Key Insights

The African sports drink market, valued at approximately $X million in 2025 (assuming a logical value based on the provided CAGR of 11.55% and a reasonable starting point considering the regional context), is projected to experience robust growth, driven by several key factors. Rising health consciousness among consumers, coupled with increasing participation in sports and fitness activities across the continent, fuels demand for functional beverages like electrolyte-enhanced waters and protein-based sports drinks. The burgeoning middle class and rising disposable incomes, particularly in countries like South Africa, UAE, and Saudi Arabia, contribute to increased purchasing power and spending on premium sports drinks. Furthermore, strategic marketing campaigns emphasizing health benefits and hydration are effectively expanding market penetration. The preference for convenient packaging formats, such as PET bottles and convenient store distribution, further enhances market accessibility. However, challenges remain, such as price sensitivity in certain markets and the availability of cheaper alternatives. Competition among established international players and local brands is fierce, requiring differentiation strategies to secure market share. The market's segmentation by product type (electrolyte-enhanced, isotonic, etc.) and distribution channel offers opportunities for targeted marketing and product development.

Looking ahead to 2033, the market is expected to maintain a steady growth trajectory, propelled by continuous improvements in product innovation, expansion of distribution networks into underserved areas, and increased consumer awareness. The rising adoption of e-commerce and online retail channels will create new avenues for reaching a wider audience. Companies are likely to focus on strategies that leverage the growing influence of social media and health and wellness influencers to reach younger demographics. A key challenge will be navigating the complexities of diverse consumer preferences and economic conditions across different African regions. Successful players will need to understand the nuanced market dynamics and adapt their product offerings and marketing approaches accordingly. Factors such as fluctuating exchange rates and infrastructure limitations should also be considered when assessing future market growth.

Africa Sports Drinks Industry: Market Analysis & Forecast 2019-2033

This comprehensive report provides a detailed analysis of the Africa sports drinks industry, covering market dynamics, leading players, key trends, and future growth opportunities. With a focus on the period 2019-2033, including a base year of 2025, this report is an indispensable resource for industry stakeholders, investors, and strategic decision-makers seeking to navigate this dynamic and rapidly evolving market. The study covers a wide spectrum, encompassing various soft drink types, packaging formats, and distribution channels. It unveils crucial insights into market concentration, competitive landscapes, and emerging trends, enabling informed business strategies.

Africa Sports Drinks Industry Market Dynamics & Concentration

The African sports drinks market presents a moderately concentrated landscape, dominated by multinational giants like PepsiCo Inc, The Coca-Cola Company, and Tiger Brands Ltd, who command substantial market share. However, a dynamic competitive environment is emerging, with smaller, regional players such as Kingsley Beverages Limited and Aje Group actively challenging the established order. Their success hinges on innovative product development and precisely targeted marketing campaigns, effectively capturing niche segments of the market. The degree of market concentration is significantly shaped by factors including brand recognition, the extent and efficiency of distribution networks, and robust marketing capabilities.

A key driver of market evolution is the relentless pursuit of innovation, with companies investing heavily in R&D to create new products catering to evolving consumer preferences. This includes the development of electrolyte-enhanced waters, protein-infused sports drinks, and other functional beverages. Regulatory pressures and growing health concerns surrounding high sugar content are further reshaping the market, fostering the creation of low-sugar and sugar-free alternatives. The presence of substitute products, such as energy drinks and plain water, adds another layer of competitive intensity. Demand for convenient, on-the-go consumption is also a major influence, prompting the adoption of practical packaging solutions and strategic distribution channel optimization. Mergers and acquisitions (M&A) activity, while moderate (approximately xx deals between 2019 and 2024), signals a growing appetite for market expansion and consolidation. The collective market share held by the top 5 players is estimated at xx%.

- Key Market Dynamics: Innovation, Regulation, Shifting Consumer Preferences, Intense Competition, Strategic M&A activity

- Market Concentration: Moderately Concentrated

- M&A Deals (2019-2024): xx

- Top 5 Players Market Share (2024): xx%

Africa Sports Drinks Industry Industry Trends & Analysis

The African sports drinks market is demonstrating robust growth, projected to achieve a Compound Annual Growth Rate (CAGR) of xx% throughout the forecast period (2025-2033). This upward trajectory is fueled by several key factors, including rising disposable incomes across various demographics, a heightened health consciousness among consumers, and a growing preference for healthier hydration choices. Technological advancements, notably improvements in packaging and distribution systems, further contribute to market expansion. Consumer preferences are decisively shifting toward healthier alternatives, with a clear preference for low-sugar and functional drinks.

The competitive landscape is fiercely contested, with established players facing significant challenges from smaller, more agile competitors adept at introducing niche products and employing innovative marketing strategies. Compared to other beverage categories, the market penetration of sports drinks remains relatively low, creating substantial opportunities for future growth. The increasing popularity of sports and fitness activities across the continent, coupled with a growing awareness of the importance of hydration for athletic performance and overall well-being, is a major impetus for market expansion. The increasing adoption of e-commerce and online retail channels presents a significant avenue for further market growth. The estimated market value in 2025 is $xx Million, projected to reach $xx Million by 2033.

Leading Markets & Segments in Africa Sports Drinks Industry

South Africa currently holds the dominant position in the African sports drinks market, followed by Nigeria and Kenya. This regional leadership is primarily attributed to robust economic growth in these countries, increased participation in sporting activities, and a larger consumer base. Analyzing market segments, PET Bottles emerge as the leading packaging type due to their cost-effectiveness and consumer convenience. Supermarket/Hypermarkets constitute the dominant distribution channel, followed by convenience stores. Isotonic drinks command the largest market share among soft drink types due to their perceived effectiveness in replenishing electrolytes lost during physical activity.

Key Drivers of Regional Dominance:

- South Africa: Strong economy, high sports participation rates, well-established distribution networks.

- Nigeria: Large and growing population, rising disposable incomes, increasing health awareness.

- Kenya: Expanding middle class, increasing urbanization, rising popularity of sports and fitness.

Dominant Segments:

- Packaging: PET Bottles

- Distribution: Supermarket/Hypermarket

- Soft Drink Type: Isotonic

Africa Sports Drinks Industry Product Developments

Recent product innovations have focused on enhancing the functional benefits of sports drinks, with a significant emphasis on low-sugar and electrolyte-enhanced formulations. The introduction of protein-based sports drinks is gaining traction, tapping into the growing health and fitness consciousness of consumers. Companies are also investing in innovative packaging solutions to enhance product shelf life and appeal. These developments demonstrate a keen focus on addressing consumer needs and preferences, emphasizing both taste and functionality.

Key Drivers of Africa Sports Drinks Industry Growth

Several factors fuel the growth of the Africa sports drinks market. Rising disposable incomes lead to increased spending on premium beverages. The expanding health and wellness sector drives demand for functional drinks, while government policies promoting sports and healthy lifestyles further encourage consumption. Technological advancements in packaging and distribution also create opportunities for increased market penetration.

Challenges in the Africa Sports Drinks Industry Market

The Africa sports drinks market faces several challenges, including fluctuating raw material prices impacting production costs. Supply chain inefficiencies can hinder distribution and availability, particularly in remote areas. Intense competition from established players and the emergence of new entrants creates price pressures and reduces profit margins. Regulatory hurdles and varying import/export policies add complexities to market operations. These challenges affect market growth at approximately xx% per year.

Emerging Opportunities in Africa Sports Drinks Industry

The burgeoning popularity of online retail platforms presents a significant opportunity to broaden market reach and access a wider consumer base, especially in urban areas. Strategic alliances and partnerships with sports organizations and fitness centers can significantly enhance brand visibility and accelerate market penetration. Exploring and developing new product categories, such as functional drinks enriched with added vitamins or antioxidants, offers promising avenues for expansion and diversification. A focus on developing sustainable and eco-friendly packaging solutions will also be a crucial driver of future growth and will appeal to increasingly environmentally conscious consumers.

Leading Players in the Africa Sports Drinks Industry Sector

- Kingsley Beverages Limited

- Aje Group

- Tiger Brands Ltd

- PepsiCo Inc

- Oshee Polska Sp Z O O

- Suntory Holdings Limited

- The Coca-Cola Company

- Thirsti Water (Pty) Ltd

- Ekhamanzi Springs (Pty) Ltd

- BOS Brands (Pty) Ltd

- Congo Brands

Key Milestones in Africa Sports Drinks Industry Industry

- May 2022: Thirsti Water (Pty) Ltd signs a three-year hydration deal with SuperSport United, boosting brand visibility.

- October 2022: Tiger Brands launches a "zero" sugar Energade variant, catering to health-conscious consumers.

- April 2023: Congo LLC invests USD 8.25 Million to relocate and expand its Louisville headquarters, creating 500 jobs—though this is outside Africa and its impact on the African market is indirect and potentially limited.

Strategic Outlook for Africa Sports Drinks Industry Market

The African sports drinks market exhibits substantial long-term growth potential. Strategic investments in product innovation, sustainable packaging practices, and the creation of efficient distribution networks are critical for effectively capitalizing on the market's opportunities. Expanding into new geographic regions and leveraging the burgeoning online retail sector are key strategic imperatives for achieving long-term success. A focused approach on health-conscious and functional beverage offerings will be a pivotal driver of future market growth and sustainability.

Africa Sports Drinks Industry Segmentation

-

1. Soft Drink Type

- 1.1. Electrolyte-Enhanced Water

- 1.2. Hypertonic

- 1.3. Hypotonic

- 1.4. Isotonic

- 1.5. Protein-based Sport Drinks

-

2. Packaging Type

- 2.1. Aseptic packages

- 2.2. Metal Can

- 2.3. PET Bottles

-

3. Sub Distribution Channel

- 3.1. Convenience Stores

- 3.2. Online Retail

- 3.3. Specialty Stores

- 3.4. Supermarket/Hypermarket

- 3.5. Others

Africa Sports Drinks Industry Segmentation By Geography

-

1. Africa

- 1.1. Nigeria

- 1.2. South Africa

- 1.3. Egypt

- 1.4. Kenya

- 1.5. Ethiopia

- 1.6. Morocco

- 1.7. Ghana

- 1.8. Algeria

- 1.9. Tanzania

- 1.10. Ivory Coast

Africa Sports Drinks Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 11.55% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Demand for Protein-Rich Food; Increasing Demand for Plant-Based and Organic Ingredients

- 3.3. Market Restrains

- 3.3.1. Presence of Counterfeit Products

- 3.4. Market Trends

- 3.4.1. OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Africa Sports Drinks Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Soft Drink Type

- 5.1.1. Electrolyte-Enhanced Water

- 5.1.2. Hypertonic

- 5.1.3. Hypotonic

- 5.1.4. Isotonic

- 5.1.5. Protein-based Sport Drinks

- 5.2. Market Analysis, Insights and Forecast - by Packaging Type

- 5.2.1. Aseptic packages

- 5.2.2. Metal Can

- 5.2.3. PET Bottles

- 5.3. Market Analysis, Insights and Forecast - by Sub Distribution Channel

- 5.3.1. Convenience Stores

- 5.3.2. Online Retail

- 5.3.3. Specialty Stores

- 5.3.4. Supermarket/Hypermarket

- 5.3.5. Others

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Africa

- 5.1. Market Analysis, Insights and Forecast - by Soft Drink Type

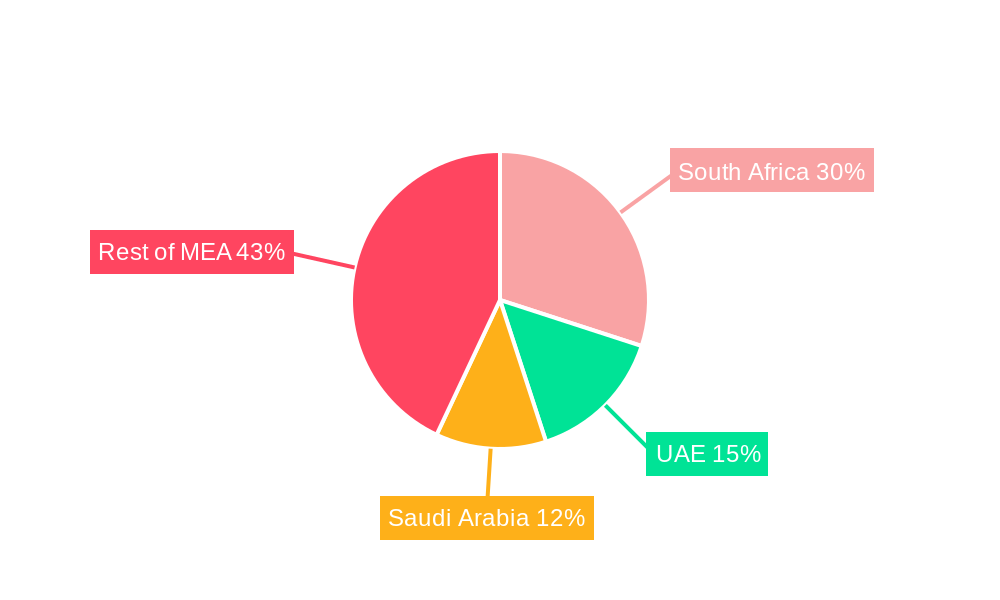

- 6. UAE Africa Sports Drinks Industry Analysis, Insights and Forecast, 2019-2031

- 7. South Africa Africa Sports Drinks Industry Analysis, Insights and Forecast, 2019-2031

- 8. Saudi Arabia Africa Sports Drinks Industry Analysis, Insights and Forecast, 2019-2031

- 9. Rest of MEA Africa Sports Drinks Industry Analysis, Insights and Forecast, 2019-2031

- 10. Competitive Analysis

- 10.1. Market Share Analysis 2024

- 10.2. Company Profiles

- 10.2.1 Kingsley Beverages Limited

- 10.2.1.1. Overview

- 10.2.1.2. Products

- 10.2.1.3. SWOT Analysis

- 10.2.1.4. Recent Developments

- 10.2.1.5. Financials (Based on Availability)

- 10.2.2 Aje Group

- 10.2.2.1. Overview

- 10.2.2.2. Products

- 10.2.2.3. SWOT Analysis

- 10.2.2.4. Recent Developments

- 10.2.2.5. Financials (Based on Availability)

- 10.2.3 Tiger Brands Ltd

- 10.2.3.1. Overview

- 10.2.3.2. Products

- 10.2.3.3. SWOT Analysis

- 10.2.3.4. Recent Developments

- 10.2.3.5. Financials (Based on Availability)

- 10.2.4 PepsiCo Inc

- 10.2.4.1. Overview

- 10.2.4.2. Products

- 10.2.4.3. SWOT Analysis

- 10.2.4.4. Recent Developments

- 10.2.4.5. Financials (Based on Availability)

- 10.2.5 Oshee Polska Sp Z O O

- 10.2.5.1. Overview

- 10.2.5.2. Products

- 10.2.5.3. SWOT Analysis

- 10.2.5.4. Recent Developments

- 10.2.5.5. Financials (Based on Availability)

- 10.2.6 Suntory Holdings Limited

- 10.2.6.1. Overview

- 10.2.6.2. Products

- 10.2.6.3. SWOT Analysis

- 10.2.6.4. Recent Developments

- 10.2.6.5. Financials (Based on Availability)

- 10.2.7 The Coca-Cola Company

- 10.2.7.1. Overview

- 10.2.7.2. Products

- 10.2.7.3. SWOT Analysis

- 10.2.7.4. Recent Developments

- 10.2.7.5. Financials (Based on Availability)

- 10.2.8 Thirsti Water (Pty) Ltd

- 10.2.8.1. Overview

- 10.2.8.2. Products

- 10.2.8.3. SWOT Analysis

- 10.2.8.4. Recent Developments

- 10.2.8.5. Financials (Based on Availability)

- 10.2.9 Ekhamanzi Springs (Pty) Ltd

- 10.2.9.1. Overview

- 10.2.9.2. Products

- 10.2.9.3. SWOT Analysis

- 10.2.9.4. Recent Developments

- 10.2.9.5. Financials (Based on Availability)

- 10.2.10 BOS Brands (Pty) Ltd

- 10.2.10.1. Overview

- 10.2.10.2. Products

- 10.2.10.3. SWOT Analysis

- 10.2.10.4. Recent Developments

- 10.2.10.5. Financials (Based on Availability)

- 10.2.11 Congo Brands

- 10.2.11.1. Overview

- 10.2.11.2. Products

- 10.2.11.3. SWOT Analysis

- 10.2.11.4. Recent Developments

- 10.2.11.5. Financials (Based on Availability)

- 10.2.1 Kingsley Beverages Limited

List of Figures

- Figure 1: Africa Sports Drinks Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Africa Sports Drinks Industry Share (%) by Company 2024

List of Tables

- Table 1: Africa Sports Drinks Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Africa Sports Drinks Industry Revenue Million Forecast, by Soft Drink Type 2019 & 2032

- Table 3: Africa Sports Drinks Industry Revenue Million Forecast, by Packaging Type 2019 & 2032

- Table 4: Africa Sports Drinks Industry Revenue Million Forecast, by Sub Distribution Channel 2019 & 2032

- Table 5: Africa Sports Drinks Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 6: Africa Sports Drinks Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 7: UAE Africa Sports Drinks Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: South Africa Africa Sports Drinks Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Saudi Arabia Africa Sports Drinks Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Rest of MEA Africa Sports Drinks Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Africa Sports Drinks Industry Revenue Million Forecast, by Soft Drink Type 2019 & 2032

- Table 12: Africa Sports Drinks Industry Revenue Million Forecast, by Packaging Type 2019 & 2032

- Table 13: Africa Sports Drinks Industry Revenue Million Forecast, by Sub Distribution Channel 2019 & 2032

- Table 14: Africa Sports Drinks Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 15: Nigeria Africa Sports Drinks Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: South Africa Africa Sports Drinks Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 17: Egypt Africa Sports Drinks Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: Kenya Africa Sports Drinks Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: Ethiopia Africa Sports Drinks Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Morocco Africa Sports Drinks Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 21: Ghana Africa Sports Drinks Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: Algeria Africa Sports Drinks Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: Tanzania Africa Sports Drinks Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: Ivory Coast Africa Sports Drinks Industry Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Africa Sports Drinks Industry?

The projected CAGR is approximately 11.55%.

2. Which companies are prominent players in the Africa Sports Drinks Industry?

Key companies in the market include Kingsley Beverages Limited, Aje Group, Tiger Brands Ltd, PepsiCo Inc, Oshee Polska Sp Z O O, Suntory Holdings Limited, The Coca-Cola Company, Thirsti Water (Pty) Ltd, Ekhamanzi Springs (Pty) Ltd, BOS Brands (Pty) Ltd, Congo Brands.

3. What are the main segments of the Africa Sports Drinks Industry?

The market segments include Soft Drink Type, Packaging Type, Sub Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Demand for Protein-Rich Food; Increasing Demand for Plant-Based and Organic Ingredients.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

Presence of Counterfeit Products.

8. Can you provide examples of recent developments in the market?

April 2023: Congo LLC to relocate, and expand Louisville headquarters with USD 8.25 million investment, creating 500 high-wage jobs. The company will relocate its Louisville headquarters to an existing 110,000-square-foot location at 13551 Triton Park Blvd., moving from its current 18,000-square-foot facility.October 2022: Tiger Brands also started producing a “zero” Energade variant, which is free from added sugar and contains very few calories. The product is available in the two classic flavors Lemon and Orange, in the practical 0.5L PET format.May 2022: To advertise its sports drinks, Thirsti Water (Pty) Ltd has expanded into football by signing a three-year hydration deal with SuperSport United.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Africa Sports Drinks Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Africa Sports Drinks Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Africa Sports Drinks Industry?

To stay informed about further developments, trends, and reports in the Africa Sports Drinks Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence