Key Insights

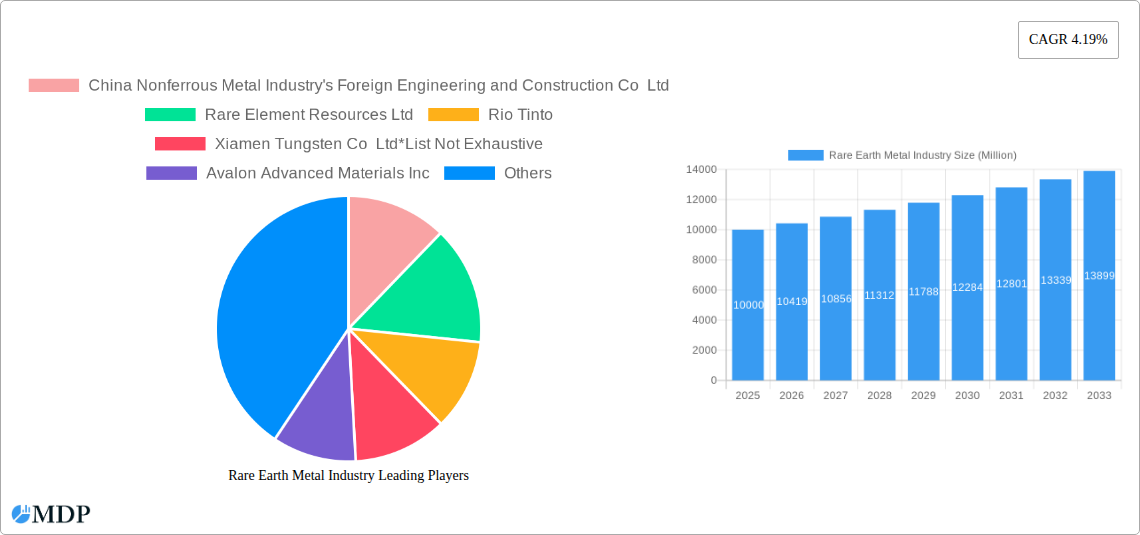

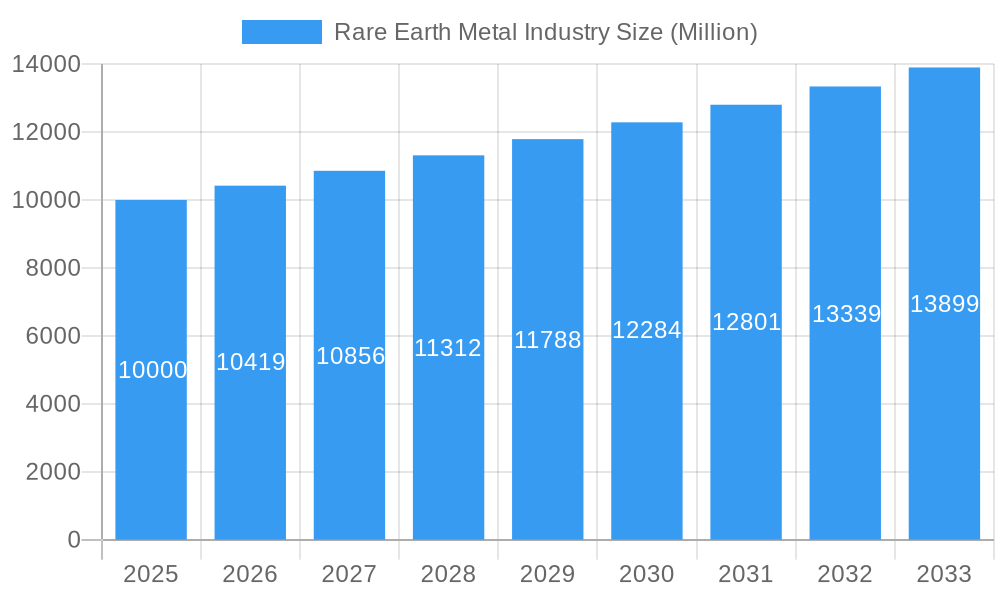

The rare earth metal industry, currently valued at approximately $XX million (estimated based on provided CAGR and market size), is experiencing steady growth, projected at a 4.19% CAGR from 2025 to 2033. This expansion is driven by escalating demand across diverse sectors. The automotive industry, particularly electric vehicles (EVs) and hybrid vehicles, is a major catalyst, requiring rare earth elements for powerful and efficient magnets in electric motors. Furthermore, advancements in renewable energy technologies, including wind turbines and solar panels, significantly contribute to the industry's growth trajectory. The increasing adoption of green technologies globally fuels demand for neodymium, dysprosium, and terbium, essential components in these applications. Technological advancements in electronics and consumer electronics also play a key role, with rare earth elements crucial for high-performance magnets and specialized displays. While China remains a dominant player in rare earth mining and processing, geographical diversification is a notable trend, with companies in North America, Australia, and other regions actively investing in exploration and development to reduce reliance on a single source. However, the industry faces challenges including fluctuating prices, environmental concerns related to mining practices, and geopolitical risks associated with supply chain dependence on specific countries. Segmentation within the industry reveals substantial growth opportunities in high-tech applications like advanced magnets for EVs, contributing to the overall market expansion.

Rare Earth Metal Industry Market Size (In Billion)

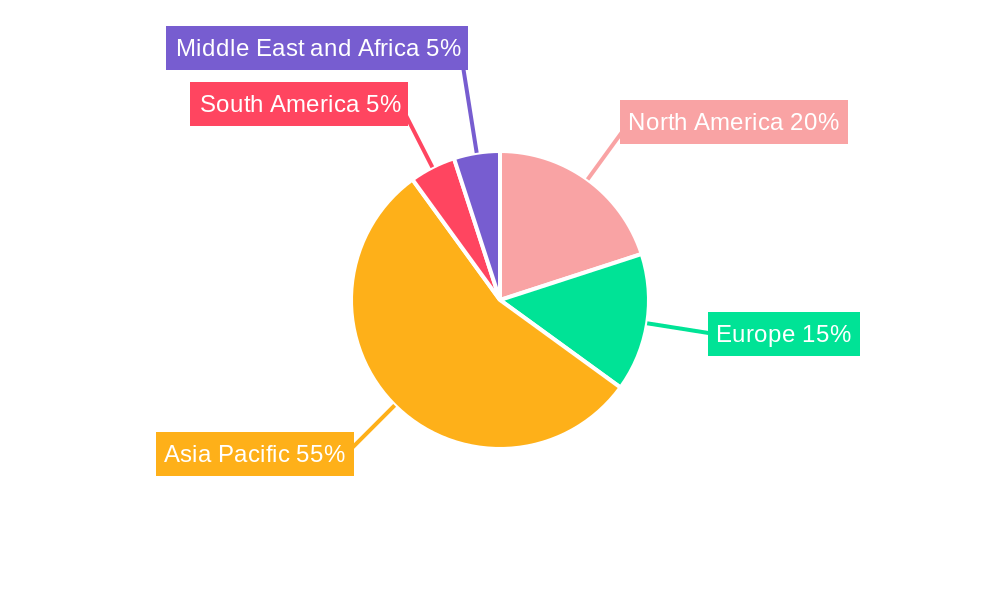

The market segmentation reveals distinct dynamics. Cerium, employed extensively in catalysts and polishing applications, comprises a significant portion of the market. Neodymium and dysprosium are pivotal in high-performance magnets, experiencing rapid growth due to the aforementioned EV and renewable energy sectors. Other elements like terbium, yttrium, and scandium also find specialized applications, contributing to market diversity. Lanthanum, prevalent in alloys, further diversifies market segments, while catalysts, ceramics, phosphors, and metallurgy represent key applications. Geographical distribution showcases a concentrated presence in the Asia-Pacific region, particularly China, driven by established mining and processing infrastructure. However, North America and Europe are witnessing rising investment in rare earth metal production, aiming for a more balanced global supply chain. The forecast period (2025-2033) anticipates robust market expansion, influenced by ongoing technological advancements and the global shift towards sustainable energy solutions. Effective resource management and sustainable mining practices will be crucial for the industry's long-term viability and environmental responsibility.

Rare Earth Metal Industry Company Market Share

Rare Earth Metal Industry Market Report: 2019-2033

Dive deep into the dynamic Rare Earth Metal industry with this comprehensive report, providing in-depth analysis and actionable insights for the period 2019-2033. This report covers market dynamics, leading players, key trends, and future growth opportunities, making it an essential resource for industry stakeholders, investors, and researchers. With a focus on key elements like Cerium, Neodymium, Dysprosium, Terbium, Yttrium, Scandium, and Lanthanum, and applications spanning catalysts, magnets, and ceramics, this report provides a 360° view of the market. The report uses 2025 as the base year and projects the market until 2033.

Rare Earth Metal Industry Market Dynamics & Concentration

The rare earth metal market is characterized by moderate concentration, with a few dominant players controlling a significant portion of the global supply. China holds a substantial market share, particularly in the mining and processing of rare earth elements. However, growing geopolitical concerns and a push for diversification are driving investments in mining and processing outside of China, leading to a gradual shift in the market landscape. Innovation is fueled by the increasing demand for high-performance magnets in electric vehicles and wind turbines. Stringent environmental regulations are impacting production methods, pushing companies to adopt cleaner and more sustainable practices. While some substitution is possible for certain applications, the unique properties of rare earth elements often make them irreplaceable. The end-user demand is driven by the burgeoning electronics, renewable energy, and automotive sectors. The past five years have witnessed a notable increase in M&A activity, with xx major deals in the past five years alone. This reflects industry consolidation and a push for securing resources and expanding downstream processing capabilities.

- Market Share: China: xx%, Other Countries: xx% (This is a combined figure for all countries outside of China).

- M&A Deal Count (2019-2024): xx

- Innovation Drivers: Electrification of transportation, renewable energy expansion, technological advancements in electronics.

- Regulatory Frameworks: Increasingly stringent environmental regulations, trade policies impacting import/export.

Rare Earth Metal Industry Industry Trends & Analysis

The rare earth metal industry exhibits a strong growth trajectory, projected to achieve a CAGR of xx% during the forecast period (2025-2033). This growth is primarily driven by the escalating demand from the electric vehicle (EV) sector and renewable energy technologies such as wind turbines. Technological disruptions, including advancements in extraction and separation techniques, are enhancing efficiency and lowering production costs. Consumer preferences for sustainable and environmentally friendly products are also positively influencing market growth, boosting the demand for rare earth elements in green technologies. Competitive dynamics are intensifying, with companies focusing on vertical integration to secure the supply chain and develop downstream processing capabilities. The market penetration of rare earth magnets in EVs is expected to reach xx% by 2033.

Leading Markets & Segments in Rare Earth Metal Industry

China remains the dominant player in the rare earth metal market, holding a significant share across various segments, including mining, refining, and manufacturing. However, other countries like Australia and the US are making significant strides to increase their production capacity and reduce reliance on China.

Key Drivers for Dominant Regions/Segments:

- China: Established infrastructure, abundant resources, government support.

- Australia: Large reserves, supportive government policies, investment in new refinery capacity.

- United States: Focus on domestic supply chain resilience, government incentives.

Segment Dominance:

- Element: Neodymium and Dysprosium are experiencing the highest growth due to their crucial role in permanent magnets. Cerium finds extensive use in catalysts and polishing compounds.

- Application: The magnet segment, fueled by EV and renewable energy demand, is the fastest-growing application area, followed by catalysts and ceramics.

Rare Earth Metal Industry Product Developments

Recent product innovations focus on enhancing the efficiency of extraction and separation processes, reducing costs, and improving the performance of rare earth-based materials. Advancements in magnet technology aim to improve magnetic strength, temperature resistance, and cost-effectiveness. New applications are constantly being explored, with ongoing research into advanced materials for energy storage, electronics, and aerospace.

Key Drivers of Rare Earth Metal Industry Growth

Several factors propel the growth of the rare earth metal industry. The burgeoning electric vehicle (EV) market is a significant driver, with rare earth magnets critical for EV motor applications. The expanding renewable energy sector relies heavily on rare earth elements for wind turbine generators and other applications. Government initiatives promoting the adoption of green technologies, along with supportive policies encouraging domestic production and resource security, are further bolstering growth.

Challenges in the Rare Earth Metal Industry Market

The rare earth metal industry faces several challenges. Supply chain vulnerabilities, particularly the concentration of production in a few countries, pose a risk to supply stability. Environmental regulations and concerns about mining's environmental impact necessitate investments in sustainable practices. Fluctuating prices and the intensifying competition among producers also represent major market challenges. The potential for disruptions caused by geopolitical instability adds to the overall complexity.

Emerging Opportunities in Rare Earth Metal Industry

The long-term growth of the rare earth metal industry is poised for expansion due to several factors. Technological advancements in extraction, processing, and magnet technology continually improve efficiency and performance. Strategic partnerships between mining companies, manufacturers, and end-users will enhance supply chain integration and reliability. The expansion of rare earth mining and processing into new regions, aiming for a diversified and more geographically balanced industry, offers substantial opportunities.

Leading Players in the Rare Earth Metal Industry Sector

- China Nonferrous Metal Industry's Foreign Engineering and Construction Co Ltd

- Rare Element Resources Ltd

- Rio Tinto

- Xiamen Tungsten Co Ltd

- Avalon Advanced Materials Inc

- Lynas Rare Earths Ltd

- Iluka Resources Limited

- Ucore Rare Metals Inc

- Peak Resources

- Shin-Etsu Chemical Co Ltd

- Minmetals Land Limited

- NORTHERN MINERALS

- Eutectix

- ARAFURA RESOURCES

- MEDALLION RESOURCES LTD

- Aluminum Corporation of China Ltd

Key Milestones in Rare Earth Metal Industry Industry

- August 2022: Lynas Rare Earths Ltd announces expansion of its Mt Weld mine in Western Australia, boosting neodymium and praseodymium production. This signals increased capacity and supply to meet growing demand.

- April 2022: Iluka Resources Ltd announces a USD 1.2 Billion investment in Eneabba Phase 3 rare earth refinery, signifying a major step toward downstream processing in Australia and enhancing the country's position in the global rare earth supply chain.

Strategic Outlook for Rare Earth Metal Industry Market

The future of the rare earth metal industry is bright, driven by sustained growth in the EV and renewable energy sectors. Strategic investments in sustainable mining and processing techniques, coupled with technological advancements, will shape the industry landscape. Geographical diversification of production and the development of robust supply chains are crucial factors in ensuring long-term growth and stability. The market's future potential is substantial, with opportunities for innovation, expansion, and the creation of new value chains.

Rare Earth Metal Industry Segmentation

-

1. Element

-

1.1. Cerium

- 1.1.1. Oxide

- 1.1.2. Sulfide

- 1.1.3. Other Elements

-

1.2. Neodymium

- 1.2.1. Alloy

- 1.3. Lanthanum

- 1.4. Dysprosium

- 1.5. Terbium

- 1.6. Yttrium

- 1.7. Scandium

-

1.1. Cerium

-

2. Application

- 2.1. Catalysts

- 2.2. Ceramics

- 2.3. Phosphors

- 2.4. Glass and Polishing

- 2.5. Metallurgy

- 2.6. Magnets

- 2.7. Other Applications

Rare Earth Metal Industry Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. India

- 1.3. Japan

- 1.4. South Korea

- 1.5. Rest of Asia Pacific

-

2. North America

- 2.1. United States

- 2.2. Canada

- 2.3. Mexico

-

3. Europe

- 3.1. Germany

- 3.2. United Kingdom

- 3.3. France

- 3.4. Italy

- 3.5. Rest of Europe

-

4. South America

- 4.1. Brazil

- 4.2. Argentina

- 4.3. Rest of South America

-

5. Middle East and Africa

- 5.1. Saudi Arabia

- 5.2. South Africa

- 5.3. Rest of Middle East and Africa

Rare Earth Metal Industry Regional Market Share

Geographic Coverage of Rare Earth Metal Industry

Rare Earth Metal Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.19% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. High Demand from Emerging Economies; Dependency of 'Green Technology' on Rare Earth Elements

- 3.3. Market Restrains

- 3.3.1. Inconsistent Supply of Rare Earth Elements

- 3.4. Market Trends

- 3.4.1. Increasing Demand for Magnets

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Rare Earth Metal Industry Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Element

- 5.1.1. Cerium

- 5.1.1.1. Oxide

- 5.1.1.2. Sulfide

- 5.1.1.3. Other Elements

- 5.1.2. Neodymium

- 5.1.2.1. Alloy

- 5.1.3. Lanthanum

- 5.1.4. Dysprosium

- 5.1.5. Terbium

- 5.1.6. Yttrium

- 5.1.7. Scandium

- 5.1.1. Cerium

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Catalysts

- 5.2.2. Ceramics

- 5.2.3. Phosphors

- 5.2.4. Glass and Polishing

- 5.2.5. Metallurgy

- 5.2.6. Magnets

- 5.2.7. Other Applications

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Asia Pacific

- 5.3.2. North America

- 5.3.3. Europe

- 5.3.4. South America

- 5.3.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Element

- 6. Asia Pacific Rare Earth Metal Industry Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Element

- 6.1.1. Cerium

- 6.1.1.1. Oxide

- 6.1.1.2. Sulfide

- 6.1.1.3. Other Elements

- 6.1.2. Neodymium

- 6.1.2.1. Alloy

- 6.1.3. Lanthanum

- 6.1.4. Dysprosium

- 6.1.5. Terbium

- 6.1.6. Yttrium

- 6.1.7. Scandium

- 6.1.1. Cerium

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Catalysts

- 6.2.2. Ceramics

- 6.2.3. Phosphors

- 6.2.4. Glass and Polishing

- 6.2.5. Metallurgy

- 6.2.6. Magnets

- 6.2.7. Other Applications

- 6.1. Market Analysis, Insights and Forecast - by Element

- 7. North America Rare Earth Metal Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Element

- 7.1.1. Cerium

- 7.1.1.1. Oxide

- 7.1.1.2. Sulfide

- 7.1.1.3. Other Elements

- 7.1.2. Neodymium

- 7.1.2.1. Alloy

- 7.1.3. Lanthanum

- 7.1.4. Dysprosium

- 7.1.5. Terbium

- 7.1.6. Yttrium

- 7.1.7. Scandium

- 7.1.1. Cerium

- 7.2. Market Analysis, Insights and Forecast - by Application

- 7.2.1. Catalysts

- 7.2.2. Ceramics

- 7.2.3. Phosphors

- 7.2.4. Glass and Polishing

- 7.2.5. Metallurgy

- 7.2.6. Magnets

- 7.2.7. Other Applications

- 7.1. Market Analysis, Insights and Forecast - by Element

- 8. Europe Rare Earth Metal Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Element

- 8.1.1. Cerium

- 8.1.1.1. Oxide

- 8.1.1.2. Sulfide

- 8.1.1.3. Other Elements

- 8.1.2. Neodymium

- 8.1.2.1. Alloy

- 8.1.3. Lanthanum

- 8.1.4. Dysprosium

- 8.1.5. Terbium

- 8.1.6. Yttrium

- 8.1.7. Scandium

- 8.1.1. Cerium

- 8.2. Market Analysis, Insights and Forecast - by Application

- 8.2.1. Catalysts

- 8.2.2. Ceramics

- 8.2.3. Phosphors

- 8.2.4. Glass and Polishing

- 8.2.5. Metallurgy

- 8.2.6. Magnets

- 8.2.7. Other Applications

- 8.1. Market Analysis, Insights and Forecast - by Element

- 9. South America Rare Earth Metal Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Element

- 9.1.1. Cerium

- 9.1.1.1. Oxide

- 9.1.1.2. Sulfide

- 9.1.1.3. Other Elements

- 9.1.2. Neodymium

- 9.1.2.1. Alloy

- 9.1.3. Lanthanum

- 9.1.4. Dysprosium

- 9.1.5. Terbium

- 9.1.6. Yttrium

- 9.1.7. Scandium

- 9.1.1. Cerium

- 9.2. Market Analysis, Insights and Forecast - by Application

- 9.2.1. Catalysts

- 9.2.2. Ceramics

- 9.2.3. Phosphors

- 9.2.4. Glass and Polishing

- 9.2.5. Metallurgy

- 9.2.6. Magnets

- 9.2.7. Other Applications

- 9.1. Market Analysis, Insights and Forecast - by Element

- 10. Middle East and Africa Rare Earth Metal Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Element

- 10.1.1. Cerium

- 10.1.1.1. Oxide

- 10.1.1.2. Sulfide

- 10.1.1.3. Other Elements

- 10.1.2. Neodymium

- 10.1.2.1. Alloy

- 10.1.3. Lanthanum

- 10.1.4. Dysprosium

- 10.1.5. Terbium

- 10.1.6. Yttrium

- 10.1.7. Scandium

- 10.1.1. Cerium

- 10.2. Market Analysis, Insights and Forecast - by Application

- 10.2.1. Catalysts

- 10.2.2. Ceramics

- 10.2.3. Phosphors

- 10.2.4. Glass and Polishing

- 10.2.5. Metallurgy

- 10.2.6. Magnets

- 10.2.7. Other Applications

- 10.1. Market Analysis, Insights and Forecast - by Element

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 China Nonferrous Metal Industry's Foreign Engineering and Construction Co Ltd

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Rare Element Resources Ltd

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Rio Tinto

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Xiamen Tungsten Co Ltd*List Not Exhaustive

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Avalon Advanced Materials Inc

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Lynas Rare Earths Ltd

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Iluka Resources Limited

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Ucore Rare Metals Inc

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 Peak Resources

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Shin-Etsu Chemical Co Ltd

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Minmetals Land Limited

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.12 NORTHERN MINERALS

- 11.2.12.1. Overview

- 11.2.12.2. Products

- 11.2.12.3. SWOT Analysis

- 11.2.12.4. Recent Developments

- 11.2.12.5. Financials (Based on Availability)

- 11.2.13 Eutectix

- 11.2.13.1. Overview

- 11.2.13.2. Products

- 11.2.13.3. SWOT Analysis

- 11.2.13.4. Recent Developments

- 11.2.13.5. Financials (Based on Availability)

- 11.2.14 ARAFURA RESOURCES

- 11.2.14.1. Overview

- 11.2.14.2. Products

- 11.2.14.3. SWOT Analysis

- 11.2.14.4. Recent Developments

- 11.2.14.5. Financials (Based on Availability)

- 11.2.15 MEDALLION RESOURCES LTD

- 11.2.15.1. Overview

- 11.2.15.2. Products

- 11.2.15.3. SWOT Analysis

- 11.2.15.4. Recent Developments

- 11.2.15.5. Financials (Based on Availability)

- 11.2.16 Aluminum Corporation of China Ltd

- 11.2.16.1. Overview

- 11.2.16.2. Products

- 11.2.16.3. SWOT Analysis

- 11.2.16.4. Recent Developments

- 11.2.16.5. Financials (Based on Availability)

- 11.2.1 China Nonferrous Metal Industry's Foreign Engineering and Construction Co Ltd

List of Figures

- Figure 1: Global Rare Earth Metal Industry Revenue Breakdown (Million, %) by Region 2025 & 2033

- Figure 2: Global Rare Earth Metal Industry Volume Breakdown (kilotons, %) by Region 2025 & 2033

- Figure 3: Asia Pacific Rare Earth Metal Industry Revenue (Million), by Element 2025 & 2033

- Figure 4: Asia Pacific Rare Earth Metal Industry Volume (kilotons), by Element 2025 & 2033

- Figure 5: Asia Pacific Rare Earth Metal Industry Revenue Share (%), by Element 2025 & 2033

- Figure 6: Asia Pacific Rare Earth Metal Industry Volume Share (%), by Element 2025 & 2033

- Figure 7: Asia Pacific Rare Earth Metal Industry Revenue (Million), by Application 2025 & 2033

- Figure 8: Asia Pacific Rare Earth Metal Industry Volume (kilotons), by Application 2025 & 2033

- Figure 9: Asia Pacific Rare Earth Metal Industry Revenue Share (%), by Application 2025 & 2033

- Figure 10: Asia Pacific Rare Earth Metal Industry Volume Share (%), by Application 2025 & 2033

- Figure 11: Asia Pacific Rare Earth Metal Industry Revenue (Million), by Country 2025 & 2033

- Figure 12: Asia Pacific Rare Earth Metal Industry Volume (kilotons), by Country 2025 & 2033

- Figure 13: Asia Pacific Rare Earth Metal Industry Revenue Share (%), by Country 2025 & 2033

- Figure 14: Asia Pacific Rare Earth Metal Industry Volume Share (%), by Country 2025 & 2033

- Figure 15: North America Rare Earth Metal Industry Revenue (Million), by Element 2025 & 2033

- Figure 16: North America Rare Earth Metal Industry Volume (kilotons), by Element 2025 & 2033

- Figure 17: North America Rare Earth Metal Industry Revenue Share (%), by Element 2025 & 2033

- Figure 18: North America Rare Earth Metal Industry Volume Share (%), by Element 2025 & 2033

- Figure 19: North America Rare Earth Metal Industry Revenue (Million), by Application 2025 & 2033

- Figure 20: North America Rare Earth Metal Industry Volume (kilotons), by Application 2025 & 2033

- Figure 21: North America Rare Earth Metal Industry Revenue Share (%), by Application 2025 & 2033

- Figure 22: North America Rare Earth Metal Industry Volume Share (%), by Application 2025 & 2033

- Figure 23: North America Rare Earth Metal Industry Revenue (Million), by Country 2025 & 2033

- Figure 24: North America Rare Earth Metal Industry Volume (kilotons), by Country 2025 & 2033

- Figure 25: North America Rare Earth Metal Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: North America Rare Earth Metal Industry Volume Share (%), by Country 2025 & 2033

- Figure 27: Europe Rare Earth Metal Industry Revenue (Million), by Element 2025 & 2033

- Figure 28: Europe Rare Earth Metal Industry Volume (kilotons), by Element 2025 & 2033

- Figure 29: Europe Rare Earth Metal Industry Revenue Share (%), by Element 2025 & 2033

- Figure 30: Europe Rare Earth Metal Industry Volume Share (%), by Element 2025 & 2033

- Figure 31: Europe Rare Earth Metal Industry Revenue (Million), by Application 2025 & 2033

- Figure 32: Europe Rare Earth Metal Industry Volume (kilotons), by Application 2025 & 2033

- Figure 33: Europe Rare Earth Metal Industry Revenue Share (%), by Application 2025 & 2033

- Figure 34: Europe Rare Earth Metal Industry Volume Share (%), by Application 2025 & 2033

- Figure 35: Europe Rare Earth Metal Industry Revenue (Million), by Country 2025 & 2033

- Figure 36: Europe Rare Earth Metal Industry Volume (kilotons), by Country 2025 & 2033

- Figure 37: Europe Rare Earth Metal Industry Revenue Share (%), by Country 2025 & 2033

- Figure 38: Europe Rare Earth Metal Industry Volume Share (%), by Country 2025 & 2033

- Figure 39: South America Rare Earth Metal Industry Revenue (Million), by Element 2025 & 2033

- Figure 40: South America Rare Earth Metal Industry Volume (kilotons), by Element 2025 & 2033

- Figure 41: South America Rare Earth Metal Industry Revenue Share (%), by Element 2025 & 2033

- Figure 42: South America Rare Earth Metal Industry Volume Share (%), by Element 2025 & 2033

- Figure 43: South America Rare Earth Metal Industry Revenue (Million), by Application 2025 & 2033

- Figure 44: South America Rare Earth Metal Industry Volume (kilotons), by Application 2025 & 2033

- Figure 45: South America Rare Earth Metal Industry Revenue Share (%), by Application 2025 & 2033

- Figure 46: South America Rare Earth Metal Industry Volume Share (%), by Application 2025 & 2033

- Figure 47: South America Rare Earth Metal Industry Revenue (Million), by Country 2025 & 2033

- Figure 48: South America Rare Earth Metal Industry Volume (kilotons), by Country 2025 & 2033

- Figure 49: South America Rare Earth Metal Industry Revenue Share (%), by Country 2025 & 2033

- Figure 50: South America Rare Earth Metal Industry Volume Share (%), by Country 2025 & 2033

- Figure 51: Middle East and Africa Rare Earth Metal Industry Revenue (Million), by Element 2025 & 2033

- Figure 52: Middle East and Africa Rare Earth Metal Industry Volume (kilotons), by Element 2025 & 2033

- Figure 53: Middle East and Africa Rare Earth Metal Industry Revenue Share (%), by Element 2025 & 2033

- Figure 54: Middle East and Africa Rare Earth Metal Industry Volume Share (%), by Element 2025 & 2033

- Figure 55: Middle East and Africa Rare Earth Metal Industry Revenue (Million), by Application 2025 & 2033

- Figure 56: Middle East and Africa Rare Earth Metal Industry Volume (kilotons), by Application 2025 & 2033

- Figure 57: Middle East and Africa Rare Earth Metal Industry Revenue Share (%), by Application 2025 & 2033

- Figure 58: Middle East and Africa Rare Earth Metal Industry Volume Share (%), by Application 2025 & 2033

- Figure 59: Middle East and Africa Rare Earth Metal Industry Revenue (Million), by Country 2025 & 2033

- Figure 60: Middle East and Africa Rare Earth Metal Industry Volume (kilotons), by Country 2025 & 2033

- Figure 61: Middle East and Africa Rare Earth Metal Industry Revenue Share (%), by Country 2025 & 2033

- Figure 62: Middle East and Africa Rare Earth Metal Industry Volume Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Rare Earth Metal Industry Revenue Million Forecast, by Element 2020 & 2033

- Table 2: Global Rare Earth Metal Industry Volume kilotons Forecast, by Element 2020 & 2033

- Table 3: Global Rare Earth Metal Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 4: Global Rare Earth Metal Industry Volume kilotons Forecast, by Application 2020 & 2033

- Table 5: Global Rare Earth Metal Industry Revenue Million Forecast, by Region 2020 & 2033

- Table 6: Global Rare Earth Metal Industry Volume kilotons Forecast, by Region 2020 & 2033

- Table 7: Global Rare Earth Metal Industry Revenue Million Forecast, by Element 2020 & 2033

- Table 8: Global Rare Earth Metal Industry Volume kilotons Forecast, by Element 2020 & 2033

- Table 9: Global Rare Earth Metal Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 10: Global Rare Earth Metal Industry Volume kilotons Forecast, by Application 2020 & 2033

- Table 11: Global Rare Earth Metal Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 12: Global Rare Earth Metal Industry Volume kilotons Forecast, by Country 2020 & 2033

- Table 13: China Rare Earth Metal Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 14: China Rare Earth Metal Industry Volume (kilotons) Forecast, by Application 2020 & 2033

- Table 15: India Rare Earth Metal Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 16: India Rare Earth Metal Industry Volume (kilotons) Forecast, by Application 2020 & 2033

- Table 17: Japan Rare Earth Metal Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 18: Japan Rare Earth Metal Industry Volume (kilotons) Forecast, by Application 2020 & 2033

- Table 19: South Korea Rare Earth Metal Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 20: South Korea Rare Earth Metal Industry Volume (kilotons) Forecast, by Application 2020 & 2033

- Table 21: Rest of Asia Pacific Rare Earth Metal Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 22: Rest of Asia Pacific Rare Earth Metal Industry Volume (kilotons) Forecast, by Application 2020 & 2033

- Table 23: Global Rare Earth Metal Industry Revenue Million Forecast, by Element 2020 & 2033

- Table 24: Global Rare Earth Metal Industry Volume kilotons Forecast, by Element 2020 & 2033

- Table 25: Global Rare Earth Metal Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 26: Global Rare Earth Metal Industry Volume kilotons Forecast, by Application 2020 & 2033

- Table 27: Global Rare Earth Metal Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 28: Global Rare Earth Metal Industry Volume kilotons Forecast, by Country 2020 & 2033

- Table 29: United States Rare Earth Metal Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 30: United States Rare Earth Metal Industry Volume (kilotons) Forecast, by Application 2020 & 2033

- Table 31: Canada Rare Earth Metal Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 32: Canada Rare Earth Metal Industry Volume (kilotons) Forecast, by Application 2020 & 2033

- Table 33: Mexico Rare Earth Metal Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 34: Mexico Rare Earth Metal Industry Volume (kilotons) Forecast, by Application 2020 & 2033

- Table 35: Global Rare Earth Metal Industry Revenue Million Forecast, by Element 2020 & 2033

- Table 36: Global Rare Earth Metal Industry Volume kilotons Forecast, by Element 2020 & 2033

- Table 37: Global Rare Earth Metal Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 38: Global Rare Earth Metal Industry Volume kilotons Forecast, by Application 2020 & 2033

- Table 39: Global Rare Earth Metal Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 40: Global Rare Earth Metal Industry Volume kilotons Forecast, by Country 2020 & 2033

- Table 41: Germany Rare Earth Metal Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 42: Germany Rare Earth Metal Industry Volume (kilotons) Forecast, by Application 2020 & 2033

- Table 43: United Kingdom Rare Earth Metal Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 44: United Kingdom Rare Earth Metal Industry Volume (kilotons) Forecast, by Application 2020 & 2033

- Table 45: France Rare Earth Metal Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 46: France Rare Earth Metal Industry Volume (kilotons) Forecast, by Application 2020 & 2033

- Table 47: Italy Rare Earth Metal Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 48: Italy Rare Earth Metal Industry Volume (kilotons) Forecast, by Application 2020 & 2033

- Table 49: Rest of Europe Rare Earth Metal Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 50: Rest of Europe Rare Earth Metal Industry Volume (kilotons) Forecast, by Application 2020 & 2033

- Table 51: Global Rare Earth Metal Industry Revenue Million Forecast, by Element 2020 & 2033

- Table 52: Global Rare Earth Metal Industry Volume kilotons Forecast, by Element 2020 & 2033

- Table 53: Global Rare Earth Metal Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 54: Global Rare Earth Metal Industry Volume kilotons Forecast, by Application 2020 & 2033

- Table 55: Global Rare Earth Metal Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 56: Global Rare Earth Metal Industry Volume kilotons Forecast, by Country 2020 & 2033

- Table 57: Brazil Rare Earth Metal Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 58: Brazil Rare Earth Metal Industry Volume (kilotons) Forecast, by Application 2020 & 2033

- Table 59: Argentina Rare Earth Metal Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 60: Argentina Rare Earth Metal Industry Volume (kilotons) Forecast, by Application 2020 & 2033

- Table 61: Rest of South America Rare Earth Metal Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 62: Rest of South America Rare Earth Metal Industry Volume (kilotons) Forecast, by Application 2020 & 2033

- Table 63: Global Rare Earth Metal Industry Revenue Million Forecast, by Element 2020 & 2033

- Table 64: Global Rare Earth Metal Industry Volume kilotons Forecast, by Element 2020 & 2033

- Table 65: Global Rare Earth Metal Industry Revenue Million Forecast, by Application 2020 & 2033

- Table 66: Global Rare Earth Metal Industry Volume kilotons Forecast, by Application 2020 & 2033

- Table 67: Global Rare Earth Metal Industry Revenue Million Forecast, by Country 2020 & 2033

- Table 68: Global Rare Earth Metal Industry Volume kilotons Forecast, by Country 2020 & 2033

- Table 69: Saudi Arabia Rare Earth Metal Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 70: Saudi Arabia Rare Earth Metal Industry Volume (kilotons) Forecast, by Application 2020 & 2033

- Table 71: South Africa Rare Earth Metal Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 72: South Africa Rare Earth Metal Industry Volume (kilotons) Forecast, by Application 2020 & 2033

- Table 73: Rest of Middle East and Africa Rare Earth Metal Industry Revenue (Million) Forecast, by Application 2020 & 2033

- Table 74: Rest of Middle East and Africa Rare Earth Metal Industry Volume (kilotons) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Rare Earth Metal Industry?

The projected CAGR is approximately 4.19%.

2. Which companies are prominent players in the Rare Earth Metal Industry?

Key companies in the market include China Nonferrous Metal Industry's Foreign Engineering and Construction Co Ltd, Rare Element Resources Ltd, Rio Tinto, Xiamen Tungsten Co Ltd*List Not Exhaustive, Avalon Advanced Materials Inc, Lynas Rare Earths Ltd, Iluka Resources Limited, Ucore Rare Metals Inc, Peak Resources, Shin-Etsu Chemical Co Ltd, Minmetals Land Limited, NORTHERN MINERALS, Eutectix, ARAFURA RESOURCES, MEDALLION RESOURCES LTD, Aluminum Corporation of China Ltd.

3. What are the main segments of the Rare Earth Metal Industry?

The market segments include Element, Application.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

High Demand from Emerging Economies; Dependency of 'Green Technology' on Rare Earth Elements.

6. What are the notable trends driving market growth?

Increasing Demand for Magnets.

7. Are there any restraints impacting market growth?

Inconsistent Supply of Rare Earth Elements.

8. Can you provide examples of recent developments in the market?

August 2022: Australia's Lynas Rare Earths Ltd unveiled a plan to expand capacity at its Western Australia-based Mt Weld mine having deposits of neodymium (Nd) and praseodymium (Pr). The company anticipates expansion work to begin by early 2023, with full operation planned for 2024.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in kilotons.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Rare Earth Metal Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Rare Earth Metal Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Rare Earth Metal Industry?

To stay informed about further developments, trends, and reports in the Rare Earth Metal Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence