Key Insights

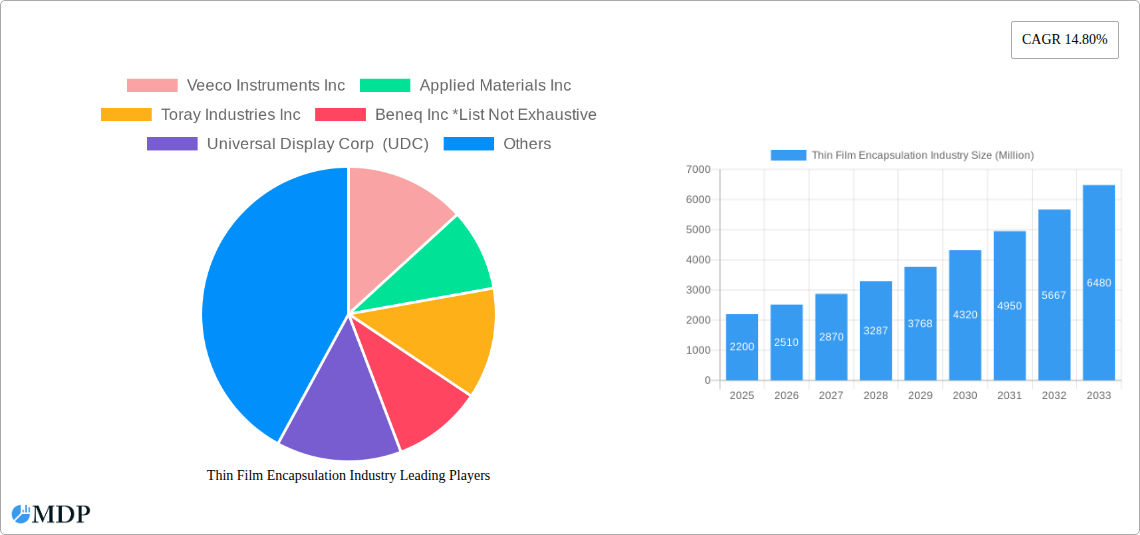

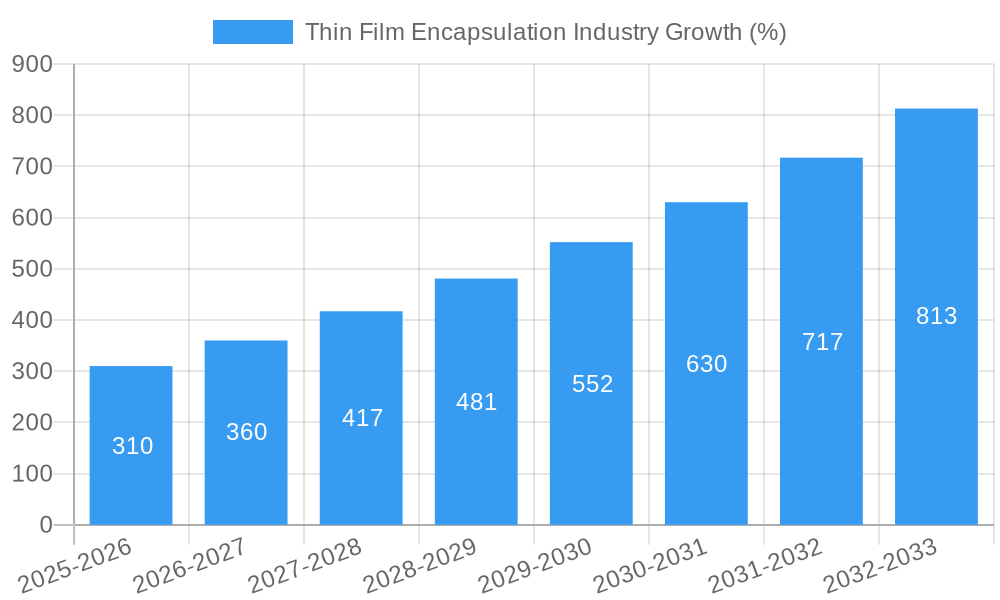

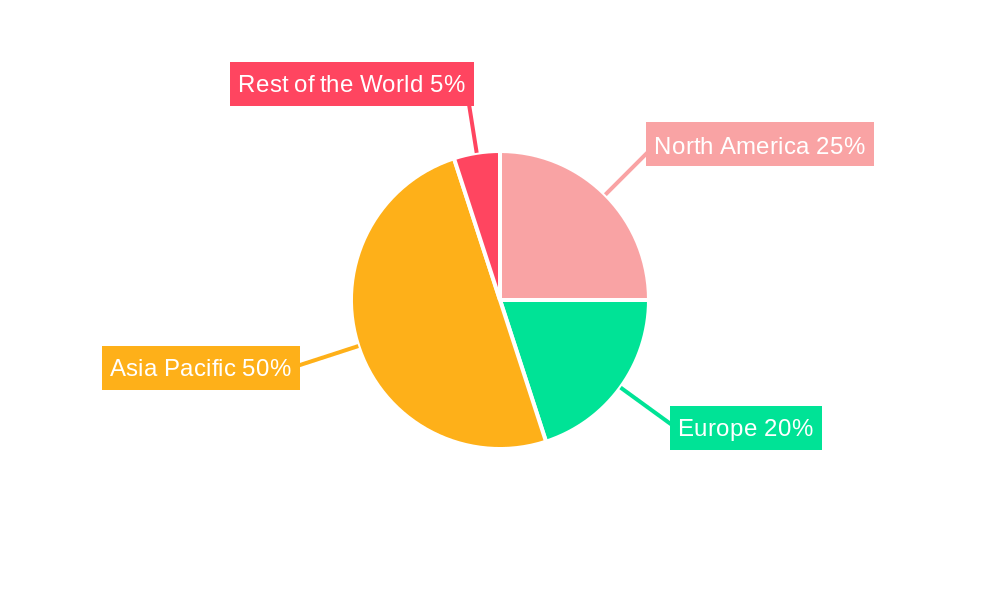

The thin film encapsulation (TFE) market is experiencing robust growth, driven by the increasing demand for flexible electronics and advancements in display technologies. The market's Compound Annual Growth Rate (CAGR) of 14.80% from 2019 to 2024 indicates a significant upward trajectory. This expansion is fueled primarily by the burgeoning flexible OLED display market, which requires advanced encapsulation techniques to protect delicate organic layers from environmental factors like moisture and oxygen. Further driving growth are applications in thin-film photovoltaics (flexible solar cells), where TFE protects solar cells from degradation, enhancing their efficiency and lifespan. The adoption of innovative technologies like plasma-enhanced chemical vapor deposition (PECVD) and atomic layer deposition (ALD) is improving the quality and performance of TFE materials, making them increasingly cost-effective and commercially viable. While challenges such as maintaining high yields in manufacturing processes and addressing the long-term reliability of encapsulated devices remain, ongoing R&D efforts focused on material science and process optimization are expected to mitigate these constraints. Major players like Veeco Instruments, Applied Materials, and Toray Industries are leading innovation and shaping market dynamics through their advanced TFE solutions and strategic partnerships. The Asia-Pacific region, particularly driven by high manufacturing activity in South Korea and China, is expected to dominate market share due to robust demand from electronics manufacturing hubs.

The segmentation within the TFE market highlights further growth opportunities. Flexible OLED displays are currently the largest application segment, but the thin-film photovoltaics segment is expected to witness significant growth due to the increasing emphasis on renewable energy sources and the growing adoption of flexible solar panels. Technological advancements are also influencing the market. PECVD and ALD are currently leading in terms of market adoption, but inkjet printing is gaining traction due to its cost-effectiveness and suitability for large-scale production of flexible devices. While the precise market size in 2025 is not provided, considering the 14.80% CAGR and assuming a reasonable starting point, a market value exceeding $2 Billion in 2025 is a plausible estimate, with a projected continued substantial growth throughout the forecast period to 2033. Competitive landscape analysis suggests that existing companies are focusing on strategic acquisitions, partnerships, and technological innovations to maintain their market positions and capture increasing market share.

Thin Film Encapsulation (TFE) Industry Report: 2019-2033

This comprehensive report provides an in-depth analysis of the Thin Film Encapsulation (TFE) industry, offering invaluable insights for stakeholders seeking to navigate this dynamic market. Covering the period from 2019 to 2033, with a base year of 2025 and a forecast period of 2025-2033, this report delves into market dynamics, technological advancements, leading players, and future growth opportunities. The market is projected to reach xx Million by 2033, exhibiting a significant CAGR of xx% during the forecast period.

Thin Film Encapsulation Industry Market Dynamics & Concentration

The Thin Film Encapsulation (TFE) market is characterized by a moderately concentrated landscape, with key players such as Veeco Instruments Inc, Applied Materials Inc, Toray Industries Inc, and Beneq Inc holding significant market share. However, the presence of several smaller, specialized firms fosters innovation and competition. The market share of the top five players is estimated at xx%, indicating opportunities for both established and emerging companies.

Several factors drive innovation within the TFE industry. The increasing demand for flexible displays in consumer electronics, coupled with advancements in materials science and deposition techniques, fuels the development of novel TFE solutions. Stringent regulatory frameworks regarding environmental impact and material safety influence product development and manufacturing processes. The emergence of alternative encapsulation technologies, such as advanced polymer-based solutions, presents both challenges and opportunities.

End-user trends toward lighter, more flexible, and energy-efficient devices are significantly impacting market demand. Mergers and acquisitions (M&A) activities are increasingly common, as larger companies seek to consolidate their market position and gain access to new technologies or geographic markets. Over the historical period (2019-2024), approximately xx M&A deals were recorded in the TFE industry, showcasing the consolidation trend.

Thin Film Encapsulation Industry Industry Trends & Analysis

The TFE industry is experiencing robust growth, driven primarily by the burgeoning demand for flexible displays in smartphones, wearable electronics, and foldable devices. The increasing adoption of thin-film photovoltaics (TFPV) in renewable energy applications further fuels market expansion. Technological disruptions, including advancements in inkjet printing and atomic layer deposition (ALD), are enhancing the efficiency and cost-effectiveness of TFE processes. Consumer preferences for high-resolution, durable, and flexible displays are shaping the demand for advanced TFE solutions. The competitive landscape is highly dynamic, with companies continually striving to improve their product offerings and manufacturing capabilities. The market is expected to witness a significant surge in growth due to the increasing demand for high-quality and flexible displays. This growth is further fueled by advancements in OLED and microLED technology, which heavily rely on TFE.

The projected Compound Annual Growth Rate (CAGR) for the TFE market is estimated at xx% for the forecast period (2025-2033). Market penetration in key applications, such as flexible OLED displays, is expected to reach xx% by 2033, reflecting the widespread adoption of this technology.

Leading Markets & Segments in Thin Film Encapsulation Industry

Dominant Region/Country: Asia-Pacific, particularly China, South Korea, and Japan, dominates the TFE market due to the concentration of major display manufacturers and the high demand for consumer electronics.

Dominant Application Segment: Flexible OLED displays represent the largest application segment, driven by the rapid growth of the smartphone and wearable electronics markets. Other applications, including thin-film photovoltaics and flexible OLED lighting, are also experiencing significant growth.

Dominant Technology Segment: Plasma-enhanced chemical vapor deposition (PECVD) holds a significant market share due to its established technology and relatively high throughput. However, inkjet printing and atomic layer deposition (ALD) are gaining traction due to their ability to enable high-resolution and low-temperature processing.

Key Drivers (by region):

- Asia-Pacific: Strong government support for renewable energy initiatives (TFPV), rapid growth of the electronics manufacturing sector, and increasing disposable incomes.

- North America: Focus on advanced display technologies, robust R&D investments, and presence of key technology providers.

- Europe: Government incentives for green technologies, focus on high-quality manufacturing, and a strong research base.

Thin Film Encapsulation Industry Product Developments

Recent product innovations focus on enhancing the barrier properties, flexibility, and durability of TFE materials. New encapsulation techniques, such as inkjet printing, are gaining traction due to their ability to achieve high resolution and reduce material waste. Companies are emphasizing the development of eco-friendly, low-cost TFE solutions that meet the stringent requirements of various applications. The competitive advantage lies in achieving a balance between performance, cost-effectiveness, and environmental sustainability. These developments strongly influence market adoption, particularly in applications demanding high flexibility, such as foldable displays and wearable devices.

Key Drivers of Thin Film Encapsulation Industry Growth

The TFE industry's growth is propelled by several key factors:

- Technological Advancements: Advancements in materials science and deposition techniques are enabling the creation of thinner, more flexible, and efficient TFE solutions.

- Economic Growth: Increasing disposable incomes in emerging economies are boosting the demand for consumer electronics, driving the need for advanced TFE technologies.

- Regulatory Support: Government initiatives promoting renewable energy and environmentally friendly technologies are supporting the growth of TFPV applications.

Challenges in the Thin Film Encapsulation Industry Market

Several factors pose challenges to the TFE industry:

- Regulatory Hurdles: Stringent environmental regulations and safety standards related to material composition and manufacturing processes increase the cost and complexity of TFE production.

- Supply Chain Issues: Disruptions in the supply chain for raw materials and specialized equipment can impact production capacity and lead times.

- Competitive Pressures: Intense competition among TFE manufacturers necessitates continuous innovation and cost optimization strategies. This, combined with the high capital expenditure required for manufacturing facilities, can lead to decreased profitability. The impact of these pressures is estimated to reduce industry profit margins by approximately xx% by 2033.

Emerging Opportunities in Thin Film Encapsulation Industry

The TFE industry is poised for significant growth due to several emerging opportunities:

- Technological Breakthroughs: Advancements in materials science and deposition technologies are continuously improving the performance and cost-effectiveness of TFE solutions.

- Strategic Partnerships: Collaborations between TFE manufacturers and display manufacturers are facilitating the development of innovative TFE solutions.

- Market Expansion: The adoption of TFE in emerging applications, such as flexible sensors and bioelectronics, presents significant growth opportunities.

Leading Players in the Thin Film Encapsulation Industry Sector

- Veeco Instruments Inc

- Applied Materials Inc

- Toray Industries Inc

- Beneq Inc

- Universal Display Corp (UDC)

- 3M

- Meyer Burger Technology Limited

- LG Chem

- Aixtron SE

- Kateeva

- BASF (Rolic) AG

- Lotus Applied Technology

- Samsung SDI

- Bystronic Glass

- Angstrom Engineering Inc

- AMS Technologies

Key Milestones in Thin Film Encapsulation Industry Industry

- December 2021: Unijet supplied inkjet equipment for micro OLED thin-film encapsulation to China's Sidtek, marking the first commercial application of Unijet's TFE inkjet equipment.

- April 2022: Samsung Display initiated development of a thinner quantum dot (QD)-OLED panel, aiming to reduce glass substrate usage and enable rollable QD-OLED products.

Strategic Outlook for Thin Film Encapsulation Industry Market

The TFE market presents significant growth potential driven by increasing demand for flexible electronics and renewable energy technologies. Strategic opportunities lie in developing innovative, cost-effective, and sustainable TFE solutions that meet the evolving needs of various applications. Companies should focus on research and development, strategic partnerships, and expanding into emerging markets to capitalize on this growth potential. The focus on sustainability and environmentally friendly materials will become increasingly important in driving future market share.

Thin Film Encapsulation Industry Segmentation

-

1. Technology

- 1.1. Plasma-enhanced chemical vapor deposition (PECVD)

- 1.2. Atomic layer deposition (ALD)

- 1.3. Inkjet Printing

- 1.4. Vacuum Thermal Evaporation (VTE)

- 1.5. Other Technologies

-

2. Application

- 2.1. Flexible OLED Display

- 2.2. Thin-Film Photovoltaics

- 2.3. Flexible OLED Lighting

- 2.4. Other Applications

Thin Film Encapsulation Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Rest of the World

Thin Film Encapsulation Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 14.80% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increase in Demand for Microelectronics and Consumer Electronics Products; Increased Adoption of Flexible OLED Displays for Smartphones and Smart Wearables

- 3.3. Market Restrains

- 3.3.1. High Capital Investment in R&D for Developing Upgraded Products; Augmented Growth of Flexible Glass

- 3.4. Market Trends

- 3.4.1. Flexible OLED Display Segment to Hold Significant Market Share

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Thin Film Encapsulation Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Technology

- 5.1.1. Plasma-enhanced chemical vapor deposition (PECVD)

- 5.1.2. Atomic layer deposition (ALD)

- 5.1.3. Inkjet Printing

- 5.1.4. Vacuum Thermal Evaporation (VTE)

- 5.1.5. Other Technologies

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Flexible OLED Display

- 5.2.2. Thin-Film Photovoltaics

- 5.2.3. Flexible OLED Lighting

- 5.2.4. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. North America

- 5.3.2. Europe

- 5.3.3. Asia Pacific

- 5.3.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Technology

- 6. North America Thin Film Encapsulation Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Technology

- 6.1.1. Plasma-enhanced chemical vapor deposition (PECVD)

- 6.1.2. Atomic layer deposition (ALD)

- 6.1.3. Inkjet Printing

- 6.1.4. Vacuum Thermal Evaporation (VTE)

- 6.1.5. Other Technologies

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Flexible OLED Display

- 6.2.2. Thin-Film Photovoltaics

- 6.2.3. Flexible OLED Lighting

- 6.2.4. Other Applications

- 6.1. Market Analysis, Insights and Forecast - by Technology

- 7. Europe Thin Film Encapsulation Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Technology

- 7.1.1. Plasma-enhanced chemical vapor deposition (PECVD)

- 7.1.2. Atomic layer deposition (ALD)

- 7.1.3. Inkjet Printing

- 7.1.4. Vacuum Thermal Evaporation (VTE)

- 7.1.5. Other Technologies

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Flexible OLED Display

- 7.2.2. Thin-Film Photovoltaics

- 7.2.3. Flexible OLED Lighting

- 7.2.4. Other Applications

- 7.1. Market Analysis, Insights and Forecast - by Technology

- 8. Asia Pacific Thin Film Encapsulation Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Technology

- 8.1.1. Plasma-enhanced chemical vapor deposition (PECVD)

- 8.1.2. Atomic layer deposition (ALD)

- 8.1.3. Inkjet Printing

- 8.1.4. Vacuum Thermal Evaporation (VTE)

- 8.1.5. Other Technologies

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Flexible OLED Display

- 8.2.2. Thin-Film Photovoltaics

- 8.2.3. Flexible OLED Lighting

- 8.2.4. Other Applications

- 8.1. Market Analysis, Insights and Forecast - by Technology

- 9. Rest of the World Thin Film Encapsulation Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Technology

- 9.1.1. Plasma-enhanced chemical vapor deposition (PECVD)

- 9.1.2. Atomic layer deposition (ALD)

- 9.1.3. Inkjet Printing

- 9.1.4. Vacuum Thermal Evaporation (VTE)

- 9.1.5. Other Technologies

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Flexible OLED Display

- 9.2.2. Thin-Film Photovoltaics

- 9.2.3. Flexible OLED Lighting

- 9.2.4. Other Applications

- 9.1. Market Analysis, Insights and Forecast - by Technology

- 10. North America Thin Film Encapsulation Industry Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 10.1.1.

- 11. Europe Thin Film Encapsulation Industry Analysis, Insights and Forecast, 2019-2031

- 11.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 11.1.1.

- 12. Asia Pacific Thin Film Encapsulation Industry Analysis, Insights and Forecast, 2019-2031

- 12.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 12.1.1.

- 13. Rest of the World Thin Film Encapsulation Industry Analysis, Insights and Forecast, 2019-2031

- 13.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 13.1.1.

- 14. Competitive Analysis

- 14.1. Global Market Share Analysis 2024

- 14.2. Company Profiles

- 14.2.1 Veeco Instruments Inc

- 14.2.1.1. Overview

- 14.2.1.2. Products

- 14.2.1.3. SWOT Analysis

- 14.2.1.4. Recent Developments

- 14.2.1.5. Financials (Based on Availability)

- 14.2.2 Applied Materials Inc

- 14.2.2.1. Overview

- 14.2.2.2. Products

- 14.2.2.3. SWOT Analysis

- 14.2.2.4. Recent Developments

- 14.2.2.5. Financials (Based on Availability)

- 14.2.3 Toray Industries Inc

- 14.2.3.1. Overview

- 14.2.3.2. Products

- 14.2.3.3. SWOT Analysis

- 14.2.3.4. Recent Developments

- 14.2.3.5. Financials (Based on Availability)

- 14.2.4 Beneq Inc *List Not Exhaustive

- 14.2.4.1. Overview

- 14.2.4.2. Products

- 14.2.4.3. SWOT Analysis

- 14.2.4.4. Recent Developments

- 14.2.4.5. Financials (Based on Availability)

- 14.2.5 Universal Display Corp (UDC)

- 14.2.5.1. Overview

- 14.2.5.2. Products

- 14.2.5.3. SWOT Analysis

- 14.2.5.4. Recent Developments

- 14.2.5.5. Financials (Based on Availability)

- 14.2.6 3M

- 14.2.6.1. Overview

- 14.2.6.2. Products

- 14.2.6.3. SWOT Analysis

- 14.2.6.4. Recent Developments

- 14.2.6.5. Financials (Based on Availability)

- 14.2.7 Meyer Burger Technology Limited

- 14.2.7.1. Overview

- 14.2.7.2. Products

- 14.2.7.3. SWOT Analysis

- 14.2.7.4. Recent Developments

- 14.2.7.5. Financials (Based on Availability)

- 14.2.8 LG Chem

- 14.2.8.1. Overview

- 14.2.8.2. Products

- 14.2.8.3. SWOT Analysis

- 14.2.8.4. Recent Developments

- 14.2.8.5. Financials (Based on Availability)

- 14.2.9 Aixtron SE

- 14.2.9.1. Overview

- 14.2.9.2. Products

- 14.2.9.3. SWOT Analysis

- 14.2.9.4. Recent Developments

- 14.2.9.5. Financials (Based on Availability)

- 14.2.10 Kateeva

- 14.2.10.1. Overview

- 14.2.10.2. Products

- 14.2.10.3. SWOT Analysis

- 14.2.10.4. Recent Developments

- 14.2.10.5. Financials (Based on Availability)

- 14.2.11 BASF (Rolic) AG

- 14.2.11.1. Overview

- 14.2.11.2. Products

- 14.2.11.3. SWOT Analysis

- 14.2.11.4. Recent Developments

- 14.2.11.5. Financials (Based on Availability)

- 14.2.12 Lotus Applied Technology

- 14.2.12.1. Overview

- 14.2.12.2. Products

- 14.2.12.3. SWOT Analysis

- 14.2.12.4. Recent Developments

- 14.2.12.5. Financials (Based on Availability)

- 14.2.13 Samsung SDI

- 14.2.13.1. Overview

- 14.2.13.2. Products

- 14.2.13.3. SWOT Analysis

- 14.2.13.4. Recent Developments

- 14.2.13.5. Financials (Based on Availability)

- 14.2.14 Bystronic Glass

- 14.2.14.1. Overview

- 14.2.14.2. Products

- 14.2.14.3. SWOT Analysis

- 14.2.14.4. Recent Developments

- 14.2.14.5. Financials (Based on Availability)

- 14.2.15 Angstrom Engineering Inc

- 14.2.15.1. Overview

- 14.2.15.2. Products

- 14.2.15.3. SWOT Analysis

- 14.2.15.4. Recent Developments

- 14.2.15.5. Financials (Based on Availability)

- 14.2.16 AMS Technologies

- 14.2.16.1. Overview

- 14.2.16.2. Products

- 14.2.16.3. SWOT Analysis

- 14.2.16.4. Recent Developments

- 14.2.16.5. Financials (Based on Availability)

- 14.2.1 Veeco Instruments Inc

List of Figures

- Figure 1: Global Thin Film Encapsulation Industry Revenue Breakdown (Million, %) by Region 2024 & 2032

- Figure 2: North America Thin Film Encapsulation Industry Revenue (Million), by Country 2024 & 2032

- Figure 3: North America Thin Film Encapsulation Industry Revenue Share (%), by Country 2024 & 2032

- Figure 4: Europe Thin Film Encapsulation Industry Revenue (Million), by Country 2024 & 2032

- Figure 5: Europe Thin Film Encapsulation Industry Revenue Share (%), by Country 2024 & 2032

- Figure 6: Asia Pacific Thin Film Encapsulation Industry Revenue (Million), by Country 2024 & 2032

- Figure 7: Asia Pacific Thin Film Encapsulation Industry Revenue Share (%), by Country 2024 & 2032

- Figure 8: Rest of the World Thin Film Encapsulation Industry Revenue (Million), by Country 2024 & 2032

- Figure 9: Rest of the World Thin Film Encapsulation Industry Revenue Share (%), by Country 2024 & 2032

- Figure 10: North America Thin Film Encapsulation Industry Revenue (Million), by Technology 2024 & 2032

- Figure 11: North America Thin Film Encapsulation Industry Revenue Share (%), by Technology 2024 & 2032

- Figure 12: North America Thin Film Encapsulation Industry Revenue (Million), by Application 2024 & 2032

- Figure 13: North America Thin Film Encapsulation Industry Revenue Share (%), by Application 2024 & 2032

- Figure 14: North America Thin Film Encapsulation Industry Revenue (Million), by Country 2024 & 2032

- Figure 15: North America Thin Film Encapsulation Industry Revenue Share (%), by Country 2024 & 2032

- Figure 16: Europe Thin Film Encapsulation Industry Revenue (Million), by Technology 2024 & 2032

- Figure 17: Europe Thin Film Encapsulation Industry Revenue Share (%), by Technology 2024 & 2032

- Figure 18: Europe Thin Film Encapsulation Industry Revenue (Million), by Application 2024 & 2032

- Figure 19: Europe Thin Film Encapsulation Industry Revenue Share (%), by Application 2024 & 2032

- Figure 20: Europe Thin Film Encapsulation Industry Revenue (Million), by Country 2024 & 2032

- Figure 21: Europe Thin Film Encapsulation Industry Revenue Share (%), by Country 2024 & 2032

- Figure 22: Asia Pacific Thin Film Encapsulation Industry Revenue (Million), by Technology 2024 & 2032

- Figure 23: Asia Pacific Thin Film Encapsulation Industry Revenue Share (%), by Technology 2024 & 2032

- Figure 24: Asia Pacific Thin Film Encapsulation Industry Revenue (Million), by Application 2024 & 2032

- Figure 25: Asia Pacific Thin Film Encapsulation Industry Revenue Share (%), by Application 2024 & 2032

- Figure 26: Asia Pacific Thin Film Encapsulation Industry Revenue (Million), by Country 2024 & 2032

- Figure 27: Asia Pacific Thin Film Encapsulation Industry Revenue Share (%), by Country 2024 & 2032

- Figure 28: Rest of the World Thin Film Encapsulation Industry Revenue (Million), by Technology 2024 & 2032

- Figure 29: Rest of the World Thin Film Encapsulation Industry Revenue Share (%), by Technology 2024 & 2032

- Figure 30: Rest of the World Thin Film Encapsulation Industry Revenue (Million), by Application 2024 & 2032

- Figure 31: Rest of the World Thin Film Encapsulation Industry Revenue Share (%), by Application 2024 & 2032

- Figure 32: Rest of the World Thin Film Encapsulation Industry Revenue (Million), by Country 2024 & 2032

- Figure 33: Rest of the World Thin Film Encapsulation Industry Revenue Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Thin Film Encapsulation Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Global Thin Film Encapsulation Industry Revenue Million Forecast, by Technology 2019 & 2032

- Table 3: Global Thin Film Encapsulation Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 4: Global Thin Film Encapsulation Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: Global Thin Film Encapsulation Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: Thin Film Encapsulation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: Global Thin Film Encapsulation Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 8: Thin Film Encapsulation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Global Thin Film Encapsulation Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 10: Thin Film Encapsulation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Global Thin Film Encapsulation Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 12: Thin Film Encapsulation Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Global Thin Film Encapsulation Industry Revenue Million Forecast, by Technology 2019 & 2032

- Table 14: Global Thin Film Encapsulation Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 15: Global Thin Film Encapsulation Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 16: Global Thin Film Encapsulation Industry Revenue Million Forecast, by Technology 2019 & 2032

- Table 17: Global Thin Film Encapsulation Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 18: Global Thin Film Encapsulation Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 19: Global Thin Film Encapsulation Industry Revenue Million Forecast, by Technology 2019 & 2032

- Table 20: Global Thin Film Encapsulation Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 21: Global Thin Film Encapsulation Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 22: Global Thin Film Encapsulation Industry Revenue Million Forecast, by Technology 2019 & 2032

- Table 23: Global Thin Film Encapsulation Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 24: Global Thin Film Encapsulation Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Thin Film Encapsulation Industry?

The projected CAGR is approximately 14.80%.

2. Which companies are prominent players in the Thin Film Encapsulation Industry?

Key companies in the market include Veeco Instruments Inc, Applied Materials Inc, Toray Industries Inc, Beneq Inc *List Not Exhaustive, Universal Display Corp (UDC), 3M, Meyer Burger Technology Limited, LG Chem, Aixtron SE, Kateeva, BASF (Rolic) AG, Lotus Applied Technology, Samsung SDI, Bystronic Glass, Angstrom Engineering Inc, AMS Technologies.

3. What are the main segments of the Thin Film Encapsulation Industry?

The market segments include Technology, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Increase in Demand for Microelectronics and Consumer Electronics Products; Increased Adoption of Flexible OLED Displays for Smartphones and Smart Wearables.

6. What are the notable trends driving market growth?

Flexible OLED Display Segment to Hold Significant Market Share.

7. Are there any restraints impacting market growth?

High Capital Investment in R&D for Developing Upgraded Products; Augmented Growth of Flexible Glass.

8. Can you provide examples of recent developments in the market?

April 2022 - Samsung Display started working on developing a thinner version of its quantum dot (QD)-OLED panel with the aim is to reduce the use of glass substrates to one. The project's success will enable the company to launch the new version of QD-OLED in a rollable format.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Thin Film Encapsulation Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Thin Film Encapsulation Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Thin Film Encapsulation Industry?

To stay informed about further developments, trends, and reports in the Thin Film Encapsulation Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence