Key Insights

The global carrier screening tests market is poised for significant expansion, projected to reach a substantial $1.64 billion by 2025, driven by an impressive compound annual growth rate (CAGR) of 12.55%. This robust growth is primarily fueled by increasing awareness of genetic disorders and the proactive desire among individuals and couples to understand their reproductive health risks. The escalating adoption of advanced sequencing technologies, such as Next-Generation Sequencing (NGS) and Whole Exome Sequencing (WES), is making carrier screening more comprehensive and accessible, allowing for the detection of a wider array of genetic conditions. Furthermore, a growing emphasis on personalized medicine and preventative healthcare strategies is steering individuals towards genetic testing for informed family planning decisions. The market is also benefiting from supportive government initiatives promoting genetic counseling and screening programs, aimed at reducing the incidence of hereditary diseases.

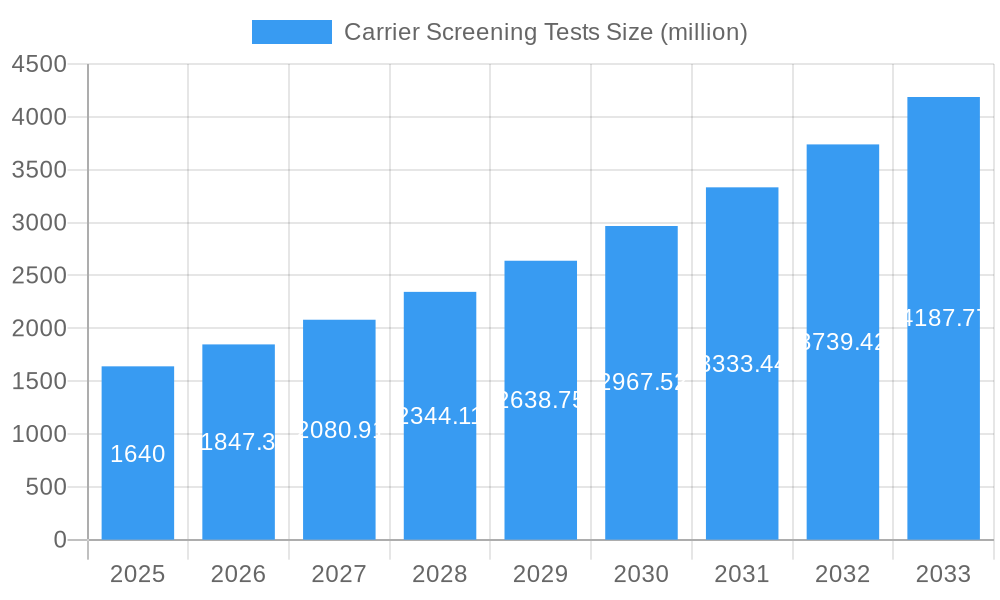

Carrier Screening Tests Market Size (In Billion)

The market's trajectory is further shaped by evolving trends in reproductive technologies and a rising prevalence of genetic predispositions. While the market demonstrates strong upward momentum, potential restraints such as the high cost of advanced genetic testing, limited reimbursement policies in certain regions, and the need for greater genetic literacy among the general population could pose challenges. However, ongoing research and development efforts focused on reducing testing costs and improving diagnostic accuracy, coupled with strategic collaborations between key market players and healthcare providers, are expected to mitigate these limitations. The segmentation of the market by application, encompassing both couple and individual screening, highlights the broad appeal of these tests. Innovations in point-of-care testing and direct-to-consumer genetic services are also contributing to market accessibility and growth.

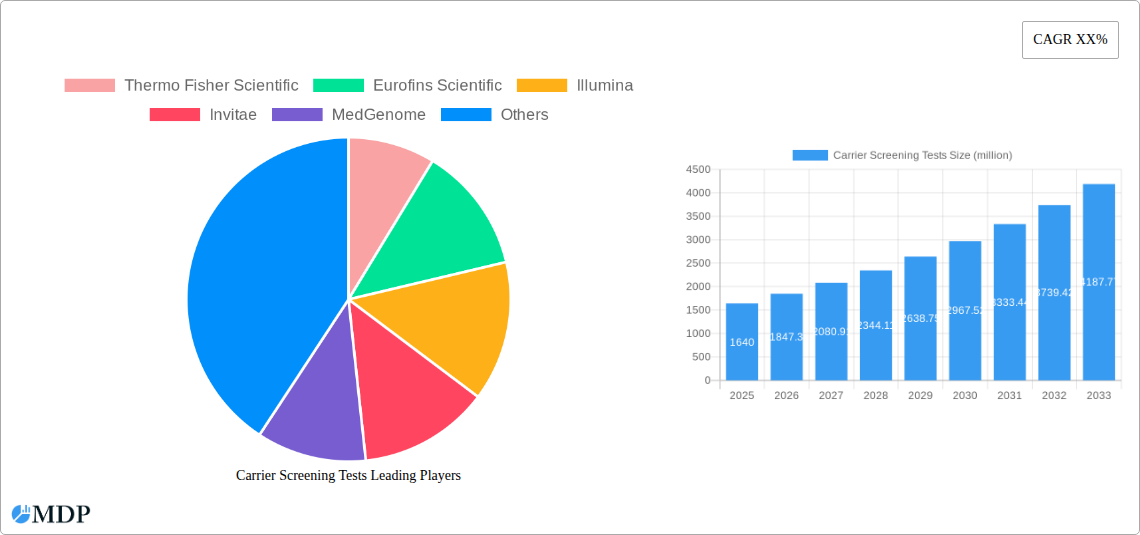

Carrier Screening Tests Company Market Share

Here is an SEO-optimized, engaging report description for Carrier Screening Tests, designed for maximum search visibility and to attract industry stakeholders, with no placeholders and all values in billions.

Unlock deep insights into the rapidly evolving carrier screening tests market. This definitive report analyzes key market dynamics, technological advancements, regional dominance, and strategic opportunities within the global carrier screening tests industry. With a study period spanning 2019–2033, a base year of 2025, and a forecast period from 2025–2033, this analysis provides actionable intelligence for industry stakeholders, including manufacturers, R&D professionals, investors, and policymakers.

Carrier Screening Tests Market Dynamics & Concentration

The global carrier screening tests market is characterized by a moderate concentration, with a significant presence of both established multinational corporations and emerging specialized players. Innovation remains a primary driver, fueled by advancements in Next-Generation Sequencing (NGS) and an increasing understanding of genetic predispositions. Regulatory frameworks, such as those from the FDA and EMA, are continuously evolving to ensure the safety and efficacy of these tests, influencing product development and market access. Product substitutes, while limited in their direct genetic coverage, include traditional prenatal diagnostic methods. End-user trends show a growing preference for comprehensive panel testing and direct-to-consumer (DTC) genetic screening, particularly for the 'Couple' application segment. Mergers and acquisitions (M&A) activities are moderately active, with approximately 15 major deals recorded historically, aimed at consolidating market share, expanding product portfolios, and acquiring new technologies. Companies like Thermo Fisher Scientific and Illumina hold substantial market shares, estimated to be over $2.5 billion and $3.2 billion respectively, while Invitae and Natera are also significant contributors. The overall market value is projected to reach over $15.0 billion by the forecast year 2025, with M&A deal values in the billions, reflecting strategic consolidation.

Carrier Screening Tests Industry Trends & Analysis

The carrier screening tests industry is poised for robust growth, driven by a confluence of factors including rising awareness of genetic health, the increasing prevalence of hereditary diseases, and significant technological breakthroughs. The market penetration of carrier screening tests is projected to escalate from approximately 20% in the historical period to over 40% by the end of the forecast period. A key growth driver is the expanding application of Next-Generation Sequencing (NGS), which has dramatically increased the scope and accuracy of genetic analysis at a reduced cost, significantly impacting market dynamics and enabling the identification of a wider array of genetic mutations. The Whole Exome Sequencing (WES) segment, in particular, is experiencing accelerated adoption due to its comprehensive genomic coverage. Consumer preferences are shifting towards proactive health management, with individuals increasingly opting for Individual screening alongside traditional Couple screening. The growing acceptance of genetic testing for family planning and the desire to prevent the transmission of genetic disorders are paramount. Economically, rising disposable incomes in emerging economies are further fueling demand. Competitive dynamics are intensifying, with players focusing on expanding their test menus, enhancing diagnostic accuracy, and developing user-friendly platforms. Strategic partnerships between diagnostic labs and healthcare providers are becoming more common, aiming to integrate carrier screening into routine reproductive healthcare. The market is anticipated to witness a Compound Annual Growth Rate (CAGR) of approximately 12.5% over the forecast period, reaching a market size estimated to exceed $30.0 billion by 2033. Technological disruptions, such as the integration of artificial intelligence (AI) for data analysis and interpretation, are further revolutionizing the field, promising enhanced diagnostic precision and more personalized genetic insights. The market value for the Couple segment alone is expected to surpass $18.0 billion by 2033, while the Individual segment is projected to grow to over $12.0 billion.

Leading Markets & Segments in Carrier Screening Tests

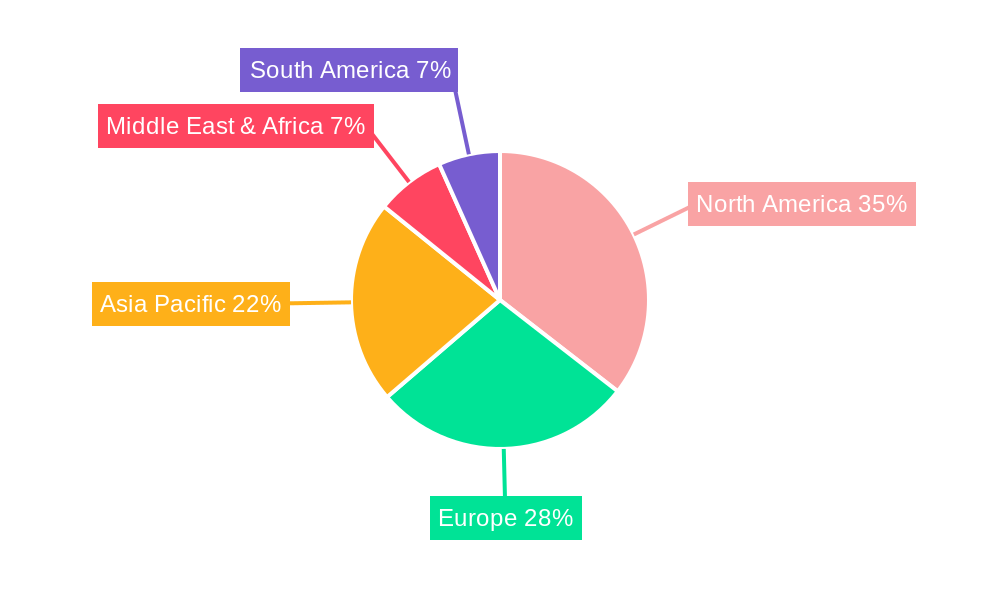

The North America region currently dominates the global carrier screening tests market, driven by a strong healthcare infrastructure, high disposable incomes, and a proactive approach to genetic health. Within North America, the United States stands out as the leading country, accounting for an estimated 65% of the regional market value, which is projected to exceed $10.0 billion by 2025. Key drivers for this dominance include robust government funding for genetic research, widespread adoption of advanced diagnostic technologies like NGS, and extensive public awareness campaigns. Economic policies favorable to healthcare innovation and significant investments by private equity firms in biotech and diagnostics further bolster the market. The Couple application segment is the most significant contributor to the overall market revenue, projected to reach over $18.0 billion by 2033. This is largely due to the widespread practice of preconception and prenatal genetic screening among couples planning to have children, aiming to identify potential carriers of recessive genetic disorders. The NGS type segment is also a major growth engine, expected to capture over 70% of the market share by 2033 due to its superior accuracy, speed, and ability to analyze multiple genes simultaneously. The market penetration of NGS-based carrier screening is estimated to reach over 80% within the dominant segments. Factors such as favorable reimbursement policies for genetic testing and the presence of leading players like Thermo Fisher Scientific, Illumina, and Invitae, with substantial market shares in the billions, solidify North America's leading position.

Carrier Screening Tests Product Developments

Recent product developments in carrier screening tests are focused on expanding the number of genes analyzed, enhancing assay sensitivity, and integrating artificial intelligence for improved interpretation of complex genetic data. Innovations in NGS technology have enabled the development of comprehensive panels that can screen for hundreds of genetic conditions simultaneously, offering a more efficient and cost-effective solution for both couple and individual testing. Companies are also focusing on developing user-friendly platforms and mobile applications to enhance the patient experience and facilitate data accessibility. Competitive advantages are being gained through superior analytical accuracy, broader gene coverage, and faster turnaround times, making these tests more appealing to healthcare providers and consumers alike, contributing to an estimated market value increase of over $5.0 billion in innovative product segments.

Key Drivers of Carrier Screening Tests Growth

The growth of the carrier screening tests market is significantly propelled by technological advancements, particularly the widespread adoption and decreasing cost of Next-Generation Sequencing (NGS), which enables the analysis of a broader spectrum of genes with higher accuracy. Increasing awareness among the general population and healthcare professionals about the benefits of genetic screening for family planning and disease prevention is a critical driver. Furthermore, favorable regulatory environments in key markets and the increasing prevalence of hereditary genetic disorders worldwide contribute to sustained market expansion. Economic factors, such as rising disposable incomes and improved healthcare access in emerging economies, also play a crucial role, estimated to contribute over $8.0 billion to market growth over the forecast period.

Challenges in the Carrier Screening Tests Market

Despite robust growth, the carrier screening tests market faces several challenges. Regulatory hurdles and the need for stringent validation of new genetic tests can slow down market entry and adoption. Reimbursement policies for genetic testing vary significantly across different healthcare systems and insurance providers, impacting patient access and affordability. High upfront costs associated with advanced sequencing technologies, although declining, can still be a barrier for some healthcare providers and individuals. Additionally, ethical concerns and the need for comprehensive genetic counseling to interpret results accurately present ongoing challenges. Supply chain disruptions for reagents and specialized equipment can also impact production and delivery timelines, with potential market impact in the hundreds of millions.

Emerging Opportunities in Carrier Screening Tests

Emerging opportunities in the carrier screening tests market are primarily driven by the expansion of genetic testing into new geographical regions, particularly in developing economies with growing healthcare awareness. Technological breakthroughs in liquid biopsy and non-invasive prenatal testing (NIPT) are creating new avenues for early detection and screening. Strategic partnerships between diagnostic companies, pharmaceutical firms, and academic research institutions are fostering innovation and accelerating the development of novel diagnostic solutions. The increasing focus on personalized medicine and pharmacogenomics presents a significant long-term growth catalyst, allowing for tailored treatment strategies based on an individual's genetic profile, estimated to unlock billions in new market segments.

Leading Players in the Carrier Screening Tests Sector

- Thermo Fisher Scientific

- Eurofins Scientific

- Illumina

- Invitae

- MedGenome

- Myriad Genetics

- Roche

- Natera

- OPKO Health

- 23andMe

- bioMérieux

- EKF Diagnostics

- Gene by Gene (myDNA)

- Fulgent Genetics

- NxGen MDx

- Sonic Genetics

- My Baby

- AncestryDNA

- DiaSorin

- Grifols

- BGI Genomics

- Chigene

- Jiajian Medical Testing

- Genesky

- Berry Genomics

- Weihansi Biomedical Technology

- Annaroad

Key Milestones in Carrier Screening Tests Industry

- 2019: Introduction of broader gene panels for carrier screening, expanding coverage for recessive disorders.

- 2020: Increased adoption of NGS-based carrier screening by major diagnostic laboratories.

- 2021: Development of AI-powered interpretation tools for genetic variants in carrier screening.

- 2022: Launch of direct-to-consumer (DTC) carrier screening kits with enhanced user interfaces.

- 2023: Significant M&A activity, with several key players acquiring smaller, innovative genetic testing companies.

- 2024: Regulatory approvals for new comprehensive carrier screening panels in major markets.

Strategic Outlook for Carrier Screening Tests Market

The strategic outlook for the carrier screening tests market is exceptionally positive, driven by continued technological innovation, increasing global demand for genetic health solutions, and favorable demographic trends. Key growth accelerators include the expansion of NGS capabilities to cover rare genetic diseases, the integration of carrier screening into routine healthcare check-ups, and the development of more accessible and affordable testing options. Strategic partnerships between industry players and healthcare providers will be crucial for market penetration, while investments in R&D will fuel the development of next-generation screening technologies. The market is projected to witness substantial growth, with an estimated total market value exceeding $50.0 billion by 2033, underscoring its immense future potential.

Carrier Screening Tests Segmentation

-

1. Application

- 1.1. Couple

- 1.2. Individual

-

2. Types

- 2.1. NGS

- 2.2. Whole Exome Sequencing

- 2.3. Others

Carrier Screening Tests Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Carrier Screening Tests Regional Market Share

Geographic Coverage of Carrier Screening Tests

Carrier Screening Tests REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.55% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Couple

- 5.1.2. Individual

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. NGS

- 5.2.2. Whole Exome Sequencing

- 5.2.3. Others

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. Global Carrier Screening Tests Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Couple

- 6.1.2. Individual

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. NGS

- 6.2.2. Whole Exome Sequencing

- 6.2.3. Others

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. North America Carrier Screening Tests Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Couple

- 7.1.2. Individual

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. NGS

- 7.2.2. Whole Exome Sequencing

- 7.2.3. Others

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. South America Carrier Screening Tests Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Couple

- 8.1.2. Individual

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. NGS

- 8.2.2. Whole Exome Sequencing

- 8.2.3. Others

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Europe Carrier Screening Tests Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Couple

- 9.1.2. Individual

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. NGS

- 9.2.2. Whole Exome Sequencing

- 9.2.3. Others

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Middle East & Africa Carrier Screening Tests Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Couple

- 10.1.2. Individual

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. NGS

- 10.2.2. Whole Exome Sequencing

- 10.2.3. Others

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Asia Pacific Carrier Screening Tests Analysis, Insights and Forecast, 2020-2032

- 11.1. Market Analysis, Insights and Forecast - by Application

- 11.1.1. Couple

- 11.1.2. Individual

- 11.2. Market Analysis, Insights and Forecast - by Types

- 11.2.1. NGS

- 11.2.2. Whole Exome Sequencing

- 11.2.3. Others

- 11.1. Market Analysis, Insights and Forecast - by Application

- 12. Competitive Analysis

- 12.1. Company Profiles

- 12.1.1 Thermo Fisher Scientific

- 12.1.1.1. Company Overview

- 12.1.1.2. Products

- 12.1.1.3. Company Financials

- 12.1.1.4. SWOT Analysis

- 12.1.2 Eurofins Scientific

- 12.1.2.1. Company Overview

- 12.1.2.2. Products

- 12.1.2.3. Company Financials

- 12.1.2.4. SWOT Analysis

- 12.1.3 Illumina

- 12.1.3.1. Company Overview

- 12.1.3.2. Products

- 12.1.3.3. Company Financials

- 12.1.3.4. SWOT Analysis

- 12.1.4 Invitae

- 12.1.4.1. Company Overview

- 12.1.4.2. Products

- 12.1.4.3. Company Financials

- 12.1.4.4. SWOT Analysis

- 12.1.5 MedGenome

- 12.1.5.1. Company Overview

- 12.1.5.2. Products

- 12.1.5.3. Company Financials

- 12.1.5.4. SWOT Analysis

- 12.1.6 Myriad Genetics

- 12.1.6.1. Company Overview

- 12.1.6.2. Products

- 12.1.6.3. Company Financials

- 12.1.6.4. SWOT Analysis

- 12.1.7 Roche

- 12.1.7.1. Company Overview

- 12.1.7.2. Products

- 12.1.7.3. Company Financials

- 12.1.7.4. SWOT Analysis

- 12.1.8 Natera

- 12.1.8.1. Company Overview

- 12.1.8.2. Products

- 12.1.8.3. Company Financials

- 12.1.8.4. SWOT Analysis

- 12.1.9 OPKO Health

- 12.1.9.1. Company Overview

- 12.1.9.2. Products

- 12.1.9.3. Company Financials

- 12.1.9.4. SWOT Analysis

- 12.1.10 23andMe

- 12.1.10.1. Company Overview

- 12.1.10.2. Products

- 12.1.10.3. Company Financials

- 12.1.10.4. SWOT Analysis

- 12.1.11 bioMérieux

- 12.1.11.1. Company Overview

- 12.1.11.2. Products

- 12.1.11.3. Company Financials

- 12.1.11.4. SWOT Analysis

- 12.1.12 EKF Diagnostics

- 12.1.12.1. Company Overview

- 12.1.12.2. Products

- 12.1.12.3. Company Financials

- 12.1.12.4. SWOT Analysis

- 12.1.13 Gene by Gene (myDNA)

- 12.1.13.1. Company Overview

- 12.1.13.2. Products

- 12.1.13.3. Company Financials

- 12.1.13.4. SWOT Analysis

- 12.1.14 Fulgent Genetics

- 12.1.14.1. Company Overview

- 12.1.14.2. Products

- 12.1.14.3. Company Financials

- 12.1.14.4. SWOT Analysis

- 12.1.15 NxGen MDx

- 12.1.15.1. Company Overview

- 12.1.15.2. Products

- 12.1.15.3. Company Financials

- 12.1.15.4. SWOT Analysis

- 12.1.16 Sonic Genetics

- 12.1.16.1. Company Overview

- 12.1.16.2. Products

- 12.1.16.3. Company Financials

- 12.1.16.4. SWOT Analysis

- 12.1.17 My Baby

- 12.1.17.1. Company Overview

- 12.1.17.2. Products

- 12.1.17.3. Company Financials

- 12.1.17.4. SWOT Analysis

- 12.1.18 AncestryDNA

- 12.1.18.1. Company Overview

- 12.1.18.2. Products

- 12.1.18.3. Company Financials

- 12.1.18.4. SWOT Analysis

- 12.1.19 DiaSorin

- 12.1.19.1. Company Overview

- 12.1.19.2. Products

- 12.1.19.3. Company Financials

- 12.1.19.4. SWOT Analysis

- 12.1.20 Grifols

- 12.1.20.1. Company Overview

- 12.1.20.2. Products

- 12.1.20.3. Company Financials

- 12.1.20.4. SWOT Analysis

- 12.1.21 BGI Genomics

- 12.1.21.1. Company Overview

- 12.1.21.2. Products

- 12.1.21.3. Company Financials

- 12.1.21.4. SWOT Analysis

- 12.1.22 Chigene

- 12.1.22.1. Company Overview

- 12.1.22.2. Products

- 12.1.22.3. Company Financials

- 12.1.22.4. SWOT Analysis

- 12.1.23 Jiajian Medical Testing

- 12.1.23.1. Company Overview

- 12.1.23.2. Products

- 12.1.23.3. Company Financials

- 12.1.23.4. SWOT Analysis

- 12.1.24 Genesky

- 12.1.24.1. Company Overview

- 12.1.24.2. Products

- 12.1.24.3. Company Financials

- 12.1.24.4. SWOT Analysis

- 12.1.25 Berry Genomics

- 12.1.25.1. Company Overview

- 12.1.25.2. Products

- 12.1.25.3. Company Financials

- 12.1.25.4. SWOT Analysis

- 12.1.26 Weihansi Biomedical Technology

- 12.1.26.1. Company Overview

- 12.1.26.2. Products

- 12.1.26.3. Company Financials

- 12.1.26.4. SWOT Analysis

- 12.1.27 Annaroad

- 12.1.27.1. Company Overview

- 12.1.27.2. Products

- 12.1.27.3. Company Financials

- 12.1.27.4. SWOT Analysis

- 12.1.1 Thermo Fisher Scientific

- 12.2. Market Entropy

- 12.2.1 Company's Key Areas Served

- 12.2.2 Recent Developments

- 12.3. Company Market Share Analysis 2025

- 12.3.1 Top 5 Companies Market Share Analysis

- 12.3.2 Top 3 Companies Market Share Analysis

- 12.4. List of Potential Customers

- 13. Research Methodology

List of Figures

- Figure 1: Global Carrier Screening Tests Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Carrier Screening Tests Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Carrier Screening Tests Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Carrier Screening Tests Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Carrier Screening Tests Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Carrier Screening Tests Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Carrier Screening Tests Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Carrier Screening Tests Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Carrier Screening Tests Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Carrier Screening Tests Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Carrier Screening Tests Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Carrier Screening Tests Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Carrier Screening Tests Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Carrier Screening Tests Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Carrier Screening Tests Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Carrier Screening Tests Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Carrier Screening Tests Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Carrier Screening Tests Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Carrier Screening Tests Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Carrier Screening Tests Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Carrier Screening Tests Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Carrier Screening Tests Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Carrier Screening Tests Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Carrier Screening Tests Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Carrier Screening Tests Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Carrier Screening Tests Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Carrier Screening Tests Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Carrier Screening Tests Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Carrier Screening Tests Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Carrier Screening Tests Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Carrier Screening Tests Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Carrier Screening Tests Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Carrier Screening Tests Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Carrier Screening Tests Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Carrier Screening Tests Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Carrier Screening Tests Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Carrier Screening Tests Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Carrier Screening Tests Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Carrier Screening Tests Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Carrier Screening Tests Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Carrier Screening Tests Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Carrier Screening Tests Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Carrier Screening Tests Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Carrier Screening Tests Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Carrier Screening Tests Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Carrier Screening Tests Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Carrier Screening Tests Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Carrier Screening Tests Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Carrier Screening Tests Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Carrier Screening Tests Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Carrier Screening Tests Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Carrier Screening Tests Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Carrier Screening Tests Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Carrier Screening Tests Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Carrier Screening Tests Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Carrier Screening Tests Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Carrier Screening Tests Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Carrier Screening Tests Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Carrier Screening Tests Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Carrier Screening Tests Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Carrier Screening Tests Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Carrier Screening Tests Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Carrier Screening Tests Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Carrier Screening Tests Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Carrier Screening Tests Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Carrier Screening Tests Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Carrier Screening Tests Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Carrier Screening Tests Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Carrier Screening Tests Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Carrier Screening Tests Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Carrier Screening Tests Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Carrier Screening Tests Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Carrier Screening Tests Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Carrier Screening Tests Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Carrier Screening Tests Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Carrier Screening Tests Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Carrier Screening Tests Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Carrier Screening Tests?

The projected CAGR is approximately 12.55%.

2. Which companies are prominent players in the Carrier Screening Tests?

Key companies in the market include Thermo Fisher Scientific, Eurofins Scientific, Illumina, Invitae, MedGenome, Myriad Genetics, Roche, Natera, OPKO Health, 23andMe, bioMérieux, EKF Diagnostics, Gene by Gene (myDNA), Fulgent Genetics, NxGen MDx, Sonic Genetics, My Baby, AncestryDNA, DiaSorin, Grifols, BGI Genomics, Chigene, Jiajian Medical Testing, Genesky, Berry Genomics, Weihansi Biomedical Technology, Annaroad.

3. What are the main segments of the Carrier Screening Tests?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4350.00, USD 6525.00, and USD 8700.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Carrier Screening Tests," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Carrier Screening Tests report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Carrier Screening Tests?

To stay informed about further developments, trends, and reports in the Carrier Screening Tests, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence