Key Insights

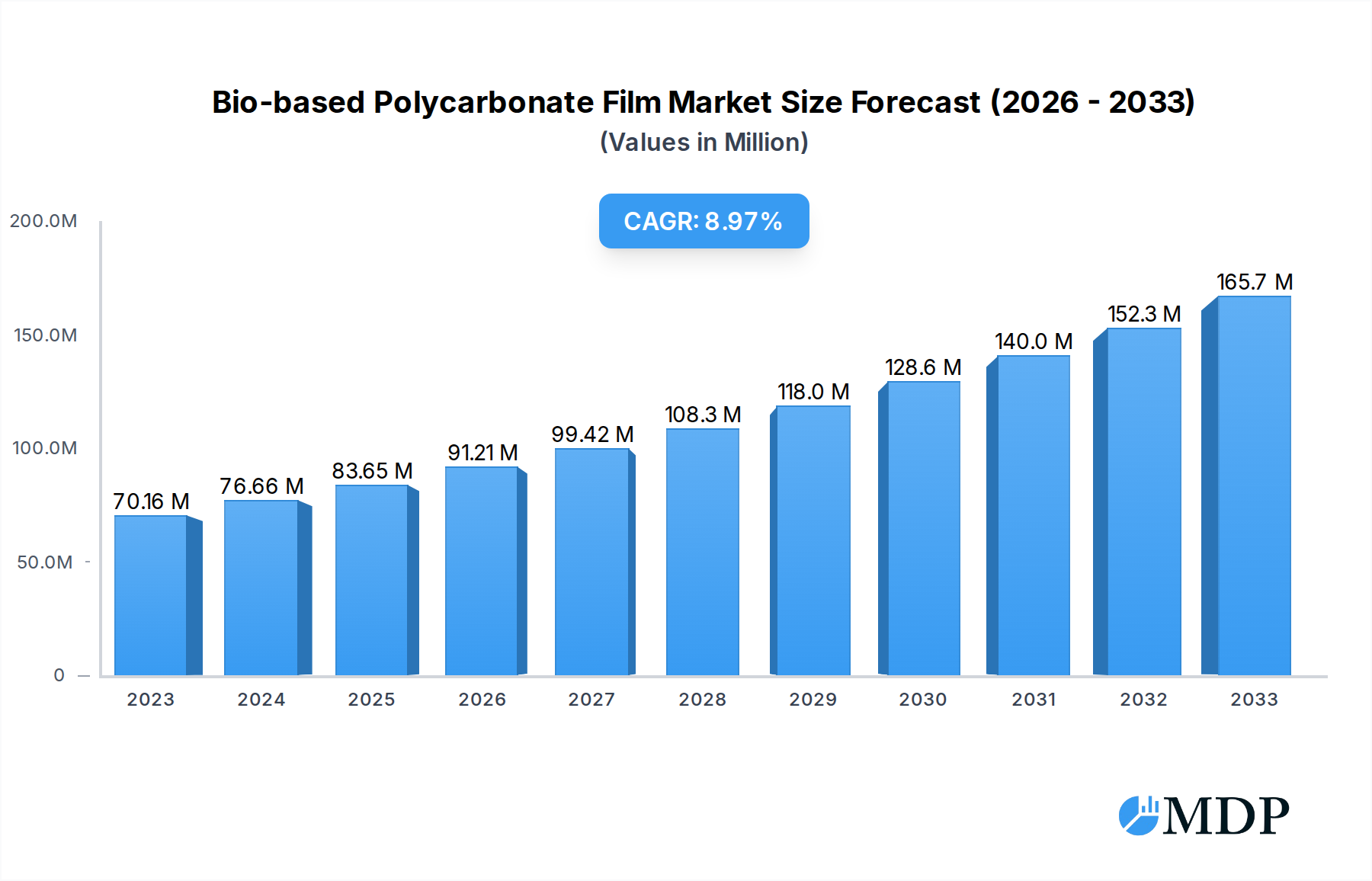

The global Bio-based Polycarbonate Film market is poised for robust expansion, exhibiting a strong CAGR of 9.11% and reaching an estimated market size of $70.16 million in 2023. This growth is propelled by an increasing demand for sustainable and eco-friendly materials across diverse applications. Key drivers include stringent environmental regulations, a growing consumer preference for green products, and advancements in bio-based material technology that enhance performance and cost-effectiveness. The market is witnessing significant penetration in the automotive sector, where lightweight and recyclable bio-based polycarbonate films contribute to fuel efficiency and reduced environmental impact. Similarly, the electronics industry is adopting these films for their excellent optical clarity, electrical insulation properties, and sustainable sourcing, particularly in display technologies and protective casings.

Bio-based Polycarbonate Film Market Size (In Million)

The market's trajectory is further shaped by evolving trends, such as the development of novel bio-based feedstocks and improved manufacturing processes that enhance the biodegradability and compostability of these films. While the widespread adoption faces challenges including higher initial production costs compared to conventional polycarbonates and the need for established recycling infrastructure, these are being systematically addressed through technological innovation and industry collaboration. Companies like Covestro, SABIC, and Mitsubishi Chemical are at the forefront, investing heavily in research and development to expand their bio-based product portfolios and meet the escalating demand for sustainable material solutions. The forecast period from 2025-2033 anticipates sustained growth, underscoring the transformative potential of bio-based polycarbonate films in creating a more circular and sustainable economy.

Bio-based Polycarbonate Film Company Market Share

Unleash Sustainable Innovation: Bio-based Polycarbonate Film Market Report 2024-2033

Gain unparalleled insights into the burgeoning bio-based polycarbonate film market with this comprehensive report. Spanning a detailed historical analysis from 2019-2024, a robust base year of 2025, and an extensive forecast period through 2033, this report provides actionable intelligence for stakeholders seeking to capitalize on the shift towards sustainable materials. Discover market dynamics, key trends, leading players like Covestro, SABIC, and Mitsubishi Chemical, and critical growth drivers within applications such as Automobiles and Electronics, and types like Plant-based and Other Source.

Bio-based Polycarbonate Film Market Dynamics & Concentration

The bio-based polycarbonate film market exhibits a dynamic and evolving concentration. Driven by increasing environmental consciousness and stringent regulations mandating the use of sustainable materials, market players are intensely focused on innovation and R&D. Key drivers include the development of novel bio-monomers and advanced polymerization techniques that enhance film properties like clarity, durability, and thermal resistance. Regulatory frameworks, particularly in Europe and North America, are increasingly favoring bio-based materials, creating a significant tailwind for market expansion. Product substitutes, while present in niche applications, are increasingly struggling to match the performance and sustainability credentials of advanced bio-polycarbonate films. End-user trends strongly point towards a preference for lightweight, recyclable, and responsibly sourced materials, especially in high-visibility sectors. Mergers and acquisition (M&A) activities are a significant indicator of market consolidation and strategic positioning. We project approximately 15 M&A deals within the forecast period, indicating strong investor confidence and a drive to acquire cutting-edge technologies and market share. Leading players such as Covestro, SABIC, and Mitsubishi Chemical hold a substantial combined market share, estimated at over 60%, but emerging players are actively gaining traction through specialized offerings.

Bio-based Polycarbonate Film Industry Trends & Analysis

The global bio-based polycarbonate film market is experiencing robust growth, fueled by a confluence of technological advancements, escalating consumer demand for sustainable products, and supportive government policies. Over the historical period (2019-2024), the market has witnessed a significant CAGR of approximately 12%, a trend projected to continue with a forecasted CAGR of 13.5% from 2025 to 2033. This impressive trajectory is underpinned by several key growth drivers. Technologically, breakthroughs in bio-monomer extraction and synthesis are enabling the production of high-performance polycarbonate films with properties rivaling or exceeding their petroleum-based counterparts. Innovations in polymer processing and film extrusion are further enhancing efficiency and scalability, making bio-based alternatives more economically viable. Consumer preferences are decisively shifting towards eco-friendly products, with a growing awareness of the environmental impact of traditional plastics. This is particularly evident in sectors like consumer electronics and automotive, where brands are actively seeking to improve their sustainability credentials. The competitive landscape is characterized by increasing R&D investments, strategic partnerships between material suppliers and end-users, and a growing number of new entrants. Market penetration for bio-based polycarbonate films, while still nascent compared to conventional plastics, is projected to reach over 25% by 2033, indicating substantial room for expansion. The emphasis on circular economy principles and the development of biodegradable or compostable bio-polycarbonate variants are also emerging as significant trends, appealing to environmentally conscious consumers and businesses alike. This evolving market necessitates continuous adaptation and innovation from all stakeholders.

Leading Markets & Segments in Bio-based Polycarbonate Film

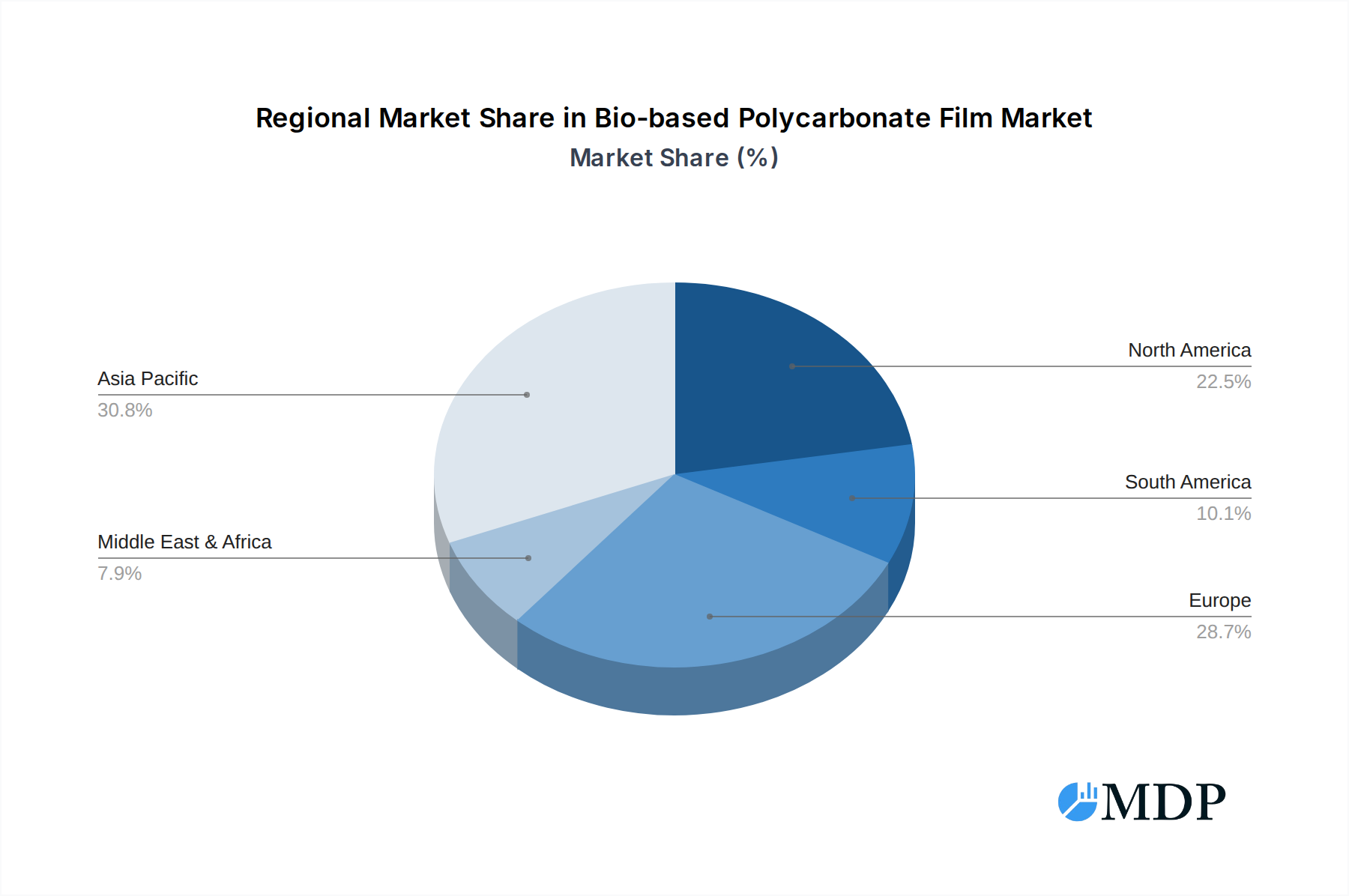

The bio-based polycarbonate film market is experiencing dominant growth in the Asia-Pacific region, driven by its robust manufacturing base, expanding automotive and electronics industries, and increasing government initiatives promoting sustainable development. Within this region, China is a leading market due to its sheer industrial output and proactive adoption of green technologies. The Automobiles application segment stands out as a primary driver, with manufacturers actively incorporating bio-based polycarbonate films for interior components, lighting, and lightweighting strategies to meet fuel efficiency standards and consumer demand for eco-friendly vehicles. Key drivers for this dominance include:

- Economic Policies: Favorable government incentives and subsidies for sustainable manufacturing and the adoption of bio-based materials in the automotive sector.

- Infrastructure: Well-established automotive manufacturing infrastructure and a readily available supply chain for advanced materials.

The Electronics segment also exhibits significant growth, fueled by the demand for sustainable materials in consumer electronics, displays, and protective casings. Companies are increasingly prioritizing the use of bio-based alternatives to reduce their carbon footprint and appeal to environmentally conscious consumers. Key drivers for dominance in this segment include:

- Technological Advancements: Continuous innovation in electronics requiring lightweight, durable, and aesthetically pleasing materials, with bio-polycarbonate films offering a compelling sustainable solution.

- Consumer Preferences: A strong and growing consumer demand for ethically sourced and environmentally friendly electronic devices.

In terms of Types, the Plant-based source segment is leading the market due to its established availability of feedstocks and advanced processing technologies. The development of novel bio-monomers derived from renewable resources like corn, sugarcane, and biomass is enabling the production of high-quality bio-polycarbonate films. Key drivers for the dominance of plant-based sources include:

- Feedstock Availability: The widespread availability and established supply chains for various plant-based feedstocks.

- Technological Maturity: Significant advancements in the chemical processes required to convert plant-based materials into the necessary monomers for polycarbonate production.

The Other Source category, while currently smaller, is poised for future growth as research into alternative bio-feedstocks, such as algae or waste streams, progresses.

Bio-based Polycarbonate Film Product Developments

Product development in the bio-based polycarbonate film sector is characterized by a strong focus on enhancing performance attributes and expanding application possibilities. Innovations are centered on improving scratch resistance, UV stability, and flame retardancy while maintaining a high degree of optical clarity and impact strength. Companies are developing specialized grades for demanding applications in automotive interiors, advanced electronic displays, and durable consumer goods. The competitive advantage lies in offering films with a demonstrably lower carbon footprint, improved recyclability, and compliance with increasingly stringent environmental regulations, thereby enabling manufacturers to achieve their sustainability targets and differentiate their products in the market.

Key Drivers of Bio-based Polycarbonate Film Growth

The bio-based polycarbonate film market is propelled by a powerful combination of factors. Technological advancements in polymerization processes and bio-monomer sourcing are making these films increasingly competitive in terms of performance and cost. Growing consumer and corporate demand for sustainable and eco-friendly materials, driven by heightened environmental awareness, is a significant market pull. Furthermore, stringent government regulations and mandates promoting the use of renewable resources and reducing reliance on fossil fuels are creating a favorable policy environment. Economic incentives, such as tax breaks and subsidies for bio-based product development and adoption, further accelerate market penetration.

Challenges in the Bio-based Polycarbonate Film Market

Despite its promising growth, the bio-based polycarbonate film market faces several challenges. The higher initial production costs compared to conventional petroleum-based polycarbonate can be a significant barrier to widespread adoption, especially in price-sensitive markets. Supply chain complexities and the need for specialized infrastructure to source and process bio-based feedstocks can also present hurdles. Furthermore, fluctuating raw material prices and the availability of sufficient bio-feedstock volumes can impact production stability and cost-effectiveness. Finally, competition from established petroleum-based alternatives and the ongoing need for extensive lifecycle analysis and certifications to validate sustainability claims present ongoing challenges.

Emerging Opportunities in Bio-based Polycarbonate Film

Emerging opportunities in the bio-based polycarbonate film market are abundant and poised to drive long-term growth. Technological breakthroughs in advanced biorefinery processes and the development of novel bio-monomers from non-food biomass sources offer pathways to reduce production costs and improve sustainability credentials. Strategic partnerships between bio-material producers, film manufacturers, and end-users are crucial for co-developing tailored solutions and accelerating market adoption. Furthermore, the expansion into new and emerging applications, such as renewable energy components, medical devices, and sustainable packaging, presents significant growth potential. The increasing focus on circular economy principles also opens avenues for developing compostable or biodegradable bio-polycarbonate films.

Leading Players in the Bio-based Polycarbonate Film Sector

- Covestro

- SABIC

- Mitsubishi Chemical

Key Milestones in Bio-based Polycarbonate Film Industry

- 2019: Increased research and development into plant-based feedstocks for polycarbonate monomer production.

- 2020: First commercial pilot production of partially bio-based polycarbonate resins with a focus on automotive applications.

- 2021: Significant investment by major chemical companies in bio-based material infrastructure and R&D.

- 2022: Launch of new bio-based polycarbonate film grades offering enhanced properties like improved scratch resistance.

- 2023: Growing regulatory pressure and consumer demand for sustainable materials driving increased adoption in consumer electronics.

- 2024: Announcement of ambitious sustainability goals by key players, including increased use of bio-based materials in their product portfolios.

Strategic Outlook for Bio-based Polycarbonate Film Market

The strategic outlook for the bio-based polycarbonate film market is exceptionally bright. Growth accelerators will be driven by continued innovation in material science, leading to enhanced performance and cost competitiveness. The increasing demand for sustainable solutions across diverse industries, coupled with supportive government policies and incentives, will solidify market expansion. Strategic collaborations and vertical integration within the supply chain will further optimize production and market access. The market's trajectory points towards a significant shift away from conventional plastics, positioning bio-based polycarbonate films as a cornerstone of future sustainable material solutions.

Bio-based Polycarbonate Film Segmentation

-

1. Application

- 1.1. Automobiles

- 1.2. Electronics

- 1.3. Other

-

2. Types

- 2.1. Plant-based

- 2.2. Other Source

Bio-based Polycarbonate Film Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

-

2. South America

- 2.1. Brazil

- 2.2. Argentina

- 2.3. Rest of South America

-

3. Europe

- 3.1. United Kingdom

- 3.2. Germany

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Benelux

- 3.8. Nordics

- 3.9. Rest of Europe

-

4. Middle East & Africa

- 4.1. Turkey

- 4.2. Israel

- 4.3. GCC

- 4.4. North Africa

- 4.5. South Africa

- 4.6. Rest of Middle East & Africa

-

5. Asia Pacific

- 5.1. China

- 5.2. India

- 5.3. Japan

- 5.4. South Korea

- 5.5. ASEAN

- 5.6. Oceania

- 5.7. Rest of Asia Pacific

Bio-based Polycarbonate Film Regional Market Share

Geographic Coverage of Bio-based Polycarbonate Film

Bio-based Polycarbonate Film REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 9.11% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.3. Market Restrains

- 3.4. Market Trends

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Bio-based Polycarbonate Film Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Application

- 5.1.1. Automobiles

- 5.1.2. Electronics

- 5.1.3. Other

- 5.2. Market Analysis, Insights and Forecast - by Types

- 5.2.1. Plant-based

- 5.2.2. Other Source

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. South America

- 5.3.3. Europe

- 5.3.4. Middle East & Africa

- 5.3.5. Asia Pacific

- 5.1. Market Analysis, Insights and Forecast - by Application

- 6. North America Bio-based Polycarbonate Film Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Application

- 6.1.1. Automobiles

- 6.1.2. Electronics

- 6.1.3. Other

- 6.2. Market Analysis, Insights and Forecast - by Types

- 6.2.1. Plant-based

- 6.2.2. Other Source

- 6.1. Market Analysis, Insights and Forecast - by Application

- 7. South America Bio-based Polycarbonate Film Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Application

- 7.1.1. Automobiles

- 7.1.2. Electronics

- 7.1.3. Other

- 7.2. Market Analysis, Insights and Forecast - by Types

- 7.2.1. Plant-based

- 7.2.2. Other Source

- 7.1. Market Analysis, Insights and Forecast - by Application

- 8. Europe Bio-based Polycarbonate Film Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Application

- 8.1.1. Automobiles

- 8.1.2. Electronics

- 8.1.3. Other

- 8.2. Market Analysis, Insights and Forecast - by Types

- 8.2.1. Plant-based

- 8.2.2. Other Source

- 8.1. Market Analysis, Insights and Forecast - by Application

- 9. Middle East & Africa Bio-based Polycarbonate Film Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Application

- 9.1.1. Automobiles

- 9.1.2. Electronics

- 9.1.3. Other

- 9.2. Market Analysis, Insights and Forecast - by Types

- 9.2.1. Plant-based

- 9.2.2. Other Source

- 9.1. Market Analysis, Insights and Forecast - by Application

- 10. Asia Pacific Bio-based Polycarbonate Film Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Application

- 10.1.1. Automobiles

- 10.1.2. Electronics

- 10.1.3. Other

- 10.2. Market Analysis, Insights and Forecast - by Types

- 10.2.1. Plant-based

- 10.2.2. Other Source

- 10.1. Market Analysis, Insights and Forecast - by Application

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Covestro

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 SABIC

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Mitsubishi Chemical

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.1 Covestro

List of Figures

- Figure 1: Global Bio-based Polycarbonate Film Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Bio-based Polycarbonate Film Revenue (undefined), by Application 2025 & 2033

- Figure 3: North America Bio-based Polycarbonate Film Revenue Share (%), by Application 2025 & 2033

- Figure 4: North America Bio-based Polycarbonate Film Revenue (undefined), by Types 2025 & 2033

- Figure 5: North America Bio-based Polycarbonate Film Revenue Share (%), by Types 2025 & 2033

- Figure 6: North America Bio-based Polycarbonate Film Revenue (undefined), by Country 2025 & 2033

- Figure 7: North America Bio-based Polycarbonate Film Revenue Share (%), by Country 2025 & 2033

- Figure 8: South America Bio-based Polycarbonate Film Revenue (undefined), by Application 2025 & 2033

- Figure 9: South America Bio-based Polycarbonate Film Revenue Share (%), by Application 2025 & 2033

- Figure 10: South America Bio-based Polycarbonate Film Revenue (undefined), by Types 2025 & 2033

- Figure 11: South America Bio-based Polycarbonate Film Revenue Share (%), by Types 2025 & 2033

- Figure 12: South America Bio-based Polycarbonate Film Revenue (undefined), by Country 2025 & 2033

- Figure 13: South America Bio-based Polycarbonate Film Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Bio-based Polycarbonate Film Revenue (undefined), by Application 2025 & 2033

- Figure 15: Europe Bio-based Polycarbonate Film Revenue Share (%), by Application 2025 & 2033

- Figure 16: Europe Bio-based Polycarbonate Film Revenue (undefined), by Types 2025 & 2033

- Figure 17: Europe Bio-based Polycarbonate Film Revenue Share (%), by Types 2025 & 2033

- Figure 18: Europe Bio-based Polycarbonate Film Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Bio-based Polycarbonate Film Revenue Share (%), by Country 2025 & 2033

- Figure 20: Middle East & Africa Bio-based Polycarbonate Film Revenue (undefined), by Application 2025 & 2033

- Figure 21: Middle East & Africa Bio-based Polycarbonate Film Revenue Share (%), by Application 2025 & 2033

- Figure 22: Middle East & Africa Bio-based Polycarbonate Film Revenue (undefined), by Types 2025 & 2033

- Figure 23: Middle East & Africa Bio-based Polycarbonate Film Revenue Share (%), by Types 2025 & 2033

- Figure 24: Middle East & Africa Bio-based Polycarbonate Film Revenue (undefined), by Country 2025 & 2033

- Figure 25: Middle East & Africa Bio-based Polycarbonate Film Revenue Share (%), by Country 2025 & 2033

- Figure 26: Asia Pacific Bio-based Polycarbonate Film Revenue (undefined), by Application 2025 & 2033

- Figure 27: Asia Pacific Bio-based Polycarbonate Film Revenue Share (%), by Application 2025 & 2033

- Figure 28: Asia Pacific Bio-based Polycarbonate Film Revenue (undefined), by Types 2025 & 2033

- Figure 29: Asia Pacific Bio-based Polycarbonate Film Revenue Share (%), by Types 2025 & 2033

- Figure 30: Asia Pacific Bio-based Polycarbonate Film Revenue (undefined), by Country 2025 & 2033

- Figure 31: Asia Pacific Bio-based Polycarbonate Film Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Bio-based Polycarbonate Film Revenue undefined Forecast, by Application 2020 & 2033

- Table 2: Global Bio-based Polycarbonate Film Revenue undefined Forecast, by Types 2020 & 2033

- Table 3: Global Bio-based Polycarbonate Film Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Bio-based Polycarbonate Film Revenue undefined Forecast, by Application 2020 & 2033

- Table 5: Global Bio-based Polycarbonate Film Revenue undefined Forecast, by Types 2020 & 2033

- Table 6: Global Bio-based Polycarbonate Film Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: United States Bio-based Polycarbonate Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Canada Bio-based Polycarbonate Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Mexico Bio-based Polycarbonate Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: Global Bio-based Polycarbonate Film Revenue undefined Forecast, by Application 2020 & 2033

- Table 11: Global Bio-based Polycarbonate Film Revenue undefined Forecast, by Types 2020 & 2033

- Table 12: Global Bio-based Polycarbonate Film Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Brazil Bio-based Polycarbonate Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 14: Argentina Bio-based Polycarbonate Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 15: Rest of South America Bio-based Polycarbonate Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Global Bio-based Polycarbonate Film Revenue undefined Forecast, by Application 2020 & 2033

- Table 17: Global Bio-based Polycarbonate Film Revenue undefined Forecast, by Types 2020 & 2033

- Table 18: Global Bio-based Polycarbonate Film Revenue undefined Forecast, by Country 2020 & 2033

- Table 19: United Kingdom Bio-based Polycarbonate Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 20: Germany Bio-based Polycarbonate Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 21: France Bio-based Polycarbonate Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: Italy Bio-based Polycarbonate Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: Spain Bio-based Polycarbonate Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Russia Bio-based Polycarbonate Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Benelux Bio-based Polycarbonate Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Nordics Bio-based Polycarbonate Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Bio-based Polycarbonate Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Bio-based Polycarbonate Film Revenue undefined Forecast, by Application 2020 & 2033

- Table 29: Global Bio-based Polycarbonate Film Revenue undefined Forecast, by Types 2020 & 2033

- Table 30: Global Bio-based Polycarbonate Film Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: Turkey Bio-based Polycarbonate Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Israel Bio-based Polycarbonate Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 33: GCC Bio-based Polycarbonate Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 34: North Africa Bio-based Polycarbonate Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 35: South Africa Bio-based Polycarbonate Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 36: Rest of Middle East & Africa Bio-based Polycarbonate Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 37: Global Bio-based Polycarbonate Film Revenue undefined Forecast, by Application 2020 & 2033

- Table 38: Global Bio-based Polycarbonate Film Revenue undefined Forecast, by Types 2020 & 2033

- Table 39: Global Bio-based Polycarbonate Film Revenue undefined Forecast, by Country 2020 & 2033

- Table 40: China Bio-based Polycarbonate Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 41: India Bio-based Polycarbonate Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 42: Japan Bio-based Polycarbonate Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 43: South Korea Bio-based Polycarbonate Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 44: ASEAN Bio-based Polycarbonate Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 45: Oceania Bio-based Polycarbonate Film Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 46: Rest of Asia Pacific Bio-based Polycarbonate Film Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Bio-based Polycarbonate Film?

The projected CAGR is approximately 9.11%.

2. Which companies are prominent players in the Bio-based Polycarbonate Film?

Key companies in the market include Covestro, SABIC, Mitsubishi Chemical.

3. What are the main segments of the Bio-based Polycarbonate Film?

The market segments include Application, Types.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

N/A

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4900.00, USD 7350.00, and USD 9800.00 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Bio-based Polycarbonate Film," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Bio-based Polycarbonate Film report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Bio-based Polycarbonate Film?

To stay informed about further developments, trends, and reports in the Bio-based Polycarbonate Film, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence