Key Insights

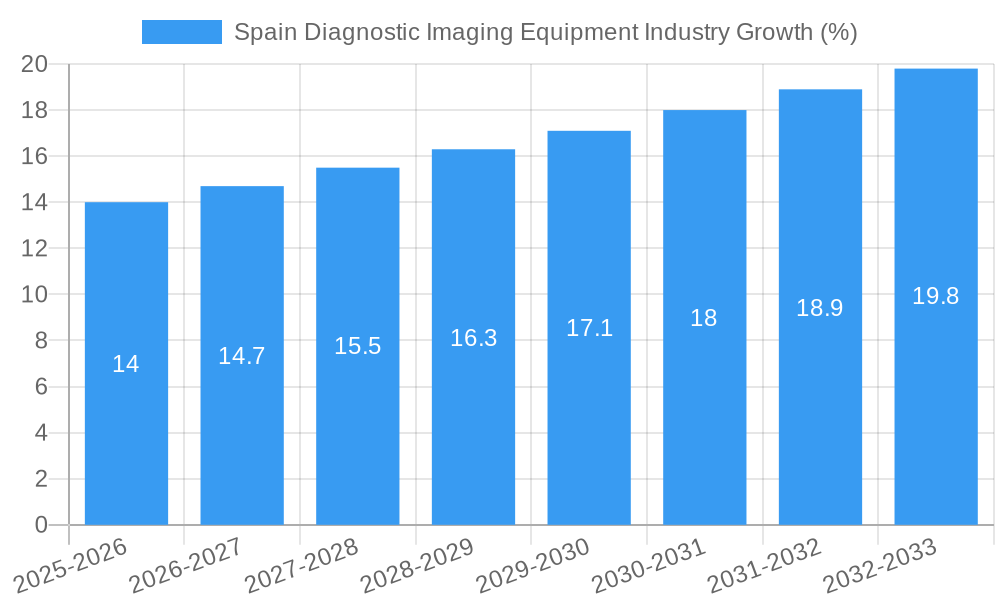

The Spanish diagnostic imaging equipment market, valued at approximately €[Estimate based on market size XX and currency conversion, e.g., €250 million] in 2025, is projected to experience robust growth, driven by a CAGR of 5.50% from 2025 to 2033. This expansion is fueled by several key factors. Firstly, an aging population necessitates increased screening and diagnostic procedures, boosting demand for advanced imaging technologies. Secondly, rising prevalence of chronic diseases such as cardiovascular ailments and cancer necessitates sophisticated diagnostic tools for early and accurate detection. Technological advancements in MRI, CT, and ultrasound systems, leading to improved image quality, faster scan times, and reduced radiation exposure, further stimulate market growth. Increased healthcare spending and government initiatives promoting preventative healthcare also contribute positively. However, the market faces challenges including high equipment costs, stringent regulatory approvals, and potential budgetary constraints within the healthcare sector. The segment breakdown reveals that MRI and CT remain dominant modalities, followed by ultrasound and X-ray. Applications are broadly distributed across cardiology, oncology, and neurology, mirroring the disease burden in Spain. Hospitals and diagnostic centers comprise the primary end-users. Key players such as GE Healthcare, Philips, Siemens, and Esaote are actively engaged in the market, competing through technological innovation and strategic partnerships.

The market segmentation reveals a dynamic landscape. While MRI and CT remain the leading modalities due to their superior diagnostic capabilities, the ultrasound segment shows potential for rapid growth, driven by its affordability and portability, making it ideal for use in smaller clinics and remote areas. The application segments reflect healthcare priorities in Spain, with cardiology, oncology, and neurology showing strong demand. The competitive landscape is characterized by both established international players and local distributors. Future growth will depend on continued technological innovation, particularly in areas like AI-powered image analysis and minimally invasive procedures. Government policies aimed at improving healthcare infrastructure and accessibility will significantly impact market performance in the forecast period. Pricing strategies, technological advancements, and strategic partnerships will be crucial determinants of success for market participants.

Spain Diagnostic Imaging Equipment Industry: Market Report 2019-2033

This comprehensive report provides a detailed analysis of the Spain Diagnostic Imaging Equipment market, offering invaluable insights for industry stakeholders, investors, and strategic decision-makers. With a focus on market dynamics, trends, leading players, and future opportunities, this report covers the period 2019-2033, with a base year of 2025 and a forecast period of 2025-2033. The report leverages robust data analysis and incorporates key industry developments to provide actionable intelligence.

Spain Diagnostic Imaging Equipment Industry Market Dynamics & Concentration

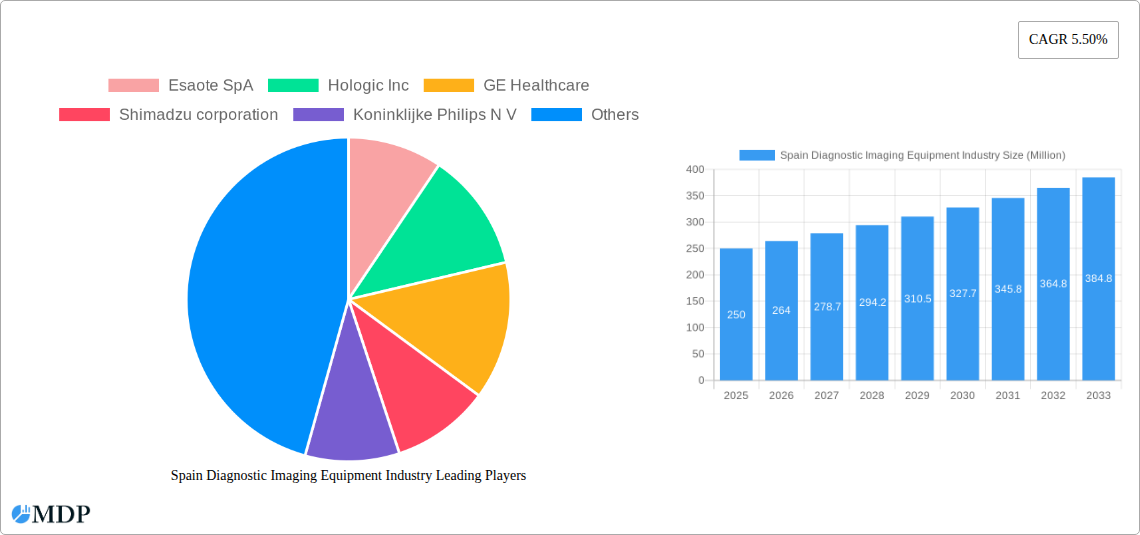

The Spain diagnostic imaging equipment market exhibits a moderately concentrated landscape, with several multinational corporations holding significant market share. Key players such as GE Healthcare, Koninklijke Philips N.V., Siemens AG, and Shimadzu Corporation dominate the market, leveraging their established brand reputation and extensive product portfolios. The market share of these leading players is estimated to be around 65% in 2025, while smaller players and regional distributors constitute the remaining 35%. Innovation remains a critical driver, with companies continuously investing in research and development to enhance image quality, reduce examination times, and improve diagnostic accuracy. Stringent regulatory frameworks, including those overseen by the Spanish Agency of Medicines and Medical Devices (AEMPS), ensure safety and efficacy standards. The market witnesses periodic M&A activities, with an estimated xx M&A deals in the historical period (2019-2024). Substitutes for traditional diagnostic imaging equipment, such as advanced software solutions for image analysis, are slowly gaining traction, but overall, these remain niche competitors. End-user trends indicate a growing preference for advanced modalities like MRI and PET/CT, fueled by an aging population and increasing prevalence of chronic diseases.

- Market Concentration: 65% dominated by leading players in 2025.

- Innovation Drivers: Continuous R&D in image quality, speed, and accuracy.

- Regulatory Framework: AEMPS oversight ensures safety and efficacy.

- Product Substitutes: Advanced image analysis software gaining limited traction.

- M&A Activity: Approximately xx deals between 2019 and 2024.

- End-User Trends: Increasing demand for advanced modalities (MRI, PET/CT).

Spain Diagnostic Imaging Equipment Industry Industry Trends & Analysis

The Spanish diagnostic imaging equipment market is experiencing robust growth, driven by factors such as rising healthcare expenditure, technological advancements, and a growing prevalence of chronic diseases. The Compound Annual Growth Rate (CAGR) is projected to be approximately xx% during the forecast period (2025-2033). Technological disruptions, particularly in AI-powered image analysis and minimally invasive procedures, are significantly impacting the market landscape. Consumer preferences are shifting towards advanced modalities offering faster results, better image quality, and reduced radiation exposure. The competitive dynamics remain intense, with established players facing pressure from emerging companies offering innovative solutions and cost-effective alternatives. Market penetration of advanced modalities, like MRI and PET/CT, is steadily increasing, driven by improved reimbursement policies and rising awareness among healthcare professionals. Technological trends such as AI-integrated systems and cloud-based image management solutions are expected to further shape market growth in the coming years. The market penetration rate for AI-integrated systems is expected to reach xx% by 2033.

Leading Markets & Segments in Spain Diagnostic Imaging Equipment Industry

The Spanish diagnostic imaging equipment market is geographically concentrated, with major metropolitan areas and regions with well-established healthcare infrastructure exhibiting higher demand. Within the market segmentation:

By Modality: Computed Tomography (CT) and Ultrasound currently hold the largest market share, driven by their widespread adoption across various healthcare settings. MRI is also a significant segment, witnessing robust growth due to its superior imaging capabilities.

By Application: Oncology and Cardiology represent the leading application segments, reflecting the high prevalence of cardiovascular diseases and cancer in Spain.

By End User: Hospitals constitute the largest end-user segment, followed by diagnostic centers.

- Key Drivers (By Region): Strong healthcare infrastructure in major urban areas, favorable government policies supporting healthcare investments.

- Dominant Segments: CT, Ultrasound, and MRI by modality; Oncology and Cardiology by application; Hospitals by end-user.

Spain Diagnostic Imaging Equipment Industry Product Developments

Recent product innovations focus on enhancing image quality, reducing radiation exposure, and improving workflow efficiency. AI-powered image analysis tools are gaining traction, assisting radiologists in faster and more accurate diagnoses. Miniaturized and portable devices are gaining prominence, enabling point-of-care diagnostics. The market is witnessing the integration of advanced technologies like deep learning algorithms to enhance image processing and analysis, leading to improved diagnostic outcomes and reduced healthcare costs. This is reflected in the competitive landscape, with major players continuously investing in R&D to launch innovative and superior products.

Key Drivers of Spain Diagnostic Imaging Equipment Industry Growth

The Spanish diagnostic imaging equipment market is propelled by several key drivers:

- Technological advancements: Introduction of AI-powered tools, enhanced image quality, and minimally invasive procedures.

- Rising healthcare expenditure: Increased government funding and private investments in healthcare infrastructure.

- Favorable regulatory environment: Policies supporting technological adoption and improved patient access to advanced diagnostic services.

- Growing prevalence of chronic diseases: Higher incidence of cardiovascular diseases, cancer, and other conditions driving demand for diagnostic imaging.

Challenges in the Spain Diagnostic Imaging Equipment Industry Market

The market faces several challenges:

- High initial investment costs: Advanced equipment requires substantial upfront investment, limiting accessibility for smaller clinics.

- Stringent regulatory approvals: Navigating the regulatory processes can be time-consuming and complex, potentially delaying product launches.

- Intense competition: The market is characterized by fierce competition from both established and emerging players.

- Economic downturns: Fluctuations in the Spanish economy can impact healthcare spending and delay investments in new equipment. This resulted in an estimated xx Million reduction in market value in 2023.

Emerging Opportunities in Spain Diagnostic Imaging Equipment Industry

Significant opportunities exist for growth in the Spanish market:

- Telemedicine integration: Remote diagnostic imaging services are gaining prominence, enhancing accessibility and efficiency.

- Strategic partnerships: Collaborations between technology providers and healthcare institutions can drive innovation and market penetration.

- Expansion into underserved regions: Reaching rural areas and expanding access to advanced diagnostic services can open significant market opportunities.

- Focus on preventive care: Increased emphasis on early detection and preventive healthcare can boost the demand for diagnostic imaging.

Leading Players in the Spain Diagnostic Imaging Equipment Industry Sector

- Esaote SpA

- Hologic Inc

- GE Healthcare

- Shimadzu corporation

- Koninklijke Philips N.V.

- Siemens AG

- AURELIUS (Agfa-Gevaert Group)

- Carestream Health

- Canon

- Fujifilm Holdings Corporation

Key Milestones in Spain Diagnostic Imaging Equipment Industry Industry

- October 2022: GE Healthcare launched the Omni PET/CT platform and Omni Legend system at the EANM meeting in Barcelona, signifying advancements in nuclear imaging technology.

- August 2022: Bellvitge University Hospital incorporated a gamma camera, enhancing oncology care and research capabilities.

Strategic Outlook for Spain Diagnostic Imaging Equipment Industry Market

The Spanish diagnostic imaging equipment market is poised for continued growth, driven by technological advancements, increasing healthcare expenditure, and the rising prevalence of chronic diseases. Strategic partnerships, investments in R&D, and expansion into new segments will be crucial for success. The market is expected to see significant growth in the adoption of AI-powered solutions, cloud-based platforms and minimally invasive procedures. The market is projected to reach xx Million by 2033.

Spain Diagnostic Imaging Equipment Industry Segmentation

-

1. Modality

- 1.1. MRI

- 1.2. Computed Tomography

- 1.3. Ultrasound

- 1.4. X-Ray

- 1.5. Nuclear Imaging

- 1.6. Fluoroscopy

- 1.7. Mammography

-

2. Application

- 2.1. Cardiology

- 2.2. Oncology

- 2.3. Neurology

- 2.4. Orthopedics

- 2.5. Gastroenterology

- 2.6. Gynecology

- 2.7. Other Applications

-

3. End User

- 3.1. Hospital

- 3.2. Diagnostic Centers

- 3.3. Other End Users

Spain Diagnostic Imaging Equipment Industry Segmentation By Geography

- 1. Spain

Spain Diagnostic Imaging Equipment Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 5.50% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Rise in the Prevalence of Chronic Diseases and Growing Geriatric Population; Technological Advancements and Rapid Innovation

- 3.3. Market Restrains

- 3.3.1. High Cost of Diagnostic Imaging Procedures and Equipment

- 3.4. Market Trends

- 3.4.1. Oncology Segment is Expected to Show Better Growth in the Forecast Years

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Spain Diagnostic Imaging Equipment Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Modality

- 5.1.1. MRI

- 5.1.2. Computed Tomography

- 5.1.3. Ultrasound

- 5.1.4. X-Ray

- 5.1.5. Nuclear Imaging

- 5.1.6. Fluoroscopy

- 5.1.7. Mammography

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Cardiology

- 5.2.2. Oncology

- 5.2.3. Neurology

- 5.2.4. Orthopedics

- 5.2.5. Gastroenterology

- 5.2.6. Gynecology

- 5.2.7. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by End User

- 5.3.1. Hospital

- 5.3.2. Diagnostic Centers

- 5.3.3. Other End Users

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Spain

- 5.1. Market Analysis, Insights and Forecast - by Modality

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 Esaote SpA

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Hologic Inc

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 GE Healthcare

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Shimadzu corporation

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Koninklijke Philips N V

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Siemens AG

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 AURELIUS (Agfa-Gevaert Group)

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Carestream Health

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Canon*List Not Exhaustive

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 Fujifilm Holdings Corporation

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.1 Esaote SpA

List of Figures

- Figure 1: Spain Diagnostic Imaging Equipment Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Spain Diagnostic Imaging Equipment Industry Share (%) by Company 2024

List of Tables

- Table 1: Spain Diagnostic Imaging Equipment Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Spain Diagnostic Imaging Equipment Industry Revenue Million Forecast, by Modality 2019 & 2032

- Table 3: Spain Diagnostic Imaging Equipment Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 4: Spain Diagnostic Imaging Equipment Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 5: Spain Diagnostic Imaging Equipment Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 6: Spain Diagnostic Imaging Equipment Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 7: Spain Diagnostic Imaging Equipment Industry Revenue Million Forecast, by Modality 2019 & 2032

- Table 8: Spain Diagnostic Imaging Equipment Industry Revenue Million Forecast, by Application 2019 & 2032

- Table 9: Spain Diagnostic Imaging Equipment Industry Revenue Million Forecast, by End User 2019 & 2032

- Table 10: Spain Diagnostic Imaging Equipment Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Spain Diagnostic Imaging Equipment Industry?

The projected CAGR is approximately 5.50%.

2. Which companies are prominent players in the Spain Diagnostic Imaging Equipment Industry?

Key companies in the market include Esaote SpA, Hologic Inc, GE Healthcare, Shimadzu corporation, Koninklijke Philips N V, Siemens AG, AURELIUS (Agfa-Gevaert Group), Carestream Health, Canon*List Not Exhaustive, Fujifilm Holdings Corporation.

3. What are the main segments of the Spain Diagnostic Imaging Equipment Industry?

The market segments include Modality, Application, End User.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Rise in the Prevalence of Chronic Diseases and Growing Geriatric Population; Technological Advancements and Rapid Innovation.

6. What are the notable trends driving market growth?

Oncology Segment is Expected to Show Better Growth in the Forecast Years.

7. Are there any restraints impacting market growth?

High Cost of Diagnostic Imaging Procedures and Equipment.

8. Can you provide examples of recent developments in the market?

In October 2022, GE Healthcare launched the Omni PET/CT platform and Omni Legend system at the annual meeting of the European Association of Nuclear Medicine (EANM) in Barcelona, Spain.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Spain Diagnostic Imaging Equipment Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Spain Diagnostic Imaging Equipment Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Spain Diagnostic Imaging Equipment Industry?

To stay informed about further developments, trends, and reports in the Spain Diagnostic Imaging Equipment Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence