and more remote offshore resources. Technological advancements in deepwater drilling and subsea infrastructure development are crucial catalysts for offshore growth.

Within the offshore domain, Spiral Submerged Arc Welded (SSAW) Pipes are gaining traction due to their cost-effectiveness for larger diameters and their ability to be manufactured in longer lengths, reducing the number of field welds. Their adaptability to various seabed conditions and water depths makes them a preferred choice for offshore projects. The demand for specialized pipes capable of withstanding high-pressure, low-temperature (HP/LT) environments is also a significant trend in offshore applications.

The forecast period is expected to witness a gradual shift in segment dominance, with offshore applications projected to grow at a higher CAGR owing to complex global energy demands and technological breakthroughs enabling exploration in previously inaccessible frontiers. The development of new offshore fields and the expansion of existing ones, particularly in regions like the Gulf of Mexico, the North Sea, and the Asia-Pacific, will continue to be major demand drivers.

Oil and Gas Conductor Pipe Product Developments

Recent product developments in the Oil and Gas Conductor Pipe sector are sharply focused on enhancing performance and sustainability. Manufacturers are innovating with advanced steel alloys and specialized coatings to improve corrosion resistance and extend service life in harsh environments, thereby reducing lifecycle costs. Innovations in welding techniques, such as multi-wire submerged arc welding, are enabling the production of larger diameter pipes with superior structural integrity. The development of thinner yet stronger pipe walls, achieved through advanced material science, offers weight reduction benefits, particularly crucial for offshore installations. These advancements directly translate to competitive advantages by offering operators increased operational efficiency, improved safety, and a reduced environmental footprint.

Key Drivers of Oil and Gas Conductor Pipe Growth

The growth of the Oil and Gas Conductor Pipe market is propelled by several key factors. Firstly, the sustained global demand for oil and natural gas necessitates continuous investment in exploration and production (E&P) infrastructure, driving demand for conductor pipes in both onshore and offshore projects. Secondly, technological advancements in drilling and extraction techniques, such as deepwater exploration and unconventional resource development, require specialized and high-performance conductor pipes. Thirdly, government initiatives focused on energy security and the development of domestic energy resources, coupled with favorable regulatory frameworks for infrastructure development, further stimulate market expansion. Finally, the aging of existing pipelines and the associated need for replacement and upgrades also contribute significantly to market growth.

Challenges in the Oil and Gas Conductor Pipe Market

Despite robust growth prospects, the Oil and Gas Conductor Pipe market faces several challenges. Stringent environmental regulations and increasing scrutiny over carbon emissions can impact exploration and production activities, indirectly affecting conductor pipe demand. Fluctuations in crude oil prices introduce uncertainty in capital expenditure for new projects, leading to project delays or cancellations. Intense competition among manufacturers, particularly from low-cost regions, exerts downward pressure on profit margins. Furthermore, supply chain disruptions, exacerbated by geopolitical events and logistical complexities, can lead to increased lead times and material costs. The high capital investment required for advanced manufacturing facilities and the long lead times for specialized pipe production also pose significant barriers to entry for new players.

Emerging Opportunities in Oil and Gas Conductor Pipe

Emerging opportunities within the Oil and Gas Conductor Pipe market are primarily driven by the increasing complexity of energy extraction and the global transition towards more sustainable energy solutions. The growing demand for offshore natural gas, especially in deepwater and Arctic regions, presents a significant avenue for growth, necessitating highly specialized and durable conductor pipes. Advancements in renewable energy infrastructure, such as offshore wind farms, also create opportunities for specialized pipe solutions used in foundation construction and subsea cable protection, indirectly benefiting pipe manufacturers. Furthermore, the focus on carbon capture, utilization, and storage (CCUS) technologies is opening new markets for specialized piping solutions designed for transporting captured CO2, offering a potential diversification strategy for manufacturers. Strategic partnerships and joint ventures aimed at developing innovative materials and technologies for extreme environments are also poised to unlock substantial growth.

Leading Players in the Oil and Gas Conductor Pipe Sector

- EVRAZ

- Baoji Petroleum Steel Pipe

- JFE

- Jindal SAW Ltd

- Europipe Group

- Essar Steel

- Jiangsu Yulong Steel Pipe

- American SpiralWeld Pipe

- Zhejiang Kingland

- Tenaris

- Cenergy Holdings

- TMK

- Nippon Steel & Sumitomo Metal

- Shengli Oil & Gas Pipe

- CNPC Bohai Equipment Manufacturing

- Chu Kong Pipe

- Baowu Steel

- Borusan Mannesmann

Key Milestones in Oil and Gas Conductor Pipe Industry

- 2019: Increased adoption of advanced coating technologies for enhanced corrosion resistance in offshore applications.

- 2020: Significant investments in LSAW pipe manufacturing capacity to meet growing demand for large-diameter onshore pipelines.

- 2021: Emergence of new high-strength steel alloys capable of withstanding extreme pressures in deepwater exploration.

- 2022: Focus on digitalizing manufacturing processes and implementing AI for quality control in pipe production.

- 2023: Strategic acquisitions aimed at expanding geographical presence and product portfolios by key market players.

- 2024: Increased R&D for developing more sustainable and environmentally friendly pipe manufacturing methods.

Strategic Outlook for Oil and Gas Conductor Pipe Market

The strategic outlook for the Oil and Gas Conductor Pipe market is characterized by a focus on innovation, sustainability, and market diversification. Growth accelerators will include continued investment in deepwater and unconventional resource development, alongside the expansion of natural gas infrastructure globally. Manufacturers are expected to prioritize the development of higher-strength, lighter-weight, and more corrosion-resistant pipes to meet the evolving demands of harsh operational environments. Strategic partnerships for technology development and market penetration, particularly in emerging economies, will be crucial. Furthermore, exploring opportunities in related sectors such as renewable energy infrastructure and CO2 transportation will provide avenues for long-term growth and resilience against the volatility of the traditional oil and gas market.

Oil and Gas Conductor Pipe Segmentation

-

1. Application

- 1.1. Onshore

- 1.2. Offshore

-

2. Types

- 2.1. Electric Resistance Welding (ERW) Pipes

- 2.2. Spiral Submerged Arc Welded (SSAW) Pipes

- 2.3. Longitudinally Submerged Arc Welding (LSAW) Pipes

- 2.4. Others

Oil and Gas Conductor Pipe Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

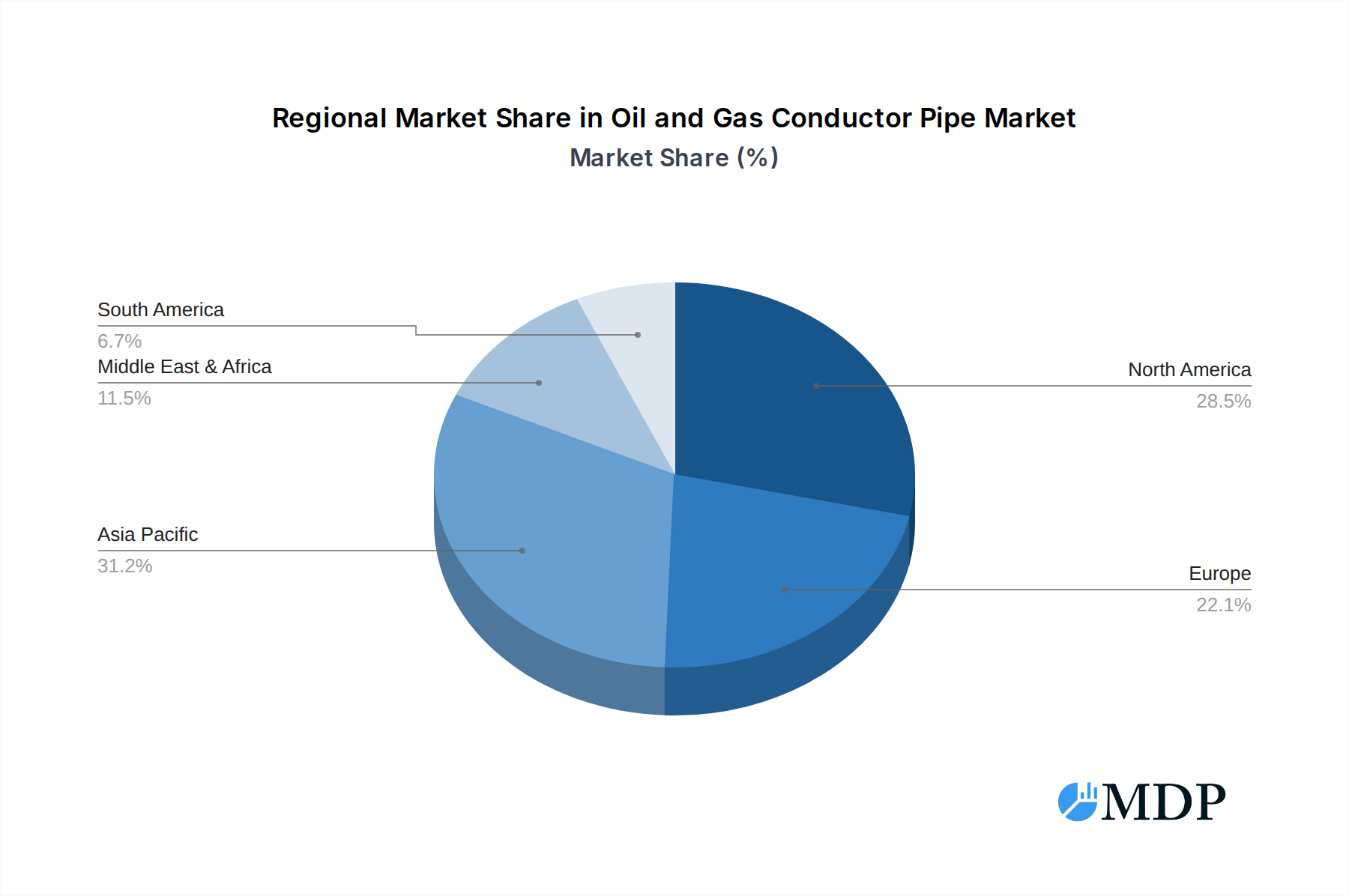

Oil and Gas Conductor Pipe Regional Market Share

Geographic Coverage of Oil and Gas Conductor Pipe

Oil and Gas Conductor Pipe REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 7.2% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Oil and Gas Conductor Pipe Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Onshore

- 5.1.2. Offshore

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Electric Resistance Welding (ERW) Pipes

- 5.2.2. Spiral Submerged Arc Welded (SSAW) Pipes

- 5.2.3. Longitudinally Submerged Arc Welding (LSAW) Pipes

- 5.2.4. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Oil and Gas Conductor Pipe Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Onshore

- 6.1.2. Offshore

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Electric Resistance Welding (ERW) Pipes

- 6.2.2. Spiral Submerged Arc Welded (SSAW) Pipes

- 6.2.3. Longitudinally Submerged Arc Welding (LSAW) Pipes

- 6.2.4. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Oil and Gas Conductor Pipe Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Onshore

- 7.1.2. Offshore

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Electric Resistance Welding (ERW) Pipes

- 7.2.2. Spiral Submerged Arc Welded (SSAW) Pipes

- 7.2.3. Longitudinally Submerged Arc Welding (LSAW) Pipes

- 7.2.4. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Oil and Gas Conductor Pipe Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Onshore

- 8.1.2. Offshore

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Electric Resistance Welding (ERW) Pipes

- 8.2.2. Spiral Submerged Arc Welded (SSAW) Pipes

- 8.2.3. Longitudinally Submerged Arc Welding (LSAW) Pipes

- 8.2.4. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Oil and Gas Conductor Pipe Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Onshore

- 9.1.2. Offshore

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Electric Resistance Welding (ERW) Pipes

- 9.2.2. Spiral Submerged Arc Welded (SSAW) Pipes

- 9.2.3. Longitudinally Submerged Arc Welding (LSAW) Pipes

- 9.2.4. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Oil and Gas Conductor Pipe Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Onshore

- 10.1.2. Offshore

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Electric Resistance Welding (ERW) Pipes

- 10.2.2. Spiral Submerged Arc Welded (SSAW) Pipes

- 10.2.3. Longitudinally Submerged Arc Welding (LSAW) Pipes

- 10.2.4. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 EVRAZ

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Baoji Petroleum Steel Pipe

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 JFE

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Jindal SAW Ltd

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Europipe Group

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Essar Steel

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Jiangsu Yulong Steel Pipe

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 American SpiralWeld Pipe

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Zhejiang Kingland

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Tenaris

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Cenergy Holdings

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 TMK

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Nippon Steel & Sumitomo Metal

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Shengli Oil & Gas Pipe

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 CNPC Bohai Equipment Manufacturing

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Chu Kong Pipe

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.17 Baowu Steel

- 11.2.17.1. Overview

- 11.2.17.2. Products

- 11.2.17.3. SWOT Analysis

- 11.2.17.4. Recent Developments

- 11.2.17.5. Financials (Based on Availability)

- 11.2.18 Borusan Mannesmann

- 11.2.18.1. Overview

- 11.2.18.2. Products

- 11.2.18.3. SWOT Analysis

- 11.2.18.4. Recent Developments

- 11.2.18.5. Financials (Based on Availability)

- 11.2.1 EVRAZ

List of Figures

- Figure 1: Global Oil and Gas Conductor Pipe Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Oil and Gas Conductor Pipe Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Oil and Gas Conductor Pipe Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Oil and Gas Conductor Pipe Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Oil and Gas Conductor Pipe Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Oil and Gas Conductor Pipe Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Oil and Gas Conductor Pipe Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Oil and Gas Conductor Pipe Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Oil and Gas Conductor Pipe Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Oil and Gas Conductor Pipe Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Oil and Gas Conductor Pipe Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Oil and Gas Conductor Pipe Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Oil and Gas Conductor Pipe Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Oil and Gas Conductor Pipe Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Oil and Gas Conductor Pipe Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Oil and Gas Conductor Pipe Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Oil and Gas Conductor Pipe Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Oil and Gas Conductor Pipe Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Oil and Gas Conductor Pipe Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Oil and Gas Conductor Pipe Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Oil and Gas Conductor Pipe Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Oil and Gas Conductor Pipe Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Oil and Gas Conductor Pipe Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Oil and Gas Conductor Pipe Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Oil and Gas Conductor Pipe Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Oil and Gas Conductor Pipe Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Oil and Gas Conductor Pipe Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Oil and Gas Conductor Pipe Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Oil and Gas Conductor Pipe Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Oil and Gas Conductor Pipe Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Oil and Gas Conductor Pipe Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Oil and Gas Conductor Pipe Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Oil and Gas Conductor Pipe Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Oil and Gas Conductor Pipe Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Oil and Gas Conductor Pipe Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Oil and Gas Conductor Pipe Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Oil and Gas Conductor Pipe Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Oil and Gas Conductor Pipe Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Oil and Gas Conductor Pipe Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Oil and Gas Conductor Pipe Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Oil and Gas Conductor Pipe Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Oil and Gas Conductor Pipe Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Oil and Gas Conductor Pipe Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Oil and Gas Conductor Pipe Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Oil and Gas Conductor Pipe Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Oil and Gas Conductor Pipe Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Oil and Gas Conductor Pipe Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Oil and Gas Conductor Pipe Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Oil and Gas Conductor Pipe Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Oil and Gas Conductor Pipe Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Oil and Gas Conductor Pipe Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Oil and Gas Conductor Pipe Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Oil and Gas Conductor Pipe Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Oil and Gas Conductor Pipe Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Oil and Gas Conductor Pipe Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Oil and Gas Conductor Pipe Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Oil and Gas Conductor Pipe Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Oil and Gas Conductor Pipe Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Oil and Gas Conductor Pipe Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Oil and Gas Conductor Pipe Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Oil and Gas Conductor Pipe Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Oil and Gas Conductor Pipe Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Oil and Gas Conductor Pipe Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Oil and Gas Conductor Pipe Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Oil and Gas Conductor Pipe Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Oil and Gas Conductor Pipe Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Oil and Gas Conductor Pipe Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Oil and Gas Conductor Pipe Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Oil and Gas Conductor Pipe Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Oil and Gas Conductor Pipe Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Oil and Gas Conductor Pipe Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Oil and Gas Conductor Pipe Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Oil and Gas Conductor Pipe Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Oil and Gas Conductor Pipe Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Oil and Gas Conductor Pipe Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Oil and Gas Conductor Pipe Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Oil and Gas Conductor Pipe Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Oil and Gas Conductor Pipe?

The projected CAGR is approximately 7.2%.

2. Which companies are prominent players in the Oil and Gas Conductor Pipe?

Key companies in the market include EVRAZ, Baoji Petroleum Steel Pipe, JFE, Jindal SAW Ltd, Europipe Group, Essar Steel, Jiangsu Yulong Steel Pipe, American SpiralWeld Pipe, Zhejiang Kingland, Tenaris, Cenergy Holdings, TMK, Nippon Steel & Sumitomo Metal, Shengli Oil & Gas Pipe, CNPC Bohai Equipment Manufacturing, Chu Kong Pipe, Baowu Steel, Borusan Mannesmann.

3. What are the main segments of the Oil and Gas Conductor Pipe?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Oil and Gas Conductor Pipe," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Oil and Gas Conductor Pipe report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Oil and Gas Conductor Pipe?

To stay informed about further developments, trends, and reports in the Oil and Gas Conductor Pipe, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence