Key Insights

The Malaysian payment industry is experiencing robust growth, projected to reach a substantial market size driven by increasing digitalization and a burgeoning e-commerce sector. The 11.40% CAGR from 2019-2033 signifies a significant upward trajectory, fueled by factors such as rising smartphone penetration, expanding internet access, and government initiatives promoting cashless transactions. Key drivers include the adoption of mobile payment solutions like Grab Pay and Huawei Pay, coupled with the increasing acceptance of online payment methods by businesses across various sectors, including retail, entertainment, and healthcare. The shift towards cashless transactions is further facilitated by the expanding infrastructure of POS systems and the proliferation of digital wallets offered by major financial institutions like Maybank and CIMB Group. While challenges like cybersecurity concerns and financial literacy gaps exist, the overall market outlook remains optimistic.

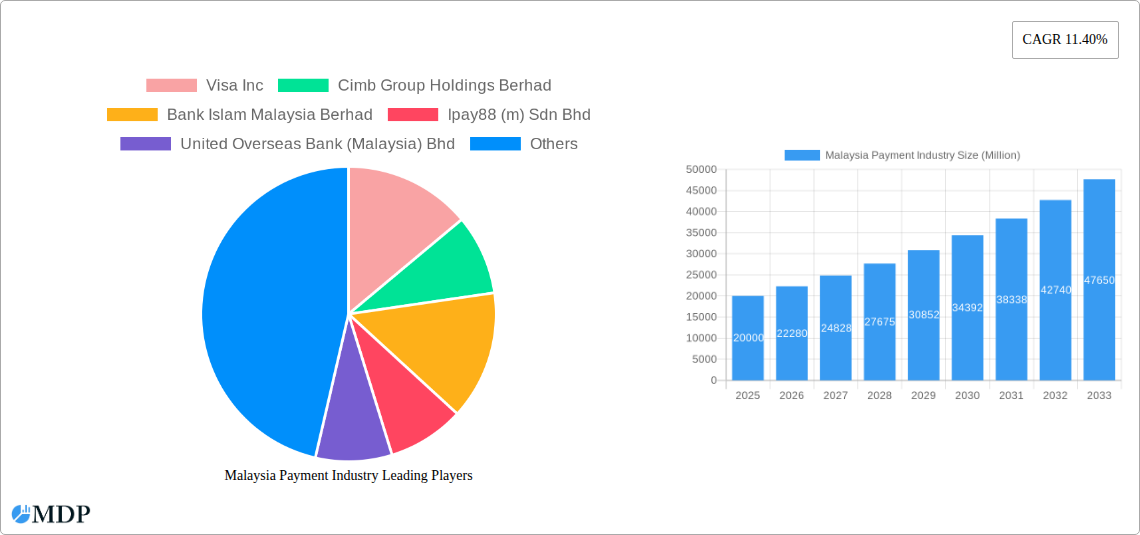

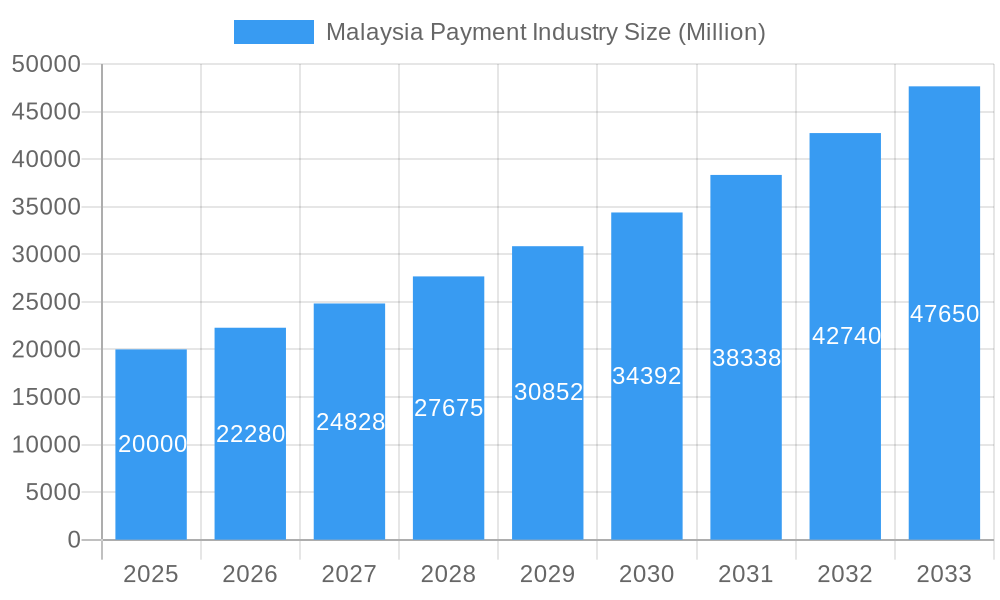

Malaysia Payment Industry Market Size (In Billion)

The industry is segmented by end-user industry and mode of payment, offering diverse growth opportunities. The retail and e-commerce sectors are major contributors, with the adoption of online payment gateways such as iPay88 experiencing significant traction. The healthcare sector is also exhibiting increasing integration of digital payment systems for enhanced convenience and efficiency. Competition among major players like Visa, PayPal, and various local banks ensures innovation and continuous improvement in payment technology and services. Furthermore, the increasing preference for contactless payments post-pandemic is further accelerating the growth of the Malaysian payment industry. The forecast period from 2025-2033 is expected to witness the consolidation of market players and the emergence of new technologies, such as biometric payments and blockchain solutions, further shaping the landscape.

Malaysia Payment Industry Company Market Share

Malaysia Payment Industry Report: 2019-2033

Dive into the dynamic Malaysian payment landscape with this comprehensive report, offering in-depth analysis and future projections for the period 2019-2033. This report provides crucial insights for stakeholders, investors, and businesses operating within or looking to enter this rapidly evolving market. We analyze market size, key players, technological advancements, and regulatory changes to give you a complete understanding of the Malaysian payment industry. The report projects a market value exceeding xx Million by 2033.

Malaysia Payment Industry Market Dynamics & Concentration

The Malaysian payment industry, valued at xx Million in 2024, exhibits a dynamic interplay of concentration, innovation, and regulatory influence. Market share is largely concentrated amongst established players like Maybank, CIMB Group, and several international giants. However, the rise of fintechs like GrabPay and iPay88 is steadily disrupting the traditional banking dominance.

- Market Concentration: Maybank and CIMB Group currently hold a significant market share, with estimates placing them collectively at approximately xx%. Other key players, including Visa and PayPal, hold substantial shares, while a growing number of smaller players compete aggressively.

- Innovation Drivers: The industry is driven by mobile technology adoption, increasing digital financial literacy, and government initiatives pushing for a cashless society. Contactless payments, QR codes, and e-wallets are key innovation drivers.

- Regulatory Frameworks: Bank Negara Malaysia's regulatory framework influences the sector significantly, impacting the licensing of payment providers, data security standards, and consumer protection measures. Recent regulations have fostered both innovation and compliance.

- Product Substitutes: The competitive landscape includes both traditional banking and non-banking payment methods. The constant emergence of new fintech solutions introduces alternative payment options, increasing competitive pressures.

- End-User Trends: Consumers are increasingly adopting digital payment solutions due to their convenience, speed, and security features. Demand for mobile wallets and online payment platforms is substantially growing.

- M&A Activities: The number of M&A deals within the Malaysian payment sector has averaged approximately xx annually in the recent past, driven by the desire of larger players to expand their market share and acquire innovative technology.

Malaysia Payment Industry Industry Trends & Analysis

The Malaysian payment industry is experiencing robust growth, driven primarily by increasing smartphone penetration, a burgeoning e-commerce sector, and government policies promoting financial inclusion. The Compound Annual Growth Rate (CAGR) for the period 2025-2033 is projected to be xx%, exceeding the global average. Several key trends are shaping the industry's trajectory.

The market penetration of digital payment methods continues its rapid rise, with the percentage of online transactions growing substantially each year. Consumer preference for contactless and mobile payment solutions is a major growth driver. Increasing competition between traditional banks, fintech companies, and international payment providers creates a dynamic market environment. Technological disruptions, such as the rise of blockchain technology and open banking, are fundamentally altering payment infrastructure.

Leading Markets & Segments in Malaysia Payment Industry

By End-user Industry:

- Retail: Remains the dominant segment, fueled by the increasing preference for cashless transactions in everyday shopping. Strong economic growth and infrastructure development in major cities contribute to retail segment dominance.

- E-commerce/Online Sales: Rapid growth driven by the burgeoning e-commerce sector and increasing online shopping habits amongst Malaysians.

- Other Segments: Hospitality and entertainment sectors show considerable growth, with healthcare gradually adapting to digital payment solutions.

By Mode of Payment:

- Point of Sale (POS): Dominated by credit/debit cards and e-wallets, with a noticeable shift towards contactless payment technologies.

- Online Sales: This segment is experiencing explosive growth, driven by the rise of e-commerce platforms and digital marketplaces.

Malaysia Payment Industry Product Developments

The Malaysian payment industry witnesses continuous innovation in payment solutions. The integration of biometrics, AI-powered fraud detection, and blockchain technology enhances security and efficiency. New products like cross-border QR payment systems are enhancing the user experience, whilst the introduction of innovative e-wallet features, such as bill payments and peer-to-peer (P2P) transfers, drives adoption. The market is characterized by a constant introduction of new payment platforms, tailored to meet specific market needs.

Key Drivers of Malaysia Payment Industry Growth

Several factors fuel the growth of the Malaysian payment industry. The government’s push for financial inclusion and a cashless economy is a significant driver, complemented by supportive infrastructure development, like improved internet penetration and mobile network coverage. Technological advancements, such as the adoption of mobile wallets and contactless payments, are streamlining transactions, and increased consumer awareness and trust in digital financial services are key contributors.

Challenges in the Malaysia Payment Industry Market

Despite considerable growth, the Malaysian payment industry faces certain challenges. Cybersecurity threats, data breaches, and fraud remain significant concerns. Maintaining robust data security and implementing stringent fraud prevention measures are crucial to consumer confidence. Furthermore, some consumers and businesses may still prefer traditional cash payments, hindering the complete adoption of cashless systems. Competition in the market, especially from new market entrants, puts pressure on profit margins.

Emerging Opportunities in Malaysia Payment Industry

The Malaysian payment industry presents numerous long-term growth opportunities. The expansion of mobile payment solutions into underserved rural areas, creating better financial inclusion, offers substantial potential. The integration of innovative technologies like artificial intelligence (AI) and big data analytics will significantly enhance personalized financial services. Strategic partnerships between traditional financial institutions and fintech companies could lead to the development of innovative products and services, fostering growth and enhanced customer experience.

Leading Players in the Malaysia Payment Industry Sector

- Visa Inc

- Cimb Group Holdings Berhad

- Bank Islam Malaysia Berhad

- Ipay88 (m) Sdn Bhd

- United Overseas Bank (Malaysia) Bhd

- Huawei Pay (Huawei Technologies Co Ltd)

- Grab Pay (Grab Holdings Limited)

- Paypal Holdings Inc

- Maybank

- Samsung Pay (Samsung Electronics Co Ltd)

Key Milestones in Malaysia Payment Industry Industry

- May 2023: Maybank launched its cross-border QR payment service, enabling seamless transactions between Malaysia, Singapore, Indonesia, and Thailand. This expansion enhances cross-border payments, boosting regional economic integration.

- January 2023: Xoom, PayPal's money transfer service, introduced debit card deposits, offering faster and more convenient access to funds for remittance receivers. This improved service increases the efficiency and accessibility of international money transfers.

Strategic Outlook for Malaysia Payment Industry Market

The Malaysian payment industry is poised for sustained growth, driven by continued digitalization and expanding financial inclusion. Strategic investments in infrastructure, technology, and cybersecurity are essential for maintaining market competitiveness. Furthermore, focusing on innovative products and services to meet evolving customer needs is critical for success in this dynamic and fast-paced environment. The industry's future potential lies in leveraging technological advancements to enhance the user experience and drive greater financial accessibility.

Malaysia Payment Industry Segmentation

-

1. Mode of Payment

-

1.1. Point of Sale

- 1.1.1. Card Payments

- 1.1.2. Digital Wallets

- 1.1.3. Cash

- 1.1.4. Other Point-of-sale Payments

-

1.2. Online Sale

- 1.2.1. Other Online Sale Payments

-

1.1. Point of Sale

-

2. End-user Industry

- 2.1. Retail

- 2.2. Entertainment

- 2.3. Healthcare

- 2.4. Hospitality

- 2.5. Other End-user Industries

Malaysia Payment Industry Segmentation By Geography

- 1. Malaysia

Malaysia Payment Industry Regional Market Share

Geographic Coverage of Malaysia Payment Industry

Malaysia Payment Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1 E-commerce Growth

- 3.2.2 Rising Basket Spend

- 3.2.3 and Rise in Digitally-aware Population; Adoption of Card-based Payments

- 3.3. Market Restrains

- 3.3.1. Challenges Faced by Small Retailers and Street Vendors while Adapting to the Cashless Payment Ecosystem

- 3.4. Market Trends

- 3.4.1. Card Payments to Witness the Growth

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Malaysia Payment Industry Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Mode of Payment

- 5.1.1. Point of Sale

- 5.1.1.1. Card Payments

- 5.1.1.2. Digital Wallets

- 5.1.1.3. Cash

- 5.1.1.4. Other Point-of-sale Payments

- 5.1.2. Online Sale

- 5.1.2.1. Other Online Sale Payments

- 5.1.1. Point of Sale

- 5.2. Market Analysis, Insights and Forecast - by End-user Industry

- 5.2.1. Retail

- 5.2.2. Entertainment

- 5.2.3. Healthcare

- 5.2.4. Hospitality

- 5.2.5. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Malaysia

- 5.1. Market Analysis, Insights and Forecast - by Mode of Payment

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2025

- 6.2. Company Profiles

- 6.2.1 Visa Inc

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Cimb Group Holdings Berhad

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Bank Islam Malaysia Berhad

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Ipay88 (m) Sdn Bhd

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 United Overseas Bank (Malaysia) Bhd

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Huawei Pay (Huawei Technologies Co Ltd)*List Not Exhaustive

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Grab Pay (Grab Holdings Limited)

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Paypal Holdings Inc

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Maybank

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 Samsung Pay (Samsung Electronics Co Ltd)

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.1 Visa Inc

List of Figures

- Figure 1: Malaysia Payment Industry Revenue Breakdown (undefined, %) by Product 2025 & 2033

- Figure 2: Malaysia Payment Industry Share (%) by Company 2025

List of Tables

- Table 1: Malaysia Payment Industry Revenue undefined Forecast, by Mode of Payment 2020 & 2033

- Table 2: Malaysia Payment Industry Revenue undefined Forecast, by End-user Industry 2020 & 2033

- Table 3: Malaysia Payment Industry Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Malaysia Payment Industry Revenue undefined Forecast, by Mode of Payment 2020 & 2033

- Table 5: Malaysia Payment Industry Revenue undefined Forecast, by End-user Industry 2020 & 2033

- Table 6: Malaysia Payment Industry Revenue undefined Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Malaysia Payment Industry?

The projected CAGR is approximately 4%.

2. Which companies are prominent players in the Malaysia Payment Industry?

Key companies in the market include Visa Inc, Cimb Group Holdings Berhad, Bank Islam Malaysia Berhad, Ipay88 (m) Sdn Bhd, United Overseas Bank (Malaysia) Bhd, Huawei Pay (Huawei Technologies Co Ltd)*List Not Exhaustive, Grab Pay (Grab Holdings Limited), Paypal Holdings Inc, Maybank, Samsung Pay (Samsung Electronics Co Ltd).

3. What are the main segments of the Malaysia Payment Industry?

The market segments include Mode of Payment, End-user Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

E-commerce Growth. Rising Basket Spend. and Rise in Digitally-aware Population; Adoption of Card-based Payments.

6. What are the notable trends driving market growth?

Card Payments to Witness the Growth.

7. Are there any restraints impacting market growth?

Challenges Faced by Small Retailers and Street Vendors while Adapting to the Cashless Payment Ecosystem.

8. Can you provide examples of recent developments in the market?

May 2023: Maybank launched its cross-border QR payment service for Maybank customers traveling to Singapore, Indonesia, and Thailand, as they can now make cashless and instant payment transactions via the MAE app. Similarly, incoming tourists from these countries can make cashless payments with Maybank QRPay merchants in Malaysia. The new offering will enable Malaysians visiting the respective countries to enjoy a cheaper, faster, and more convenient payment option through the MAE app.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Malaysia Payment Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Malaysia Payment Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Malaysia Payment Industry?

To stay informed about further developments, trends, and reports in the Malaysia Payment Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence