Key Insights

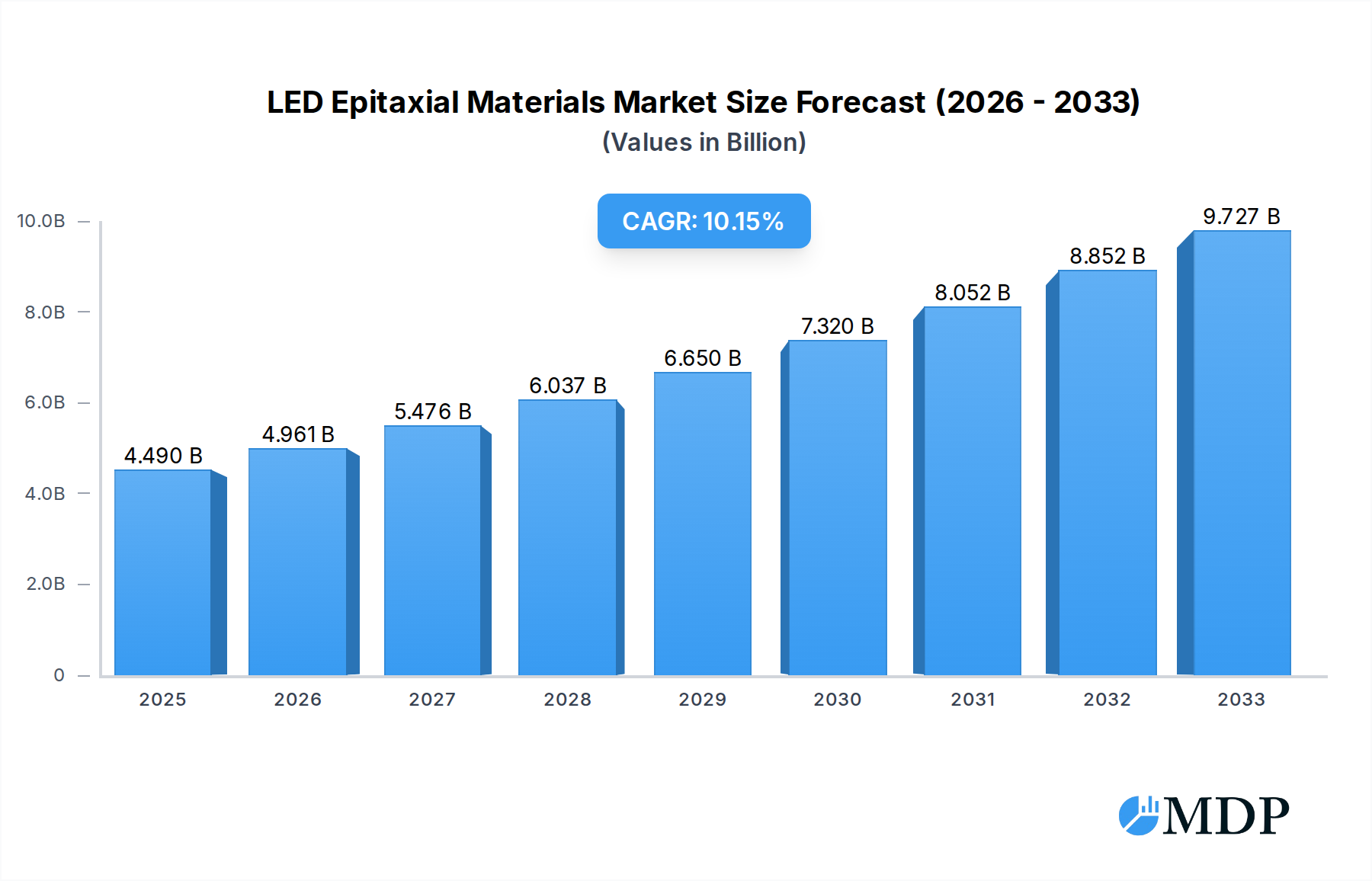

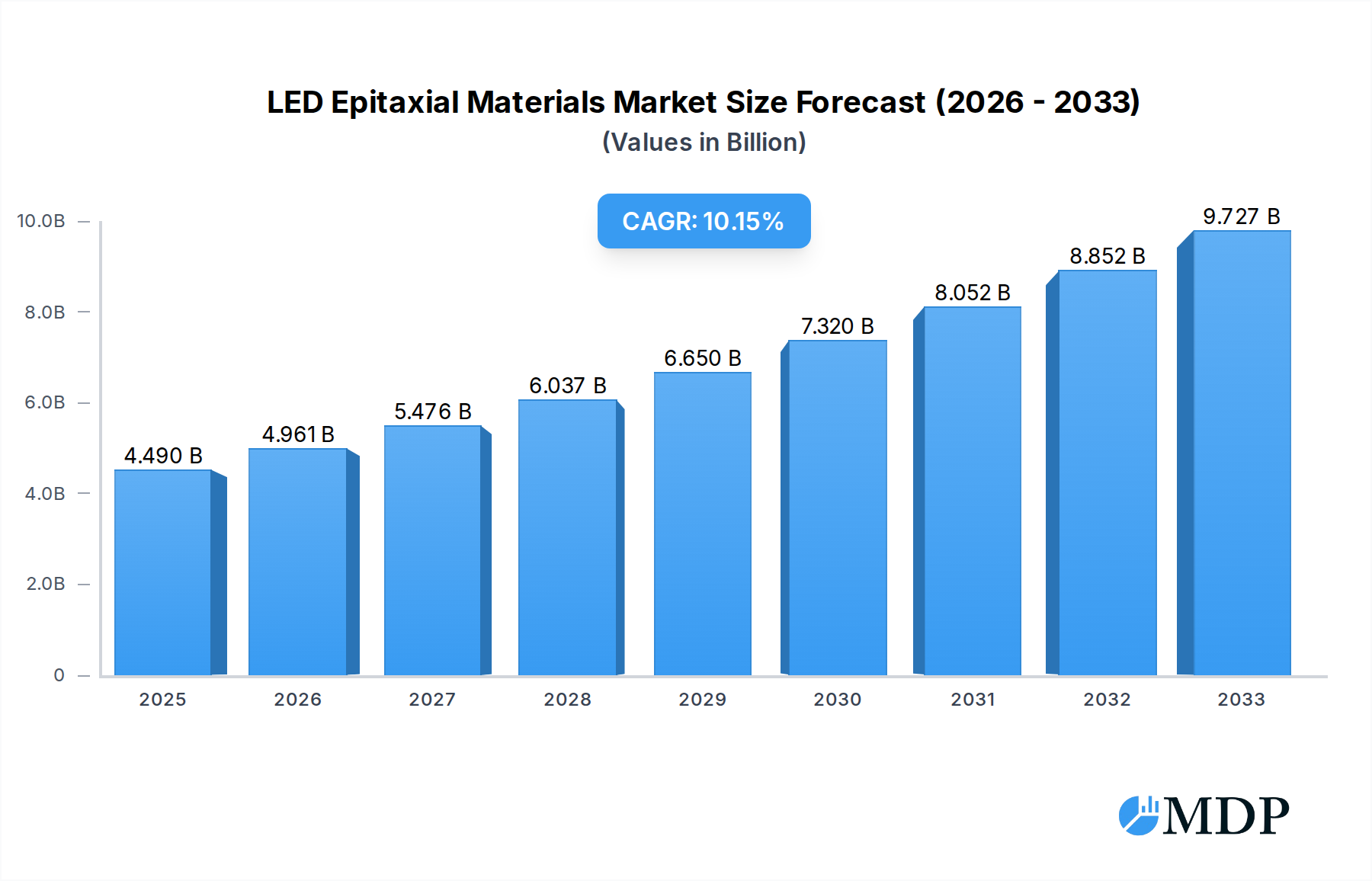

The global LED Epitaxial Materials market is poised for significant expansion, projected to reach $4.49 billion in 2025, and is expected to grow at a robust compound annual growth rate (CAGR) of 10.5% through 2033. This impressive growth is primarily propelled by the escalating demand for energy-efficient lighting solutions across residential, commercial, and industrial sectors. The automotive industry's increasing adoption of LED technology for headlights, taillights, and interior lighting further fuels this market momentum. Furthermore, advancements in communication technologies, particularly the burgeoning demand for high-speed data transmission and sophisticated displays, are creating substantial opportunities for advanced LED epitaxial materials. Emerging applications in specialized fields are also contributing to market expansion, highlighting the versatility and critical role of these materials in next-generation technologies.

LED Epitaxial Materials Market Size (In Billion)

The market's trajectory is also shaped by prevailing trends such as the continuous innovation in material science leading to enhanced LED performance, including higher brightness, improved color rendering, and extended lifespan. The development of new epitaxial structures and growth techniques is crucial for meeting the evolving demands of various applications. However, the market faces certain restraints, including the high initial investment costs associated with manufacturing advanced epitaxial materials and the complex manufacturing processes that require specialized expertise and equipment. Fluctuations in raw material prices, particularly for precursor chemicals, can also impact market profitability. Despite these challenges, the strong underlying demand drivers and the continuous push for technological advancements within the LED industry position the LED Epitaxial Materials market for sustained and dynamic growth.

LED Epitaxial Materials Company Market Share

Global LED Epitaxial Materials Market Report: Driving Innovation and Growth (2019-2033)

This comprehensive report provides an in-depth analysis of the global LED epitaxial materials market, offering critical insights for industry stakeholders. Covering the historical period from 2019 to 2024, a base year of 2025, and a robust forecast period extending to 2033, this study is your definitive guide to understanding market dynamics, technological advancements, and future opportunities. With an estimated market size of $15.2 billion in 2025, projected to reach $32.5 billion by 2033, and a Compound Annual Growth Rate (CAGR) of 9.8%, this report pinpoints key growth drivers and challenges within this rapidly evolving sector.

LED Epitaxial Materials Market Dynamics & Concentration

The LED epitaxial materials market exhibits a moderate concentration, with key players investing heavily in research and development to maintain a competitive edge. Innovation drivers are primarily fueled by the relentless demand for higher efficiency, increased luminosity, and advanced functionalities across various applications. Regulatory frameworks, particularly those focused on energy efficiency and environmental standards, significantly influence material choices and manufacturing processes. Product substitutes, while present, struggle to match the performance and cost-effectiveness of advanced epitaxial materials in high-demand segments. End-user trends are steering the market towards miniaturization, enhanced color rendering, and integration into smart technologies. Mergers and acquisitions (M&A) activities are strategically employed to consolidate market share, acquire technological capabilities, and expand geographical reach. For instance, M&A deal counts have seen an upward trend in the last two years, indicating strategic consolidation. Market share for leading players ranges from 5% to 12%, with a significant portion held by diversified chemical and materials science companies. The competitive landscape is characterized by a blend of established giants and emerging innovators, all striving for dominance in this critical semiconductor material sector.

LED Epitaxial Materials Industry Trends & Analysis

The LED epitaxial materials industry is experiencing robust growth, propelled by a confluence of technological advancements, expanding application arenas, and evolving consumer preferences. The market size, estimated at $15.2 billion in 2025, is projected to reach $32.5 billion by 2033, demonstrating a compelling CAGR of 9.8% over the forecast period. This significant expansion is largely driven by the insatiable demand for energy-efficient illumination solutions across residential, commercial, and industrial sectors. Furthermore, the burgeoning automotive industry's adoption of advanced LED lighting for headlights, taillights, and interior ambiance, along with the rapid growth of the communication sector leveraging high-speed data transmission through optical components, are critical growth catalysts. Technological disruptions, including advancements in epitaxy techniques such as Metal-Organic Chemical Vapor Deposition (MOCVD) and Molecular Beam Epitaxy (MBE), are enabling the creation of novel material compositions and structures that offer superior performance metrics, including increased brightness and spectral purity. Consumer preferences are increasingly leaning towards dynamic lighting solutions, color-tunable LEDs, and integrated smart lighting systems, all of which necessitate sophisticated epitaxial material development. The competitive dynamics within the industry are intense, characterized by a race to achieve higher quantum efficiencies, longer device lifetimes, and lower manufacturing costs. Companies are investing billions in R&D to develop next-generation materials like Gallium Nitride (GaN) for high-power applications and Gallium Phosphide (GaP) for specialized optical functions. Market penetration of LED technology, especially in emerging economies, is still substantial, offering ample room for continued growth. The interplay between technological innovation and market demand creates a virtuous cycle, ensuring sustained momentum in the LED epitaxial materials sector. The estimated market penetration of LED technology in general lighting applications stands at 70% in developed regions and is expected to surpass 60% globally by 2028, underscoring the vast potential for epitaxial material suppliers.

Leading Markets & Segments in LED Epitaxial Materials

The global LED epitaxial materials market is characterized by distinct regional strengths and segment dominance, driven by a combination of economic policies, infrastructure development, and technological adoption. The Illumination application segment currently holds the largest market share, projected to account for over 45% of the total market value by 2025. This dominance is fueled by increasing adoption of energy-efficient LED lighting in urban development projects, smart city initiatives, and retrofitting of older infrastructure worldwide. Government incentives and stricter energy consumption regulations in major economies like China, the United States, and the European Union are significant economic policies that bolster this segment.

Within the Types of LED epitaxial materials, GaN (Gallium Nitride) commands the most significant market share, expected to exceed 55% by 2025. This is primarily due to its exceptional performance characteristics for blue, green, and ultraviolet LEDs, which are foundational for white light generation and a wide range of other applications. The rapid expansion of the Communication segment, driven by the rollout of 5G networks and advancements in fiber optic communication, is also a key driver for GaN and other specialized III-V semiconductor materials. The projected market size for GaN-based epitaxy is estimated to reach $16.8 billion by 2033.

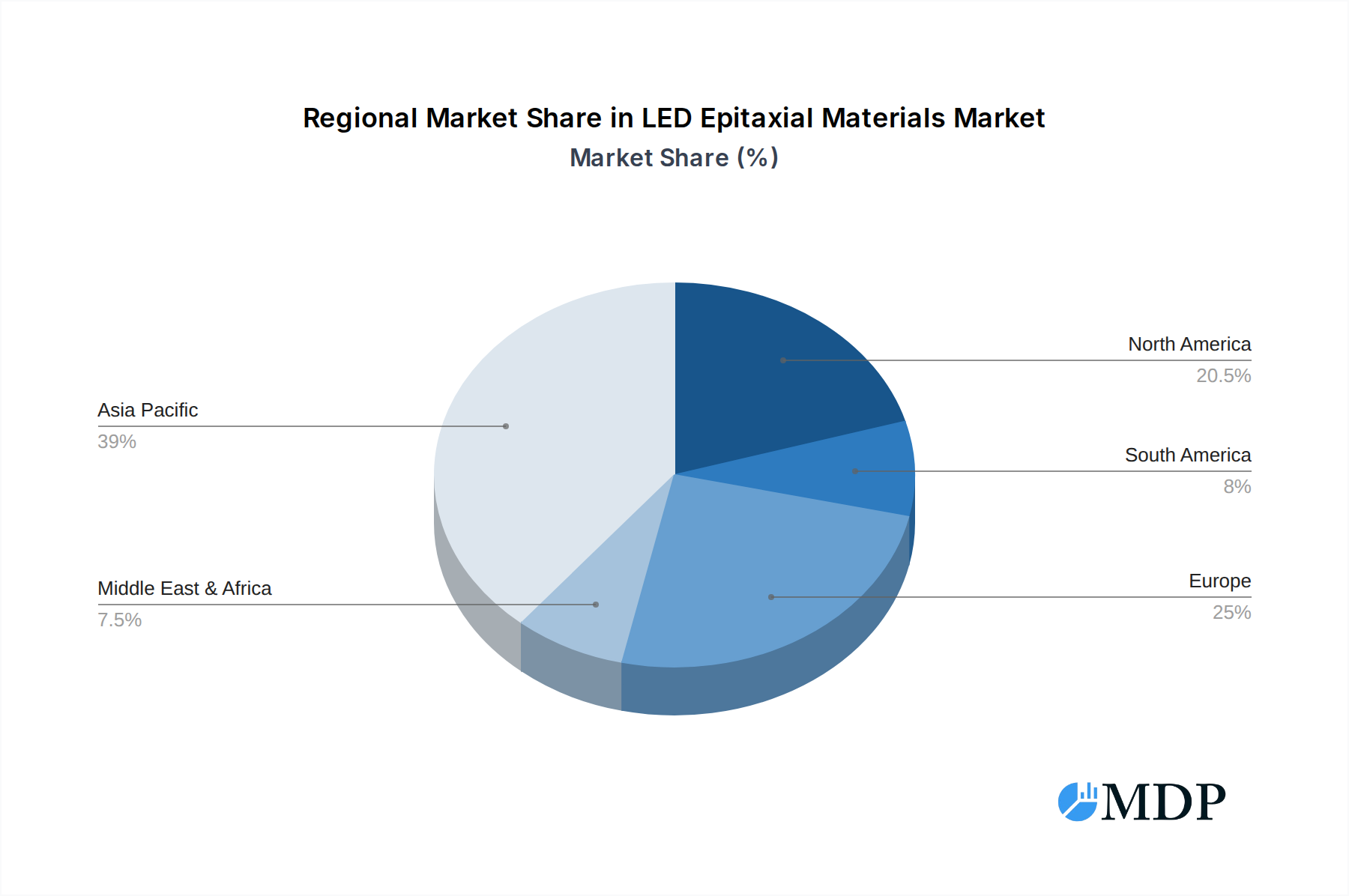

Geographically, Asia Pacific, particularly China, is the leading market for LED epitaxial materials, representing over 40% of the global market share. This leadership is attributed to its robust manufacturing ecosystem, substantial domestic demand across all application segments, and significant government investments in the semiconductor and LED industries. Infrastructure development, including the widespread deployment of smart grids and high-speed internet, further cements Asia Pacific's dominance.

- Key Drivers for Illumination Segment Dominance:

- Government mandates for energy efficiency and reduced carbon emissions.

- Decreasing manufacturing costs of LED chips and modules.

- Growing consumer awareness of the benefits of LED lighting.

- Development of smart lighting systems and IoT integration.

- Key Drivers for GaN Dominance:

- Superior electrical and optical properties for high-brightness and efficient LEDs.

- Crucial for blue LEDs, enabling white light generation.

- Increasing demand for high-power LEDs in automotive and industrial applications.

- Advancements in MOCVD technology for improved GaN epitaxy.

- Key Drivers for Asia Pacific Dominance:

- Largest global LED manufacturing hub.

- Strong domestic demand from diverse application sectors.

- Supportive government policies and subsidies.

- Rapid urbanization and infrastructure development.

LED Epitaxial Materials Product Developments

Recent product developments in LED epitaxial materials are focused on enhancing efficiency, expanding spectral capabilities, and improving device reliability. Innovations in GaN-on-GaN technology are yielding higher power density and improved thermal management for demanding applications like automotive headlights and industrial lighting. Furthermore, advancements in materials for micro-LED displays are enabling smaller, brighter, and more power-efficient visual interfaces. The development of novel epitaxy techniques and precursor chemistries by companies such as Nata Chem and Merck (SAFC Hitech) are crucial in achieving these performance gains, offering competitive advantages through superior light output, extended lifespan, and reduced manufacturing costs for end products.

Key Drivers of LED Epitaxial Materials Growth

The growth of the LED epitaxial materials market is significantly propelled by several interconnected factors. Technologically, the relentless pursuit of higher luminous efficacy and enhanced color quality in LEDs for illumination and display applications remains a primary driver. The increasing integration of LED technology into automotive lighting systems, driven by safety regulations and aesthetic demands, further fuels market expansion. Economically, the declining cost of LED components, coupled with government initiatives promoting energy efficiency, makes LEDs a more attractive alternative to traditional lighting. Regulatory frameworks encouraging the phase-out of less efficient lighting technologies also play a crucial role. The widespread adoption of 5G infrastructure, requiring advanced optical components, also contributes to the demand for specialized epitaxial materials.

Challenges in the LED Epitaxial Materials Market

Despite its robust growth trajectory, the LED epitaxial materials market faces several challenges. Intense price competition among manufacturers, particularly in high-volume segments like general illumination, can erode profit margins. Supply chain vulnerabilities, including the availability and cost of critical raw materials like Gallium and Indium, can lead to price volatility and production disruptions. Moreover, the development of advanced epitaxial materials often requires substantial capital investment in R&D and specialized manufacturing equipment, posing a barrier for smaller players. Evolving regulatory landscapes concerning environmental impact and material sourcing also necessitate continuous adaptation. The market share impact of these challenges is estimated to be a potential 5-8% reduction in projected growth if not effectively mitigated.

Emerging Opportunities in LED Epitaxial Materials

Emerging opportunities in the LED epitaxial materials sector are largely centered around technological breakthroughs and new application frontiers. The development of ultra-high brightness and high-efficiency LEDs for advanced display technologies, such as virtual reality (VR) and augmented reality (AR) headsets, presents a significant growth avenue. The expansion of LED applications in horticulture lighting, medical devices, and UV-C disinfection systems also offers substantial market potential. Strategic partnerships between material suppliers and device manufacturers are crucial for co-developing tailored solutions and accelerating market adoption. Furthermore, the growing demand for solid-state lighting in emerging economies, coupled with ongoing infrastructure development, provides a fertile ground for market expansion.

Leading Players in the LED Epitaxial Materials Sector

- Nata Chem

- Jiangxi Jiayin Optoelectronic Materials

- Nouryon

- EpiValence

- GELEST(Mitsubishi Chemical)

- Sinocompound

- Strem

- Merck(SAFC Hitech)

- Lake Materials

- Ube Industries

- Jucan Optoelectronics

- CREE

- Rohn

- Showa Denko

- Tianke Heda

Key Milestones in LED Epitaxial Materials Industry

- 2019: Significant advancements in GaN-on-GaN epitaxy for high-power applications.

- 2020: Increased investment in R&D for micro-LED materials.

- 2021: Launch of next-generation epitaxial materials with enhanced luminous efficacy.

- 2022: Growing demand for LED materials in automotive and communication sectors.

- 2023: Strategic partnerships formed for advanced material development.

- 2024: Innovations in epitaxy techniques leading to cost reductions.

Strategic Outlook for LED Epitaxial Materials Market

The strategic outlook for the LED epitaxial materials market is overwhelmingly positive, driven by sustained demand for energy-efficient lighting, advanced display technologies, and burgeoning applications in automotive and communications. Growth accelerators include continued innovation in material science, enabling higher performance and lower costs, and the increasing global adoption of smart city initiatives and 5G infrastructure. Manufacturers who focus on developing specialized materials for high-growth segments like micro-LEDs and automotive lighting, while also optimizing production processes for cost-effectiveness, are poised for significant success. Strategic collaborations and a keen eye on emerging application trends will be pivotal in capitalizing on the substantial future market potential.

LED Epitaxial Materials Segmentation

-

1. Application

- 1.1. Illumination

- 1.2. Automobile

- 1.3. Communication

- 1.4. Others

-

2. Types

- 2.1. GaN

- 2.2. GaP

- 2.3. GaAs

- 2.4. SiC

- 2.5. Others

LED Epitaxial Materials Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

LED Epitaxial Materials Regional Market Share

Geographic Coverage of LED Epitaxial Materials

LED Epitaxial Materials REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 10.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global LED Epitaxial Materials Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Illumination

- 5.1.2. Automobile

- 5.1.3. Communication

- 5.1.4. Others

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. GaN

- 5.2.2. GaP

- 5.2.3. GaAs

- 5.2.4. SiC

- 5.2.5. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America LED Epitaxial Materials Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Illumination

- 6.1.2. Automobile

- 6.1.3. Communication

- 6.1.4. Others

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. GaN

- 6.2.2. GaP

- 6.2.3. GaAs

- 6.2.4. SiC

- 6.2.5. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America LED Epitaxial Materials Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Illumination

- 7.1.2. Automobile

- 7.1.3. Communication

- 7.1.4. Others

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. GaN

- 7.2.2. GaP

- 7.2.3. GaAs

- 7.2.4. SiC

- 7.2.5. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe LED Epitaxial Materials Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Illumination

- 8.1.2. Automobile

- 8.1.3. Communication

- 8.1.4. Others

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. GaN

- 8.2.2. GaP

- 8.2.3. GaAs

- 8.2.4. SiC

- 8.2.5. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa LED Epitaxial Materials Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Illumination

- 9.1.2. Automobile

- 9.1.3. Communication

- 9.1.4. Others

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. GaN

- 9.2.2. GaP

- 9.2.3. GaAs

- 9.2.4. SiC

- 9.2.5. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific LED Epitaxial Materials Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Illumination

- 10.1.2. Automobile

- 10.1.3. Communication

- 10.1.4. Others

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. GaN

- 10.2.2. GaP

- 10.2.3. GaAs

- 10.2.4. SiC

- 10.2.5. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Nata Chem

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Jiangxi Jiayin Optoelectronic Materials

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Nouryon

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 EpiValence

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 GELEST(Mitsubishi Chemical)

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Sinocompound

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Strem

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Merck(SAFC Hitech)

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Lake Materials

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Ube Industries

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Jucan Optoelectronics

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 CREE

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Rohn

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 Showa Denko

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 Tianke Heda

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.1 Nata Chem

List of Figures

- Figure 1: Global LED Epitaxial Materials Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America LED Epitaxial Materials Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America LED Epitaxial Materials Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America LED Epitaxial Materials Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America LED Epitaxial Materials Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America LED Epitaxial Materials Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America LED Epitaxial Materials Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America LED Epitaxial Materials Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America LED Epitaxial Materials Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America LED Epitaxial Materials Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America LED Epitaxial Materials Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America LED Epitaxial Materials Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America LED Epitaxial Materials Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe LED Epitaxial Materials Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe LED Epitaxial Materials Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe LED Epitaxial Materials Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe LED Epitaxial Materials Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe LED Epitaxial Materials Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe LED Epitaxial Materials Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa LED Epitaxial Materials Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa LED Epitaxial Materials Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa LED Epitaxial Materials Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa LED Epitaxial Materials Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa LED Epitaxial Materials Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa LED Epitaxial Materials Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific LED Epitaxial Materials Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific LED Epitaxial Materials Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific LED Epitaxial Materials Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific LED Epitaxial Materials Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific LED Epitaxial Materials Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific LED Epitaxial Materials Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global LED Epitaxial Materials Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global LED Epitaxial Materials Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global LED Epitaxial Materials Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global LED Epitaxial Materials Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global LED Epitaxial Materials Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global LED Epitaxial Materials Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States LED Epitaxial Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada LED Epitaxial Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico LED Epitaxial Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global LED Epitaxial Materials Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global LED Epitaxial Materials Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global LED Epitaxial Materials Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil LED Epitaxial Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina LED Epitaxial Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America LED Epitaxial Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global LED Epitaxial Materials Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global LED Epitaxial Materials Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global LED Epitaxial Materials Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom LED Epitaxial Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany LED Epitaxial Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France LED Epitaxial Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy LED Epitaxial Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain LED Epitaxial Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia LED Epitaxial Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux LED Epitaxial Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics LED Epitaxial Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe LED Epitaxial Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global LED Epitaxial Materials Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global LED Epitaxial Materials Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global LED Epitaxial Materials Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey LED Epitaxial Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel LED Epitaxial Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC LED Epitaxial Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa LED Epitaxial Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa LED Epitaxial Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa LED Epitaxial Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global LED Epitaxial Materials Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global LED Epitaxial Materials Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global LED Epitaxial Materials Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China LED Epitaxial Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India LED Epitaxial Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan LED Epitaxial Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea LED Epitaxial Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN LED Epitaxial Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania LED Epitaxial Materials Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific LED Epitaxial Materials Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the LED Epitaxial Materials?

The projected CAGR is approximately 10.5%.

2. Which companies are prominent players in the LED Epitaxial Materials?

Key companies in the market include Nata Chem, Jiangxi Jiayin Optoelectronic Materials, Nouryon, EpiValence, GELEST(Mitsubishi Chemical), Sinocompound, Strem, Merck(SAFC Hitech), Lake Materials, Ube Industries, Jucan Optoelectronics, CREE, Rohn, Showa Denko, Tianke Heda.

3. What are the main segments of the LED Epitaxial Materials?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "LED Epitaxial Materials," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the LED Epitaxial Materials report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the LED Epitaxial Materials?

To stay informed about further developments, trends, and reports in the LED Epitaxial Materials, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence