Key Insights

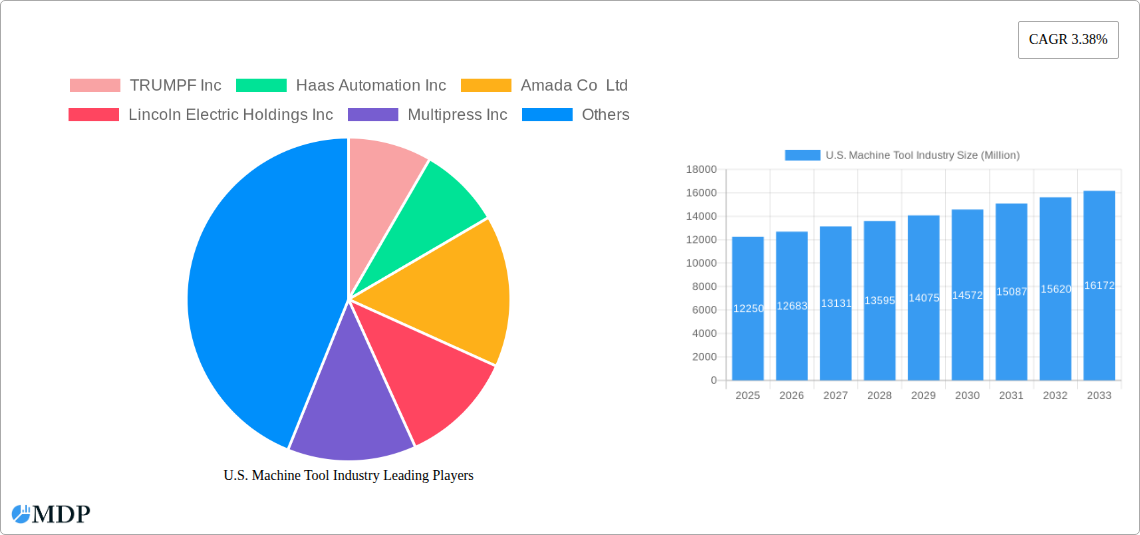

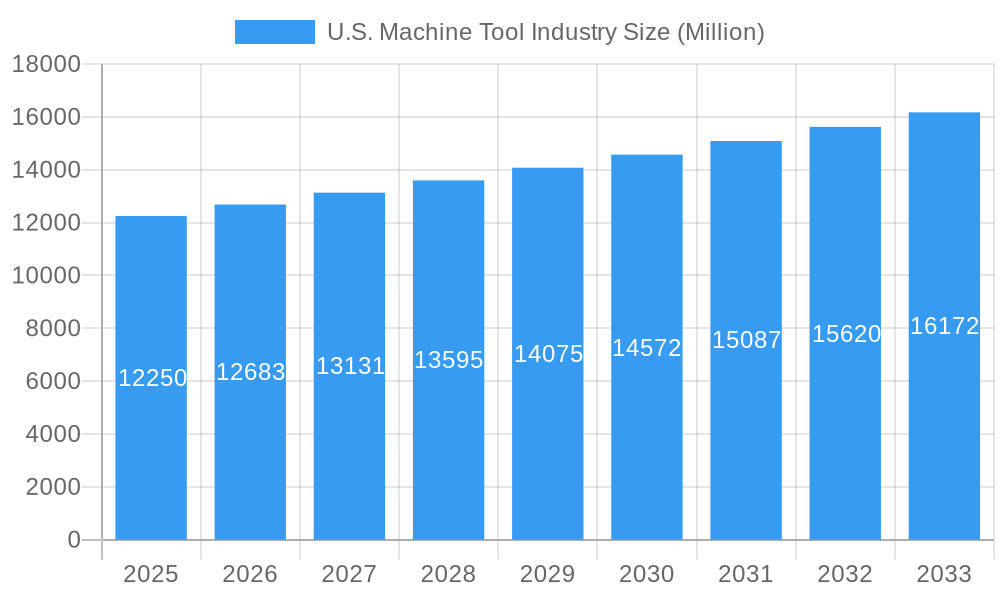

The U.S. machine tool industry, valued at $12.25 billion in 2025, is projected to experience steady growth, driven by increasing automation in manufacturing, reshoring initiatives, and the expansion of key sectors like automotive, aerospace, and energy. A Compound Annual Growth Rate (CAGR) of 3.38% from 2025 to 2033 suggests a continued, albeit moderate, expansion of the market. Key drivers include advancements in technology, such as the adoption of Industry 4.0 technologies (including AI and IoT integration in machine tools), leading to improved productivity and efficiency. Furthermore, government initiatives promoting domestic manufacturing and investment in advanced manufacturing technologies are fueling demand. However, factors like economic fluctuations, supply chain disruptions, and skilled labor shortages could potentially restrain growth. The industry is segmented by machine type (e.g., CNC machines, milling machines, lathes), application (e.g., metal cutting, metal forming), and end-user industry. Leading players, including TRUMPF Inc, Haas Automation Inc, and Amada Co Ltd, are actively investing in research and development to maintain their competitive edge through innovation and technological advancements. The competitive landscape is characterized by both established players and specialized niche manufacturers.

U.S. Machine Tool Industry Market Size (In Billion)

Looking ahead to 2033, the continued adoption of advanced manufacturing techniques, including additive manufacturing and digital twins, will likely reshape the market landscape. The focus will shift towards more flexible and adaptable machine tools capable of handling smaller batch sizes and customized production runs. The industry’s success will depend on effectively navigating the challenges of talent acquisition and retention, while simultaneously capitalizing on technological breakthroughs and the growing demand for precision and efficiency in manufacturing. This necessitates strategic investments in workforce training and collaboration between industry stakeholders to ensure the continued competitiveness of the U.S. machine tool sector. Specific regional variations in growth may exist, reflecting the concentration of manufacturing activities and industrial hubs across the country.

U.S. Machine Tool Industry Company Market Share

U.S. Machine Tool Industry Market Report: 2019-2033

Dive deep into the comprehensive analysis of the U.S. Machine Tool Industry, covering market dynamics, trends, leading players, and future projections (2019-2033). This report provides actionable insights for stakeholders, investors, and industry professionals.

Study Period: 2019–2033 Base Year: 2025 Estimated Year: 2025 Forecast Period: 2025–2033 Historical Period: 2019–2024

U.S. Machine Tool Industry Market Dynamics & Concentration

The U.S. machine tool industry is a dynamic and evolving sector, characterized by a vibrant mix of established global players and agile, specialized small to medium-sized enterprises (SMEs). This section delves into the competitive landscape, examining market concentration, the key drivers fueling innovation, the influence of regulatory frameworks, and the overarching market dynamics shaping its trajectory. While the market share remains somewhat fragmented, with no single entity dominating, a select group of influential companies plays a pivotal role in shaping industry trends and technological advancements. The estimated market size for the U.S. machine tool industry in 2025 is projected to reach **$XX Million**, reflecting ongoing growth and investment.

- Market Concentration: The market exhibits moderate fragmentation, with the top 5 players anticipated to hold approximately **XX%** of the market share by 2025. This indicates a competitive environment where strategic acquisitions and technological differentiation are key to capturing market share.

- Innovation Drivers: The industry is experiencing a significant surge in innovation, propelled by the relentless pursuit of increased efficiency, precision, and flexibility. Key drivers include the widespread adoption of automation and robotics, the integration of Artificial Intelligence (AI) for smarter manufacturing processes, the development and application of advanced materials, and the transformative potential of Industry 4.0 technologies, including the Industrial Internet of Things (IIoT) and digital twins.

- Regulatory Frameworks: A robust and evolving regulatory landscape significantly influences manufacturing processes and product development. Compliance with stringent safety standards, environmental regulations (such as emissions controls and waste management), and evolving trade policies are critical considerations for all industry participants.

- Product Substitutes and Complementary Technologies: While traditional machining technologies remain foundational, emerging disruptive forces are reshaping the competitive panorama. 3D printing and additive manufacturing technologies are not only presenting challenges to conventional methods but are also increasingly being integrated as complementary solutions, offering new possibilities for prototyping, complex part production, and customized manufacturing.

- End-User Trends: The demand for advanced machine tools is significantly influenced by the growth and technological advancements within key end-user sectors. The automotive industry, with its ongoing shift towards electric vehicles and sophisticated manufacturing techniques, continues to be a major driver. The aerospace sector, demanding high-precision components and advanced materials, also represents a critical market. Furthermore, the expanding renewable energy sector, particularly in areas like wind turbine manufacturing and solar panel production, is creating new avenues for demand.

- M&A Activities: The period between 2019 and 2024 has seen a notable increase in Merger and Acquisition (M&A) activities, signaling a trend towards industry consolidation and strategic expansion. These deals often involve established players acquiring innovative startups or complementary businesses to enhance their product portfolios, technological capabilities, and market reach. For instance, the acquisition of Peterson Tool Company by Sandvik in July 2022 exemplifies a significant consolidation move, aimed at strengthening Sandvik's position in specialized tooling.

U.S. Machine Tool Industry Industry Trends & Analysis

The U.S. machine tool industry exhibits a dynamic growth trajectory, driven by several key factors. Technological advancements, evolving consumer preferences, and intense competition shape the industry landscape. The industry is expected to experience a CAGR of xx% during the forecast period (2025-2033). Market penetration of advanced technologies like CNC machines and robotic automation continues to increase, reaching an estimated xx% in 2025.

- Market Growth Drivers: Increased automation, reshoring of manufacturing activities, and rising demand across diverse end-use sectors are driving the market's expansion.

- Technological Disruptions: The adoption of AI, IoT, and digital twins is revolutionizing manufacturing processes and improving efficiency.

- Consumer Preferences: Demand for high-precision, high-speed, and energy-efficient machines is shaping product development.

- Competitive Dynamics: Intense competition drives innovation and fosters the development of cutting-edge technologies.

Leading Markets & Segments in U.S. Machine Tool Industry

The U.S. machine tool industry exhibits a geographically diverse market, with distinct regional variations in market size, growth potential, and technological adoption. Currently, the Midwest region stands out as a leading hub, largely due to its deeply entrenched and robust manufacturing base. This regional dominance is further bolstered by a combination of well-established industrial infrastructure, a readily available pool of skilled labor, and a supportive ecosystem of government policies and incentives designed to foster manufacturing growth.

- Key Drivers of Midwest Dominance:

- Established Industrial Infrastructure: The region boasts a long history of manufacturing, resulting in a mature and well-developed infrastructure that supports efficient production and supply chains.

- Concentration of Automotive and Aerospace Manufacturing: The significant presence of major automotive and aerospace companies in the Midwest creates a consistent and substantial demand for advanced machine tools and related services.

- Presence of Skilled Workforce: A deep-rooted tradition of manufacturing has cultivated a highly skilled and experienced workforce, essential for operating and maintaining sophisticated machinery.

- Supportive State and Local Government Policies: Numerous state and local governments in the Midwest have implemented favorable policies, tax incentives, and workforce development programs to attract and retain manufacturing businesses.

Within the broader market, the automotive segment continues to represent the largest end-use market for machine tools, followed closely by the aerospace and energy sectors. The growth and evolving technological demands of these key sectors have a direct and profound impact on the overall demand for machine tools, driving innovation and investment across the industry.

U.S. Machine Tool Industry Product Developments

Recent years have witnessed significant advancements in machine tool technology. Innovations include the integration of AI-powered predictive maintenance, improved automation features, and the development of more sustainable and energy-efficient machines. These advancements enhance precision, speed, and overall manufacturing efficiency. The development of hybrid and multi-functional machines is another important trend, enhancing flexibility and reducing the overall footprint of manufacturing operations.

Key Drivers of U.S. Machine Tool Industry Growth

Several factors fuel the growth of the U.S. machine tool industry. Government incentives for manufacturing automation, increased investments in infrastructure, and technological advancements contribute significantly. The growing adoption of Industry 4.0 principles enhances productivity and efficiency.

- Technological Advancements: Automation, AI, and digitalization improve efficiency and productivity.

- Economic Factors: Government investment in infrastructure and reshoring initiatives stimulate demand.

- Regulatory Factors: Incentives and tax benefits encourage investment in advanced technologies.

Challenges in the U.S. Machine Tool Industry Market

The industry faces several challenges, including supply chain disruptions, skilled labor shortages, and intense global competition. These factors impact production costs and profitability. For instance, supply chain disruptions related to the pandemic caused significant delays and cost increases in 2020-2022, impacting the industry by approximately $xx Million.

- Supply Chain Issues: Global supply chain vulnerabilities impact the availability of components.

- Skilled Labor Shortages: A lack of skilled workers hinders the industry's growth.

- Competitive Pressures: Global competition from low-cost manufacturers puts pressure on pricing.

Emerging Opportunities in U.S. Machine Tool Industry

Notwithstanding existing challenges, the U.S. machine tool industry is ripe with opportunities for sustained growth and innovation. A significant avenue lies in the seamless integration of additive manufacturing (3D printing) technologies into existing subtractive machining operations, creating hybrid manufacturing solutions that offer unparalleled design freedom and material efficiency. Expansion into burgeoning new markets, such as the rapidly growing renewable energy sector, presents substantial potential for specialized tooling and automated manufacturing solutions. Furthermore, forging strategic partnerships and collaborative ventures focused on pioneering technological advancements, such as AI-driven process optimization and the development of next-generation smart machine tools, will be crucial for future success. The development and provision of highly customized machine tools, precisely engineered to meet the unique and demanding requirements of specific industry applications, represents another highly lucrative and expanding niche within the market.

Leading Players in the U.S. Machine Tool Industry Sector

- TRUMPF Inc

- Haas Automation Inc

- Amada Co Ltd

- Lincoln Electric Holdings Inc

- Multipress Inc

- MITUSA Inc

- MC Machinery Systems Inc

- Mate Precision Tooling Inc

- Bystronic Inc

- Laser Mechanisms Inc

- Koike Aronson Inc /Ransome

- FENN Metal Forming Machinery Solutions

- Cincinnati Inc (List Not Exhaustive)

Key Milestones in U.S. Machine Tool Industry Industry

- July 2022: Sandvik acquires Peterson Tool Company, expanding its tooling portfolio and strengthening its position in the market.

- June 2022: Doosan Machine Tools rebrands as DN Solutions, signifying a strategic shift towards comprehensive manufacturing solutions.

Strategic Outlook for U.S. Machine Tool Industry Market

The U.S. machine tool industry is strategically positioned for robust and sustained growth in the coming years. This expansion will be fueled by continuous technological innovation, including advancements in automation, AI, and digital manufacturing, alongside increasing demand from pivotal sectors like automotive, aerospace, and renewable energy. To thrive in this evolving landscape, companies must prioritize strategic partnerships, significant investment in cutting-edge automation and smart manufacturing technologies, and a strong commitment to sustainable manufacturing practices. The industry's long-term success will hinge on its ability to adapt proactively to technological disruptions, effectively address evolving workforce needs and skill gaps, and skillfully navigate the complexities of global supply chain dynamics. The projected market size for the U.S. machine tool industry in 2033 is estimated to reach **$XX Million**, indicating a promising future driven by innovation and market demand.

U.S. Machine Tool Industry Segmentation

-

1. Type

- 1.1. Metalworking Machines

- 1.2. Parts and Accessories

- 1.3. Installation

- 1.4. Repair

- 1.5. Maintenance

-

2. End User

- 2.1. Automotive

- 2.2. Fabrication and Industrial Machinery Manufacturing

- 2.3. Marine, Aerospace & Defense

- 2.4. Precision Engineering

- 2.5. Other End Users

U.S. Machine Tool Industry Segmentation By Geography

- 1. U.S.

U.S. Machine Tool Industry Regional Market Share

Geographic Coverage of U.S. Machine Tool Industry

U.S. Machine Tool Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 3.38% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Metalworking Machines

- 5.1.2. Parts and Accessories

- 5.1.3. Installation

- 5.1.4. Repair

- 5.1.5. Maintenance

- 5.2. Market Analysis, Insights and Forecast - by End User

- 5.2.1. Automotive

- 5.2.2. Fabrication and Industrial Machinery Manufacturing

- 5.2.3. Marine, Aerospace & Defense

- 5.2.4. Precision Engineering

- 5.2.5. Other End Users

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. U.S.

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. U.S. Machine Tool Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Metalworking Machines

- 6.1.2. Parts and Accessories

- 6.1.3. Installation

- 6.1.4. Repair

- 6.1.5. Maintenance

- 6.2. Market Analysis, Insights and Forecast - by End User

- 6.2.1. Automotive

- 6.2.2. Fabrication and Industrial Machinery Manufacturing

- 6.2.3. Marine, Aerospace & Defense

- 6.2.4. Precision Engineering

- 6.2.5. Other End Users

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 TRUMPF Inc

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Haas Automation Inc

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Amada Co Ltd

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 Lincoln Electric Holdings Inc

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Multipress Inc

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 MITUSA Inc

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 MC Machinery Systems Inc

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Mate Precision Tooling Inc

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Bystronic Inc

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Laser Mechanisms Inc

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.11 Koike Aronson Inc /Ransome

- 7.1.11.1. Company Overview

- 7.1.11.2. Products

- 7.1.11.3. Company Financials

- 7.1.11.4. SWOT Analysis

- 7.1.12 FENN Metal Forming Machinery Solutions

- 7.1.12.1. Company Overview

- 7.1.12.2. Products

- 7.1.12.3. Company Financials

- 7.1.12.4. SWOT Analysis

- 7.1.13 Cincinnati Inc **List Not Exhaustive

- 7.1.13.1. Company Overview

- 7.1.13.2. Products

- 7.1.13.3. Company Financials

- 7.1.13.4. SWOT Analysis

- 7.1.1 TRUMPF Inc

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: U.S. Machine Tool Industry Revenue Breakdown (Million, %) by Product 2025 & 2033

- Figure 2: U.S. Machine Tool Industry Share (%) by Company 2025

List of Tables

- Table 1: U.S. Machine Tool Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 2: U.S. Machine Tool Industry Volume Billion Forecast, by Type 2020 & 2033

- Table 3: U.S. Machine Tool Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 4: U.S. Machine Tool Industry Volume Billion Forecast, by End User 2020 & 2033

- Table 5: U.S. Machine Tool Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 6: U.S. Machine Tool Industry Volume Billion Forecast, by Region 2020 & 2033

- Table 7: U.S. Machine Tool Industry Revenue Million Forecast, by Type 2020 & 2033

- Table 8: U.S. Machine Tool Industry Volume Billion Forecast, by Type 2020 & 2033

- Table 9: U.S. Machine Tool Industry Revenue Million Forecast, by End User 2020 & 2033

- Table 10: U.S. Machine Tool Industry Volume Billion Forecast, by End User 2020 & 2033

- Table 11: U.S. Machine Tool Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 12: U.S. Machine Tool Industry Volume Billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the U.S. Machine Tool Industry?

The projected CAGR is approximately 3.38%.

2. Which companies are prominent players in the U.S. Machine Tool Industry?

Key companies in the market include TRUMPF Inc, Haas Automation Inc, Amada Co Ltd, Lincoln Electric Holdings Inc, Multipress Inc, MITUSA Inc, MC Machinery Systems Inc, Mate Precision Tooling Inc, Bystronic Inc, Laser Mechanisms Inc, Koike Aronson Inc /Ransome, FENN Metal Forming Machinery Solutions, Cincinnati Inc **List Not Exhaustive.

3. What are the main segments of the U.S. Machine Tool Industry?

The market segments include Type, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD 12.25 Million as of 2022.

5. What are some drivers contributing to market growth?

N/A

6. What are the notable trends driving market growth?

Increasing demand for domestic machine tools driving the market.

7. Are there any restraints impacting market growth?

N/A

8. Can you provide examples of recent developments in the market?

July 2022: Peterson Tool Company, Inc. ("PTC"), a leading provider of machine-specific custom insert tooling solutions, had the previously announced finalized acquisition of its assets by Sandvik. Custom carbide form inserts are part of the product line and are used mainly in the general engineering and automotive industries for high-production turning and grooving applications. The operation will be referred to as Walter's GWS Tool division, which is a part of the Sandvik Manufacturing and Machining Solutions business area.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in Billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "U.S. Machine Tool Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the U.S. Machine Tool Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the U.S. Machine Tool Industry?

To stay informed about further developments, trends, and reports in the U.S. Machine Tool Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence