Key Insights

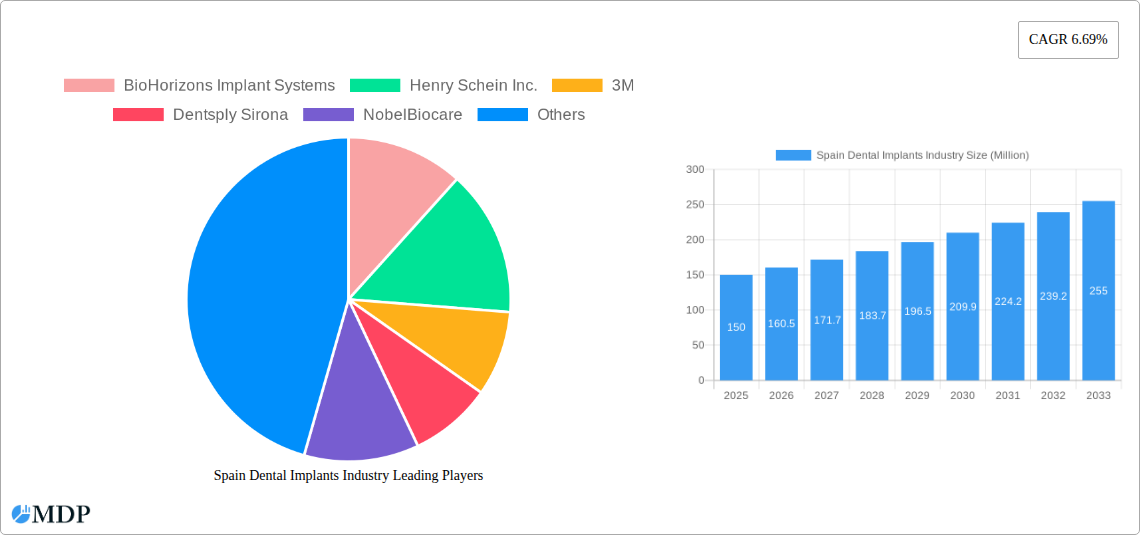

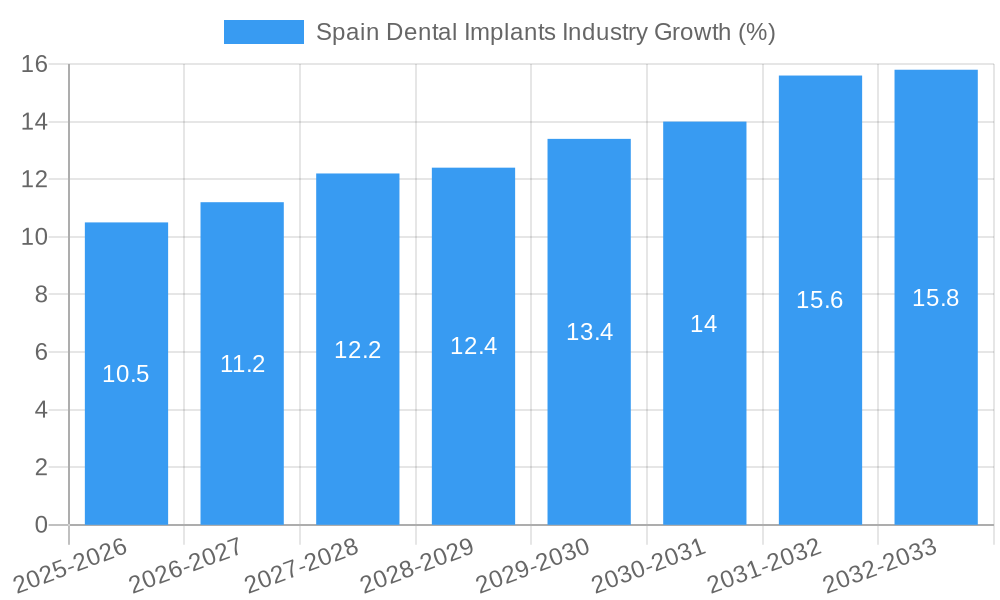

The Spanish dental implants market, valued at approximately €150 million in 2025, is projected to experience robust growth, exhibiting a Compound Annual Growth Rate (CAGR) of 6.69% from 2025 to 2033. This expansion is driven by several key factors. An aging population, increasing prevalence of periodontal disease, and rising awareness regarding improved oral health and aesthetics are fueling demand for dental implants. Furthermore, advancements in implant technology, such as minimally invasive procedures and improved biocompatible materials, contribute to higher success rates and patient satisfaction, further boosting market growth. The increasing affordability of dental implants through insurance coverage and financing options also plays a crucial role. The market is segmented by treatment type (orthodontic, endodontic, periodontic, prosthodontic), end-users (hospitals, clinics, other end-users), and product type (general and diagnostic equipment, dental lasers, extra-oral and intra-oral radiology equipment). Major players like BioHorizons, Henry Schein, 3M, Dentsply Sirona, and NobelBiocare are actively competing in this dynamic market, investing in research and development and expanding their product portfolios to cater to evolving patient needs and technological advancements.

The competitive landscape is characterized by both established multinational corporations and specialized local companies. While larger companies benefit from economies of scale and established distribution networks, smaller players are often more agile and focused on niche segments. The market is expected to witness increased consolidation through mergers and acquisitions as companies strive to gain market share and expand their product offerings. Potential restraints include economic fluctuations impacting healthcare spending and the relatively high cost of dental implants, which could potentially limit accessibility for some segments of the population. However, ongoing technological advancements and increasing affordability are likely to mitigate these restraints in the long term, ensuring continued expansion of the Spanish dental implants market over the forecast period.

Spain Dental Implants Industry: A Comprehensive Market Report (2019-2033)

This comprehensive report provides an in-depth analysis of the Spain dental implants industry, offering invaluable insights for stakeholders, investors, and industry professionals. With a focus on market dynamics, leading players, and future growth potential, this report covers the period from 2019 to 2033, providing both historical data and future projections. The study uses 2025 as its base and estimated year. The report is meticulously crafted to maximize search visibility and drive engagement through targeted keyword optimization. Key areas covered include market size analysis, competitive landscape, segment performance, technological advancements, and key growth drivers. This report is crucial for understanding the current state and future trajectory of the Spanish dental implants market.

Spain Dental Implants Industry Market Dynamics & Concentration

The Spain dental implants market, valued at xx Million in 2024, exhibits a moderately concentrated landscape. Key players like BioHorizons Implant Systems, Henry Schein Inc., 3M, Dentsply Sirona, NobelBiocare, Carestream Health, Straumann Holding AG, and Zimmer Biomet hold significant market share, driving innovation and shaping industry trends. Terrats Medical SL also contributes significantly to the domestic market.

Market concentration is influenced by factors including:

- Innovation Drivers: Continuous advancements in implant materials, surgical techniques, and digital dentistry are driving market growth.

- Regulatory Frameworks: Stringent regulatory approvals and quality standards influence market entry and competition.

- Product Substitutes: While dental implants are often the preferred solution, alternatives like dentures and bridges exert some competitive pressure.

- End-User Trends: Growing awareness of dental health and increasing demand for aesthetically pleasing and functional restorations fuel market expansion.

- M&A Activities: The acquisition of Condor Dental by Henry Schein in June 2022 highlights the consolidation trend within the industry, aiming for enhanced pan-European reach and service capabilities. The number of M&A deals in the period 2019-2024 totaled xx, indicating a moderate level of consolidation. Market share data indicates that the top five players hold approximately xx% of the market collectively.

Spain Dental Implants Industry Industry Trends & Analysis

The Spain dental implants market is experiencing robust growth, with a projected CAGR of xx% during the forecast period (2025-2033). This growth is fueled by several key factors:

- Increasing Geriatric Population: The aging population necessitates increased restorative dental procedures, boosting demand for implants.

- Rising Disposable Incomes: Improved economic conditions enable more individuals to afford advanced dental treatments.

- Technological Advancements: The integration of digital technologies, such as CAD/CAM systems and guided surgery, enhances precision and efficiency, driving adoption.

- Enhanced Aesthetic Outcomes: Patients increasingly seek aesthetically pleasing solutions, leading to higher demand for implants.

- Growing Awareness of Oral Health: Improved public awareness of the importance of oral hygiene and preventative care contributes to increased treatment rates.

The market penetration rate for dental implants in Spain is currently estimated at xx%, signifying significant untapped potential. Competitive dynamics are characterized by both intense competition among established players and the emergence of new, innovative companies.

Leading Markets & Segments in Spain Dental Implants Industry

While data on regional variations is not readily available for specific regional breakdowns within Spain, the analysis suggests the following:

- Dominant Segment: The Prosthodontic segment is likely the largest, owing to the significant number of patients requiring tooth replacements.

- Key End-Users: Clinics constitute the largest end-user segment, followed by hospitals and other specialized dental practices.

- Dominant Product Category: General and diagnostics equipment represent the largest product segment, encompassing essential instruments and tools.

Key Drivers:

- Strong Healthcare Infrastructure: Spain possesses a relatively well-developed healthcare system, providing a supportive framework for the industry.

- Favorable Government Policies: Government initiatives promoting oral health and access to dental care are contributing positively to market growth.

- Growing Private Healthcare Sector: The expanding private healthcare sector plays a significant role in driving demand for advanced dental treatments, including implants.

Spain Dental Implants Industry Product Developments

Recent product developments emphasize minimally invasive techniques, improved biocompatibility, and enhanced aesthetics. The integration of digital technologies, such as 3D printing and computer-guided surgery, is revolutionizing implant placement, resulting in shorter treatment times, reduced invasiveness, and improved precision. These advancements contribute to increased patient satisfaction and improved clinical outcomes. The market is also seeing a surge in the development of specialized implants for various clinical indications, such as immediate-load implants and implants for challenging anatomical conditions.

Key Drivers of Spain Dental Implants Industry Growth

Several factors drive the growth of the Spain dental implants market:

- Technological advancements: Digital dentistry, CAD/CAM technology, and guided surgery enhance precision and efficiency.

- Economic growth: Rising disposable incomes enable more people to afford expensive dental treatments.

- Favorable regulatory environment: Supportive government policies and regulations create a conducive business environment.

- Increasing awareness of oral health: Improved awareness promotes preventative care and restorative treatments.

Challenges in the Spain Dental Implants Industry Market

The Spanish dental implants market faces challenges including:

- High treatment costs: Dental implants are expensive, limiting access for some patients.

- Supply chain disruptions: Global supply chain issues can affect the availability of materials and equipment.

- Competition from alternative treatments: Dentures and bridges remain competitive alternatives.

- Strict regulatory approvals: The process of obtaining regulatory approval can be time-consuming and costly. These factors together could reduce the market growth by approximately xx% in the next 5 years.

Emerging Opportunities in Spain Dental Implants Industry

Several factors indicate promising future growth:

- Advancements in implant materials: New materials offer improved biocompatibility and longevity.

- Strategic partnerships: Collaborations between dental professionals and implant manufacturers will help to improve service offerings.

- Expansion into underserved markets: Reaching patients in rural areas can significantly boost market size.

- Growing demand for minimally invasive procedures: Patients prefer less invasive treatments with shorter recovery periods.

Leading Players in the Spain Dental Implants Industry Sector

- BioHorizons Implant Systems

- Henry Schein Inc.

- 3M

- Dentsply Sirona

- NobelBiocare

- Carestream Health

- Straumann Holding AG

- Zimmer Biomet

- Terrats Medical SL

Key Milestones in Spain Dental Implants Industry Industry

- June 2022: Henry Schein acquires Condor Dental, expanding its Swiss operations and pan-European reach.

- February 2021: 3M Oral Care donates USD 2 Million and 3,000 PAPRs to support dental offices recovering from pandemic-related challenges and adopting new technologies like teledentistry.

Strategic Outlook for Spain Dental Implants Industry Market

The Spain dental implants market holds significant long-term growth potential. Continued innovation in implant technology, coupled with rising awareness of oral health and increased access to quality dental care, will drive market expansion. Strategic partnerships, targeted marketing campaigns, and expansion into underserved regions will create additional growth opportunities. The market is poised to expand considerably in the next decade, driven by the factors described above.

Spain Dental Implants Industry Segmentation

-

1. Product

-

1.1. General and Diagnostics Equipment

-

1.1.1. Dental Laser

- 1.1.1.1. Soft Tissue Lasers

- 1.1.1.2. Hard Tissue Lasers

-

1.1.2. Radiology Equipment

- 1.1.2.1. Extra Oral Radiology Equipment

- 1.1.2.2. Intra-oral Radiology Equipment

- 1.1.3. Dental Chair and Equipment

- 1.1.4. Other General and Diagnostic Equipment

-

1.1.1. Dental Laser

-

1.2. Dental Consumables

- 1.2.1. Dental Biomaterial

- 1.2.2. Dental Implants

- 1.2.3. Crowns and Bridges

- 1.2.4. Other Dental Consumables

- 1.3. Other Dental Devices

-

1.1. General and Diagnostics Equipment

-

2. Treatment

- 2.1. Orthodontic

- 2.2. Endodontic

- 2.3. Periodontic

- 2.4. Prosthodontic

-

3. End-Users

- 3.1. Hospitals

- 3.2. Clinics

- 3.3. Other End-Users

Spain Dental Implants Industry Segmentation By Geography

- 1. Spain

Spain Dental Implants Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 6.69% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Burden of Oral Diseases and Ageing Population; Technological Advancements in Dentistry

- 3.3. Market Restrains

- 3.3.1. Increasing Cost of Surgeries

- 3.4. Market Trends

- 3.4.1. Prosthodontic Equipment is Expected to Witness a Significant Growth Over a Forecast Period

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Spain Dental Implants Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Product

- 5.1.1. General and Diagnostics Equipment

- 5.1.1.1. Dental Laser

- 5.1.1.1.1. Soft Tissue Lasers

- 5.1.1.1.2. Hard Tissue Lasers

- 5.1.1.2. Radiology Equipment

- 5.1.1.2.1. Extra Oral Radiology Equipment

- 5.1.1.2.2. Intra-oral Radiology Equipment

- 5.1.1.3. Dental Chair and Equipment

- 5.1.1.4. Other General and Diagnostic Equipment

- 5.1.1.1. Dental Laser

- 5.1.2. Dental Consumables

- 5.1.2.1. Dental Biomaterial

- 5.1.2.2. Dental Implants

- 5.1.2.3. Crowns and Bridges

- 5.1.2.4. Other Dental Consumables

- 5.1.3. Other Dental Devices

- 5.1.1. General and Diagnostics Equipment

- 5.2. Market Analysis, Insights and Forecast - by Treatment

- 5.2.1. Orthodontic

- 5.2.2. Endodontic

- 5.2.3. Periodontic

- 5.2.4. Prosthodontic

- 5.3. Market Analysis, Insights and Forecast - by End-Users

- 5.3.1. Hospitals

- 5.3.2. Clinics

- 5.3.3. Other End-Users

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. Spain

- 5.1. Market Analysis, Insights and Forecast - by Product

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2024

- 6.2. Company Profiles

- 6.2.1 BioHorizons Implant Systems

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 Henry Schein Inc.

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 3M

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Dentsply Sirona

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 NobelBiocare

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Carestream Health

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Straumann Holding AG

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Zimmer Biomet

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Terrats Medical SL

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.1 BioHorizons Implant Systems

List of Figures

- Figure 1: Spain Dental Implants Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Spain Dental Implants Industry Share (%) by Company 2024

List of Tables

- Table 1: Spain Dental Implants Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Spain Dental Implants Industry Volume K Units Forecast, by Region 2019 & 2032

- Table 3: Spain Dental Implants Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 4: Spain Dental Implants Industry Volume K Units Forecast, by Product 2019 & 2032

- Table 5: Spain Dental Implants Industry Revenue Million Forecast, by Treatment 2019 & 2032

- Table 6: Spain Dental Implants Industry Volume K Units Forecast, by Treatment 2019 & 2032

- Table 7: Spain Dental Implants Industry Revenue Million Forecast, by End-Users 2019 & 2032

- Table 8: Spain Dental Implants Industry Volume K Units Forecast, by End-Users 2019 & 2032

- Table 9: Spain Dental Implants Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 10: Spain Dental Implants Industry Volume K Units Forecast, by Region 2019 & 2032

- Table 11: Spain Dental Implants Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 12: Spain Dental Implants Industry Volume K Units Forecast, by Country 2019 & 2032

- Table 13: Spain Dental Implants Industry Revenue Million Forecast, by Product 2019 & 2032

- Table 14: Spain Dental Implants Industry Volume K Units Forecast, by Product 2019 & 2032

- Table 15: Spain Dental Implants Industry Revenue Million Forecast, by Treatment 2019 & 2032

- Table 16: Spain Dental Implants Industry Volume K Units Forecast, by Treatment 2019 & 2032

- Table 17: Spain Dental Implants Industry Revenue Million Forecast, by End-Users 2019 & 2032

- Table 18: Spain Dental Implants Industry Volume K Units Forecast, by End-Users 2019 & 2032

- Table 19: Spain Dental Implants Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 20: Spain Dental Implants Industry Volume K Units Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Spain Dental Implants Industry?

The projected CAGR is approximately 6.69%.

2. Which companies are prominent players in the Spain Dental Implants Industry?

Key companies in the market include BioHorizons Implant Systems, Henry Schein Inc., 3M, Dentsply Sirona, NobelBiocare, Carestream Health, Straumann Holding AG, Zimmer Biomet, Terrats Medical SL.

3. What are the main segments of the Spain Dental Implants Industry?

The market segments include Product, Treatment, End-Users.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Burden of Oral Diseases and Ageing Population; Technological Advancements in Dentistry.

6. What are the notable trends driving market growth?

Prosthodontic Equipment is Expected to Witness a Significant Growth Over a Forecast Period.

7. Are there any restraints impacting market growth?

Increasing Cost of Surgeries.

8. Can you provide examples of recent developments in the market?

In June 2022, Henry Schein acquired Condor Dental, to expand its dental sales and service operations in Switzerland transaction to enhance its ability to serve pan-European Dental Service Organizations.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in K Units.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Spain Dental Implants Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Spain Dental Implants Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Spain Dental Implants Industry?

To stay informed about further developments, trends, and reports in the Spain Dental Implants Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence