Key Insights

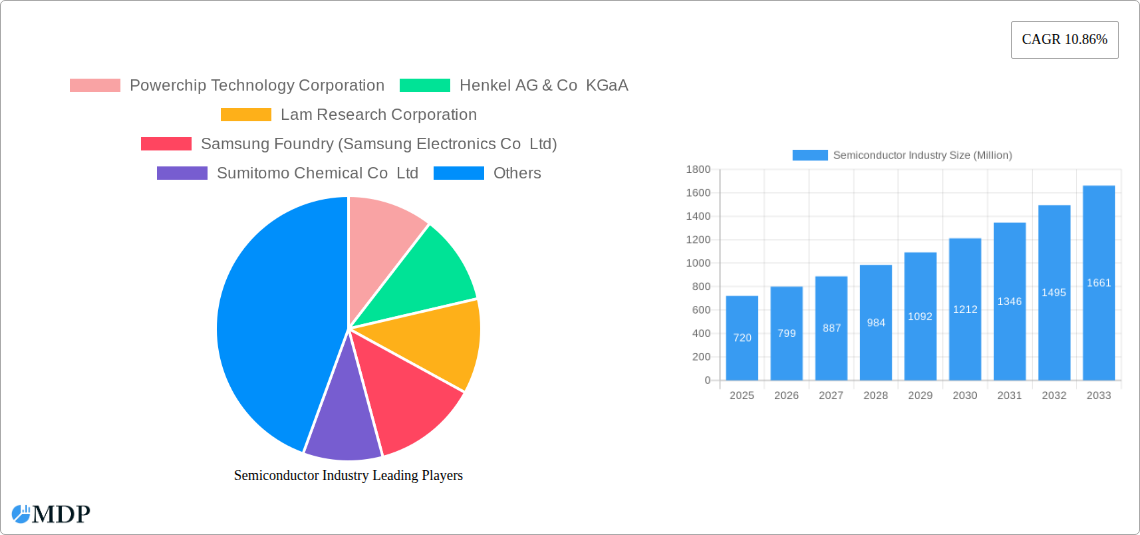

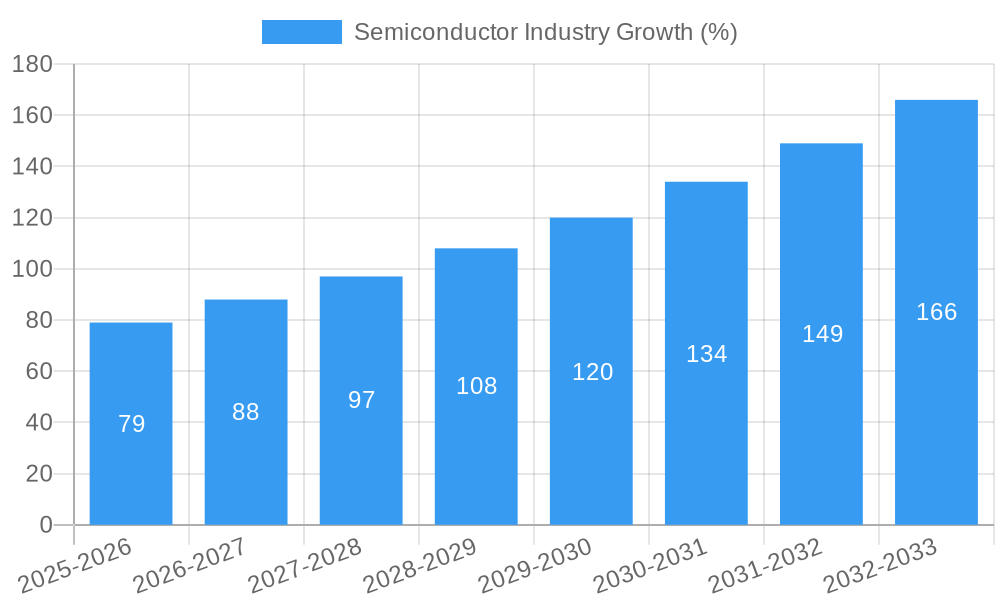

The semiconductor industry, valued at $720 million in 2025, is projected to experience robust growth, exhibiting a compound annual growth rate (CAGR) of 10.86% from 2025 to 2033. This expansion is driven by several key factors. The increasing demand for high-performance computing, particularly in data centers and artificial intelligence applications, is fueling significant investment in advanced semiconductor technologies. Furthermore, the proliferation of connected devices in the Internet of Things (IoT) ecosystem and the automotive industry's shift towards electric vehicles and autonomous driving are creating substantial demand for various semiconductor components, including sensors, microcontrollers, and integrated circuits. Growth in the semiconductor manufacturing equipment market mirrors this trend, reflecting substantial investment in upgrading fabrication capabilities to meet evolving technological needs. While supply chain disruptions and geopolitical uncertainties pose potential restraints, the long-term outlook for the industry remains optimistic, given the continuous innovation in semiconductor technology and its pervasive role across various sectors.

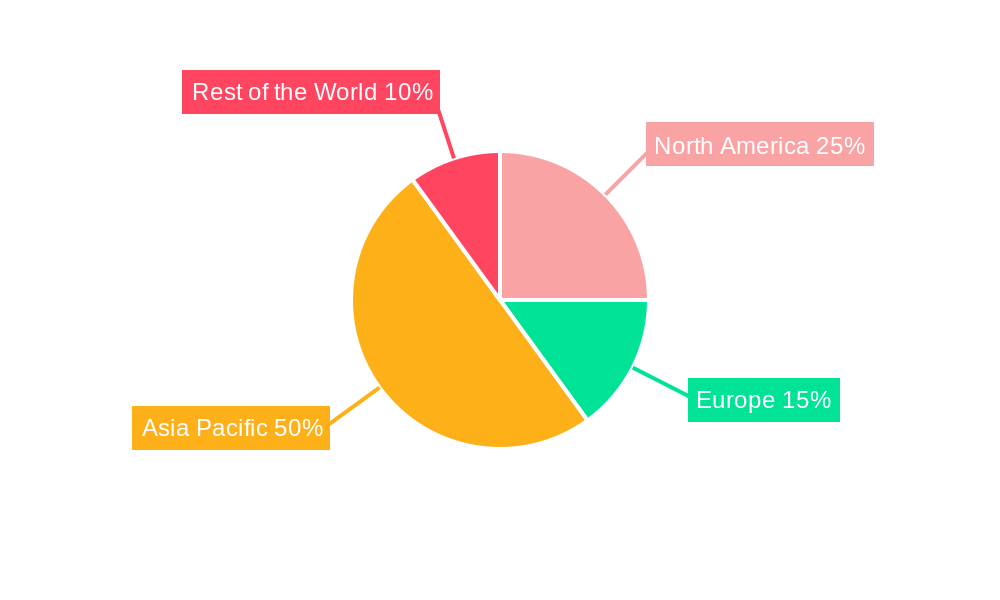

Market segmentation reveals a diverse landscape. The fabrication and packaging segments within semiconductor materials are expected to grow at comparable rates, reflecting the equal importance of both aspects in modern chip manufacturing. In semiconductor devices, integrated circuits (ICs) hold the largest market share, driven by their critical role in computing and communication technologies, followed by the growth in sensors and optoelectronics fueled by IoT and automotive advancements. Similarly, within semiconductor equipment, the front-end and back-end segments are poised for significant growth, but the specific proportion may shift based on the technology adoption cycle and investment trends. Leading players like TSMC, Samsung Foundry, Intel, and others are strategically investing in capacity expansion and advanced node technology to maintain their market leadership and cater to the booming demand. Regional growth patterns indicate a strong presence in Asia Pacific, driven by major manufacturing hubs in countries like Taiwan, South Korea, and China, followed by North America and Europe, where significant design and R&D activities take place. The industry's future will be shaped by continuous technological advancements in areas like 3D packaging, advanced materials, and novel architectures, aimed at enhancing performance, power efficiency, and cost-effectiveness.

Semiconductor Industry Market Report: 2019-2033

This comprehensive report provides an in-depth analysis of the global semiconductor industry, covering market dynamics, leading players, technological advancements, and future growth prospects. With a study period spanning 2019-2033, a base year of 2025, and a forecast period of 2025-2033, this report is an essential resource for industry stakeholders, investors, and researchers seeking to understand the complexities and opportunities within this crucial sector. The report leverages extensive data analysis to deliver actionable insights and strategic recommendations. Total market value is predicted to reach xx Million by 2033.

Semiconductor Industry Market Dynamics & Concentration

The global semiconductor market is characterized by high concentration among a few key players, intense competition, and continuous technological innovation. Market consolidation is driven by mergers and acquisitions (M&A) activity, with xx M&A deals recorded between 2019 and 2024. The top five players – TSMC, Samsung Foundry, Intel, GlobalFoundries, and UMC – collectively held an estimated xx% market share in the semiconductor foundry market in 2024. This dominance is challenged by the rise of regional players and government initiatives promoting domestic semiconductor manufacturing.

- Market Concentration: High, with a few dominant players.

- Innovation Drivers: Advancements in process technology (e.g., EUV lithography), materials science, and design methodologies.

- Regulatory Frameworks: Government policies and subsidies (e.g., the US CHIPS Act) are shaping investment and manufacturing location decisions.

- Product Substitutes: Limited direct substitutes, but alternative technologies and design approaches impact market segments.

- End-User Trends: Growing demand from automotive, consumer electronics, 5G infrastructure, and AI sectors are key growth drivers.

- M&A Activities: Significant M&A activity indicates consolidation and expansion strategies among leading players.

Semiconductor Industry Industry Trends & Analysis

The semiconductor industry is experiencing robust growth, driven by the increasing demand for high-performance computing, IoT devices, and artificial intelligence (AI). The market is expected to achieve a Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025-2033). This growth is fuelled by several factors: technological advancements, particularly in memory technologies (DRAM, NAND flash), the expanding adoption of 5G networks and the increasing computing power demand fueled by AI and machine learning applications, and the rise of new applications such as autonomous vehicles and industrial automation. Market penetration of advanced semiconductor technologies continues to increase, with xx% market penetration expected for EUV lithography by 2030. The competitive landscape is highly dynamic, with leading players continuously investing in R&D and pursuing strategic alliances to maintain their market positions.

Leading Markets & Segments in Semiconductor Industry

Asia, particularly Taiwan, South Korea, and China, dominates the semiconductor manufacturing landscape. This dominance is attributed to a confluence of factors:

- Economic Policies: Supportive government policies, including financial incentives and infrastructure development.

- Infrastructure: Well-established manufacturing clusters, skilled workforce, and advanced infrastructure.

Within the semiconductor industry, the Integrated Circuits segment is the largest, accounting for xx% of total market value in 2024. Other significant segments include:

- By Semiconductors Materials: Fabrication materials account for a larger share compared to packaging materials due to increasing demand for advanced node chips.

- By Semiconductor Devices: Integrated Circuits dominate due to their widespread use across various applications. Optoelectronics and sensors are also showing substantial growth potential.

- By Semiconductor Equipment: The front-end equipment segment is larger than the back-end segment due to higher capital expenditure requirements for advanced node manufacturing.

Semiconductor Industry Product Developments

Recent product innovations focus on enhanced performance, lower power consumption, and miniaturization. The adoption of EUV lithography for advanced node production, the development of advanced packaging technologies (e.g., 3D stacking), and the emergence of novel materials (e.g., GaN, SiC) are key technological trends shaping the market. These advancements are driving the development of more powerful and energy-efficient chips for high-growth application segments like AI, 5G, and automotive.

Key Drivers of Semiconductor Industry Growth

Several factors fuel the semiconductor industry's expansion:

- Technological Advancements: Continuous improvements in chip design, manufacturing processes, and materials science drive performance improvements and cost reductions.

- Economic Growth: Growing global economies and increased consumer spending fuel demand for electronics and related products.

- Government Support: Government initiatives and subsidies promote domestic semiconductor manufacturing and technological advancements (e.g., the US CHIPS Act).

Challenges in the Semiconductor Industry Market

The semiconductor industry faces several challenges:

- Geopolitical Risks: Trade tensions and supply chain disruptions impact manufacturing and distribution.

- Supply Chain Issues: Shortages of critical materials and manufacturing capacity constraints lead to production bottlenecks.

- Competitive Pressures: Intense competition among major players requires ongoing investment in R&D and innovation to remain competitive.

Emerging Opportunities in Semiconductor Industry

The long-term growth of the semiconductor industry is underpinned by numerous opportunities:

- Technological Breakthroughs: Advancements in AI, 5G, and other emerging technologies create significant demand for advanced semiconductor chips.

- Strategic Partnerships: Collaborations among leading players accelerate innovation and improve supply chain resilience.

- Market Expansion: Expanding into new and underserved markets (e.g., IoT, automotive, industrial automation) offers significant growth potential.

Leading Players in the Semiconductor Industry Sector

- Powerchip Technology Corporation

- Henkel AG & Co KGaA

- Lam Research Corporation

- Samsung Foundry (Samsung Electronics Co Ltd)

- Sumitomo Chemical Co Ltd

- Indium Corporation

- Advantest Corporation

- KLA Corporation

- Teradyne Inc

- Vendor Market Share - Semiconductor Equipment Market

- United Microelectronics Corporation (UMC)

- Micron Technology Inc

- Tongfu Microelectronics Co Ltd

- Kyocera Corporation

- Applied Materials Inc

- Tianshui Huatian Technology Co Ltd

- LG Chem Ltd

- Vendor Market Share - OSAT Market

- Samsung Electronics Co Ltd

- ASE Technology Holding Co Ltd

- Screen Holdings Co Ltd

- Hua Hong Semiconductor Limited

- Tokyo Electron Limited

- Broadcom Inc

- BASF SE

- Vendor Market Share - Semiconductor Devices Market

- Jiangsu Changjiang Electronics Technology Co Ltd

- Qualcomm Incorporated

- Semiconductor Manufacturing International Corporation (SMIC)

- SK Hynix Inc

- ASML Holding NV

- Texas Instruments Incorporated

- Powertech Technology Inc

- King Yuan Electronics Co Ltd

- Vendor Market Share

- Resonac Holding Corporation

- Amkor Technology Inc

- Vendor Market Share - Semiconductor Foundry Market

- Taiwan Semiconductor Manufacturing Company (TSMC) Limited

- Intel Corporation

- GlobalFoundries Inc

- Dow Chemical Co (Dow Inc )

- Mediatek Inc

Key Milestones in Semiconductor Industry Industry

- May 2023: Micron Technology, Inc. announced its adoption of Extreme Ultraviolet (EUV) technology for its 1-gamma node DRAM production in Japan, representing a USD 4.5 billion investment.

- March 2023: SK Hynix plans to build a USD 15 billion semiconductor chip facility in the US, leveraging incentives from the US CHIPS Act.

Strategic Outlook for Semiconductor Industry Market

The semiconductor industry's future is bright, driven by relentless technological innovation and expanding application areas. Strategic opportunities lie in focusing on advanced process technologies, developing innovative packaging solutions, and strategically expanding into high-growth markets. The industry's ability to address supply chain challenges and navigate geopolitical uncertainties will be crucial in realizing its full potential.

Semiconductor Industry Segmentation

-

1. Semiconductor Devices

- 1.1. Discrete Semiconductors

- 1.2. Optoelectronics

- 1.3. Sensors

- 1.4. Integrated Circuits

-

2. Semiconductor Equipment

- 2.1. Front-end Equipment

- 2.2. Back-end Equipment

-

3. Semiconductors Materials

- 3.1. Fabrication

- 3.2. Pacakging

- 4. Semiconductor Foundry Market

- 5. Outso

Semiconductor Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia

- 4. Australia and New Zealand

- 5. Latin America

- 6. Middle East and Africa

Semiconductor Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 10.86% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1 Increasing Needs of Consumer Electronic Devices Boosting the Manufacturing Prospects; Proliferation of AI

- 3.2.2 IoT

- 3.2.3 and Connected Devices Across Industry Verticals; Increased Applications of Semiconductors in Automotive; Increased Deployment of 5G and Rising Demand for 5G Smartphones

- 3.3. Market Restrains

- 3.3.1. Supply Chain Disruptions Resulting in Semiconductor Chip Shortage; Dynamic Nature of Technologies Requires Several Changes in Manufacturing Equipment; Vertical Integration is One of the Significant Concerns of OSAT Players

- 3.4. Market Trends

- 3.4.1. Discrete Semiconductors to Hold Significant Market Share in the Semiconductor Devices Segment

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Semiconductor Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Semiconductor Devices

- 5.1.1. Discrete Semiconductors

- 5.1.2. Optoelectronics

- 5.1.3. Sensors

- 5.1.4. Integrated Circuits

- 5.2. Market Analysis, Insights and Forecast - by Semiconductor Equipment

- 5.2.1. Front-end Equipment

- 5.2.2. Back-end Equipment

- 5.3. Market Analysis, Insights and Forecast - by Semiconductors Materials

- 5.3.1. Fabrication

- 5.3.2. Pacakging

- 5.4. Market Analysis, Insights and Forecast - by Semiconductor Foundry Market

- 5.5. Market Analysis, Insights and Forecast - by Outso

- 5.6. Market Analysis, Insights and Forecast - by Region

- 5.6.1. North America

- 5.6.2. Europe

- 5.6.3. Asia

- 5.6.4. Australia and New Zealand

- 5.6.5. Latin America

- 5.6.6. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Semiconductor Devices

- 6. North America Semiconductor Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Semiconductor Devices

- 6.1.1. Discrete Semiconductors

- 6.1.2. Optoelectronics

- 6.1.3. Sensors

- 6.1.4. Integrated Circuits

- 6.2. Market Analysis, Insights and Forecast - by Semiconductor Equipment

- 6.2.1. Front-end Equipment

- 6.2.2. Back-end Equipment

- 6.3. Market Analysis, Insights and Forecast - by Semiconductors Materials

- 6.3.1. Fabrication

- 6.3.2. Pacakging

- 6.4. Market Analysis, Insights and Forecast - by Semiconductor Foundry Market

- 6.5. Market Analysis, Insights and Forecast - by Outso

- 6.1. Market Analysis, Insights and Forecast - by Semiconductor Devices

- 7. Europe Semiconductor Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Semiconductor Devices

- 7.1.1. Discrete Semiconductors

- 7.1.2. Optoelectronics

- 7.1.3. Sensors

- 7.1.4. Integrated Circuits

- 7.2. Market Analysis, Insights and Forecast - by Semiconductor Equipment

- 7.2.1. Front-end Equipment

- 7.2.2. Back-end Equipment

- 7.3. Market Analysis, Insights and Forecast - by Semiconductors Materials

- 7.3.1. Fabrication

- 7.3.2. Pacakging

- 7.4. Market Analysis, Insights and Forecast - by Semiconductor Foundry Market

- 7.5. Market Analysis, Insights and Forecast - by Outso

- 7.1. Market Analysis, Insights and Forecast - by Semiconductor Devices

- 8. Asia Semiconductor Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Semiconductor Devices

- 8.1.1. Discrete Semiconductors

- 8.1.2. Optoelectronics

- 8.1.3. Sensors

- 8.1.4. Integrated Circuits

- 8.2. Market Analysis, Insights and Forecast - by Semiconductor Equipment

- 8.2.1. Front-end Equipment

- 8.2.2. Back-end Equipment

- 8.3. Market Analysis, Insights and Forecast - by Semiconductors Materials

- 8.3.1. Fabrication

- 8.3.2. Pacakging

- 8.4. Market Analysis, Insights and Forecast - by Semiconductor Foundry Market

- 8.5. Market Analysis, Insights and Forecast - by Outso

- 8.1. Market Analysis, Insights and Forecast - by Semiconductor Devices

- 9. Australia and New Zealand Semiconductor Industry Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Semiconductor Devices

- 9.1.1. Discrete Semiconductors

- 9.1.2. Optoelectronics

- 9.1.3. Sensors

- 9.1.4. Integrated Circuits

- 9.2. Market Analysis, Insights and Forecast - by Semiconductor Equipment

- 9.2.1. Front-end Equipment

- 9.2.2. Back-end Equipment

- 9.3. Market Analysis, Insights and Forecast - by Semiconductors Materials

- 9.3.1. Fabrication

- 9.3.2. Pacakging

- 9.4. Market Analysis, Insights and Forecast - by Semiconductor Foundry Market

- 9.5. Market Analysis, Insights and Forecast - by Outso

- 9.1. Market Analysis, Insights and Forecast - by Semiconductor Devices

- 10. Latin America Semiconductor Industry Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Semiconductor Devices

- 10.1.1. Discrete Semiconductors

- 10.1.2. Optoelectronics

- 10.1.3. Sensors

- 10.1.4. Integrated Circuits

- 10.2. Market Analysis, Insights and Forecast - by Semiconductor Equipment

- 10.2.1. Front-end Equipment

- 10.2.2. Back-end Equipment

- 10.3. Market Analysis, Insights and Forecast - by Semiconductors Materials

- 10.3.1. Fabrication

- 10.3.2. Pacakging

- 10.4. Market Analysis, Insights and Forecast - by Semiconductor Foundry Market

- 10.5. Market Analysis, Insights and Forecast - by Outso

- 10.1. Market Analysis, Insights and Forecast - by Semiconductor Devices

- 11. Middle East and Africa Semiconductor Industry Analysis, Insights and Forecast, 2019-2031

- 11.1. Market Analysis, Insights and Forecast - by Semiconductor Devices

- 11.1.1. Discrete Semiconductors

- 11.1.2. Optoelectronics

- 11.1.3. Sensors

- 11.1.4. Integrated Circuits

- 11.2. Market Analysis, Insights and Forecast - by Semiconductor Equipment

- 11.2.1. Front-end Equipment

- 11.2.2. Back-end Equipment

- 11.3. Market Analysis, Insights and Forecast - by Semiconductors Materials

- 11.3.1. Fabrication

- 11.3.2. Pacakging

- 11.4. Market Analysis, Insights and Forecast - by Semiconductor Foundry Market

- 11.5. Market Analysis, Insights and Forecast - by Outso

- 11.1. Market Analysis, Insights and Forecast - by Semiconductor Devices

- 12. North America Semiconductor Industry Analysis, Insights and Forecast, 2019-2031

- 12.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 12.1.1 United States

- 12.1.2 Canada

- 13. Europe Semiconductor Industry Analysis, Insights and Forecast, 2019-2031

- 13.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 13.1.1 Germany

- 13.1.2 United Kingdom

- 13.1.3 France

- 13.1.4 Rest of Europe

- 14. Asia Pacific Semiconductor Industry Analysis, Insights and Forecast, 2019-2031

- 14.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 14.1.1 China

- 14.1.2 Taiwan

- 14.1.3 South Korea

- 14.1.4 Rest of Asia Pacific

- 15. Rest of the World Semiconductor Industry Analysis, Insights and Forecast, 2019-2031

- 15.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 15.1.1.

- 16. Competitive Analysis

- 16.1. Market Share Analysis 2024

- 16.2. Company Profiles

- 16.2.1 Powerchip Technology Corporation

- 16.2.1.1. Overview

- 16.2.1.2. Products

- 16.2.1.3. SWOT Analysis

- 16.2.1.4. Recent Developments

- 16.2.1.5. Financials (Based on Availability)

- 16.2.2 Henkel AG & Co KGaA

- 16.2.2.1. Overview

- 16.2.2.2. Products

- 16.2.2.3. SWOT Analysis

- 16.2.2.4. Recent Developments

- 16.2.2.5. Financials (Based on Availability)

- 16.2.3 Lam Research Corporation

- 16.2.3.1. Overview

- 16.2.3.2. Products

- 16.2.3.3. SWOT Analysis

- 16.2.3.4. Recent Developments

- 16.2.3.5. Financials (Based on Availability)

- 16.2.4 Samsung Foundry (Samsung Electronics Co Ltd)

- 16.2.4.1. Overview

- 16.2.4.2. Products

- 16.2.4.3. SWOT Analysis

- 16.2.4.4. Recent Developments

- 16.2.4.5. Financials (Based on Availability)

- 16.2.5 Sumitomo Chemical Co Ltd

- 16.2.5.1. Overview

- 16.2.5.2. Products

- 16.2.5.3. SWOT Analysis

- 16.2.5.4. Recent Developments

- 16.2.5.5. Financials (Based on Availability)

- 16.2.6 Indium Corporation

- 16.2.6.1. Overview

- 16.2.6.2. Products

- 16.2.6.3. SWOT Analysis

- 16.2.6.4. Recent Developments

- 16.2.6.5. Financials (Based on Availability)

- 16.2.7 Advantest Corporation

- 16.2.7.1. Overview

- 16.2.7.2. Products

- 16.2.7.3. SWOT Analysis

- 16.2.7.4. Recent Developments

- 16.2.7.5. Financials (Based on Availability)

- 16.2.8 KLA Corporation

- 16.2.8.1. Overview

- 16.2.8.2. Products

- 16.2.8.3. SWOT Analysis

- 16.2.8.4. Recent Developments

- 16.2.8.5. Financials (Based on Availability)

- 16.2.9 Teradyne Inc

- 16.2.9.1. Overview

- 16.2.9.2. Products

- 16.2.9.3. SWOT Analysis

- 16.2.9.4. Recent Developments

- 16.2.9.5. Financials (Based on Availability)

- 16.2.10 Vendor Market Share - Semiconductor Equipment Market

- 16.2.10.1. Overview

- 16.2.10.2. Products

- 16.2.10.3. SWOT Analysis

- 16.2.10.4. Recent Developments

- 16.2.10.5. Financials (Based on Availability)

- 16.2.11 United Microelectronics Corporation (UMC)

- 16.2.11.1. Overview

- 16.2.11.2. Products

- 16.2.11.3. SWOT Analysis

- 16.2.11.4. Recent Developments

- 16.2.11.5. Financials (Based on Availability)

- 16.2.12 Micron Technology Inc

- 16.2.12.1. Overview

- 16.2.12.2. Products

- 16.2.12.3. SWOT Analysis

- 16.2.12.4. Recent Developments

- 16.2.12.5. Financials (Based on Availability)

- 16.2.13 Tongfu Microelectronics Co Ltd

- 16.2.13.1. Overview

- 16.2.13.2. Products

- 16.2.13.3. SWOT Analysis

- 16.2.13.4. Recent Developments

- 16.2.13.5. Financials (Based on Availability)

- 16.2.14 Kyocera Corporation

- 16.2.14.1. Overview

- 16.2.14.2. Products

- 16.2.14.3. SWOT Analysis

- 16.2.14.4. Recent Developments

- 16.2.14.5. Financials (Based on Availability)

- 16.2.15 Applied Materials Inc

- 16.2.15.1. Overview

- 16.2.15.2. Products

- 16.2.15.3. SWOT Analysis

- 16.2.15.4. Recent Developments

- 16.2.15.5. Financials (Based on Availability)

- 16.2.16 Tianshui Huatian Technology Co Ltd

- 16.2.16.1. Overview

- 16.2.16.2. Products

- 16.2.16.3. SWOT Analysis

- 16.2.16.4. Recent Developments

- 16.2.16.5. Financials (Based on Availability)

- 16.2.17 LG Chem Ltd

- 16.2.17.1. Overview

- 16.2.17.2. Products

- 16.2.17.3. SWOT Analysis

- 16.2.17.4. Recent Developments

- 16.2.17.5. Financials (Based on Availability)

- 16.2.18 Vendor Market Share - OSAT Marke

- 16.2.18.1. Overview

- 16.2.18.2. Products

- 16.2.18.3. SWOT Analysis

- 16.2.18.4. Recent Developments

- 16.2.18.5. Financials (Based on Availability)

- 16.2.19 Samsung Electronics Co Ltd

- 16.2.19.1. Overview

- 16.2.19.2. Products

- 16.2.19.3. SWOT Analysis

- 16.2.19.4. Recent Developments

- 16.2.19.5. Financials (Based on Availability)

- 16.2.20 ASE Technology Holding Co Ltd

- 16.2.20.1. Overview

- 16.2.20.2. Products

- 16.2.20.3. SWOT Analysis

- 16.2.20.4. Recent Developments

- 16.2.20.5. Financials (Based on Availability)

- 16.2.21 Screen Holdings Co Ltd

- 16.2.21.1. Overview

- 16.2.21.2. Products

- 16.2.21.3. SWOT Analysis

- 16.2.21.4. Recent Developments

- 16.2.21.5. Financials (Based on Availability)

- 16.2.22 Hua Hong Semiconductor Limited

- 16.2.22.1. Overview

- 16.2.22.2. Products

- 16.2.22.3. SWOT Analysis

- 16.2.22.4. Recent Developments

- 16.2.22.5. Financials (Based on Availability)

- 16.2.23 Tokyo Electron Limited

- 16.2.23.1. Overview

- 16.2.23.2. Products

- 16.2.23.3. SWOT Analysis

- 16.2.23.4. Recent Developments

- 16.2.23.5. Financials (Based on Availability)

- 16.2.24 Broadcom Inc

- 16.2.24.1. Overview

- 16.2.24.2. Products

- 16.2.24.3. SWOT Analysis

- 16.2.24.4. Recent Developments

- 16.2.24.5. Financials (Based on Availability)

- 16.2.25 BASF SE

- 16.2.25.1. Overview

- 16.2.25.2. Products

- 16.2.25.3. SWOT Analysis

- 16.2.25.4. Recent Developments

- 16.2.25.5. Financials (Based on Availability)

- 16.2.26 Vendor Market Share - Semiconductor Devices Market

- 16.2.26.1. Overview

- 16.2.26.2. Products

- 16.2.26.3. SWOT Analysis

- 16.2.26.4. Recent Developments

- 16.2.26.5. Financials (Based on Availability)

- 16.2.27 Jiangsu Changjiang Electronics Technology Co Ltd

- 16.2.27.1. Overview

- 16.2.27.2. Products

- 16.2.27.3. SWOT Analysis

- 16.2.27.4. Recent Developments

- 16.2.27.5. Financials (Based on Availability)

- 16.2.28 Qualcomm Incorporated

- 16.2.28.1. Overview

- 16.2.28.2. Products

- 16.2.28.3. SWOT Analysis

- 16.2.28.4. Recent Developments

- 16.2.28.5. Financials (Based on Availability)

- 16.2.29 Semiconductor Manufacturing International Corporation (SMIC)

- 16.2.29.1. Overview

- 16.2.29.2. Products

- 16.2.29.3. SWOT Analysis

- 16.2.29.4. Recent Developments

- 16.2.29.5. Financials (Based on Availability)

- 16.2.30 SK Hynix Inc

- 16.2.30.1. Overview

- 16.2.30.2. Products

- 16.2.30.3. SWOT Analysis

- 16.2.30.4. Recent Developments

- 16.2.30.5. Financials (Based on Availability)

- 16.2.31 ASML Holding NV

- 16.2.31.1. Overview

- 16.2.31.2. Products

- 16.2.31.3. SWOT Analysis

- 16.2.31.4. Recent Developments

- 16.2.31.5. Financials (Based on Availability)

- 16.2.32 Texas Instruments Incorporated

- 16.2.32.1. Overview

- 16.2.32.2. Products

- 16.2.32.3. SWOT Analysis

- 16.2.32.4. Recent Developments

- 16.2.32.5. Financials (Based on Availability)

- 16.2.33 Powertech Technology Inc

- 16.2.33.1. Overview

- 16.2.33.2. Products

- 16.2.33.3. SWOT Analysis

- 16.2.33.4. Recent Developments

- 16.2.33.5. Financials (Based on Availability)

- 16.2.34 King Yuan Electronics Co Ltd7 2 Vendor Market Share

- 16.2.34.1. Overview

- 16.2.34.2. Products

- 16.2.34.3. SWOT Analysis

- 16.2.34.4. Recent Developments

- 16.2.34.5. Financials (Based on Availability)

- 16.2.35 Resonac Holding Corporation

- 16.2.35.1. Overview

- 16.2.35.2. Products

- 16.2.35.3. SWOT Analysis

- 16.2.35.4. Recent Developments

- 16.2.35.5. Financials (Based on Availability)

- 16.2.36 Amkor Technology Inc

- 16.2.36.1. Overview

- 16.2.36.2. Products

- 16.2.36.3. SWOT Analysis

- 16.2.36.4. Recent Developments

- 16.2.36.5. Financials (Based on Availability)

- 16.2.37 Vendor Market Share - Semiconductor Foundry Market

- 16.2.37.1. Overview

- 16.2.37.2. Products

- 16.2.37.3. SWOT Analysis

- 16.2.37.4. Recent Developments

- 16.2.37.5. Financials (Based on Availability)

- 16.2.38 Taiwan Semiconductor Manufacturing Company (TSMC) Limited

- 16.2.38.1. Overview

- 16.2.38.2. Products

- 16.2.38.3. SWOT Analysis

- 16.2.38.4. Recent Developments

- 16.2.38.5. Financials (Based on Availability)

- 16.2.39 Intel Corporation

- 16.2.39.1. Overview

- 16.2.39.2. Products

- 16.2.39.3. SWOT Analysis

- 16.2.39.4. Recent Developments

- 16.2.39.5. Financials (Based on Availability)

- 16.2.40 GlobalFoundries Inc

- 16.2.40.1. Overview

- 16.2.40.2. Products

- 16.2.40.3. SWOT Analysis

- 16.2.40.4. Recent Developments

- 16.2.40.5. Financials (Based on Availability)

- 16.2.41 Dow Chemical Co (Dow Inc )

- 16.2.41.1. Overview

- 16.2.41.2. Products

- 16.2.41.3. SWOT Analysis

- 16.2.41.4. Recent Developments

- 16.2.41.5. Financials (Based on Availability)

- 16.2.42 Mediatek Inc

- 16.2.42.1. Overview

- 16.2.42.2. Products

- 16.2.42.3. SWOT Analysis

- 16.2.42.4. Recent Developments

- 16.2.42.5. Financials (Based on Availability)

- 16.2.1 Powerchip Technology Corporation

List of Figures

- Figure 1: Semiconductor Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Semiconductor Industry Share (%) by Company 2024

List of Tables

- Table 1: Semiconductor Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Semiconductor Industry Revenue Million Forecast, by Semiconductor Devices 2019 & 2032

- Table 3: Semiconductor Industry Revenue Million Forecast, by Semiconductor Equipment 2019 & 2032

- Table 4: Semiconductor Industry Revenue Million Forecast, by Semiconductors Materials 2019 & 2032

- Table 5: Semiconductor Industry Revenue Million Forecast, by Semiconductor Foundry Market 2019 & 2032

- Table 6: Semiconductor Industry Revenue Million Forecast, by Outso 2019 & 2032

- Table 7: Semiconductor Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 8: Semiconductor Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 9: United States Semiconductor Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Canada Semiconductor Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Semiconductor Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 12: Germany Semiconductor Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: United Kingdom Semiconductor Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: France Semiconductor Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 15: Rest of Europe Semiconductor Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 16: Semiconductor Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 17: China Semiconductor Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: Taiwan Semiconductor Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: South Korea Semiconductor Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Rest of Asia Pacific Semiconductor Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 21: Semiconductor Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 22: Semiconductor Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: Semiconductor Industry Revenue Million Forecast, by Semiconductor Devices 2019 & 2032

- Table 24: Semiconductor Industry Revenue Million Forecast, by Semiconductor Equipment 2019 & 2032

- Table 25: Semiconductor Industry Revenue Million Forecast, by Semiconductors Materials 2019 & 2032

- Table 26: Semiconductor Industry Revenue Million Forecast, by Semiconductor Foundry Market 2019 & 2032

- Table 27: Semiconductor Industry Revenue Million Forecast, by Outso 2019 & 2032

- Table 28: Semiconductor Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 29: Semiconductor Industry Revenue Million Forecast, by Semiconductor Devices 2019 & 2032

- Table 30: Semiconductor Industry Revenue Million Forecast, by Semiconductor Equipment 2019 & 2032

- Table 31: Semiconductor Industry Revenue Million Forecast, by Semiconductors Materials 2019 & 2032

- Table 32: Semiconductor Industry Revenue Million Forecast, by Semiconductor Foundry Market 2019 & 2032

- Table 33: Semiconductor Industry Revenue Million Forecast, by Outso 2019 & 2032

- Table 34: Semiconductor Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 35: Semiconductor Industry Revenue Million Forecast, by Semiconductor Devices 2019 & 2032

- Table 36: Semiconductor Industry Revenue Million Forecast, by Semiconductor Equipment 2019 & 2032

- Table 37: Semiconductor Industry Revenue Million Forecast, by Semiconductors Materials 2019 & 2032

- Table 38: Semiconductor Industry Revenue Million Forecast, by Semiconductor Foundry Market 2019 & 2032

- Table 39: Semiconductor Industry Revenue Million Forecast, by Outso 2019 & 2032

- Table 40: Semiconductor Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 41: Semiconductor Industry Revenue Million Forecast, by Semiconductor Devices 2019 & 2032

- Table 42: Semiconductor Industry Revenue Million Forecast, by Semiconductor Equipment 2019 & 2032

- Table 43: Semiconductor Industry Revenue Million Forecast, by Semiconductors Materials 2019 & 2032

- Table 44: Semiconductor Industry Revenue Million Forecast, by Semiconductor Foundry Market 2019 & 2032

- Table 45: Semiconductor Industry Revenue Million Forecast, by Outso 2019 & 2032

- Table 46: Semiconductor Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 47: Semiconductor Industry Revenue Million Forecast, by Semiconductor Devices 2019 & 2032

- Table 48: Semiconductor Industry Revenue Million Forecast, by Semiconductor Equipment 2019 & 2032

- Table 49: Semiconductor Industry Revenue Million Forecast, by Semiconductors Materials 2019 & 2032

- Table 50: Semiconductor Industry Revenue Million Forecast, by Semiconductor Foundry Market 2019 & 2032

- Table 51: Semiconductor Industry Revenue Million Forecast, by Outso 2019 & 2032

- Table 52: Semiconductor Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 53: Semiconductor Industry Revenue Million Forecast, by Semiconductor Devices 2019 & 2032

- Table 54: Semiconductor Industry Revenue Million Forecast, by Semiconductor Equipment 2019 & 2032

- Table 55: Semiconductor Industry Revenue Million Forecast, by Semiconductors Materials 2019 & 2032

- Table 56: Semiconductor Industry Revenue Million Forecast, by Semiconductor Foundry Market 2019 & 2032

- Table 57: Semiconductor Industry Revenue Million Forecast, by Outso 2019 & 2032

- Table 58: Semiconductor Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Semiconductor Industry?

The projected CAGR is approximately 10.86%.

2. Which companies are prominent players in the Semiconductor Industry?

Key companies in the market include Powerchip Technology Corporation, Henkel AG & Co KGaA, Lam Research Corporation, Samsung Foundry (Samsung Electronics Co Ltd), Sumitomo Chemical Co Ltd, Indium Corporation, Advantest Corporation, KLA Corporation, Teradyne Inc, Vendor Market Share - Semiconductor Equipment Market, United Microelectronics Corporation (UMC), Micron Technology Inc, Tongfu Microelectronics Co Ltd, Kyocera Corporation, Applied Materials Inc, Tianshui Huatian Technology Co Ltd, LG Chem Ltd, Vendor Market Share - OSAT Marke, Samsung Electronics Co Ltd, ASE Technology Holding Co Ltd, Screen Holdings Co Ltd, Hua Hong Semiconductor Limited, Tokyo Electron Limited, Broadcom Inc, BASF SE, Vendor Market Share - Semiconductor Devices Market, Jiangsu Changjiang Electronics Technology Co Ltd, Qualcomm Incorporated, Semiconductor Manufacturing International Corporation (SMIC), SK Hynix Inc, ASML Holding NV, Texas Instruments Incorporated, Powertech Technology Inc, King Yuan Electronics Co Ltd7 2 Vendor Market Share, Resonac Holding Corporation, Amkor Technology Inc, Vendor Market Share - Semiconductor Foundry Market, Taiwan Semiconductor Manufacturing Company (TSMC) Limited, Intel Corporation, GlobalFoundries Inc, Dow Chemical Co (Dow Inc ), Mediatek Inc.

3. What are the main segments of the Semiconductor Industry?

The market segments include Semiconductor Devices, Semiconductor Equipment, Semiconductors Materials, Semiconductor Foundry Market, Outso.

4. Can you provide details about the market size?

The market size is estimated to be USD 0.72 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Needs of Consumer Electronic Devices Boosting the Manufacturing Prospects; Proliferation of AI. IoT. and Connected Devices Across Industry Verticals; Increased Applications of Semiconductors in Automotive; Increased Deployment of 5G and Rising Demand for 5G Smartphones.

6. What are the notable trends driving market growth?

Discrete Semiconductors to Hold Significant Market Share in the Semiconductor Devices Segment.

7. Are there any restraints impacting market growth?

Supply Chain Disruptions Resulting in Semiconductor Chip Shortage; Dynamic Nature of Technologies Requires Several Changes in Manufacturing Equipment; Vertical Integration is One of the Significant Concerns of OSAT Players.

8. Can you provide examples of recent developments in the market?

May 2023: Micron Technology, Inc. announced its adoption of Extreme Ultraviolet (EUV) technology, a sophisticated patterning technique for producing its 1-gamma node DRAM. Given the pivotal role of its Hiroshima fab in advancing the 1-gamma node, Micron became the first semiconductor manufacturer to introduce EUV technology to Japan for manufacturing purposes. Over the upcoming years, Micron anticipates investing up to JPY 500 billion (USD 4.5 billion) in 1-gamma process technology. Supported by the Japanese government, this investment aims to fuel the next wave of end-to-end technological innovation, especially in the rapidly evolving field of generative artificial intelligence (AI) applications."

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Semiconductor Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Semiconductor Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Semiconductor Industry?

To stay informed about further developments, trends, and reports in the Semiconductor Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence