Key Insights

The 3D radar market is experiencing robust growth, projected to reach a substantial size driven by increasing demand for advanced surveillance and air traffic management systems. The market's Compound Annual Growth Rate (CAGR) of 18.69% from 2019 to 2024 indicates a significant upward trajectory. This growth is fueled by several key factors. Firstly, the rising adoption of 3D radar technology in defense applications, including early warning systems and missile defense, is a major driver. Secondly, the increasing need for improved air traffic control in a world with burgeoning air travel is pushing demand. Thirdly, technological advancements leading to smaller, more efficient, and cost-effective 3D radar systems are further stimulating market expansion. Segmentation by platform (airborne, ground, naval) and range type (long, medium, short) reveals diverse application opportunities, with airborne systems likely dominating due to their crucial role in both military and civilian aviation. Competitive dynamics are shaped by the presence of major players like Saab, Honeywell, and Raytheon, engaged in continuous innovation and strategic partnerships to capture market share. Geographical distribution indicates strong growth across North America, Europe, and the Asia-Pacific region, reflecting the concentration of both military expenditure and advanced technological infrastructure in these areas. However, restraints such as high initial investment costs and the complexities of integrating new systems into existing infrastructure might pose challenges to market expansion. Despite these challenges, the long-term outlook for the 3D radar market remains positive, indicating substantial growth potential over the coming decade.

While precise market sizing data is absent, considering the provided CAGR of 18.69% from 2019 to 2024 and a base year of 2025, we can infer significant market expansion. Estimating a conservative market value for 2025, considering the stated value unit of "millions," let's assume a starting point of $2 billion USD for 2019 and apply the CAGR to extrapolate to future years. This estimation does not incorporate any unforeseen market fluctuations. Regional variations in market size would reflect the varying defense budgets, technological advancements, and air traffic density of different geographical areas. For example, North America and Europe are expected to maintain substantial market share due to their advanced technological landscapes and large defense spending. Asia-Pacific, fueled by economic growth and rising investments in infrastructure, is projected to experience a robust growth trajectory. While detailed regional market shares require more precise data, a reasonable assumption is that these three regions will collectively dominate the market, with North America and Europe holding a larger share than Asia-Pacific initially.

3D Radar Industry Market Report: 2019-2033 Forecast

Dive deep into the burgeoning 3D Radar market with our comprehensive report, providing invaluable insights for strategic decision-making. This in-depth analysis covers market dynamics, leading players, technological advancements, and future growth projections from 2019 to 2033. The report leverages extensive data analysis and expert insights to paint a clear picture of the industry's trajectory. With a base year of 2025 and an estimated year of 2025, this report offers a robust forecast period from 2025 to 2033, building upon the historical period of 2019-2024. The global 3D radar market is projected to reach xx Million by 2033, presenting significant opportunities for stakeholders.

3D Radar Industry Market Dynamics & Concentration

The 3D radar market exhibits a moderately consolidated structure, with key players such as SAAB Group, Honeywell International Inc, Rheinmetall AG, and Thales Group commanding significant market share. The market's concentration is influenced by high barriers to entry, including substantial R&D investments and stringent regulatory approvals. Innovation, particularly in areas like advanced signal processing and AI integration, drives market growth. Mergers and acquisitions (M&A) activity has been relatively moderate (xx deals in the past five years), primarily focusing on strategic technology acquisitions and expansion into new geographical markets. The regulatory landscape varies significantly across regions, impacting market access and product development. Product substitutes, such as advanced optical sensors, pose a limited threat currently, but their advancements could influence future market dynamics. End-user preferences are shifting towards higher resolution and longer-range systems, particularly in the defense and security sectors.

- Market Share (2024 Estimate): SAAB Group (xx%), Honeywell International Inc (xx%), Rheinmetall AG (xx%), Thales Group (xx%), Others (xx%).

- M&A Deal Count (2019-2024): xx

- Key Innovation Drivers: AI integration, advanced signal processing, miniaturization.

- Regulatory Impact: Stringent certifications and compliance requirements vary regionally.

3D Radar Industry Industry Trends & Analysis

The 3D radar market is experiencing robust growth, driven by increasing demand from defense and security sectors, the expanding adoption in civilian applications (air traffic control, autonomous vehicles), and technological advancements. The compound annual growth rate (CAGR) from 2025 to 2033 is estimated at xx%, fueled by factors such as rising geopolitical instability, investments in modernization of military infrastructure, and the increasing need for enhanced situational awareness. Technological disruptions, such as the development of solid-state radar technologies and improved software-defined radios, are significantly influencing market dynamics. Increased consumer preference for higher accuracy, improved reliability, and cost-effective solutions is shaping product development strategies. Competitive dynamics are characterized by intense competition among established players, with an ongoing focus on product differentiation and technological innovation. Market penetration of 3D radar systems is steadily increasing across various sectors, with substantial growth projected in airborne and ground-based applications.

Leading Markets & Segments in 3D Radar Industry

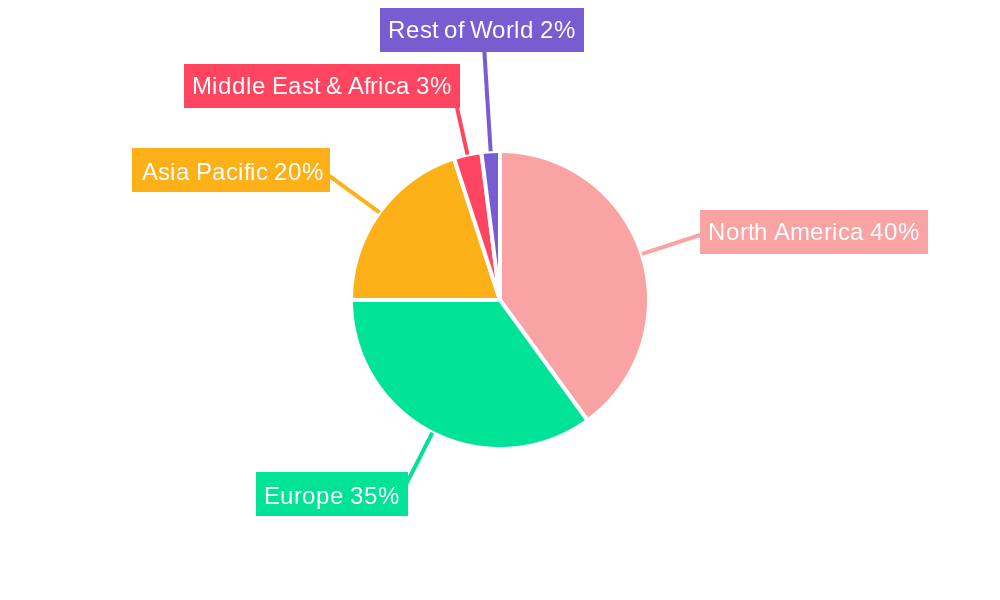

The North American region currently dominates the 3D radar market, driven by strong defense budgets, technological advancements, and a well-established ecosystem of radar manufacturers. Within the platform segment, airborne systems currently hold the largest market share, followed by ground and naval systems. The long-range segment is experiencing the fastest growth due to increasing demand for enhanced surveillance capabilities.

- Dominant Region: North America

- Largest Segment (Platform): Airborne

- Fastest Growing Segment (Range Type): Long Range

Key Drivers for North American Dominance:

- High Defense Spending: Significant investments in military modernization.

- Technological Leadership: Strong presence of key players and advanced R&D capabilities.

- Robust Infrastructure: Well-established supply chains and supportive regulatory frameworks.

Airborne Segment Dominance Analysis: This segment's growth is driven by increasing demand for advanced air traffic management systems and enhanced situational awareness capabilities for military aircraft. The ongoing modernization of military aircraft fleets globally also fuels this segment's expansion.

3D Radar Industry Product Developments

Recent product developments focus on miniaturization, improved resolution, increased range, and better integration with other sensor systems. Solid-state technology is gradually replacing traditional vacuum tube-based radars, offering advantages in terms of size, weight, power consumption, and reliability. These advancements are improving radar performance and creating new applications across various sectors, including autonomous driving and advanced driver-assistance systems (ADAS). The market's competitive landscape is shaped by continuous innovation and the pursuit of cost-effective solutions while maintaining high performance standards.

Key Drivers of 3D Radar Industry Growth

Technological advancements such as the development of solid-state radar and AI integration are leading drivers of market growth. Increased defense spending globally, particularly in regions experiencing geopolitical instability, is another key factor. Stringent regulatory requirements for air safety and security are also pushing adoption of advanced radar systems.

Challenges in the 3D Radar Industry Market

The 3D radar market faces challenges including high initial investment costs, complex supply chains vulnerable to disruptions, and intense competition from established players. Stringent regulatory approvals and certification processes can also delay product launches and market entry. The cost of integrating advanced software and processing units can impact profitability and accessibility.

Emerging Opportunities in 3D Radar Industry

Emerging opportunities include the integration of 3D radar into autonomous vehicles, the expansion into new applications such as environmental monitoring and weather forecasting, and the development of cost-effective solutions for wider market adoption. Strategic partnerships between radar manufacturers and software providers are likely to drive innovation and create new market opportunities. The development of compact and lightweight radar systems suitable for UAVs presents a significant growth avenue.

Leading Players in the 3D Radar Industry Sector

- SAAB Group

- Honeywell International Inc

- Rheinmetall AG

- Aselsan AS

- Airbus Defense and Space

- Raytheon Company

- Leonardo SpA

- Thales Group

- Elta Systems Ltd (Israel Aerospace Industries)

- BAE Systems PLC

- Northrop Grumman Corporation

Key Milestones in 3D Radar Industry Industry

- 2020: Introduction of the first commercially available solid-state 3D radar for automotive applications by xx company.

- 2021: Successful integration of AI algorithms for improved target recognition in military 3D radar systems by xx company.

- 2022: Merger of two leading radar manufacturers expands market share and product portfolio, significantly impacting competitive dynamics.

- 2023: Launch of a new generation of long-range 3D radar systems for air surveillance by xx company.

- 2024: xx

Strategic Outlook for 3D Radar Industry Market

The 3D radar market is poised for significant growth over the next decade, driven by technological innovation, increasing defense spending, and expanding applications across diverse sectors. Strategic partnerships, investments in R&D, and the development of cost-effective solutions will be crucial for success. The market's future depends on addressing challenges related to supply chain vulnerabilities and regulatory complexities.

3D Radar Industry Segmentation

-

1. Platform

- 1.1. Airborne

- 1.2. Ground

- 1.3. Naval

-

2. Range Type

- 2.1. Long Range

- 2.2. Medium and Short Range

3D Radar Industry Segmentation By Geography

-

1. North America

- 1.1. United States

- 1.2. Canada

-

2. Europe

- 2.1. United Kingdom

- 2.2. Germany

- 2.3. France

- 2.4. Rest of Europe

-

3. Asia Pacific

- 3.1. China

- 3.2. Japan

- 3.3. India

- 3.4. Rest of Asia Pacific

-

4. Middle East and Africa

- 4.1. United Arab Emirates

- 4.2. Saudi Arabia

- 5. Rest of the World

3D Radar Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 18.69% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. ; Rising Use of 3D Radar in Unmanned Aerial Vehicles

- 3.3. Market Restrains

- 3.3.1. ; High Initial Deployment Cost

- 3.4. Market Trends

- 3.4.1. Airborne 3D Radar is Expected to Witness Highest growth

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global 3D Radar Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Platform

- 5.1.1. Airborne

- 5.1.2. Ground

- 5.1.3. Naval

- 5.2. Market Analysis, Insights and Forecast - by Range Type

- 5.2.1. Long Range

- 5.2.2. Medium and Short Range

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Middle East and Africa

- 5.3.5. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Platform

- 6. North America 3D Radar Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Platform

- 6.1.1. Airborne

- 6.1.2. Ground

- 6.1.3. Naval

- 6.2. Market Analysis, Insights and Forecast - by Range Type

- 6.2.1. Long Range

- 6.2.2. Medium and Short Range

- 6.1. Market Analysis, Insights and Forecast - by Platform

- 7. Europe 3D Radar Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Platform

- 7.1.1. Airborne

- 7.1.2. Ground

- 7.1.3. Naval

- 7.2. Market Analysis, Insights and Forecast - by Range Type

- 7.2.1. Long Range

- 7.2.2. Medium and Short Range

- 7.1. Market Analysis, Insights and Forecast - by Platform

- 8. Asia Pacific 3D Radar Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Platform

- 8.1.1. Airborne

- 8.1.2. Ground

- 8.1.3. Naval

- 8.2. Market Analysis, Insights and Forecast - by Range Type

- 8.2.1. Long Range

- 8.2.2. Medium and Short Range

- 8.1. Market Analysis, Insights and Forecast - by Platform

- 9. Middle East and Africa 3D Radar Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Platform

- 9.1.1. Airborne

- 9.1.2. Ground

- 9.1.3. Naval

- 9.2. Market Analysis, Insights and Forecast - by Range Type

- 9.2.1. Long Range

- 9.2.2. Medium and Short Range

- 9.1. Market Analysis, Insights and Forecast - by Platform

- 10. Rest of the World 3D Radar Industry Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Platform

- 10.1.1. Airborne

- 10.1.2. Ground

- 10.1.3. Naval

- 10.2. Market Analysis, Insights and Forecast - by Range Type

- 10.2.1. Long Range

- 10.2.2. Medium and Short Range

- 10.1. Market Analysis, Insights and Forecast - by Platform

- 11. North America 3D Radar Industry Analysis, Insights and Forecast, 2019-2031

- 11.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 11.1.1 United States

- 11.1.2 Canada

- 12. Europe 3D Radar Industry Analysis, Insights and Forecast, 2019-2031

- 12.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 12.1.1 United Kingdom

- 12.1.2 Germany

- 12.1.3 France

- 12.1.4 Rest of Europe

- 13. Asia Pacific 3D Radar Industry Analysis, Insights and Forecast, 2019-2031

- 13.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 13.1.1 China

- 13.1.2 Japan

- 13.1.3 India

- 13.1.4 Rest of Asia Pacific

- 14. Middle East and Africa 3D Radar Industry Analysis, Insights and Forecast, 2019-2031

- 14.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 14.1.1 United Arab Emirates

- 14.1.2 Saudi Arabia

- 15. Rest of the World 3D Radar Industry Analysis, Insights and Forecast, 2019-2031

- 15.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 15.1.1.

- 16. Competitive Analysis

- 16.1. Global Market Share Analysis 2024

- 16.2. Company Profiles

- 16.2.1 SAAB Group

- 16.2.1.1. Overview

- 16.2.1.2. Products

- 16.2.1.3. SWOT Analysis

- 16.2.1.4. Recent Developments

- 16.2.1.5. Financials (Based on Availability)

- 16.2.2 Honeywell International Inc

- 16.2.2.1. Overview

- 16.2.2.2. Products

- 16.2.2.3. SWOT Analysis

- 16.2.2.4. Recent Developments

- 16.2.2.5. Financials (Based on Availability)

- 16.2.3 Rheinmetall AG

- 16.2.3.1. Overview

- 16.2.3.2. Products

- 16.2.3.3. SWOT Analysis

- 16.2.3.4. Recent Developments

- 16.2.3.5. Financials (Based on Availability)

- 16.2.4 Aselsan AS

- 16.2.4.1. Overview

- 16.2.4.2. Products

- 16.2.4.3. SWOT Analysis

- 16.2.4.4. Recent Developments

- 16.2.4.5. Financials (Based on Availability)

- 16.2.5 Airbus Defense and Space

- 16.2.5.1. Overview

- 16.2.5.2. Products

- 16.2.5.3. SWOT Analysis

- 16.2.5.4. Recent Developments

- 16.2.5.5. Financials (Based on Availability)

- 16.2.6 Raytheon Company

- 16.2.6.1. Overview

- 16.2.6.2. Products

- 16.2.6.3. SWOT Analysis

- 16.2.6.4. Recent Developments

- 16.2.6.5. Financials (Based on Availability)

- 16.2.7 Leonardo SpA*List Not Exhaustive

- 16.2.7.1. Overview

- 16.2.7.2. Products

- 16.2.7.3. SWOT Analysis

- 16.2.7.4. Recent Developments

- 16.2.7.5. Financials (Based on Availability)

- 16.2.8 Thales Group

- 16.2.8.1. Overview

- 16.2.8.2. Products

- 16.2.8.3. SWOT Analysis

- 16.2.8.4. Recent Developments

- 16.2.8.5. Financials (Based on Availability)

- 16.2.9 Elta Systems Ltd (Israel Aerospace Industries)

- 16.2.9.1. Overview

- 16.2.9.2. Products

- 16.2.9.3. SWOT Analysis

- 16.2.9.4. Recent Developments

- 16.2.9.5. Financials (Based on Availability)

- 16.2.10 BAE Systems PLC

- 16.2.10.1. Overview

- 16.2.10.2. Products

- 16.2.10.3. SWOT Analysis

- 16.2.10.4. Recent Developments

- 16.2.10.5. Financials (Based on Availability)

- 16.2.11 Northrop Grumman Corporation

- 16.2.11.1. Overview

- 16.2.11.2. Products

- 16.2.11.3. SWOT Analysis

- 16.2.11.4. Recent Developments

- 16.2.11.5. Financials (Based on Availability)

- 16.2.1 SAAB Group

List of Figures

- Figure 1: Global 3D Radar Industry Revenue Breakdown (Million, %) by Region 2024 & 2032

- Figure 2: North America 3D Radar Industry Revenue (Million), by Country 2024 & 2032

- Figure 3: North America 3D Radar Industry Revenue Share (%), by Country 2024 & 2032

- Figure 4: Europe 3D Radar Industry Revenue (Million), by Country 2024 & 2032

- Figure 5: Europe 3D Radar Industry Revenue Share (%), by Country 2024 & 2032

- Figure 6: Asia Pacific 3D Radar Industry Revenue (Million), by Country 2024 & 2032

- Figure 7: Asia Pacific 3D Radar Industry Revenue Share (%), by Country 2024 & 2032

- Figure 8: Middle East and Africa 3D Radar Industry Revenue (Million), by Country 2024 & 2032

- Figure 9: Middle East and Africa 3D Radar Industry Revenue Share (%), by Country 2024 & 2032

- Figure 10: Rest of the World 3D Radar Industry Revenue (Million), by Country 2024 & 2032

- Figure 11: Rest of the World 3D Radar Industry Revenue Share (%), by Country 2024 & 2032

- Figure 12: North America 3D Radar Industry Revenue (Million), by Platform 2024 & 2032

- Figure 13: North America 3D Radar Industry Revenue Share (%), by Platform 2024 & 2032

- Figure 14: North America 3D Radar Industry Revenue (Million), by Range Type 2024 & 2032

- Figure 15: North America 3D Radar Industry Revenue Share (%), by Range Type 2024 & 2032

- Figure 16: North America 3D Radar Industry Revenue (Million), by Country 2024 & 2032

- Figure 17: North America 3D Radar Industry Revenue Share (%), by Country 2024 & 2032

- Figure 18: Europe 3D Radar Industry Revenue (Million), by Platform 2024 & 2032

- Figure 19: Europe 3D Radar Industry Revenue Share (%), by Platform 2024 & 2032

- Figure 20: Europe 3D Radar Industry Revenue (Million), by Range Type 2024 & 2032

- Figure 21: Europe 3D Radar Industry Revenue Share (%), by Range Type 2024 & 2032

- Figure 22: Europe 3D Radar Industry Revenue (Million), by Country 2024 & 2032

- Figure 23: Europe 3D Radar Industry Revenue Share (%), by Country 2024 & 2032

- Figure 24: Asia Pacific 3D Radar Industry Revenue (Million), by Platform 2024 & 2032

- Figure 25: Asia Pacific 3D Radar Industry Revenue Share (%), by Platform 2024 & 2032

- Figure 26: Asia Pacific 3D Radar Industry Revenue (Million), by Range Type 2024 & 2032

- Figure 27: Asia Pacific 3D Radar Industry Revenue Share (%), by Range Type 2024 & 2032

- Figure 28: Asia Pacific 3D Radar Industry Revenue (Million), by Country 2024 & 2032

- Figure 29: Asia Pacific 3D Radar Industry Revenue Share (%), by Country 2024 & 2032

- Figure 30: Middle East and Africa 3D Radar Industry Revenue (Million), by Platform 2024 & 2032

- Figure 31: Middle East and Africa 3D Radar Industry Revenue Share (%), by Platform 2024 & 2032

- Figure 32: Middle East and Africa 3D Radar Industry Revenue (Million), by Range Type 2024 & 2032

- Figure 33: Middle East and Africa 3D Radar Industry Revenue Share (%), by Range Type 2024 & 2032

- Figure 34: Middle East and Africa 3D Radar Industry Revenue (Million), by Country 2024 & 2032

- Figure 35: Middle East and Africa 3D Radar Industry Revenue Share (%), by Country 2024 & 2032

- Figure 36: Rest of the World 3D Radar Industry Revenue (Million), by Platform 2024 & 2032

- Figure 37: Rest of the World 3D Radar Industry Revenue Share (%), by Platform 2024 & 2032

- Figure 38: Rest of the World 3D Radar Industry Revenue (Million), by Range Type 2024 & 2032

- Figure 39: Rest of the World 3D Radar Industry Revenue Share (%), by Range Type 2024 & 2032

- Figure 40: Rest of the World 3D Radar Industry Revenue (Million), by Country 2024 & 2032

- Figure 41: Rest of the World 3D Radar Industry Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global 3D Radar Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Global 3D Radar Industry Revenue Million Forecast, by Platform 2019 & 2032

- Table 3: Global 3D Radar Industry Revenue Million Forecast, by Range Type 2019 & 2032

- Table 4: Global 3D Radar Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: Global 3D Radar Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: United States 3D Radar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: Canada 3D Radar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: Global 3D Radar Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 9: United Kingdom 3D Radar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Germany 3D Radar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: France 3D Radar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Rest of Europe 3D Radar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Global 3D Radar Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 14: China 3D Radar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 15: Japan 3D Radar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: India 3D Radar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 17: Rest of Asia Pacific 3D Radar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: Global 3D Radar Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 19: United Arab Emirates 3D Radar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Saudi Arabia 3D Radar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 21: Global 3D Radar Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 22: 3D Radar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: Global 3D Radar Industry Revenue Million Forecast, by Platform 2019 & 2032

- Table 24: Global 3D Radar Industry Revenue Million Forecast, by Range Type 2019 & 2032

- Table 25: Global 3D Radar Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 26: United States 3D Radar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 27: Canada 3D Radar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 28: Global 3D Radar Industry Revenue Million Forecast, by Platform 2019 & 2032

- Table 29: Global 3D Radar Industry Revenue Million Forecast, by Range Type 2019 & 2032

- Table 30: Global 3D Radar Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 31: United Kingdom 3D Radar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 32: Germany 3D Radar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 33: France 3D Radar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 34: Rest of Europe 3D Radar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 35: Global 3D Radar Industry Revenue Million Forecast, by Platform 2019 & 2032

- Table 36: Global 3D Radar Industry Revenue Million Forecast, by Range Type 2019 & 2032

- Table 37: Global 3D Radar Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 38: China 3D Radar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 39: Japan 3D Radar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 40: India 3D Radar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 41: Rest of Asia Pacific 3D Radar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 42: Global 3D Radar Industry Revenue Million Forecast, by Platform 2019 & 2032

- Table 43: Global 3D Radar Industry Revenue Million Forecast, by Range Type 2019 & 2032

- Table 44: Global 3D Radar Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 45: United Arab Emirates 3D Radar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 46: Saudi Arabia 3D Radar Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 47: Global 3D Radar Industry Revenue Million Forecast, by Platform 2019 & 2032

- Table 48: Global 3D Radar Industry Revenue Million Forecast, by Range Type 2019 & 2032

- Table 49: Global 3D Radar Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the 3D Radar Industry?

The projected CAGR is approximately 18.69%.

2. Which companies are prominent players in the 3D Radar Industry?

Key companies in the market include SAAB Group, Honeywell International Inc, Rheinmetall AG, Aselsan AS, Airbus Defense and Space, Raytheon Company, Leonardo SpA*List Not Exhaustive, Thales Group, Elta Systems Ltd (Israel Aerospace Industries), BAE Systems PLC, Northrop Grumman Corporation.

3. What are the main segments of the 3D Radar Industry?

The market segments include Platform, Range Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

; Rising Use of 3D Radar in Unmanned Aerial Vehicles.

6. What are the notable trends driving market growth?

Airborne 3D Radar is Expected to Witness Highest growth.

7. Are there any restraints impacting market growth?

; High Initial Deployment Cost.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "3D Radar Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the 3D Radar Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the 3D Radar Industry?

To stay informed about further developments, trends, and reports in the 3D Radar Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence