Key Insights

The China oil & gas upstream industry, a significant contributor to the nation's energy security, is projected to experience robust growth throughout the forecast period (2025-2033). While precise market size figures for 2025 are unavailable, leveraging the provided CAGR of >3% and considering the substantial existing market size (implied by the mention of "Million" value unit), a reasonable estimate for the 2025 market value could range from $150 to $250 billion USD, depending on the specific definition of "upstream" and the inclusion of associated services. This growth is driven by increasing domestic energy demand fueled by a rapidly developing economy and urbanization. The government's continued investment in exploration and production activities, particularly in unconventional resources like shale gas, further stimulates market expansion. Key segments such as crude oil and natural gas production are expected to be major contributors to this growth. However, challenges remain, including environmental concerns related to emissions and the need for technological advancements to enhance efficiency and reduce production costs in mature fields. The industry's reliance on government policies and regulations also presents both opportunities and risks. The dominance of state-owned enterprises like CNPC, Sinopec, and CNOOC, while providing stability, may also limit market competition. Future growth will likely be shaped by the interplay of these factors, including technological innovations, regulatory frameworks, and global energy market dynamics.

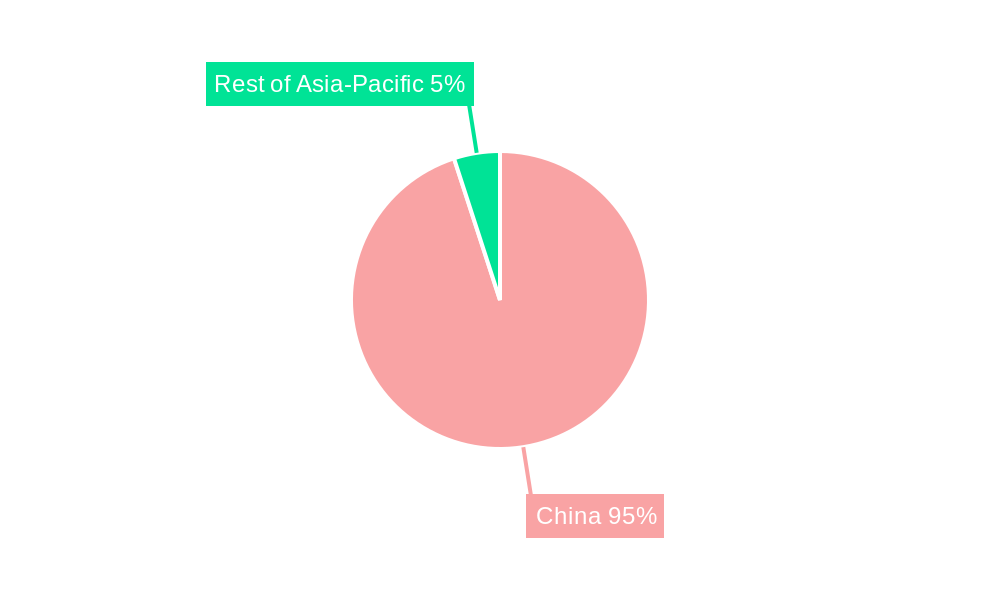

The competitive landscape is characterized by both large multinational corporations like ExxonMobil and Chevron and significant domestic players such as Yanchang Petroleum. These companies are engaged in a constant effort to optimize exploration and production techniques, enhance operational efficiency, and secure new resource reserves. The Asia-Pacific region, and specifically China, dominates this market, with considerable future growth potential driven by rising energy demands and ongoing investments in infrastructure. Future analysis should focus on understanding the impact of global geopolitical events on resource prices and investment decisions. Further research into the specific growth rates of each segment (crude oil, natural gas, NGLs) within the exploration, development and production stages would provide a more granular view of the market dynamics. A detailed examination of regulatory changes and government initiatives focused on environmental sustainability will also be critical for a more complete understanding of the sector's future trajectory.

China Oil & Gas Upstream Industry: A Comprehensive Market Report (2019-2033)

This in-depth report provides a comprehensive analysis of China's oil and gas upstream industry, covering market dynamics, leading players, key trends, and future growth prospects. The study period spans from 2019 to 2033, with a base year of 2025 and a forecast period from 2025 to 2033. This report is crucial for stakeholders including investors, industry professionals, and government agencies seeking to understand and capitalize on the opportunities and challenges within this dynamic sector.

China Oil & Gas Upstream Industry Market Dynamics & Concentration

The Chinese oil and gas upstream industry exhibits a complex interplay of market concentration, technological innovation, regulatory shifts, and competitive pressures. Dominated by state-owned enterprises (SOEs) like China National Petroleum Corporation (CNPC), China National Offshore Oil Corporation (CNOOC), and China Petroleum & Chemical Corporation (Sinopec), the market displays high concentration. However, the presence of international players such as Exxon Mobil Corporation, Chevron Corporation, BP PLC, and Shell PLC, and smaller players like Yanchang Petroleum International Limited adds dynamism.

Market share analysis reveals that SOEs hold a significant majority, with CNPC, CNOOC, and Sinopec controlling the lion's share of production and reserves. The industry is influenced by stringent government regulations and policies focused on energy security and environmental sustainability. The increasing adoption of advanced exploration and production technologies like enhanced oil recovery (EOR) and shale gas extraction fuels innovation. Substitutes like renewable energy sources are gaining traction, creating pressure on the industry to diversify and innovate. Consolidation through mergers and acquisitions (M&A) is a notable trend, with an estimated xx number of deals concluded between 2019 and 2024, signaling industry restructuring and expansion. End-user trends are shifting toward cleaner energy solutions, putting further pressure on the industry to adapt and improve efficiency.

China Oil & Gas Upstream Industry Industry Trends & Analysis

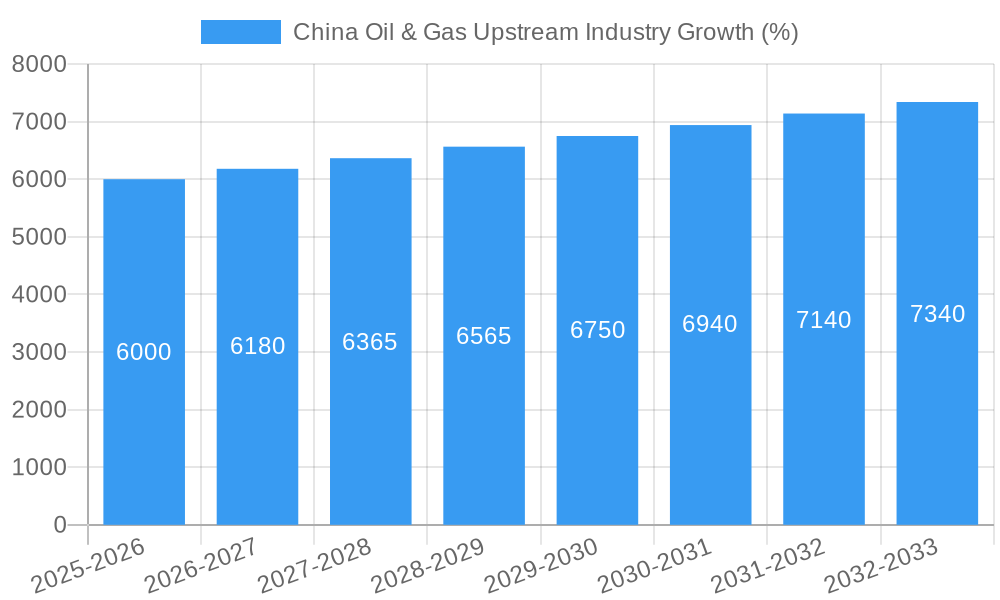

The Chinese oil and gas upstream market is projected to experience a Compound Annual Growth Rate (CAGR) of xx% during the forecast period (2025-2033), driven by several factors. Rising energy demand from a burgeoning population and industrial expansion are key growth drivers. Government initiatives supporting domestic energy production and infrastructure development contribute to market expansion. Technological advancements, specifically in unconventional oil and gas exploration (shale oil and gas), enhance resource accessibility and improve production efficiency. Market penetration of advanced technologies remains relatively low but is anticipated to increase rapidly, potentially reaching xx% by 2033. However, growing environmental concerns and international pressure for emissions reduction represent significant challenges. The increasing adoption of renewable energy sources and policies aimed at curbing greenhouse gas emissions create competitive pressure and necessitate investments in carbon capture and storage (CCS) technologies. The competitive landscape is shaped by the ongoing tension between SOEs and international companies competing for resources and market share, leading to strategic alliances and technological exchanges.

Leading Markets & Segments in China Oil & Gas Upstream Industry

The Tarim Basin and other significant onshore and offshore areas dominate the Chinese oil and gas upstream sector. Crude oil continues to be the leading segment by type of resource, accounting for approximately xx% of total production in 2025. Natural gas and Natural Gas Liquids (NGLs) are experiencing strong growth, driven by increasing demand for cleaner fuels and petrochemical feedstocks.

By Type of Resource:

- Crude Oil: Dominance driven by existing infrastructure, established production fields, and persistent demand from refineries and petrochemical industries.

- Natural Gas: Rapid expansion fueled by government policies promoting gas-based power generation and the development of pipeline infrastructure.

- Natural Gas Liquids (NGLs): Growth propelled by the increasing demand for petrochemical feedstocks and downstream processing facilities.

By Exploration and Production Stage:

- Development and Production: The majority of upstream activity, with continuous investments in mature fields and exploration of new reserves.

- Exploration: Significant investments directed toward discovering new oil and gas reserves, particularly in unconventional resources.

Key drivers of regional dominance include:

- Favorable geological conditions: The presence of substantial oil and gas reserves in specific basins.

- Government policies: Investment incentives, tax breaks, and regulatory frameworks that encourage exploration and production in certain areas.

- Infrastructure: The availability of transportation and processing facilities significantly impacts resource exploitation and market access.

China Oil & Gas Upstream Industry Product Developments

Product innovation focuses on improving extraction efficiency, lowering production costs, and reducing environmental impact. Advanced technologies, such as horizontal drilling and hydraulic fracturing, have revolutionized shale gas production. Enhanced oil recovery (EOR) techniques are employed in mature fields to maximize resource extraction. The integration of digital technologies, including data analytics and artificial intelligence, optimizes production processes and enhances decision-making. These innovations provide competitive advantages in terms of cost reduction, production efficiency, and environmental sustainability, enhancing the market fit of domestic and international companies.

Key Drivers of China Oil & Gas Upstream Industry Growth

Technological advancements, especially in unconventional resource extraction (shale gas and tight oil), are key growth catalysts. Government policies encouraging domestic energy production and infrastructure investments play a significant role. Rising energy demand from industrialization and population growth fuels market expansion. The strategic partnerships between domestic SOEs and international companies facilitate technology transfer and investment.

Challenges in the China Oil & Gas Upstream Industry Market

Regulatory hurdles and environmental concerns present significant challenges. Stringent environmental regulations and growing public awareness of climate change impose stricter emission standards and lead to increased operational costs. Supply chain disruptions and geopolitical factors can impact resource availability and production. Intense competition among domestic and international players creates pressure on pricing and profitability. These factors combine to potentially reduce profit margins by an estimated xx% by 2033.

Emerging Opportunities in China Oil & Gas Upstream Industry

The increasing adoption of digital technologies, including data analytics and artificial intelligence, presents significant opportunities for optimization and efficiency gains. Strategic partnerships between international and domestic companies can facilitate technology transfer and capital investment. Expansion into frontier exploration areas and unconventional resources holds immense potential. Further development of carbon capture and storage (CCS) technologies is vital to address environmental concerns and support long-term growth.

Leading Players in the China Oil & Gas Upstream Industry Sector

- Yanchang Petroleum International Limited

- Exxon Mobil Corporation

- China National Petroleum Corporation (CNPC)

- China National Offshore Oil Corporation (CNOOC)

- Chevron Corporation

- BP PLC

- Shell PLC

- China Petroleum & Chemical Corporation (Sinopec)

Key Milestones in China Oil & Gas Upstream Industry Industry

- August 2021: PetroChina's massive shale oil discovery at the Gulong prospect (1.268 billion tons of oil in place). This significantly boosted China's shale oil reserves and highlighted the potential of unconventional resources.

- June 2021: CNPC's discovery of a 1-billion-ton super-deep oil and gas area in the Tarim Basin, pushing the boundaries of deep-water exploration and expanding China's energy reserves.

- January 2022: Sinopec's discovery of a new oil and gas area in the Tarim Basin (approximately 100 million tons of reserves), further solidifying the basin's importance as a key resource hub.

Strategic Outlook for China Oil & Gas Upstream Industry Market

The future of China's oil and gas upstream industry hinges on technological innovation, strategic partnerships, and a balanced approach to environmental sustainability. Continued investment in unconventional resources, digitalization of operations, and the development of CCS technologies will be crucial for long-term growth. Navigating regulatory complexities and adapting to evolving global energy dynamics will define the success of players in this increasingly competitive market. The potential for significant growth remains high, particularly in the exploitation of unconventional resources and the expansion of gas-based energy.

China Oil & Gas Upstream Industry Segmentation

- 1. Onshore

- 2. Offshore

China Oil & Gas Upstream Industry Segmentation By Geography

- 1. China

China Oil & Gas Upstream Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of > 3.00% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. 4.; Increasing Electricity Demand4.; Rsing Investments in the Coal Industry

- 3.3. Market Restrains

- 3.3.1. 4.; Increasing Installation of Renewable Energy Sources

- 3.4. Market Trends

- 3.4.1. Offshore Segment to Dominate the Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. China Oil & Gas Upstream Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Onshore

- 5.2. Market Analysis, Insights and Forecast - by Offshore

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. China

- 5.1. Market Analysis, Insights and Forecast - by Onshore

- 6. China China Oil & Gas Upstream Industry Analysis, Insights and Forecast, 2019-2031

- 7. Japan China Oil & Gas Upstream Industry Analysis, Insights and Forecast, 2019-2031

- 8. India China Oil & Gas Upstream Industry Analysis, Insights and Forecast, 2019-2031

- 9. South Korea China Oil & Gas Upstream Industry Analysis, Insights and Forecast, 2019-2031

- 10. Taiwan China Oil & Gas Upstream Industry Analysis, Insights and Forecast, 2019-2031

- 11. Australia China Oil & Gas Upstream Industry Analysis, Insights and Forecast, 2019-2031

- 12. Rest of Asia-Pacific China Oil & Gas Upstream Industry Analysis, Insights and Forecast, 2019-2031

- 13. Competitive Analysis

- 13.1. Market Share Analysis 2024

- 13.2. Company Profiles

- 13.2.1 Yanchang Petroleum International Limited

- 13.2.1.1. Overview

- 13.2.1.2. Products

- 13.2.1.3. SWOT Analysis

- 13.2.1.4. Recent Developments

- 13.2.1.5. Financials (Based on Availability)

- 13.2.2 Exxon Mobil Corporation

- 13.2.2.1. Overview

- 13.2.2.2. Products

- 13.2.2.3. SWOT Analysis

- 13.2.2.4. Recent Developments

- 13.2.2.5. Financials (Based on Availability)

- 13.2.3 China National Petroleum Corporation

- 13.2.3.1. Overview

- 13.2.3.2. Products

- 13.2.3.3. SWOT Analysis

- 13.2.3.4. Recent Developments

- 13.2.3.5. Financials (Based on Availability)

- 13.2.4 China National Offshore Oil Corporation (CNOOC)

- 13.2.4.1. Overview

- 13.2.4.2. Products

- 13.2.4.3. SWOT Analysis

- 13.2.4.4. Recent Developments

- 13.2.4.5. Financials (Based on Availability)

- 13.2.5 Chevron Corporation

- 13.2.5.1. Overview

- 13.2.5.2. Products

- 13.2.5.3. SWOT Analysis

- 13.2.5.4. Recent Developments

- 13.2.5.5. Financials (Based on Availability)

- 13.2.6 BP PLC

- 13.2.6.1. Overview

- 13.2.6.2. Products

- 13.2.6.3. SWOT Analysis

- 13.2.6.4. Recent Developments

- 13.2.6.5. Financials (Based on Availability)

- 13.2.7 Shell PLC*List Not Exhaustive

- 13.2.7.1. Overview

- 13.2.7.2. Products

- 13.2.7.3. SWOT Analysis

- 13.2.7.4. Recent Developments

- 13.2.7.5. Financials (Based on Availability)

- 13.2.8 China Petroleum & Chemical Corporation (Sinopec)

- 13.2.8.1. Overview

- 13.2.8.2. Products

- 13.2.8.3. SWOT Analysis

- 13.2.8.4. Recent Developments

- 13.2.8.5. Financials (Based on Availability)

- 13.2.1 Yanchang Petroleum International Limited

List of Figures

- Figure 1: China Oil & Gas Upstream Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: China Oil & Gas Upstream Industry Share (%) by Company 2024

List of Tables

- Table 1: China Oil & Gas Upstream Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: China Oil & Gas Upstream Industry Revenue Million Forecast, by Onshore 2019 & 2032

- Table 3: China Oil & Gas Upstream Industry Revenue Million Forecast, by Offshore 2019 & 2032

- Table 4: China Oil & Gas Upstream Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: China Oil & Gas Upstream Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: China China Oil & Gas Upstream Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: Japan China Oil & Gas Upstream Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: India China Oil & Gas Upstream Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: South Korea China Oil & Gas Upstream Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Taiwan China Oil & Gas Upstream Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Australia China Oil & Gas Upstream Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 12: Rest of Asia-Pacific China Oil & Gas Upstream Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: China Oil & Gas Upstream Industry Revenue Million Forecast, by Onshore 2019 & 2032

- Table 14: China Oil & Gas Upstream Industry Revenue Million Forecast, by Offshore 2019 & 2032

- Table 15: China Oil & Gas Upstream Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the China Oil & Gas Upstream Industry?

The projected CAGR is approximately > 3.00%.

2. Which companies are prominent players in the China Oil & Gas Upstream Industry?

Key companies in the market include Yanchang Petroleum International Limited, Exxon Mobil Corporation, China National Petroleum Corporation, China National Offshore Oil Corporation (CNOOC), Chevron Corporation, BP PLC, Shell PLC*List Not Exhaustive, China Petroleum & Chemical Corporation (Sinopec).

3. What are the main segments of the China Oil & Gas Upstream Industry?

The market segments include Onshore, Offshore.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Increasing Electricity Demand4.; Rsing Investments in the Coal Industry.

6. What are the notable trends driving market growth?

Offshore Segment to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Increasing Installation of Renewable Energy Sources.

8. Can you provide examples of recent developments in the market?

In January 2022, Sinopec discovered a new oil and gas area with approximately 100 million tons of reserves in the Tarim Basin of northwest China's Xinjiang Uygur Autonomous Region. These latest reserves in Sinopec's Shunbei oil and gas field are estimated to provide 88 million tons of condensate oil and 290 billion cubic meters of natural gas.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "China Oil & Gas Upstream Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the China Oil & Gas Upstream Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the China Oil & Gas Upstream Industry?

To stay informed about further developments, trends, and reports in the China Oil & Gas Upstream Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence