Key Insights

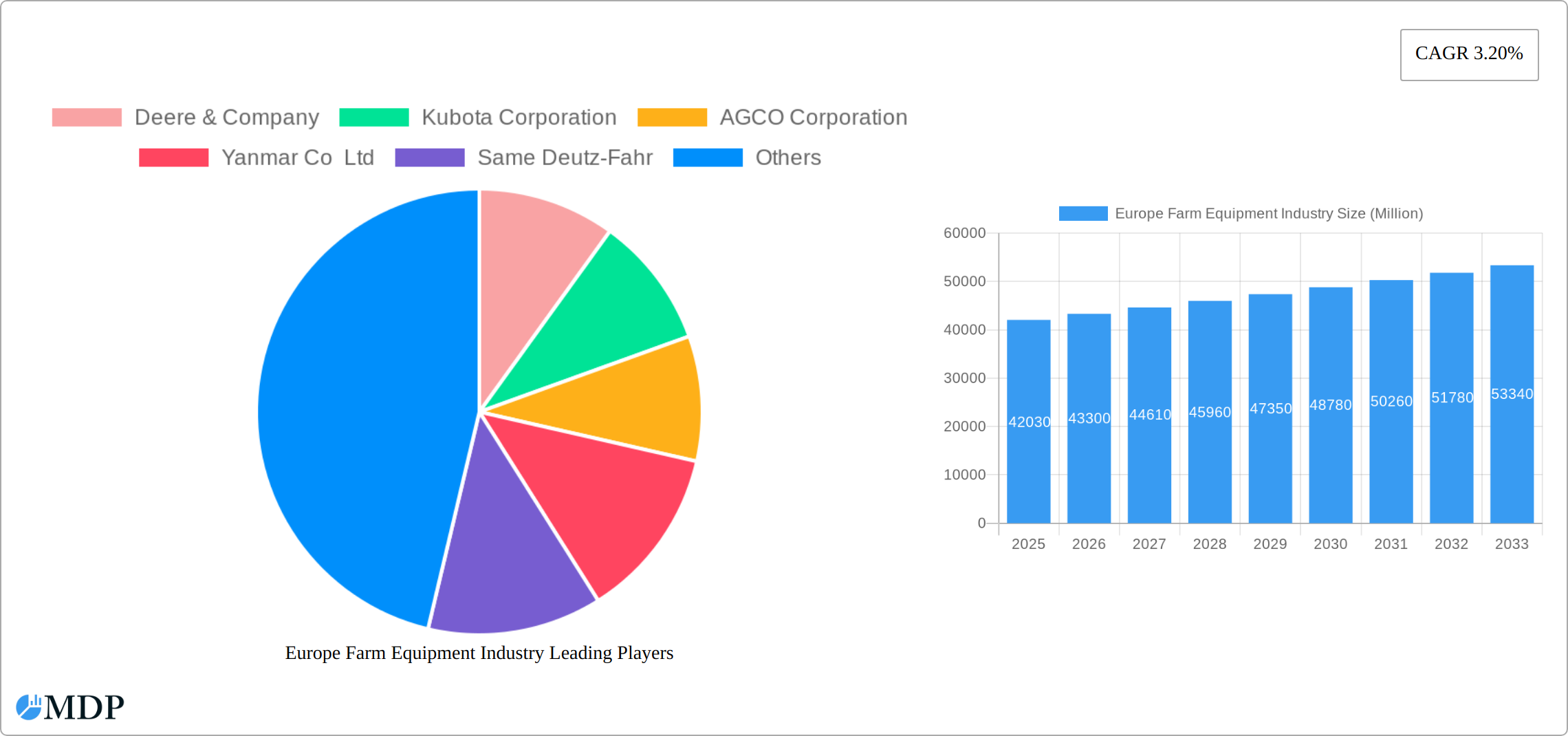

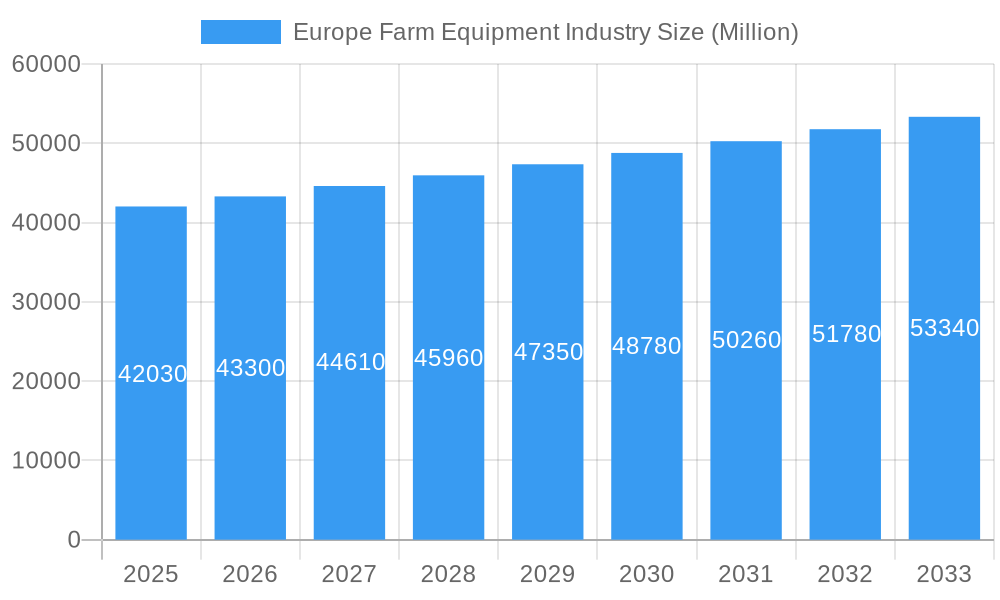

The European farm equipment market, valued at €42.03 billion in 2025, is projected to experience steady growth, exhibiting a Compound Annual Growth Rate (CAGR) of 3.20% from 2025 to 2033. This growth is fueled by several key factors. Firstly, increasing demand for efficient and technologically advanced machinery to enhance agricultural productivity is a major driver. Precision farming techniques, incorporating GPS-guided equipment and data analytics, are gaining traction, boosting the adoption of sophisticated tractors, harvesting machinery (including haying and forage machinery), and irrigation systems. Secondly, the growing emphasis on sustainable agriculture practices, including reducing environmental impact and optimizing resource use, is driving innovation in farm equipment design. Manufacturers are focusing on developing more fuel-efficient and environmentally friendly machinery to meet these demands. Finally, favorable government policies supporting agricultural modernization and technological upgrades across major European nations like Germany, France, and the UK are further strengthening market growth. However, the market faces potential restraints, including fluctuating commodity prices, potential labor shortages, and the high initial investment costs associated with advanced farm equipment.

Europe Farm Equipment Industry Market Size (In Billion)

Segment-wise, tractors constitute a significant portion of the market, particularly higher horsepower models (above 150 HP) used for plowing and cultivating. The demand for specialized machinery such as haying and forage equipment is also considerable, driven by the prevalence of livestock farming and the need for efficient feed production. Competition in the European farm equipment market is intense, with major players like Deere & Company, Kubota Corporation, AGCO Corporation, and CLAAS KGaA mbH vying for market share. These companies continuously innovate and expand their product offerings to cater to evolving farmer needs and technological advancements. The market's future hinges on continued technological advancements, supportive government policies, and the overall health of the European agricultural sector. The forecast period will likely witness a gradual increase in market size, influenced by factors such as technological breakthroughs in automation, precision farming, and sustainable agricultural practices.

Europe Farm Equipment Industry Company Market Share

Europe Farm Equipment Industry Market Report: 2019-2033

This comprehensive report provides a detailed analysis of the Europe farm equipment industry, offering invaluable insights for stakeholders seeking to navigate this dynamic market. From market size and segmentation to leading players and future trends, this report is your go-to resource for understanding the current landscape and anticipating future developments. The report covers the period 2019-2033, with a focus on the 2025-2033 forecast period. Expect actionable data and strategic recommendations to inform your business decisions.

Europe Farm Equipment Industry Market Dynamics & Concentration

The European farm equipment market, valued at an estimated €XX Billion in 2024, is characterized by a dynamic and moderately concentrated landscape. This sector is primarily shaped by a core group of global industry leaders alongside a robust network of regional specialists. The degree of market concentration is influenced by several critical factors, including the pursuit of economies of scale in manufacturing and distribution, the powerful impact of established brand recognition among farmers, and the continuous drive for technological innovation. To gain a comprehensive understanding of the competitive currents within this industry, it is essential to analyze key metrics such as market share evolution and the strategic significance of mergers and acquisitions (M&A) activity.

The engine driving innovation within the European farm equipment market is predominantly fueled by the escalating demand for high-efficiency solutions and the widespread adoption of precision farming technologies and advanced automation systems. Concurrently, increasingly stringent environmental regulations are acting as a powerful catalyst, compelling the industry to develop and implement more sustainable and eco-friendly equipment options. The ongoing replacement of older, less efficient machinery with modern, technologically sophisticated alternatives remains a consistent contributor to market expansion. Furthermore, evolving end-user preferences, such as the growing embrace of precision agriculture techniques and a discernible shift towards rental or leasing models for equipment, are actively reshaping the market's trajectory.

Mergers and acquisitions (M&A) have demonstrably played a pivotal role in sculpting the competitive contours of the European farm equipment industry. Over the past five years, the sector has witnessed approximately XX strategic M&A transactions. These strategic consolidations have frequently been targeted towards solidifying market share, broadening existing product portfolios to meet diverse farmer needs, and acquiring cutting-edge or specialized technologies that offer a competitive edge.

- Market Share Dynamics: Industry giants such as Deere & Company, Kubota Corporation, and AGCO Corporation currently command the largest market shares, collectively representing an estimated XX% of the total European market value.

- M&A Activity Outlook: A notable surge in M&A activity is anticipated in the coming years as companies strategically position themselves to enhance their market reach, diversify their product and service offerings, and achieve greater operational synergies.

- Key Innovation Drivers: The relentless pursuit of advanced precision farming technologies, the integration of sophisticated automation solutions, and the imperative to meet sustainability initiatives are collectively propelling significant innovation across the entire sector.

Europe Farm Equipment Industry Industry Trends & Analysis

The European farm equipment market exhibits a positive growth trajectory, with a projected Compound Annual Growth Rate (CAGR) of XX% during the forecast period (2025-2033). This growth is primarily driven by factors including rising agricultural production, increasing demand for high-efficiency equipment, and ongoing technological advancements. Technological disruptions, particularly in areas like precision agriculture, automation, and data analytics, are revolutionizing farming practices and driving demand for advanced equipment. Consumer preferences are shifting towards equipment that offers greater efficiency, precision, sustainability, and ease of use. This trend is particularly evident among larger farms and agricultural cooperatives that are actively adopting advanced technologies to optimize their operations. Competitive dynamics are characterized by intense rivalry among major global players and smaller regional competitors, with continuous product innovation, strategic partnerships, and mergers and acquisitions driving growth. Market penetration of precision agriculture technologies, while still relatively low, is steadily growing, indicating substantial future market potential.

Leading Markets & Segments in Europe Farm Equipment Industry

In-depth analysis of the European farm equipment landscape reveals that Germany and France stand out as the preeminent markets, largely due to their deeply entrenched and technologically advanced agricultural sectors, bolstered by supportive government policies designed to foster modernization and growth. Within these leading markets, tractors continue to represent the dominant segment, accounting for an impressive XX% of total revenue. Notably, there is a burgeoning demand for higher-horsepower tractor models, particularly those exceeding 150 HP, reflecting the need for more powerful and versatile machinery. The "other equipment" segment, which encompasses crucial machinery for irrigation and harvesting, secures a significant XX% of the market share. This segment has experienced robust growth, propelled by the increasing adoption of sophisticated machinery designed to optimize crop yields and enhance overall operational efficiencies. The haying and forage machinery sub-segment is also exhibiting strong growth, driven by the escalating demand for high-quality fodder to support a growing livestock farming sector across Europe.

- Key Drivers for Tractors: The demand for tractors is significantly influenced by factors such as enhanced fuel efficiency, cutting-edge technological advancements in automation and GPS guidance systems, and the availability of governmental support programs championing sustainable agricultural practices.

- Key Drivers for Other Equipment (Irrigation): The paramount importance of effective water management strategies and the increasing need to address drought resilience measures across various European regions have substantially amplified the demand for advanced irrigation machinery.

- Key Drivers for Harvesting Machinery: With rising crop yields and an ever-present need for highly efficient and timely harvesting operations, the harvesting equipment segment continues its expansion trajectory, driven by these critical agricultural demands.

- Dominance Analysis: Germany's leadership in the tractor segment is intrinsically linked to its highly developed agricultural infrastructure, its strong capacity for technological innovation, and the significant presence of major tractor manufacturers within its borders.

Europe Farm Equipment Industry Product Developments

Recent product development in the European farm equipment industry is sharply focused on elevating precision capabilities, expanding automation features, and enhancing the integration of sophisticated data analytics. Manufacturers are increasingly embedding technologies such as GPS, advanced sensor systems, and artificial intelligence (AI) into their machinery. The primary objectives of these integrations are to optimize operational processes, maximize crop yields, and significantly reduce the consumption of vital resources like water, fertilizers, and fuel. These advancements are strategically designed to boost overall efficiency, mitigate labor costs, and substantially improve the environmental sustainability of agricultural practices. The market's receptiveness to these technologies is exceptionally strong, given the prevailing emphasis among European farmers on precision farming methodologies and a growing commitment to environmentally responsible agricultural operations.

Key Drivers of Europe Farm Equipment Industry Growth

The sustained growth of the European farm equipment industry is propelled by a confluence of powerful factors. Foremost among these are technological advancements, particularly in the realms of automation, precision farming techniques, and sophisticated data analytics, all of which are instrumental in driving substantial gains in operational efficiency and overall productivity. Favorable macroeconomic conditions, coupled with proactive government policies that actively promote agricultural modernization and investment, further contribute to the upward momentum. The persistent and increasing global demand for food products also serves as a significant market driver. Moreover, the implementation of increasingly stringent environmental regulations is acting as a powerful incentive, encouraging the widespread adoption of sustainable farming practices and the procurement of equipment that aligns with ecological principles.

Challenges in the Europe Farm Equipment Industry Market

The European farm equipment market faces several challenges. Stringent environmental regulations increase compliance costs for manufacturers. Supply chain disruptions caused by global events and geopolitical instability pose risks to production and delivery. Intense competition from established players and new entrants pressure profit margins. Fluctuations in commodity prices impact farmer investment decisions and overall market demand, leading to a level of unpredictability in the market.

Emerging Opportunities in Europe Farm Equipment Industry

The industry presents significant long-term growth opportunities. The adoption of precision agriculture technologies and AI-driven solutions is expected to substantially increase efficiency and reduce resource consumption. Strategic partnerships among equipment manufacturers, technology providers, and agricultural service companies are creating innovative solutions that enhance farm operations. Expansion into emerging markets within Europe, particularly those with growing agricultural sectors, offers further opportunities for growth and market diversification.

Leading Players in the Europe Farm Equipment Industry Sector

- Deere & Company

- Kubota Corporation

- AGCO Corporation

- Yanmar Co Ltd

- Same Deutz-Fahr

- CNH Industrial NV

- CLAAS KGaA mbH

- Kuhn Group

- Lely France

Key Milestones in Europe Farm Equipment Industry Industry

- November 2023: CNH Industrial NV unveiled the CR11 New Holland combine at Agritechnica '23, featuring a powerful engine and large grain tank, enhancing harvesting efficiency.

- November 2023: Yanmar Co. Ltd partnered with International Tractors Limited (ITL) to expand its market reach and service capabilities across Europe.

- September 2023: John Deere and Yara partnered to improve fertilizer efficiency and crop yields through precision technology and agronomic expertise.

Strategic Outlook for Europe Farm Equipment Industry Market

The European farm equipment market is poised for continued substantial growth, fueled by the relentless pace of technological innovation, a rising demand for sustainable agricultural solutions, and the ongoing support from government initiatives. To secure a leading position in this evolving market, strategic partnerships, dedicated investments in research and development (R&D), and targeted expansion into specialized market niches will be paramount. The enduring focus on precision agriculture, the widespread integration of automation, and the leverage of data-driven decision-making processes will undoubtedly shape the industry's future landscape. Ultimately, companies that proactively embrace these transformative trends and demonstrate a keen ability to adapt to the ever-changing needs and expectations of modern farmers will be exceptionally well-positioned for enduring success and market leadership.

Europe Farm Equipment Industry Segmentation

- 1. Production Analysis

- 2. Consumption Analysis

- 3. Import Market Analysis (Value & Volume)

- 4. Export Market Analysis (Value & Volume)

- 5. Price Trend Analysis

Europe Farm Equipment Industry Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

Europe Farm Equipment Industry Regional Market Share

Geographic Coverage of Europe Farm Equipment Industry

Europe Farm Equipment Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.20% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Production Analysis

- 5.2. Market Analysis, Insights and Forecast - by Consumption Analysis

- 5.3. Market Analysis, Insights and Forecast - by Import Market Analysis (Value & Volume)

- 5.4. Market Analysis, Insights and Forecast - by Export Market Analysis (Value & Volume)

- 5.5. Market Analysis, Insights and Forecast - by Price Trend Analysis

- 5.6. Market Analysis, Insights and Forecast - by Region

- 5.6.1. Europe

- 6. Europe Farm Equipment Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Production Analysis

- 6.2. Market Analysis, Insights and Forecast - by Consumption Analysis

- 6.3. Market Analysis, Insights and Forecast - by Import Market Analysis (Value & Volume)

- 6.4. Market Analysis, Insights and Forecast - by Export Market Analysis (Value & Volume)

- 6.5. Market Analysis, Insights and Forecast - by Price Trend Analysis

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Deere & Company

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Kubota Corporation

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 AGCO Corporation

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Yanmar Co Ltd

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Same Deutz-Fahr

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 CNH Industrial NV

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 CLAAS KGaA mbH

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Kuhn Group*List Not Exhaustive

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Lely France

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.1 Deere & Company

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Europe Farm Equipment Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Europe Farm Equipment Industry Share (%) by Company 2025

List of Tables

- Table 1: Europe Farm Equipment Industry Revenue Million Forecast, by Production Analysis 2020 & 2033

- Table 2: Europe Farm Equipment Industry Revenue Million Forecast, by Consumption Analysis 2020 & 2033

- Table 3: Europe Farm Equipment Industry Revenue Million Forecast, by Import Market Analysis (Value & Volume) 2020 & 2033

- Table 4: Europe Farm Equipment Industry Revenue Million Forecast, by Export Market Analysis (Value & Volume) 2020 & 2033

- Table 5: Europe Farm Equipment Industry Revenue Million Forecast, by Price Trend Analysis 2020 & 2033

- Table 6: Europe Farm Equipment Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 7: Europe Farm Equipment Industry Revenue Million Forecast, by Production Analysis 2020 & 2033

- Table 8: Europe Farm Equipment Industry Revenue Million Forecast, by Consumption Analysis 2020 & 2033

- Table 9: Europe Farm Equipment Industry Revenue Million Forecast, by Import Market Analysis (Value & Volume) 2020 & 2033

- Table 10: Europe Farm Equipment Industry Revenue Million Forecast, by Export Market Analysis (Value & Volume) 2020 & 2033

- Table 11: Europe Farm Equipment Industry Revenue Million Forecast, by Price Trend Analysis 2020 & 2033

- Table 12: Europe Farm Equipment Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 13: United Kingdom Europe Farm Equipment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: Germany Europe Farm Equipment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: France Europe Farm Equipment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Italy Europe Farm Equipment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: Spain Europe Farm Equipment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Netherlands Europe Farm Equipment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 19: Belgium Europe Farm Equipment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: Sweden Europe Farm Equipment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 21: Norway Europe Farm Equipment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Poland Europe Farm Equipment Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 23: Denmark Europe Farm Equipment Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Farm Equipment Industry?

The projected CAGR is approximately 3.20%.

2. Which companies are prominent players in the Europe Farm Equipment Industry?

Key companies in the market include Deere & Company, Kubota Corporation, AGCO Corporation, Yanmar Co Ltd, Same Deutz-Fahr, CNH Industrial NV, CLAAS KGaA mbH, Kuhn Group*List Not Exhaustive, Lely France.

3. What are the main segments of the Europe Farm Equipment Industry?

The market segments include Production Analysis, Consumption Analysis, Import Market Analysis (Value & Volume), Export Market Analysis (Value & Volume), Price Trend Analysis.

4. Can you provide details about the market size?

The market size is estimated to be USD 42.03 Million as of 2022.

5. What are some drivers contributing to market growth?

Shortage of Skilled Labor; Government Support to Enhance Farm Mechanization.

6. What are the notable trends driving market growth?

Shortage of Skilled Labor.

7. Are there any restraints impacting market growth?

Heavy Initial Procurement Cost and High Expenditure on Maintenance.

8. Can you provide examples of recent developments in the market?

November 2023: CNH Industrial NV unveiled CR11 New Holland combine at Agritechnica '23. Its 775-horsepower C16 engine powers 2x24-inch rotors, while the 567-bushel (20,000-liter) grain tank ensures ample storage capacity. With a rapid six bushels (210 liters) per second unload rate, the CR11 minimizes grain loss.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Farm Equipment Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Farm Equipment Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Farm Equipment Industry?

To stay informed about further developments, trends, and reports in the Europe Farm Equipment Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence