Key Insights

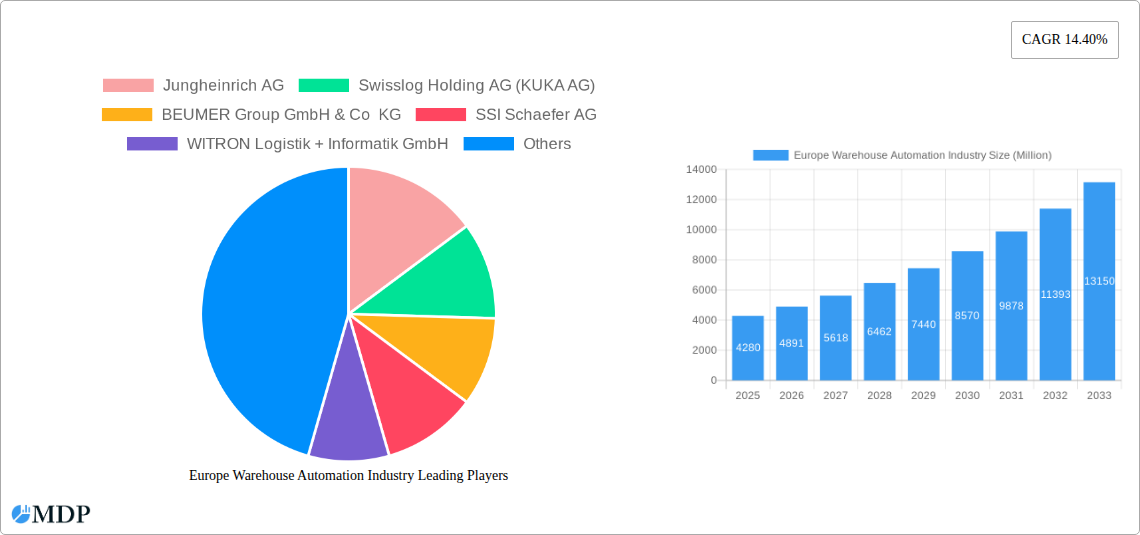

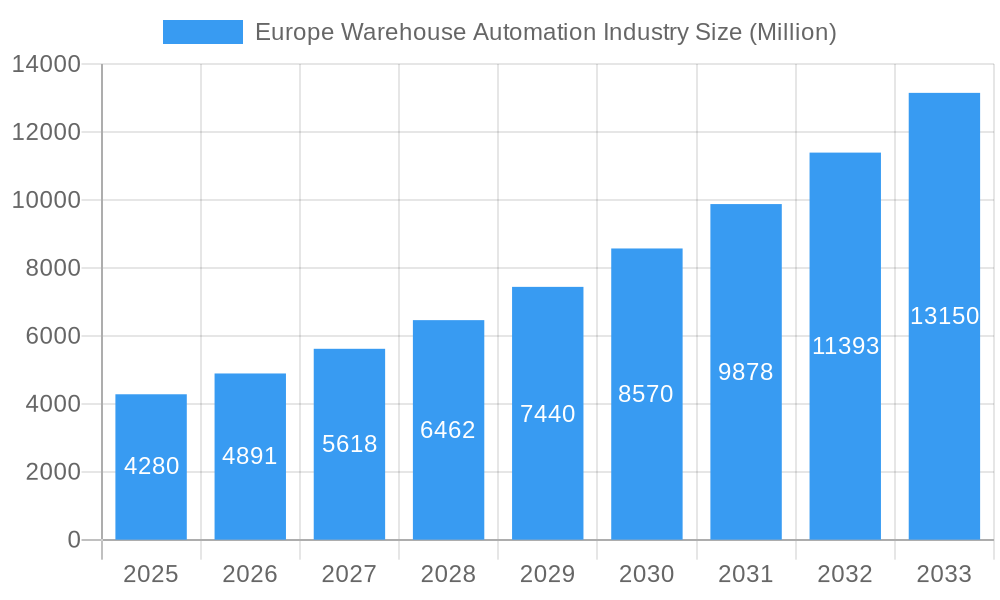

The European warehouse automation market is experiencing robust growth, projected to reach €4.28 billion in 2025 and maintain a Compound Annual Growth Rate (CAGR) of 14.40% from 2025 to 2033. This expansion is driven by several key factors. The increasing demand for faster and more efficient order fulfillment, fueled by the rise of e-commerce and the need for optimized supply chains, is a primary catalyst. Furthermore, labor shortages across Europe are pushing businesses to automate warehouse operations, reducing reliance on manual labor and increasing productivity. Technological advancements in robotics, particularly piece-picking robots, and sophisticated software like Warehouse Management Systems (WMS) and Warehouse Execution Systems (WES), are further enhancing efficiency and driving market growth. The integration of these systems allows for real-time inventory management, optimized routing, and automated order processing, leading to significant cost savings and improved accuracy. Germany, France, and the United Kingdom represent the largest national markets within Europe, reflecting their established industrial bases and significant e-commerce sectors. However, growth is expected across all regions, with expansion driven by both established players like Jungheinrich, Swisslog, and Dematic, and emerging technology providers offering innovative solutions.

Europe Warehouse Automation Industry Market Size (In Billion)

Market segmentation reveals a strong demand across various end-user industries. The food and beverage sector, encompassing manufacturing, distribution centers, and retail, is a significant contributor to market growth, followed by the post and parcel, and grocery sectors. The hardware component of warehouse automation systems, encompassing robots and automated guided vehicles (AGVs), commands a substantial share of the market, reflecting the increasing adoption of automated material handling solutions. Software and services, including WMS, WES, and maintenance contracts, play a critical role in maximizing the effectiveness of the hardware investments. The continued focus on improving last-mile delivery, expanding cold chain logistics, and implementing sustainable warehousing practices will shape future market developments. The ongoing integration of Artificial Intelligence (AI) and machine learning (ML) into warehouse automation solutions will further enhance efficiency and adaptability, contributing to continued growth throughout the forecast period.

Europe Warehouse Automation Industry Company Market Share

Europe Warehouse Automation Industry: A Comprehensive Market Report (2019-2033)

This comprehensive report provides an in-depth analysis of the European warehouse automation industry, covering market dynamics, leading players, technological advancements, and future growth prospects. With a detailed forecast period spanning 2025-2033 and a base year of 2025, this report is an essential resource for industry stakeholders, investors, and strategic decision-makers. The report analyzes a market valued at xx Million in 2025, projecting significant growth through 2033.

Europe Warehouse Automation Industry Market Dynamics & Concentration

The European warehouse automation market is characterized by moderate concentration, with several major players holding significant market share. The market's growth is driven by factors such as the increasing adoption of e-commerce, rising labor costs, and the need for improved supply chain efficiency. Stringent regulatory frameworks related to safety and data privacy also influence market dynamics. Product substitutes, while limited, include manual labor and less sophisticated automation solutions. However, the continuous innovation in robotics, AI, and software solutions keeps pushing the market forward.

The industry witnesses consistent M&A activity, with xx major deals recorded between 2019 and 2024. This consolidation trend reflects the competitive landscape and the drive towards acquiring cutting-edge technologies and expanding market reach. Key players like Jungheinrich AG and Swisslog Holding AG (KUKA AG) hold substantial market share, while smaller companies focus on niche segments or specialized solutions. Market share data for 2025 suggests the following distribution (approximate values):

- Jungheinrich AG: xx%

- Swisslog Holding AG (KUKA AG): xx%

- BEUMER Group GmbH & Co KG: xx%

- SSI Schaefer AG: xx%

- Others: xx%

Europe Warehouse Automation Industry Industry Trends & Analysis

The European warehouse automation market exhibits robust growth, with a projected Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025-2033). This growth is fueled by several key factors. The burgeoning e-commerce sector drives the demand for faster and more efficient order fulfillment, pushing companies to adopt automation solutions. Simultaneously, rising labor costs and a shortage of skilled workers in several European countries make automation a financially viable and necessary strategy. Technological disruptions, especially in areas like AI-powered robotics and advanced warehouse management systems (WMS), are revolutionizing warehouse operations. Consumer preferences for faster delivery times and increased product availability also contribute to this industry's growth. The market penetration of automated solutions is gradually increasing, with xx% of warehouses in major European countries expected to utilize some form of automation by 2033. The competitive dynamics are marked by intense innovation and strategic partnerships, leading to the constant evolution of warehouse automation solutions.

Leading Markets & Segments in Europe Warehouse Automation Industry

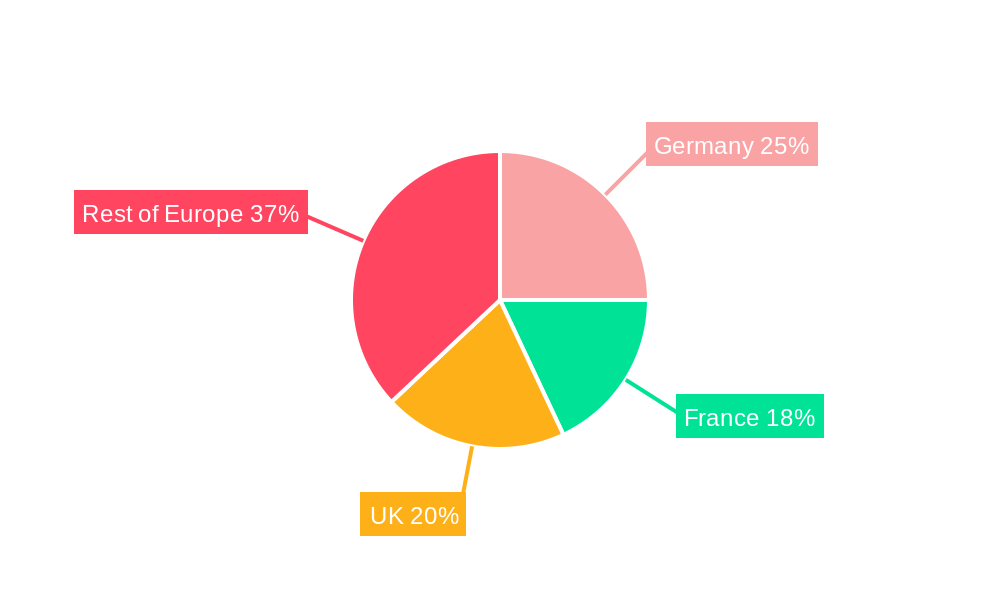

The UK, Germany, and France represent the largest markets for warehouse automation in Europe, accounting for xx% of the total market value in 2025. However, the "Rest of Europe" segment also shows significant growth potential.

Dominant Segments:

- End-User: The Food and Beverage sector, followed by Post and Parcel and Groceries, is a major driver of warehouse automation adoption.

- Component: Hardware (including Automated Guided Vehicles (AGVs), robots, and conveyors) constitutes the largest segment. Software (WMS and WES) and services (maintenance, etc.) are also key areas of growth.

Key Drivers by Country:

- United Kingdom: Strong e-commerce growth, favorable government policies supporting logistics infrastructure development.

- Germany: High industrial automation adoption, robust manufacturing sector, and a skilled workforce driving innovation.

- France: Growing logistics sector, government initiatives promoting digitalization, and investment in smart infrastructure.

- Rest of Europe: Diverse industrial landscape, increasing adoption of warehouse automation across various sectors.

Europe Warehouse Automation Industry Product Developments

The warehouse automation industry is witnessing rapid innovation in robotics, software, and system integration. Advanced technologies like AI-powered piece-picking robots, autonomous mobile robots (AMRs), and cloud-based WMS are revolutionizing warehouse operations. These innovations offer enhanced speed, accuracy, and scalability, leading to significant improvements in efficiency and cost reduction. The market is also witnessing a growing trend towards modular and flexible automation solutions, enabling businesses to customize their systems to their evolving needs. These developments are leading to a highly competitive landscape where market fit hinges on factors such as adaptability, integration capabilities, and cost-effectiveness.

Key Drivers of Europe Warehouse Automation Industry Growth

Several factors contribute to the growth of the European warehouse automation industry. Technological advancements, particularly in robotics and AI, significantly enhance warehouse efficiency and reduce labor costs. The rise of e-commerce fuels the need for faster and more efficient order fulfillment. Government initiatives promoting digitalization and infrastructure development within the logistics sector further stimulate market growth. Finally, rising labor costs and a skilled labor shortage across Europe make automation an increasingly attractive investment.

Challenges in the Europe Warehouse Automation Industry Market

The European warehouse automation market faces challenges such as high initial investment costs associated with implementing automation systems. Supply chain disruptions, particularly in the procurement of critical components, can impact project timelines and budgets. Integration complexities and the need for skilled workforce to operate and maintain the sophisticated systems also present obstacles. Furthermore, the competitive landscape necessitates continuous innovation to remain relevant. This necessitates a strategic approach to address both technological and economic challenges effectively.

Emerging Opportunities in Europe Warehouse Automation Industry

The long-term growth of the European warehouse automation industry is driven by several key opportunities. The increasing adoption of collaborative robots (cobots) that work alongside human workers promises safer and more efficient operations. Strategic partnerships between automation vendors and logistics providers open doors to wider market penetration and innovation. Moreover, the expansion into emerging markets within Europe provides significant potential for growth. Advances in AI and machine learning are unlocking even higher levels of efficiency and automation, creating new possibilities for optimizing warehouse operations.

Leading Players in the Europe Warehouse Automation Industry Sector

Key Milestones in Europe Warehouse Automation Industry Industry

- July 2021: ABB acquires ASTI Mobile Robotics Group, expanding its AMR portfolio and strengthening its position in flexible automation.

- May 2022: Lineage Logistics expands its automated warehouse in Peterborough, UK, significantly increasing its capacity and solidifying its presence in the Southeast region.

Strategic Outlook for Europe Warehouse Automation Industry Market

The future of the European warehouse automation market is bright. Continued technological advancements, coupled with the ever-increasing demand for efficient logistics solutions driven by e-commerce and supply chain optimization, will propel significant growth in the coming years. Strategic partnerships and investments in research and development will play a crucial role in shaping the industry's trajectory. The market presents substantial opportunities for both established players and innovative newcomers. The focus will be on developing increasingly sophisticated, flexible, and integrated automation solutions to meet the dynamic requirements of a constantly evolving landscape.

Europe Warehouse Automation Industry Segmentation

-

1. Component

-

1.1. Hardware

- 1.1.1. Mobile Robots (AGV, AMR)

- 1.1.2. Automated Storage and Retrieval Systems (AS/RS)

- 1.1.3. Automated Conveyor & Sorting Systems

- 1.1.4. De-palletizing/Palletizing Systems

- 1.1.5. Automati

- 1.1.6. Piece Picking Robots

- 1.2. Software

- 1.3. Services (Value Added Services, Maintenance, etc.)

-

1.1. Hardware

-

2. End-User

- 2.1. Food and

- 2.2. Post and Parcel

- 2.3. Groceries

- 2.4. General Merchandise

- 2.5. Apparel

- 2.6. Manufacturing (Durable and Non-Durable)

- 2.7. Other End-user Industries

Europe Warehouse Automation Industry Segmentation By Geography

-

1. Europe

- 1.1. United Kingdom

- 1.2. Germany

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Netherlands

- 1.7. Belgium

- 1.8. Sweden

- 1.9. Norway

- 1.10. Poland

- 1.11. Denmark

Europe Warehouse Automation Industry Regional Market Share

Geographic Coverage of Europe Warehouse Automation Industry

Europe Warehouse Automation Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 14.40% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Component

- 5.1.1. Hardware

- 5.1.1.1. Mobile Robots (AGV, AMR)

- 5.1.1.2. Automated Storage and Retrieval Systems (AS/RS)

- 5.1.1.3. Automated Conveyor & Sorting Systems

- 5.1.1.4. De-palletizing/Palletizing Systems

- 5.1.1.5. Automati

- 5.1.1.6. Piece Picking Robots

- 5.1.2. Software

- 5.1.3. Services (Value Added Services, Maintenance, etc.)

- 5.1.1. Hardware

- 5.2. Market Analysis, Insights and Forecast - by End-User

- 5.2.1. Food and

- 5.2.2. Post and Parcel

- 5.2.3. Groceries

- 5.2.4. General Merchandise

- 5.2.5. Apparel

- 5.2.6. Manufacturing (Durable and Non-Durable)

- 5.2.7. Other End-user Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Component

- 6. Europe Warehouse Automation Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Component

- 6.1.1. Hardware

- 6.1.1.1. Mobile Robots (AGV, AMR)

- 6.1.1.2. Automated Storage and Retrieval Systems (AS/RS)

- 6.1.1.3. Automated Conveyor & Sorting Systems

- 6.1.1.4. De-palletizing/Palletizing Systems

- 6.1.1.5. Automati

- 6.1.1.6. Piece Picking Robots

- 6.1.2. Software

- 6.1.3. Services (Value Added Services, Maintenance, etc.)

- 6.1.1. Hardware

- 6.2. Market Analysis, Insights and Forecast - by End-User

- 6.2.1. Food and

- 6.2.2. Post and Parcel

- 6.2.3. Groceries

- 6.2.4. General Merchandise

- 6.2.5. Apparel

- 6.2.6. Manufacturing (Durable and Non-Durable)

- 6.2.7. Other End-user Industries

- 6.1. Market Analysis, Insights and Forecast - by Component

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Jungheinrich AG

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Swisslog Holding AG (KUKA AG)

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 BEUMER Group GmbH & Co KG

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 SSI Schaefer AG

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 WITRON Logistik + Informatik GmbH

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 TGW Logistics Group GmbH

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Mecalux SA*List Not Exhaustive

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Vanderlande Industries BV

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Kion Group AG (Dematic Group)

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Knapp AG

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Jungheinrich AG

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: Europe Warehouse Automation Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: Europe Warehouse Automation Industry Share (%) by Company 2025

List of Tables

- Table 1: Europe Warehouse Automation Industry Revenue Million Forecast, by Component 2020 & 2033

- Table 2: Europe Warehouse Automation Industry Revenue Million Forecast, by End-User 2020 & 2033

- Table 3: Europe Warehouse Automation Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 4: Europe Warehouse Automation Industry Revenue Million Forecast, by Component 2020 & 2033

- Table 5: Europe Warehouse Automation Industry Revenue Million Forecast, by End-User 2020 & 2033

- Table 6: Europe Warehouse Automation Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 7: United Kingdom Europe Warehouse Automation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 8: Germany Europe Warehouse Automation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 9: France Europe Warehouse Automation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 10: Italy Europe Warehouse Automation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 11: Spain Europe Warehouse Automation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 12: Netherlands Europe Warehouse Automation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 13: Belgium Europe Warehouse Automation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: Sweden Europe Warehouse Automation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 15: Norway Europe Warehouse Automation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: Poland Europe Warehouse Automation Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 17: Denmark Europe Warehouse Automation Industry Revenue (Million) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Warehouse Automation Industry?

The projected CAGR is approximately 14.40%.

2. Which companies are prominent players in the Europe Warehouse Automation Industry?

Key companies in the market include Jungheinrich AG, Swisslog Holding AG (KUKA AG), BEUMER Group GmbH & Co KG, SSI Schaefer AG, WITRON Logistik + Informatik GmbH, TGW Logistics Group GmbH, Mecalux SA*List Not Exhaustive, Vanderlande Industries BV, Kion Group AG (Dematic Group), Knapp AG.

3. What are the main segments of the Europe Warehouse Automation Industry?

The market segments include Component, End-User.

4. Can you provide details about the market size?

The market size is estimated to be USD 4.28 Million as of 2022.

5. What are some drivers contributing to market growth?

Exponential Growth of the E-commerce Industry and Customer Expectation; Increasing Manufacturing Complexity and Technology Availability; Industry 4.0 Investments Driving The Demand For Automation & Material Handling.

6. What are the notable trends driving market growth?

Autonomous Mobile Robots (AMRs) are Gaining Popularity Throughout Europe.

7. Are there any restraints impacting market growth?

High Cost of Infrastructure set up.

8. Can you provide examples of recent developments in the market?

May 2022 - Lineage expanded its fully automated warehouse in Peterborough by adding 45,000 pallet spots, bringing its total capacity to roughly 71,000 pallets. The additional warehouse creates a critical Southeast Superhub that will support retail and foodservice customers with specific supply chain needs.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Warehouse Automation Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Warehouse Automation Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Warehouse Automation Industry?

To stay informed about further developments, trends, and reports in the Europe Warehouse Automation Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence