Key Insights

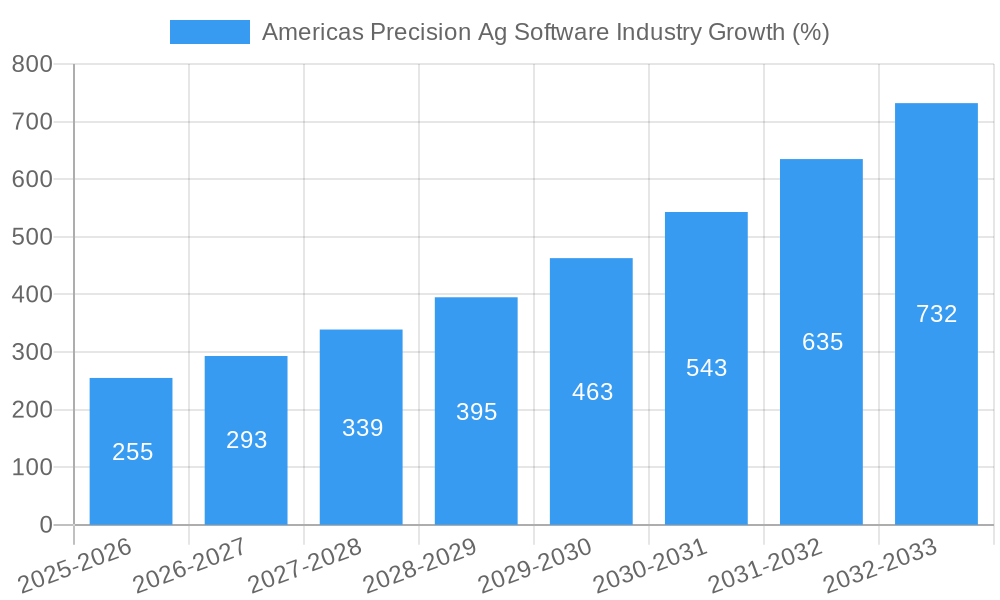

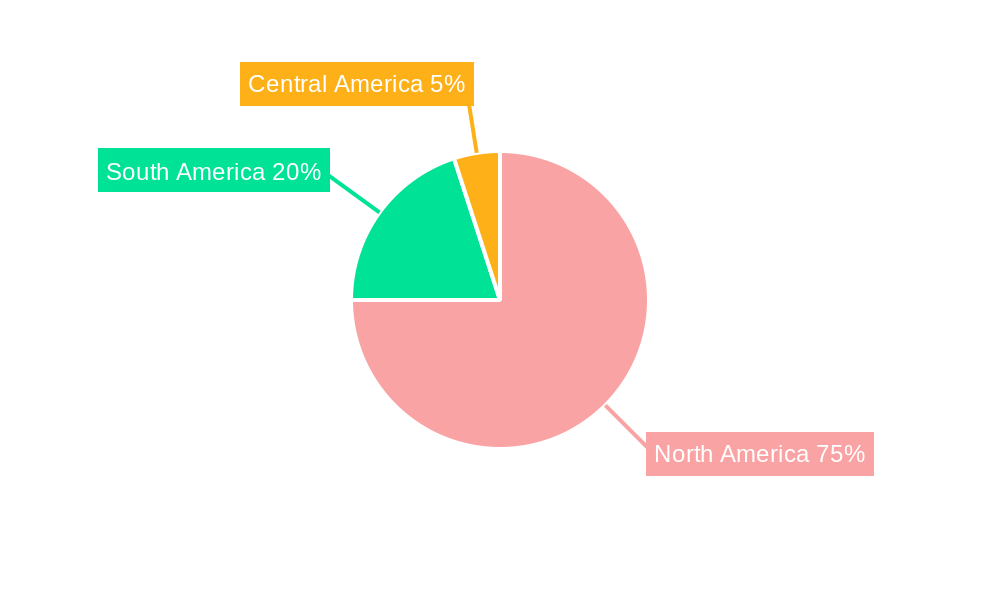

The Americas precision agriculture software market is experiencing robust growth, projected to reach a significant market size by 2033. A Compound Annual Growth Rate (CAGR) of 17% from 2025 to 2033 indicates a substantial expansion driven by several key factors. The increasing adoption of technology by farmers to improve efficiency, optimize resource utilization, and enhance crop yields is a primary driver. Favorable government initiatives promoting digital agriculture and precision farming techniques in both North and South America are further accelerating market growth. Specific trends include the rising demand for cloud-based solutions offering scalability and accessibility, the integration of AI and machine learning for predictive analytics and decision support, and the growing use of IoT sensors for real-time data collection. However, factors such as the high initial investment costs associated with implementing precision agriculture software and the need for reliable internet connectivity, particularly in remote areas, present challenges to broader market penetration. The market is segmented by deployment type (cloud, local/web-based) and geography (United States, Canada, Mexico, Argentina, and the Rest of the Americas), with North America currently holding the largest market share due to higher technology adoption rates and established agricultural infrastructure. Leading companies such as Deere & Company, IBM, and Trimble are actively investing in research and development, driving innovation and expanding product offerings within this dynamic market. The competitive landscape is characterized by both established players and emerging technology companies, creating a diverse and rapidly evolving market.

The South American market, while currently smaller than North America, demonstrates significant growth potential. Brazil, in particular, is poised for considerable expansion due to its large agricultural sector and increasing investment in agricultural technology. The continued development of affordable and user-friendly software solutions, coupled with targeted initiatives to enhance digital literacy among farmers, will be crucial for unlocking the full potential of the precision agriculture software market in the Americas. The presence of major agricultural players in both North and South America, combined with supportive government policies, positions the region for sustained growth in the coming years. The increasing focus on sustainable agricultural practices further fuels the adoption of precision agriculture technologies, as farmers seek to optimize resource use and reduce their environmental footprint.

Unlock the Potential: Americas Precision Ag Software Market Report (2019-2033)

This comprehensive report provides an in-depth analysis of the Americas Precision Agriculture Software market, offering invaluable insights for stakeholders seeking to capitalize on its significant growth potential. From market dynamics and leading players to emerging opportunities and future trends, this report is your essential guide to navigating this rapidly evolving landscape. The study period covers 2019-2033, with a base year of 2025 and a forecast period of 2025-2033. The market size in 2025 is estimated at $XX Million.

Americas Precision Ag Software Industry Market Dynamics & Concentration

The Americas precision agriculture software market is experiencing robust growth, driven by increasing adoption of advanced technologies and a rising demand for enhanced farm efficiency. Market concentration is moderate, with several key players holding significant market share, but a considerable number of smaller, specialized firms also contributing. Deere & Company, IBM Corporation, and Trimble Inc. are among the dominant players, collectively accounting for an estimated xx% of the market share in 2025. However, the landscape is dynamic, with ongoing mergers and acquisitions (M&A) activity shaping the competitive landscape. Over the historical period (2019-2024), approximately xx M&A deals were recorded, indicating a high level of consolidation and strategic investment in the sector.

- Innovation Drivers: Advancements in AI, IoT, and cloud computing are fueling the development of sophisticated software solutions that optimize crop yields, resource management, and overall farm profitability.

- Regulatory Frameworks: Government initiatives promoting sustainable agriculture and technological adoption are creating a favorable environment for market expansion. However, data privacy regulations and cybersecurity concerns pose challenges.

- Product Substitutes: While precision agriculture software is increasingly becoming the standard, traditional farming practices and less sophisticated software still represent potential substitutes.

- End-User Trends: Farmers are increasingly adopting precision agriculture software to improve efficiency, reduce costs, and increase yields. Demand is particularly strong among large-scale commercial farms and cooperatives.

Americas Precision Ag Software Industry Industry Trends & Analysis

The Americas precision agriculture software market is witnessing impressive growth, with a projected Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025-2033). This growth is primarily driven by several key factors: increasing adoption of cloud-based solutions, the rising penetration of smartphones and other connected devices on farms, and the growing awareness of the benefits of data-driven decision-making in agriculture. Technological disruptions, particularly the integration of AI and machine learning into precision agriculture software, are further enhancing the market's capabilities and attracting new users. Consumer preferences are shifting towards integrated, user-friendly solutions offering comprehensive data analysis and actionable insights. Competitive dynamics are characterized by intense innovation, strategic partnerships, and occasional M&A activity, as companies strive to consolidate their market positions and expand their offerings. Market penetration is expected to reach xx% by 2033.

Leading Markets & Segments in Americas Precision Ag Software Industry

The United States remains the dominant market for precision agriculture software in the Americas, accounting for approximately xx% of the total market value in 2025. This is driven by factors such as high adoption rates among large-scale farms, well-developed agricultural infrastructure, and a favorable regulatory environment.

- United States: Strong agricultural sector, high technology adoption rate, advanced infrastructure.

- Canada: Growing adoption of precision agriculture technologies, significant government support for agricultural innovation.

- Mexico: Expanding agricultural sector, increasing investment in modern farming practices.

- Argentina: Significant potential for growth, increasing adoption of precision agriculture in key crops like soybeans.

- Rest of Americas: Varied levels of adoption, opportunities for market expansion in emerging economies.

Cloud-based solutions dominate the market by type, holding a significantly larger share compared to local/web-based software. The advantages of scalability, accessibility, and real-time data synchronization make cloud solutions highly attractive to farmers.

Americas Precision Ag Software Industry Product Developments

Recent product innovations focus on enhancing data analytics capabilities, integrating AI for predictive modeling, and improving user interfaces for greater accessibility. Applications are expanding beyond yield monitoring to encompass areas like soil health management, irrigation optimization, and pest and disease control. Competitive advantages are increasingly being built on data integration capabilities, the ability to tailor solutions to specific crop types and farming practices, and the provision of comprehensive support and training to farmers.

Key Drivers of Americas Precision Ag Software Industry Growth

The growth of the Americas precision agriculture software market is fueled by a convergence of technological, economic, and regulatory factors. Technological advancements, specifically in AI, IoT, and cloud computing, are enabling the development of sophisticated software solutions that optimize farming operations. Economic factors, such as the rising cost of agricultural inputs and the need for enhanced farm efficiency, are driving adoption. Favorable government policies promoting sustainable agriculture and technological adoption also play a significant role.

Challenges in the Americas Precision Ag Software Industry Market

Challenges facing the market include high initial investment costs for some precision agriculture technologies, the digital divide affecting smaller farms, data security and privacy concerns, and the need for robust internet connectivity in rural areas. These factors can significantly impact adoption rates and limit market penetration, particularly in certain regions.

Emerging Opportunities in Americas Precision Ag Software Industry

Significant opportunities lie in the integration of AI and machine learning to provide even more precise and predictive insights for farmers. Strategic partnerships between software providers and agricultural equipment manufacturers can drive wider adoption. Expansion into emerging markets in the Americas, where the adoption of precision agriculture is still in its early stages, offers significant potential for growth.

Leading Players in the Americas Precision Ag Software Industry Sector

- Deere & Company

- IBM Corporation

- AGCO Corporation

- AG Leader Technology Inc

- Taranis Inc

- AGJunction Inc

- Harris Geospatial Solutions Inc

- Trimble Inc

- AgDNA Technologies Inc

- Granular Inc

- Bayer CropScience AG

Key Milestones in Americas Precision Ag Software Industry Industry

- 2020: Increased investment in AI-powered precision agriculture software solutions.

- 2021: Several significant mergers and acquisitions among major players in the industry.

- 2022: Launch of several new cloud-based platforms offering integrated precision agriculture solutions.

- 2023: Growing adoption of software solutions incorporating sustainability metrics.

- 2024: Increased focus on data security and privacy regulations within the sector.

Strategic Outlook for Americas Precision Ag Software Industry Market

The future of the Americas precision agriculture software market appears bright, with continued growth driven by technological innovation, increasing farm efficiency demands, and supportive government policies. Strategic opportunities exist in expanding into underserved markets, developing more integrated and user-friendly solutions, and focusing on data-driven decision-making to enhance sustainability and profitability in agriculture. The market's potential for growth remains substantial, and companies that can adapt to the changing technological landscape and consumer preferences are well-positioned to succeed.

Americas Precision Ag Software Industry Segmentation

-

1. Type

- 1.1. Cloud

- 1.2. Local/Web-based

Americas Precision Ag Software Industry Segmentation By Geography

-

1. Americas

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

- 1.4. Brazil

- 1.5. Argentina

- 1.6. Chile

- 1.7. Colombia

- 1.8. Peru

Americas Precision Ag Software Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 17.00% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1 ; Adoption of Precision Technology in the Sustainable and Efficient Agriculture Sector in Americas; Shortage of Farm labor

- 3.2.2 Along with Increasing Farm Size Across North America

- 3.3. Market Restrains

- 3.3.1. ; High Capital Cost and Complexity Regarding System Upgrades

- 3.4. Market Trends

- 3.4.1. Cloud-based Precision Farming Software is Expected to Grow Significantly

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Americas Precision Ag Software Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Cloud

- 5.1.2. Local/Web-based

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Americas

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Latin America Americas Precision Ag Software Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 6.1.1 Mexico

- 6.1.2 Brazil

- 7. North America Americas Precision Ag Software Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 7.1.1 United States

- 7.1.2 Canada

- 7.1.3 Mexico

- 8. South America Americas Precision Ag Software Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 8.1.1 Brazil

- 8.1.2 Argentina

- 8.1.3 Rest of South America

- 9. Competitive Analysis

- 9.1. Market Share Analysis 2024

- 9.2. Company Profiles

- 9.2.1 Deere & Company

- 9.2.1.1. Overview

- 9.2.1.2. Products

- 9.2.1.3. SWOT Analysis

- 9.2.1.4. Recent Developments

- 9.2.1.5. Financials (Based on Availability)

- 9.2.2 IBM Corporation

- 9.2.2.1. Overview

- 9.2.2.2. Products

- 9.2.2.3. SWOT Analysis

- 9.2.2.4. Recent Developments

- 9.2.2.5. Financials (Based on Availability)

- 9.2.3 AGCO Corporation

- 9.2.3.1. Overview

- 9.2.3.2. Products

- 9.2.3.3. SWOT Analysis

- 9.2.3.4. Recent Developments

- 9.2.3.5. Financials (Based on Availability)

- 9.2.4 AG Leader Technology Inc

- 9.2.4.1. Overview

- 9.2.4.2. Products

- 9.2.4.3. SWOT Analysis

- 9.2.4.4. Recent Developments

- 9.2.4.5. Financials (Based on Availability)

- 9.2.5 Taranis Inc

- 9.2.5.1. Overview

- 9.2.5.2. Products

- 9.2.5.3. SWOT Analysis

- 9.2.5.4. Recent Developments

- 9.2.5.5. Financials (Based on Availability)

- 9.2.6 AGJunction Inc

- 9.2.6.1. Overview

- 9.2.6.2. Products

- 9.2.6.3. SWOT Analysis

- 9.2.6.4. Recent Developments

- 9.2.6.5. Financials (Based on Availability)

- 9.2.7 Harris Geospatial Solutions Inc *List Not Exhaustive

- 9.2.7.1. Overview

- 9.2.7.2. Products

- 9.2.7.3. SWOT Analysis

- 9.2.7.4. Recent Developments

- 9.2.7.5. Financials (Based on Availability)

- 9.2.8 Trimble Inc

- 9.2.8.1. Overview

- 9.2.8.2. Products

- 9.2.8.3. SWOT Analysis

- 9.2.8.4. Recent Developments

- 9.2.8.5. Financials (Based on Availability)

- 9.2.9 AgDNA Technologies Inc

- 9.2.9.1. Overview

- 9.2.9.2. Products

- 9.2.9.3. SWOT Analysis

- 9.2.9.4. Recent Developments

- 9.2.9.5. Financials (Based on Availability)

- 9.2.10 Granular Inc

- 9.2.10.1. Overview

- 9.2.10.2. Products

- 9.2.10.3. SWOT Analysis

- 9.2.10.4. Recent Developments

- 9.2.10.5. Financials (Based on Availability)

- 9.2.11 Bayer CropScience AG

- 9.2.11.1. Overview

- 9.2.11.2. Products

- 9.2.11.3. SWOT Analysis

- 9.2.11.4. Recent Developments

- 9.2.11.5. Financials (Based on Availability)

- 9.2.1 Deere & Company

List of Figures

- Figure 1: Americas Precision Ag Software Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Americas Precision Ag Software Industry Share (%) by Company 2024

List of Tables

- Table 1: Americas Precision Ag Software Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Americas Precision Ag Software Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 3: Americas Precision Ag Software Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 4: Americas Precision Ag Software Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 5: Mexico Americas Precision Ag Software Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 6: Brazil Americas Precision Ag Software Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: Americas Precision Ag Software Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 8: United States Americas Precision Ag Software Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Canada Americas Precision Ag Software Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Mexico Americas Precision Ag Software Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Americas Precision Ag Software Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 12: Brazil Americas Precision Ag Software Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Argentina Americas Precision Ag Software Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Rest of South America Americas Precision Ag Software Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 15: Americas Precision Ag Software Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 16: Americas Precision Ag Software Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 17: United States Americas Precision Ag Software Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: Canada Americas Precision Ag Software Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: Mexico Americas Precision Ag Software Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Brazil Americas Precision Ag Software Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 21: Argentina Americas Precision Ag Software Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: Chile Americas Precision Ag Software Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: Colombia Americas Precision Ag Software Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: Peru Americas Precision Ag Software Industry Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Americas Precision Ag Software Industry?

The projected CAGR is approximately 17.00%.

2. Which companies are prominent players in the Americas Precision Ag Software Industry?

Key companies in the market include Deere & Company, IBM Corporation, AGCO Corporation, AG Leader Technology Inc, Taranis Inc, AGJunction Inc, Harris Geospatial Solutions Inc *List Not Exhaustive, Trimble Inc, AgDNA Technologies Inc, Granular Inc, Bayer CropScience AG.

3. What are the main segments of the Americas Precision Ag Software Industry?

The market segments include Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

; Adoption of Precision Technology in the Sustainable and Efficient Agriculture Sector in Americas; Shortage of Farm labor. Along with Increasing Farm Size Across North America.

6. What are the notable trends driving market growth?

Cloud-based Precision Farming Software is Expected to Grow Significantly.

7. Are there any restraints impacting market growth?

; High Capital Cost and Complexity Regarding System Upgrades.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Americas Precision Ag Software Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Americas Precision Ag Software Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Americas Precision Ag Software Industry?

To stay informed about further developments, trends, and reports in the Americas Precision Ag Software Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence