Key Insights

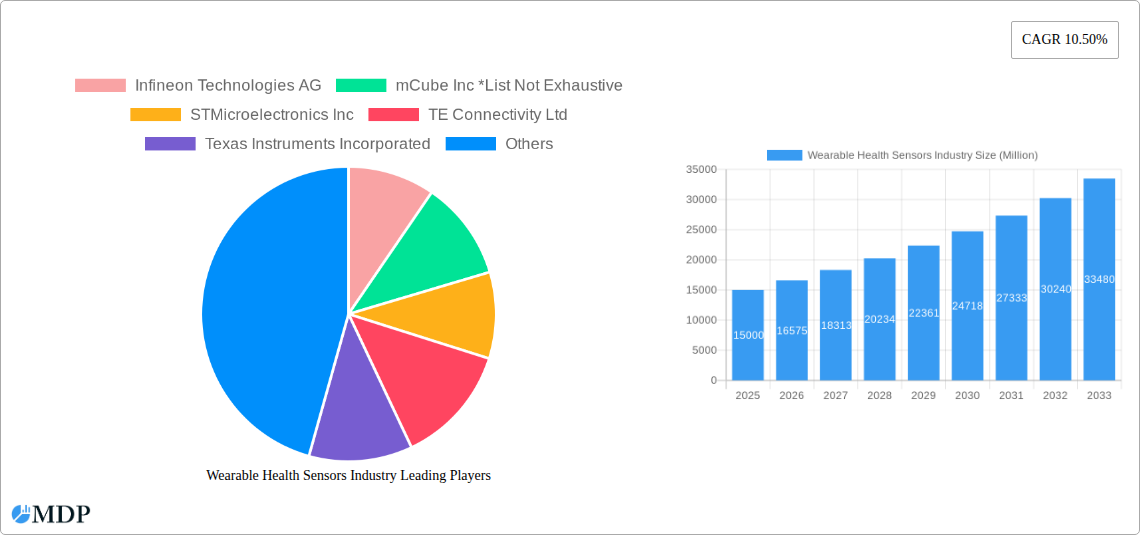

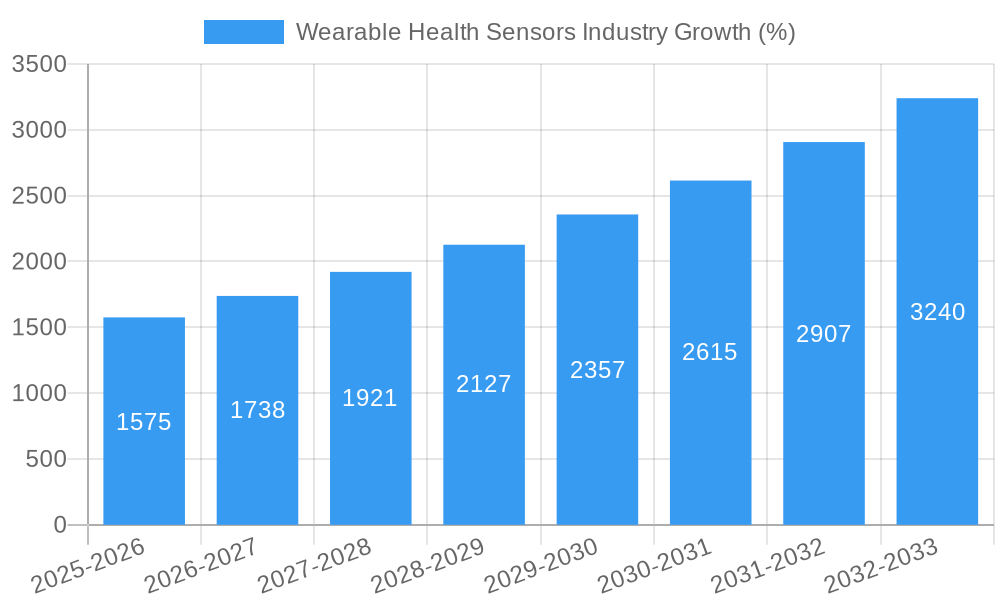

The Wearable Health Sensors market is experiencing robust growth, driven by the increasing prevalence of chronic diseases, a rising demand for remote patient monitoring, and the proliferation of sophisticated, yet affordable, wearable technology. The market, currently valued at approximately $XX million in 2025 (assuming a logical extrapolation based on the provided CAGR of 10.50% and a "XX" representing a substantial market size within the realm of medical technology), is projected to witness a Compound Annual Growth Rate (CAGR) of 10.50% from 2025 to 2033. This expansion is fueled by several key factors, including advancements in sensor miniaturization and power efficiency, leading to more comfortable and longer-lasting devices. The integration of advanced analytics and AI capabilities is enhancing the diagnostic accuracy and predictive potential of these sensors, further driving adoption within healthcare settings and personal wellness applications. Major market segments include pressure, temperature, and position sensors, with significant growth expected across healthcare, consumer electronics, and sports/fitness sectors. Companies such as Infineon Technologies, STMicroelectronics, and Texas Instruments are key players, constantly innovating to improve sensor performance and functionality.

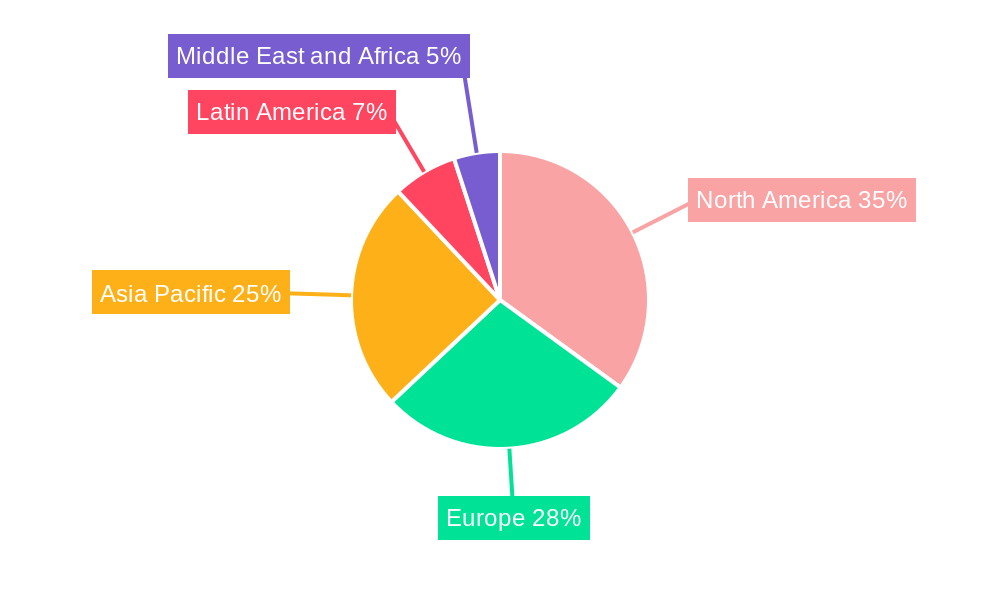

The restraints on market growth primarily involve challenges related to data privacy and security concerns surrounding the collection and transmission of sensitive health data. Regulatory hurdles in various regions also pose obstacles to market penetration. However, ongoing technological advancements in data encryption and anonymization techniques, coupled with the increasing clarity and standardization of regulations, are expected to mitigate these concerns over time. Future growth is strongly linked to the continuous development of more accurate, reliable, and user-friendly wearable health sensors, along with the integration of these sensors into broader connected healthcare ecosystems. The Asia-Pacific region, with its large and growing population and increasing healthcare expenditure, is anticipated to be a key growth driver in the coming years.

Wearable Health Sensors Market: A Comprehensive Report (2019-2033)

This in-depth report provides a comprehensive analysis of the Wearable Health Sensors market, offering invaluable insights for industry stakeholders, investors, and strategic decision-makers. The study covers the period from 2019 to 2033, with a focus on the 2025-2033 forecast period. We delve into market dynamics, leading players, technological advancements, and emerging trends to provide a clear picture of this rapidly evolving landscape. The market is segmented by type (Pressure Sensor, Temperature Sensor, Position Sensor, Other Types) and end-user industry (Healthcare, Consumer Electronics, Sports/Fitness, Other End User Industries). The report projects a market valued at xx Million by 2033, presenting a compelling opportunity for significant growth.

Wearable Health Sensors Industry Market Dynamics & Concentration

The Wearable Health Sensors market is experiencing robust growth, driven by several key factors. Market concentration is moderate, with several key players holding significant market share but no single entity dominating. The industry is characterized by ongoing innovation, particularly in miniaturization, power efficiency, and data analytics capabilities. Stringent regulatory frameworks, especially concerning data privacy and medical device approvals (e.g., FDA approvals), significantly influence market dynamics. Product substitutes, such as traditional medical monitoring devices, pose some competitive pressure, but the convenience and continuous monitoring capabilities of wearable sensors are driving adoption. End-user trends reflect a growing preference for personalized healthcare and remote patient monitoring, further fueling market growth.

Mergers and acquisitions (M&A) activity is relatively high. For example, in June 2022, Nitto Denko Corporation's acquisition of Bend Labs, Inc. (now Nitto Bend Technologies) demonstrated the industry's consolidation trend and the focus on integrating advanced sensor technologies. This reflects the strategic importance of acquiring cutting-edge sensor technology for expanding product portfolios and capabilities. The number of M&A deals in the past five years is estimated at xx. Key players are actively engaged in strategic partnerships and collaborations to enhance their product offerings and market reach. Market share is distributed among key players with top 5 companies holding approximately xx% of market share.

Wearable Health Sensors Industry Industry Trends & Analysis

The Wearable Health Sensors market exhibits a robust Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025-2033). This growth is primarily driven by technological advancements leading to smaller, more accurate, and energy-efficient sensors. The increasing demand for remote patient monitoring, particularly for chronic conditions like heart failure (as highlighted by Abbott's FDA approval in February 2022 for its Cardio MEMS HF System, adding 1.2 Million eligible patients), is a significant driver. Consumer preference for health and wellness tracking is also contributing significantly to market penetration. Increasing smartphone integration and the development of sophisticated data analytics platforms are changing the landscape, enabling better disease management and personalized health interventions. Competitive dynamics are marked by both collaboration and competition, with established players focusing on innovation and new product development alongside the emergence of innovative startups. Market penetration is projected to reach xx% by 2033, indicating substantial market expansion.

Leading Markets & Segments in Wearable Health Sensors Industry

The Healthcare segment dominates the end-user industry, representing xx% of the market in 2025. This is driven by the increasing demand for continuous health monitoring, remote diagnostics, and personalized medicine. The North American market holds the largest market share, currently at xx%, due to factors like high healthcare expenditure and technological advancements. This dominance is supported by:

- Strong regulatory support: The FDA's approval process, while stringent, provides a framework for innovation and market entry.

- High disposable income: A substantial portion of the population can afford advanced healthcare technology.

- Well-established healthcare infrastructure: Existing infrastructure facilitates the adoption and integration of new technologies.

Within the "By Type" segmentation, Pressure Sensors are currently the leading segment, holding xx% market share in 2025, due to their widespread applications in blood pressure and other vital sign monitoring. However, the "Other Types" category is expected to witness significant growth due to the development of advanced biosensors and novel sensor technologies.

Wearable Health Sensors Industry Product Developments

Recent product innovations focus on enhancing sensor accuracy, miniaturization, and power efficiency. Advanced materials, integrated circuits, and improved data processing algorithms are key technological drivers. New applications are emerging in areas such as sleep monitoring, mental health tracking, and early disease detection. Competitive advantages are increasingly based on data analytics capabilities, seamless integration with other healthcare systems, and the development of user-friendly interfaces. The market is witnessing a shift towards more sophisticated, integrated wearable health solutions.

Key Drivers of Wearable Health Sensors Industry Growth

Several factors contribute to the Wearable Health Sensors market's rapid growth. Technological advancements, such as the development of more accurate, smaller, and energy-efficient sensors, are paramount. Economic factors, including increasing healthcare expenditure and rising disposable incomes in developed and emerging economies, are also significant drivers. Favorable regulatory environments, such as the FDA's approval of new applications for existing sensors, accelerate market adoption. For example, the expanded indication for Abbott's Cardio MEMS HF system exemplifies the regulatory support driving market growth.

Challenges in the Wearable Health Sensors Industry Market

The industry faces several challenges. Strict regulatory hurdles and approval processes for medical devices can significantly delay product launches and increase costs. Supply chain disruptions and fluctuations in raw material prices can impact production and profitability. Intense competition among established players and emerging startups necessitates ongoing innovation and differentiation. Data security and privacy concerns also pose significant challenges. These factors, coupled with varying reimbursement policies in different healthcare systems, impose significant barriers to market entry and expansion.

Emerging Opportunities in Wearable Health Sensors Industry

Significant long-term growth opportunities exist in the development of advanced biosensors for continuous glucose monitoring, early cancer detection, and personalized drug delivery. Strategic partnerships between sensor manufacturers, healthcare providers, and data analytics companies can unlock new market segments. Expanding into emerging markets with large populations and growing healthcare needs presents a significant potential for market expansion. The development of AI-powered diagnostic tools leveraging data from wearable sensors will offer further growth opportunities.

Leading Players in the Wearable Health Sensors Industry Sector

- Infineon Technologies AG

- mCube Inc

- STMicroelectronics Inc

- TE Connectivity Ltd

- Texas Instruments Incorporated

- Arm Limited

- TDK Corporation

- Fraunhofer IIS

- Analog Devices Inc

- Maxim Integrated Products Inc

Key Milestones in Wearable Health Sensors Industry Industry

- June 2022: Nitto Denko Corporation acquired Bend Labs, Inc., forming Nitto Bend Technologies, leading to expanded sensor technology portfolios and new business opportunities.

- February 2022: Abbott received FDA approval for expanded use of its Cardio MEMS HF System, significantly increasing the addressable market for heart failure monitoring by 1.2 Million patients.

Strategic Outlook for Wearable Health Sensors Industry Market

The Wearable Health Sensors market is poised for sustained growth, driven by technological advancements, increasing demand for personalized healthcare, and the expansion of remote patient monitoring. Strategic opportunities lie in developing innovative sensor technologies, focusing on data analytics and AI integration, and forging strategic partnerships to expand market reach and develop comprehensive healthcare solutions. The market's future is bright, characterized by continuous innovation and the potential to transform healthcare delivery.

Wearable Health Sensors Industry Segmentation

-

1. Type

- 1.1. Pressure Sensor

- 1.2. Temperature Sensor

- 1.3. Position Sensor

- 1.4. Other Types

-

2. End User Industry

- 2.1. Healthcare

- 2.2. Consumer Electronic

- 2.3. Sports/Fitness

- 2.4. Other End User Industries

Wearable Health Sensors Industry Segmentation By Geography

- 1. Asia Pacific

- 2. Europe

- 3. Latin America

- 4. Middle East and Africa

- 5. North America

Wearable Health Sensors Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 10.50% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Need for Continuous Monitoring In Healthcare Services; Rising Growth toward Advanced Functions Sensors in Smart Gadgets; Miniaturization of Physiological Sensors

- 3.3. Market Restrains

- 3.3.1. Dearth of Common Standards and Interoperability Issues

- 3.4. Market Trends

- 3.4.1. Healthcare Industry Holds a Dominant Share in Wearable Health Sensors Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Wearable Health Sensors Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Pressure Sensor

- 5.1.2. Temperature Sensor

- 5.1.3. Position Sensor

- 5.1.4. Other Types

- 5.2. Market Analysis, Insights and Forecast - by End User Industry

- 5.2.1. Healthcare

- 5.2.2. Consumer Electronic

- 5.2.3. Sports/Fitness

- 5.2.4. Other End User Industries

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Asia Pacific

- 5.3.2. Europe

- 5.3.3. Latin America

- 5.3.4. Middle East and Africa

- 5.3.5. North America

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Asia Pacific Wearable Health Sensors Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Pressure Sensor

- 6.1.2. Temperature Sensor

- 6.1.3. Position Sensor

- 6.1.4. Other Types

- 6.2. Market Analysis, Insights and Forecast - by End User Industry

- 6.2.1. Healthcare

- 6.2.2. Consumer Electronic

- 6.2.3. Sports/Fitness

- 6.2.4. Other End User Industries

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Europe Wearable Health Sensors Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Pressure Sensor

- 7.1.2. Temperature Sensor

- 7.1.3. Position Sensor

- 7.1.4. Other Types

- 7.2. Market Analysis, Insights and Forecast - by End User Industry

- 7.2.1. Healthcare

- 7.2.2. Consumer Electronic

- 7.2.3. Sports/Fitness

- 7.2.4. Other End User Industries

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Latin America Wearable Health Sensors Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Pressure Sensor

- 8.1.2. Temperature Sensor

- 8.1.3. Position Sensor

- 8.1.4. Other Types

- 8.2. Market Analysis, Insights and Forecast - by End User Industry

- 8.2.1. Healthcare

- 8.2.2. Consumer Electronic

- 8.2.3. Sports/Fitness

- 8.2.4. Other End User Industries

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Middle East and Africa Wearable Health Sensors Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Pressure Sensor

- 9.1.2. Temperature Sensor

- 9.1.3. Position Sensor

- 9.1.4. Other Types

- 9.2. Market Analysis, Insights and Forecast - by End User Industry

- 9.2.1. Healthcare

- 9.2.2. Consumer Electronic

- 9.2.3. Sports/Fitness

- 9.2.4. Other End User Industries

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. North America Wearable Health Sensors Industry Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Type

- 10.1.1. Pressure Sensor

- 10.1.2. Temperature Sensor

- 10.1.3. Position Sensor

- 10.1.4. Other Types

- 10.2. Market Analysis, Insights and Forecast - by End User Industry

- 10.2.1. Healthcare

- 10.2.2. Consumer Electronic

- 10.2.3. Sports/Fitness

- 10.2.4. Other End User Industries

- 10.1. Market Analysis, Insights and Forecast - by Type

- 11. Asia Pacific Wearable Health Sensors Industry Analysis, Insights and Forecast, 2019-2031

- 11.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 11.1.1.

- 12. Europe Wearable Health Sensors Industry Analysis, Insights and Forecast, 2019-2031

- 12.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 12.1.1.

- 13. Latin America Wearable Health Sensors Industry Analysis, Insights and Forecast, 2019-2031

- 13.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 13.1.1.

- 14. Middle East and Africa Wearable Health Sensors Industry Analysis, Insights and Forecast, 2019-2031

- 14.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 14.1.1.

- 15. North America Wearable Health Sensors Industry Analysis, Insights and Forecast, 2019-2031

- 15.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 15.1.1.

- 16. Competitive Analysis

- 16.1. Global Market Share Analysis 2024

- 16.2. Company Profiles

- 16.2.1 Infineon Technologies AG

- 16.2.1.1. Overview

- 16.2.1.2. Products

- 16.2.1.3. SWOT Analysis

- 16.2.1.4. Recent Developments

- 16.2.1.5. Financials (Based on Availability)

- 16.2.2 mCube Inc *List Not Exhaustive

- 16.2.2.1. Overview

- 16.2.2.2. Products

- 16.2.2.3. SWOT Analysis

- 16.2.2.4. Recent Developments

- 16.2.2.5. Financials (Based on Availability)

- 16.2.3 STMicroelectronics Inc

- 16.2.3.1. Overview

- 16.2.3.2. Products

- 16.2.3.3. SWOT Analysis

- 16.2.3.4. Recent Developments

- 16.2.3.5. Financials (Based on Availability)

- 16.2.4 TE Connectivity Ltd

- 16.2.4.1. Overview

- 16.2.4.2. Products

- 16.2.4.3. SWOT Analysis

- 16.2.4.4. Recent Developments

- 16.2.4.5. Financials (Based on Availability)

- 16.2.5 Texas Instruments Incorporated

- 16.2.5.1. Overview

- 16.2.5.2. Products

- 16.2.5.3. SWOT Analysis

- 16.2.5.4. Recent Developments

- 16.2.5.5. Financials (Based on Availability)

- 16.2.6 Arm Limited

- 16.2.6.1. Overview

- 16.2.6.2. Products

- 16.2.6.3. SWOT Analysis

- 16.2.6.4. Recent Developments

- 16.2.6.5. Financials (Based on Availability)

- 16.2.7 TDK Corporation

- 16.2.7.1. Overview

- 16.2.7.2. Products

- 16.2.7.3. SWOT Analysis

- 16.2.7.4. Recent Developments

- 16.2.7.5. Financials (Based on Availability)

- 16.2.8 Fraunhofer IIS

- 16.2.8.1. Overview

- 16.2.8.2. Products

- 16.2.8.3. SWOT Analysis

- 16.2.8.4. Recent Developments

- 16.2.8.5. Financials (Based on Availability)

- 16.2.9 Analog Devices Inc

- 16.2.9.1. Overview

- 16.2.9.2. Products

- 16.2.9.3. SWOT Analysis

- 16.2.9.4. Recent Developments

- 16.2.9.5. Financials (Based on Availability)

- 16.2.10 Maxim Integrated Products Inc

- 16.2.10.1. Overview

- 16.2.10.2. Products

- 16.2.10.3. SWOT Analysis

- 16.2.10.4. Recent Developments

- 16.2.10.5. Financials (Based on Availability)

- 16.2.1 Infineon Technologies AG

List of Figures

- Figure 1: Global Wearable Health Sensors Industry Revenue Breakdown (Million, %) by Region 2024 & 2032

- Figure 2: Asia Pacific Wearable Health Sensors Industry Revenue (Million), by Country 2024 & 2032

- Figure 3: Asia Pacific Wearable Health Sensors Industry Revenue Share (%), by Country 2024 & 2032

- Figure 4: Europe Wearable Health Sensors Industry Revenue (Million), by Country 2024 & 2032

- Figure 5: Europe Wearable Health Sensors Industry Revenue Share (%), by Country 2024 & 2032

- Figure 6: Latin America Wearable Health Sensors Industry Revenue (Million), by Country 2024 & 2032

- Figure 7: Latin America Wearable Health Sensors Industry Revenue Share (%), by Country 2024 & 2032

- Figure 8: Middle East and Africa Wearable Health Sensors Industry Revenue (Million), by Country 2024 & 2032

- Figure 9: Middle East and Africa Wearable Health Sensors Industry Revenue Share (%), by Country 2024 & 2032

- Figure 10: North America Wearable Health Sensors Industry Revenue (Million), by Country 2024 & 2032

- Figure 11: North America Wearable Health Sensors Industry Revenue Share (%), by Country 2024 & 2032

- Figure 12: Asia Pacific Wearable Health Sensors Industry Revenue (Million), by Type 2024 & 2032

- Figure 13: Asia Pacific Wearable Health Sensors Industry Revenue Share (%), by Type 2024 & 2032

- Figure 14: Asia Pacific Wearable Health Sensors Industry Revenue (Million), by End User Industry 2024 & 2032

- Figure 15: Asia Pacific Wearable Health Sensors Industry Revenue Share (%), by End User Industry 2024 & 2032

- Figure 16: Asia Pacific Wearable Health Sensors Industry Revenue (Million), by Country 2024 & 2032

- Figure 17: Asia Pacific Wearable Health Sensors Industry Revenue Share (%), by Country 2024 & 2032

- Figure 18: Europe Wearable Health Sensors Industry Revenue (Million), by Type 2024 & 2032

- Figure 19: Europe Wearable Health Sensors Industry Revenue Share (%), by Type 2024 & 2032

- Figure 20: Europe Wearable Health Sensors Industry Revenue (Million), by End User Industry 2024 & 2032

- Figure 21: Europe Wearable Health Sensors Industry Revenue Share (%), by End User Industry 2024 & 2032

- Figure 22: Europe Wearable Health Sensors Industry Revenue (Million), by Country 2024 & 2032

- Figure 23: Europe Wearable Health Sensors Industry Revenue Share (%), by Country 2024 & 2032

- Figure 24: Latin America Wearable Health Sensors Industry Revenue (Million), by Type 2024 & 2032

- Figure 25: Latin America Wearable Health Sensors Industry Revenue Share (%), by Type 2024 & 2032

- Figure 26: Latin America Wearable Health Sensors Industry Revenue (Million), by End User Industry 2024 & 2032

- Figure 27: Latin America Wearable Health Sensors Industry Revenue Share (%), by End User Industry 2024 & 2032

- Figure 28: Latin America Wearable Health Sensors Industry Revenue (Million), by Country 2024 & 2032

- Figure 29: Latin America Wearable Health Sensors Industry Revenue Share (%), by Country 2024 & 2032

- Figure 30: Middle East and Africa Wearable Health Sensors Industry Revenue (Million), by Type 2024 & 2032

- Figure 31: Middle East and Africa Wearable Health Sensors Industry Revenue Share (%), by Type 2024 & 2032

- Figure 32: Middle East and Africa Wearable Health Sensors Industry Revenue (Million), by End User Industry 2024 & 2032

- Figure 33: Middle East and Africa Wearable Health Sensors Industry Revenue Share (%), by End User Industry 2024 & 2032

- Figure 34: Middle East and Africa Wearable Health Sensors Industry Revenue (Million), by Country 2024 & 2032

- Figure 35: Middle East and Africa Wearable Health Sensors Industry Revenue Share (%), by Country 2024 & 2032

- Figure 36: North America Wearable Health Sensors Industry Revenue (Million), by Type 2024 & 2032

- Figure 37: North America Wearable Health Sensors Industry Revenue Share (%), by Type 2024 & 2032

- Figure 38: North America Wearable Health Sensors Industry Revenue (Million), by End User Industry 2024 & 2032

- Figure 39: North America Wearable Health Sensors Industry Revenue Share (%), by End User Industry 2024 & 2032

- Figure 40: North America Wearable Health Sensors Industry Revenue (Million), by Country 2024 & 2032

- Figure 41: North America Wearable Health Sensors Industry Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Wearable Health Sensors Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Global Wearable Health Sensors Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 3: Global Wearable Health Sensors Industry Revenue Million Forecast, by End User Industry 2019 & 2032

- Table 4: Global Wearable Health Sensors Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: Global Wearable Health Sensors Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: Wearable Health Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: Global Wearable Health Sensors Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 8: Wearable Health Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Global Wearable Health Sensors Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 10: Wearable Health Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Global Wearable Health Sensors Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 12: Wearable Health Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Global Wearable Health Sensors Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 14: Wearable Health Sensors Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 15: Global Wearable Health Sensors Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 16: Global Wearable Health Sensors Industry Revenue Million Forecast, by End User Industry 2019 & 2032

- Table 17: Global Wearable Health Sensors Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 18: Global Wearable Health Sensors Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 19: Global Wearable Health Sensors Industry Revenue Million Forecast, by End User Industry 2019 & 2032

- Table 20: Global Wearable Health Sensors Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 21: Global Wearable Health Sensors Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 22: Global Wearable Health Sensors Industry Revenue Million Forecast, by End User Industry 2019 & 2032

- Table 23: Global Wearable Health Sensors Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 24: Global Wearable Health Sensors Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 25: Global Wearable Health Sensors Industry Revenue Million Forecast, by End User Industry 2019 & 2032

- Table 26: Global Wearable Health Sensors Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 27: Global Wearable Health Sensors Industry Revenue Million Forecast, by Type 2019 & 2032

- Table 28: Global Wearable Health Sensors Industry Revenue Million Forecast, by End User Industry 2019 & 2032

- Table 29: Global Wearable Health Sensors Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Wearable Health Sensors Industry?

The projected CAGR is approximately 10.50%.

2. Which companies are prominent players in the Wearable Health Sensors Industry?

Key companies in the market include Infineon Technologies AG, mCube Inc *List Not Exhaustive, STMicroelectronics Inc, TE Connectivity Ltd, Texas Instruments Incorporated, Arm Limited, TDK Corporation, Fraunhofer IIS, Analog Devices Inc, Maxim Integrated Products Inc.

3. What are the main segments of the Wearable Health Sensors Industry?

The market segments include Type, End User Industry.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Need for Continuous Monitoring In Healthcare Services; Rising Growth toward Advanced Functions Sensors in Smart Gadgets; Miniaturization of Physiological Sensors.

6. What are the notable trends driving market growth?

Healthcare Industry Holds a Dominant Share in Wearable Health Sensors Market.

7. Are there any restraints impacting market growth?

Dearth of Common Standards and Interoperability Issues.

8. Can you provide examples of recent developments in the market?

June 2022 : Nitto Denko Corporation agreed to acquire Bend Labs, Inc. In line with this acquisition, Bend merged into the Nitto Group from June 1, 2022 to continue its business operations as Nitto Bend Technologies. As a result of this merger agreement, Bend's sensor device technologies were combined with Nitto's strengths for developing a next-generation technologies and products portfolio and new businesses utilizing sensor-acquired data.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Wearable Health Sensors Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Wearable Health Sensors Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Wearable Health Sensors Industry?

To stay informed about further developments, trends, and reports in the Wearable Health Sensors Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence