Key Insights

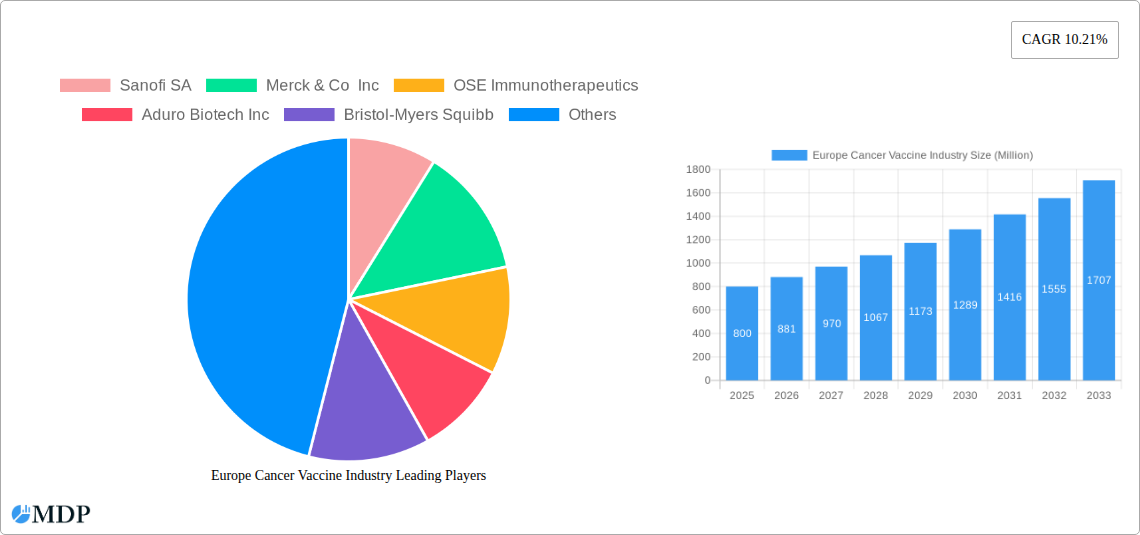

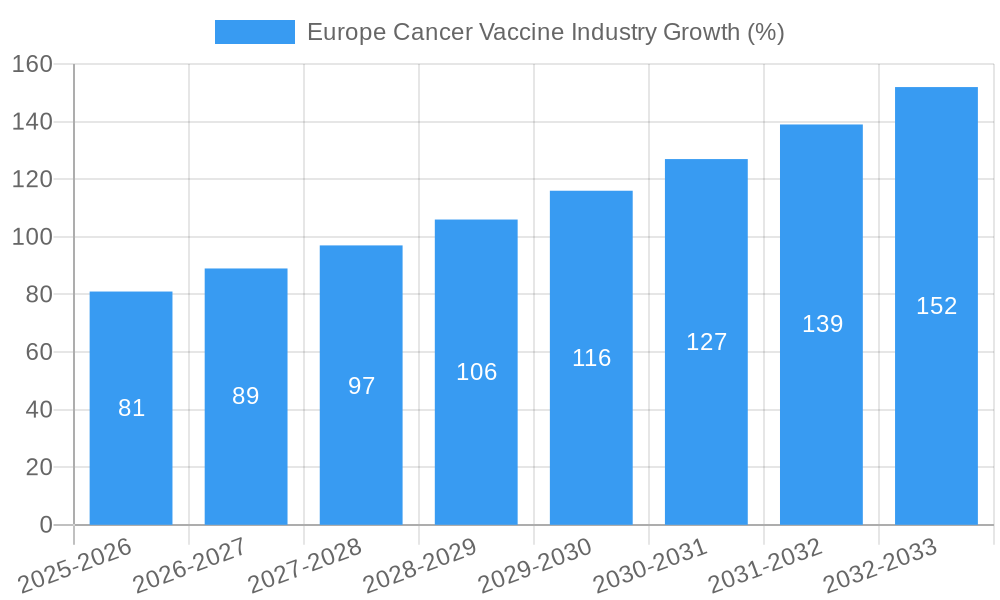

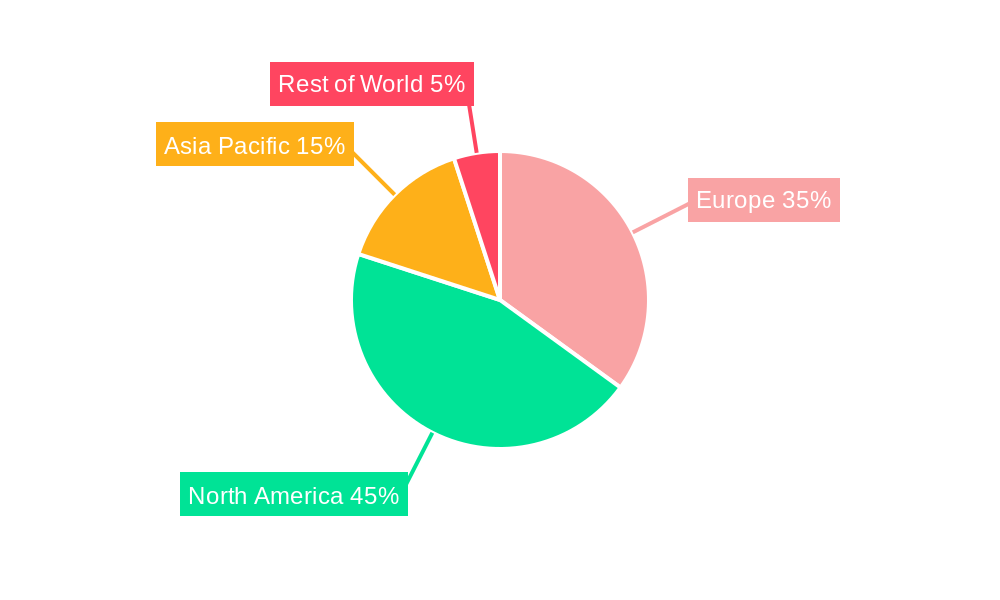

The European cancer vaccine market is experiencing robust growth, projected to reach a substantial size driven by several key factors. The rising prevalence of various cancer types, particularly prostate and cervical cancers, coupled with increasing awareness and demand for effective treatment options, fuels this expansion. Technological advancements in vaccine development, such as recombinant and viral vector vaccines, are leading to more targeted and efficacious therapies, further stimulating market growth. Furthermore, favorable government regulations and increased funding for cancer research contribute to the positive market outlook. The market is segmented by treatment method (preventive and therapeutic vaccines), application (prostate, cervical, and other cancers), and technology (recombinant, whole-cell, viral vector/DNA, and others). The competitive landscape features both established pharmaceutical giants like Sanofi, Merck, and GlaxoSmithKline, and emerging biotech companies, fostering innovation and competition. Based on a 10.21% CAGR from 2019-2024 and considering market trends, the European cancer vaccine market is expected to maintain a similar or slightly higher growth trajectory during the forecast period (2025-2033), expanding into new therapeutic areas and leveraging technological advancements. Germany, France, and the UK are expected to be the leading markets within Europe due to their robust healthcare infrastructure and high cancer incidence rates.

The market's growth is not without challenges. High research and development costs associated with developing and bringing novel cancer vaccines to market represent a significant hurdle. Furthermore, stringent regulatory approvals and the inherent complexities of cancer immunology can impede the market's expansion. Despite these restraints, the increasing investment in personalized medicine and the potential for combination therapies incorporating cancer vaccines alongside other treatments is expected to drive future growth and contribute significantly to the overall market value over the forecast period. The focus will likely be on improving vaccine efficacy, reducing side effects, and extending their applicability to a broader range of cancers.

Europe Cancer Vaccine Industry: A Comprehensive Market Report (2019-2033)

This comprehensive report provides an in-depth analysis of the European cancer vaccine market, offering invaluable insights for stakeholders across the industry. From market dynamics and leading players to emerging opportunities and future trends, this report is your essential guide to navigating this rapidly evolving landscape. With a study period spanning 2019-2033, a base year of 2025, and a forecast period of 2025-2033, this report delivers data-driven projections and actionable strategies. The market size is predicted to reach xx Million by 2033, exhibiting a CAGR of xx% during the forecast period.

Europe Cancer Vaccine Industry Market Dynamics & Concentration

The European cancer vaccine market is characterized by a moderate level of concentration, with key players such as Sanofi SA, Merck & Co Inc, and GlaxoSmithKline PLC holding significant market share. However, the market also features several smaller, innovative companies driving competition and technological advancements. The market is shaped by a complex interplay of factors including stringent regulatory frameworks (EMA approvals heavily influencing market entry), the emergence of novel treatment methods (e.g., personalized vaccines), and ongoing mergers & acquisitions (M&A) activity reshaping the competitive landscape.

- Market Concentration: The top 5 players account for approximately xx% of the market share in 2025.

- Innovation Drivers: Significant R&D investments are focused on developing more effective and targeted cancer vaccines, personalized medicine, and combination therapies.

- Regulatory Landscape: EMA approvals and stringent clinical trial requirements significantly influence market access and product lifecycle.

- Product Substitutes: Existing cancer treatments, such as chemotherapy and immunotherapy, represent key competitive alternatives.

- End-User Trends: Growing awareness of cancer prevention and treatment, alongside increasing demand for personalized medicine, is driving market growth.

- M&A Activity: The past five years have witnessed xx M&A deals in the European cancer vaccine industry, signaling industry consolidation and strategic expansion.

Europe Cancer Vaccine Industry Industry Trends & Analysis

The European cancer vaccine market is experiencing robust growth, fueled by several key trends. Technological advancements, such as the development of personalized vaccines and improved delivery systems, are driving innovation. Changing consumer preferences toward less invasive and more targeted treatments are boosting demand. Furthermore, favorable reimbursement policies in several European countries are contributing to market expansion. The market's competitive landscape is characterized by both established pharmaceutical giants and emerging biotech companies, fostering a dynamic environment of innovation and competition. Increased collaborations between academia, research institutions, and industry players are accelerating the development pipeline. The market is expected to see significant growth in the therapeutic vaccine segment, driven by the increasing prevalence of cancer and the rising awareness of the benefits of cancer vaccines. The CAGR for the overall market is projected at xx% during the forecast period, with the therapeutic vaccine segment exhibiting a higher growth rate than the preventive vaccine segment. Market penetration of cancer vaccines is expected to increase from xx% in 2025 to xx% by 2033.

Leading Markets & Segments in Europe Cancer Vaccine Industry

Germany and France are leading markets within Europe, driven by robust healthcare infrastructure, high cancer incidence rates, and supportive regulatory environments. The therapeutic vaccine segment holds the largest market share, owing to the significant unmet needs in existing cancer treatment options. Within applications, prostate and cervical cancers represent the largest segments, owing to their prevalence and the availability of targeted vaccine therapies. In terms of technology, recombinant cancer vaccines currently dominate, though viral vector and DNA cancer vaccines are gaining traction due to their enhanced efficacy and targeted delivery capabilities.

- Key Drivers for Germany and France:

- Well-developed healthcare infrastructure

- High levels of research and development investment

- Supportive regulatory frameworks and reimbursement policies

- High cancer prevalence rates

- Dominance Analysis: Therapeutic vaccines command a larger market share due to the high prevalence of cancers requiring treatment and growing demand for less toxic and more targeted options. Recombinant vaccines benefit from established manufacturing processes and a longer track record, while newer technologies like viral vectors are expected to capture significant market share over the forecast period. Prostate and cervical cancers dominate applications owing to the availability of vaccines, advanced research, and targeted treatment strategies.

Europe Cancer Vaccine Industry Product Developments

Recent years have witnessed significant advancements in cancer vaccine technology, focusing on improved efficacy, targeted delivery, and personalized approaches. Novel vaccines utilizing viral vectors and DNA delivery systems are entering the market, offering enhanced immunogenicity and targeting capabilities. These advancements, coupled with a better understanding of tumor immunology, are leading to the development of more effective and personalized cancer vaccines, improving patient outcomes and driving market growth.

Key Drivers of Europe Cancer Vaccine Industry Growth

Several factors are driving the growth of the European cancer vaccine market. Firstly, technological advancements in vaccine development are leading to more effective and targeted therapies. Secondly, increasing prevalence of cancer, coupled with rising awareness about the benefits of cancer vaccines, are fueling demand. Thirdly, supportive government policies and favorable reimbursement scenarios are further boosting market expansion.

Challenges in the Europe Cancer Vaccine Industry Market

The European cancer vaccine market faces several challenges, including high R&D costs, stringent regulatory requirements, and intense competition from established cancer treatments. Furthermore, supply chain complexities and the need for robust infrastructure for vaccine manufacturing and distribution pose additional obstacles. The relatively long clinical trial process significantly impacts market entry, affecting overall growth.

Emerging Opportunities in Europe Cancer Vaccine Industry

Several opportunities exist for growth in the European cancer vaccine market. The development of personalized vaccines, tailored to individual patient characteristics, holds significant promise. Strategic partnerships and collaborations between pharmaceutical companies, research institutions, and healthcare providers can further accelerate market expansion. Moreover, expanding into new therapeutic areas and exploring combination therapies with other cancer treatments can unlock significant growth potential.

Leading Players in the Europe Cancer Vaccine Industry Sector

- Sanofi SA

- Merck & Co Inc

- OSE Immunotherapeutics

- Aduro Biotech Inc

- Bristol-Myers Squibb

- Amgen Inc

- Sanpower Group Co Ltd (Dendreon Pharmaceuticals LLC)

- GlaxoSmithKline PLC

Key Milestones in Europe Cancer Vaccine Industry Industry

- 2021: Approval of a novel viral vector-based cancer vaccine for a specific cancer type in a major European market.

- 2022: Launch of a large-scale clinical trial evaluating a personalized cancer vaccine approach.

- 2023: Significant investment by a major pharmaceutical company in a promising cancer vaccine technology.

Strategic Outlook for Europe Cancer Vaccine Industry Market

The European cancer vaccine market presents substantial long-term growth potential. Continued advancements in vaccine technology, increasing collaborations, and expansion into new therapeutic areas will drive future growth. Strategic investments in R&D, focusing on personalized medicine and combination therapies, will be key for success. Companies that can effectively navigate the regulatory landscape and establish strong partnerships will be best positioned to capitalize on the market's future opportunities.

Europe Cancer Vaccine Industry Segmentation

-

1. Technology

- 1.1. Recombinant Cancer Vaccines

- 1.2. Whole-cell Cancer Vaccines

- 1.3. Viral Vector and DNA Cancer Vaccines

- 1.4. Other Technologies

-

2. Treatment Method

- 2.1. Preventive Vaccine

- 2.2. Therapeutic Vaccine

-

3. Application

- 3.1. Prostate Cancer

- 3.2. Cervical Cancer

- 3.3. Other Applications

Europe Cancer Vaccine Industry Segmentation By Geography

-

1. Europe

- 1.1. Germany

- 1.2. United Kingdom

- 1.3. France

- 1.4. Italy

- 1.5. Spain

- 1.6. Rest of Europe

Europe Cancer Vaccine Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 10.21% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. ; Increasing Number of Cancer Cases; Technological Developments in Cancer Vaccines coupled with Huge Expenditure on Cancer Care

- 3.3. Market Restrains

- 3.3.1. ; Stringent Regulatory Guidelines; Presence of Alternative Therapies

- 3.4. Market Trends

- 3.4.1. Preventive Vaccines are Expected to a Hold Significant Market Share in the Treatment Method

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Europe Cancer Vaccine Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Technology

- 5.1.1. Recombinant Cancer Vaccines

- 5.1.2. Whole-cell Cancer Vaccines

- 5.1.3. Viral Vector and DNA Cancer Vaccines

- 5.1.4. Other Technologies

- 5.2. Market Analysis, Insights and Forecast - by Treatment Method

- 5.2.1. Preventive Vaccine

- 5.2.2. Therapeutic Vaccine

- 5.3. Market Analysis, Insights and Forecast - by Application

- 5.3.1. Prostate Cancer

- 5.3.2. Cervical Cancer

- 5.3.3. Other Applications

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Europe

- 5.1. Market Analysis, Insights and Forecast - by Technology

- 6. Germany Europe Cancer Vaccine Industry Analysis, Insights and Forecast, 2019-2031

- 7. France Europe Cancer Vaccine Industry Analysis, Insights and Forecast, 2019-2031

- 8. Italy Europe Cancer Vaccine Industry Analysis, Insights and Forecast, 2019-2031

- 9. United Kingdom Europe Cancer Vaccine Industry Analysis, Insights and Forecast, 2019-2031

- 10. Netherlands Europe Cancer Vaccine Industry Analysis, Insights and Forecast, 2019-2031

- 11. Sweden Europe Cancer Vaccine Industry Analysis, Insights and Forecast, 2019-2031

- 12. Rest of Europe Europe Cancer Vaccine Industry Analysis, Insights and Forecast, 2019-2031

- 13. Competitive Analysis

- 13.1. Market Share Analysis 2024

- 13.2. Company Profiles

- 13.2.1 Sanofi SA

- 13.2.1.1. Overview

- 13.2.1.2. Products

- 13.2.1.3. SWOT Analysis

- 13.2.1.4. Recent Developments

- 13.2.1.5. Financials (Based on Availability)

- 13.2.2 Merck & Co Inc

- 13.2.2.1. Overview

- 13.2.2.2. Products

- 13.2.2.3. SWOT Analysis

- 13.2.2.4. Recent Developments

- 13.2.2.5. Financials (Based on Availability)

- 13.2.3 OSE Immunotherapeutics

- 13.2.3.1. Overview

- 13.2.3.2. Products

- 13.2.3.3. SWOT Analysis

- 13.2.3.4. Recent Developments

- 13.2.3.5. Financials (Based on Availability)

- 13.2.4 Aduro Biotech Inc

- 13.2.4.1. Overview

- 13.2.4.2. Products

- 13.2.4.3. SWOT Analysis

- 13.2.4.4. Recent Developments

- 13.2.4.5. Financials (Based on Availability)

- 13.2.5 Bristol-Myers Squibb

- 13.2.5.1. Overview

- 13.2.5.2. Products

- 13.2.5.3. SWOT Analysis

- 13.2.5.4. Recent Developments

- 13.2.5.5. Financials (Based on Availability)

- 13.2.6 Amgen Inc

- 13.2.6.1. Overview

- 13.2.6.2. Products

- 13.2.6.3. SWOT Analysis

- 13.2.6.4. Recent Developments

- 13.2.6.5. Financials (Based on Availability)

- 13.2.7 Sanpower Group Co Ltd (Dendreon Pharmaceuticals LLC)

- 13.2.7.1. Overview

- 13.2.7.2. Products

- 13.2.7.3. SWOT Analysis

- 13.2.7.4. Recent Developments

- 13.2.7.5. Financials (Based on Availability)

- 13.2.8 GlaxoSmithKline PLC

- 13.2.8.1. Overview

- 13.2.8.2. Products

- 13.2.8.3. SWOT Analysis

- 13.2.8.4. Recent Developments

- 13.2.8.5. Financials (Based on Availability)

- 13.2.1 Sanofi SA

List of Figures

- Figure 1: Europe Cancer Vaccine Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Europe Cancer Vaccine Industry Share (%) by Company 2024

List of Tables

- Table 1: Europe Cancer Vaccine Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Europe Cancer Vaccine Industry Volume K Unit Forecast, by Region 2019 & 2032

- Table 3: Europe Cancer Vaccine Industry Revenue Million Forecast, by Technology 2019 & 2032

- Table 4: Europe Cancer Vaccine Industry Volume K Unit Forecast, by Technology 2019 & 2032

- Table 5: Europe Cancer Vaccine Industry Revenue Million Forecast, by Treatment Method 2019 & 2032

- Table 6: Europe Cancer Vaccine Industry Volume K Unit Forecast, by Treatment Method 2019 & 2032

- Table 7: Europe Cancer Vaccine Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 8: Europe Cancer Vaccine Industry Volume K Unit Forecast, by Application 2019 & 2032

- Table 9: Europe Cancer Vaccine Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 10: Europe Cancer Vaccine Industry Volume K Unit Forecast, by Region 2019 & 2032

- Table 11: Europe Cancer Vaccine Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 12: Europe Cancer Vaccine Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 13: Germany Europe Cancer Vaccine Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Germany Europe Cancer Vaccine Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 15: France Europe Cancer Vaccine Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: France Europe Cancer Vaccine Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 17: Italy Europe Cancer Vaccine Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: Italy Europe Cancer Vaccine Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 19: United Kingdom Europe Cancer Vaccine Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: United Kingdom Europe Cancer Vaccine Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 21: Netherlands Europe Cancer Vaccine Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: Netherlands Europe Cancer Vaccine Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 23: Sweden Europe Cancer Vaccine Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: Sweden Europe Cancer Vaccine Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 25: Rest of Europe Europe Cancer Vaccine Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 26: Rest of Europe Europe Cancer Vaccine Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 27: Europe Cancer Vaccine Industry Revenue Million Forecast, by Technology 2019 & 2032

- Table 28: Europe Cancer Vaccine Industry Volume K Unit Forecast, by Technology 2019 & 2032

- Table 29: Europe Cancer Vaccine Industry Revenue Million Forecast, by Treatment Method 2019 & 2032

- Table 30: Europe Cancer Vaccine Industry Volume K Unit Forecast, by Treatment Method 2019 & 2032

- Table 31: Europe Cancer Vaccine Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 32: Europe Cancer Vaccine Industry Volume K Unit Forecast, by Application 2019 & 2032

- Table 33: Europe Cancer Vaccine Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 34: Europe Cancer Vaccine Industry Volume K Unit Forecast, by Country 2019 & 2032

- Table 35: Germany Europe Cancer Vaccine Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 36: Germany Europe Cancer Vaccine Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 37: United Kingdom Europe Cancer Vaccine Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 38: United Kingdom Europe Cancer Vaccine Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 39: France Europe Cancer Vaccine Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 40: France Europe Cancer Vaccine Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 41: Italy Europe Cancer Vaccine Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 42: Italy Europe Cancer Vaccine Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 43: Spain Europe Cancer Vaccine Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 44: Spain Europe Cancer Vaccine Industry Volume (K Unit) Forecast, by Application 2019 & 2032

- Table 45: Rest of Europe Europe Cancer Vaccine Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 46: Rest of Europe Europe Cancer Vaccine Industry Volume (K Unit) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Europe Cancer Vaccine Industry?

The projected CAGR is approximately 10.21%.

2. Which companies are prominent players in the Europe Cancer Vaccine Industry?

Key companies in the market include Sanofi SA, Merck & Co Inc, OSE Immunotherapeutics, Aduro Biotech Inc, Bristol-Myers Squibb, Amgen Inc , Sanpower Group Co Ltd (Dendreon Pharmaceuticals LLC), GlaxoSmithKline PLC.

3. What are the main segments of the Europe Cancer Vaccine Industry?

The market segments include Technology, Treatment Method, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

; Increasing Number of Cancer Cases; Technological Developments in Cancer Vaccines coupled with Huge Expenditure on Cancer Care.

6. What are the notable trends driving market growth?

Preventive Vaccines are Expected to a Hold Significant Market Share in the Treatment Method.

7. Are there any restraints impacting market growth?

; Stringent Regulatory Guidelines; Presence of Alternative Therapies.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Unit.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Europe Cancer Vaccine Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Europe Cancer Vaccine Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Europe Cancer Vaccine Industry?

To stay informed about further developments, trends, and reports in the Europe Cancer Vaccine Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence