Key Insights

China's e-commerce market is a global leader, projected to reach $885.5 billion by 2025, with a CAGR of 21.5%. Key growth drivers include widespread internet and smartphone adoption, a burgeoning middle class with increasing disposable income, and the rapid rise of mobile commerce. Innovative models like livestreaming and social commerce, prominent on platforms such as Xiaohongshu and Pinduoduo, are accelerating this expansion. Major players like Alibaba, JD.com, and Tencent face intense competition, while data privacy and regulatory landscapes present ongoing challenges. The market is highly diversified across product categories, from apparel and electronics to groceries and pharmaceuticals, reflecting its maturity and extensive consumer reach.

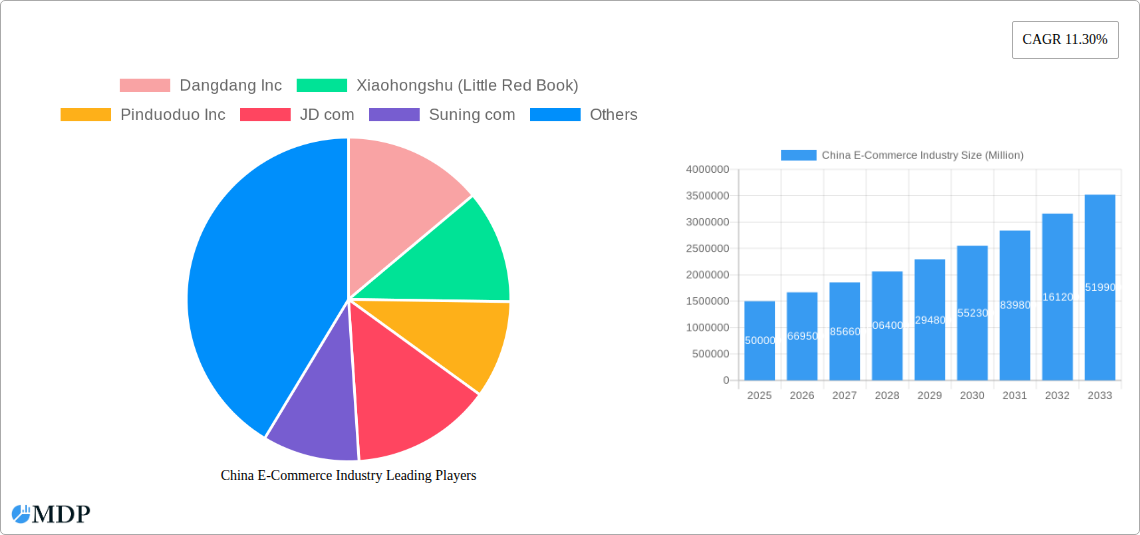

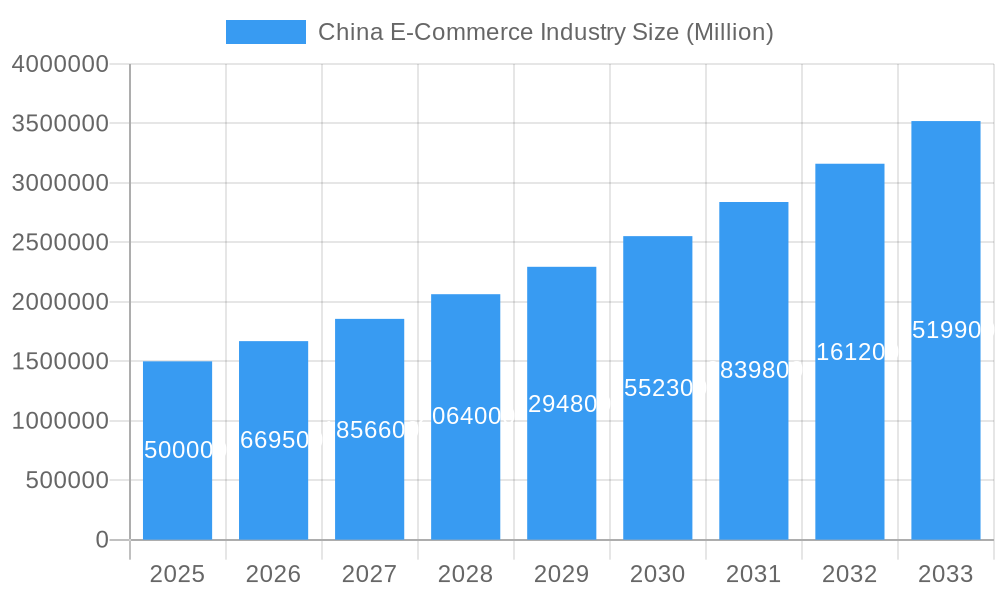

China E-Commerce Industry Market Size (In Million)

The forecast period (2025-2033) anticipates continued robust growth. Advancements in AI and big data analytics will enhance personalization and logistics, while government investment in digital infrastructure will provide further support. Macroeconomic conditions and evolving consumer spending patterns may influence market dynamics. Success for both domestic and international businesses will hinge on leveraging data analytics, innovative marketing, and efficient supply chain management within this dynamic and opportunity-rich sector.

China E-Commerce Industry Company Market Share

China E-Commerce Industry: 2019-2033 Market Report - Unlocking Trillion-Dollar Opportunities

Dive deep into the dynamic landscape of China's e-commerce industry with this comprehensive report, covering the period 2019-2033. This in-depth analysis provides critical insights for investors, businesses, and policymakers seeking to navigate this rapidly evolving market. The report leverages a robust methodology, utilizing historical data (2019-2024), a base year of 2025, and forecasts extending to 2033. Expect detailed breakdowns of market segmentation, leading players, key milestones, and emerging opportunities within this multi-billion dollar sector. Projected market values are presented in Millions.

China E-Commerce Industry Market Dynamics & Concentration

This section analyzes the competitive intensity of the Chinese e-commerce market. We examine market concentration, identifying leading players and their market share, with an emphasis on mergers and acquisitions (M&A) activity. The report also explores innovation drivers, regulatory landscapes, the impact of substitute products, and evolving end-user trends.

- Market Concentration: In 2024, Alibaba and JD.com held a combined market share of approximately 60%, indicating a duopoly. However, the rise of Pinduoduo and other players is challenging this dominance. The remaining 40% is split among many other players which includes the likes of Dangdang Inc, Xiaohongshu (Little Red Book), Suning.com, JuMei.com, Mogujie, Yihaodian, and Vipshop Holdings Ltd.

- Innovation Drivers: Technological advancements such as AI, big data analytics, and mobile commerce are driving innovation and shaping the competitive landscape. Livestreaming commerce and social commerce platforms are also significantly impacting the sector.

- Regulatory Frameworks: Government regulations regarding data privacy, anti-monopoly laws, and cross-border e-commerce are key factors influencing market dynamics. xx number of major regulatory changes impacted the sector between 2019 and 2024.

- Product Substitutes: Traditional brick-and-mortar retail remains a significant competitor, but its market share is steadily declining. The emergence of social commerce platforms as an alternative shopping channel also impacts the traditional e-commerce players.

- End-User Trends: Growing mobile penetration, increasing internet usage, and shifting consumer preferences toward convenience and personalized experiences are key drivers of e-commerce growth.

- M&A Activities: The Chinese e-commerce sector witnessed xx M&A deals between 2019 and 2024, primarily focused on consolidation and expansion into new segments.

China E-Commerce Industry Industry Trends & Analysis

This section delves into the key trends shaping the Chinese e-commerce industry. We analyze market growth drivers, technological disruptions, evolving consumer preferences, and competitive dynamics, providing a comprehensive overview of the sector's evolution. The report projects a CAGR of xx% for the forecast period (2025-2033), with market penetration reaching xx% by 2033. Specific trends examined include the increasing adoption of mobile payments, the rise of social commerce, and the growth of cross-border e-commerce. The increasing preference for customized products and services is also driving growth within niche markets. The impact of geopolitical factors and supply chain disruptions on the industry is also explored.

Leading Markets & Segments in China E-Commerce Industry

This section identifies the dominant regions and segments within the Chinese e-commerce market. We analyze the factors contributing to their dominance, including economic policies, infrastructure development, and consumer behavior.

Key Drivers for Dominant Segments:

- Robust Logistics Infrastructure: Extensive delivery networks and efficient logistics systems support rapid growth.

- Government Support: Favorable policies and initiatives promote digitalization and e-commerce adoption.

- High Smartphone Penetration: Widespread mobile device usage fuels mobile commerce growth.

- Growing Middle Class: Increased disposable incomes drive higher spending on online purchases.

Dominance Analysis: Tier 1 cities (e.g., Beijing, Shanghai, Guangzhou) continue to dominate in terms of e-commerce revenue, representing xx% of total revenue in 2024. However, growth in Tier 2 and 3 cities is accelerating, fueled by increasing internet and mobile penetration. The apparel and electronics segments are the largest by revenue in 2024, accounting for approximately xx% of the total market.

China E-Commerce Industry Product Developments

Recent product innovations in the Chinese e-commerce sector are characterized by increased personalization, improved user experience, and integration of emerging technologies. This includes the adoption of AI-powered recommendation engines, the use of augmented reality (AR) and virtual reality (VR) for enhanced product visualization, and the rise of livestreaming commerce. These innovations are enhancing customer engagement and driving sales growth.

Key Drivers of China E-Commerce Industry Growth

Several factors are propelling the growth of China's e-commerce industry. These include:

- Technological Advancements: The rapid development and adoption of mobile technologies, AI, big data analytics, and blockchain are transforming the industry.

- Economic Growth: A rising middle class with increasing disposable incomes fuels higher e-commerce spending.

- Favorable Government Policies: Supportive government regulations and initiatives encourage e-commerce adoption and digitalization.

Challenges in the China E-Commerce Industry Market

Despite its rapid growth, the Chinese e-commerce sector faces several challenges:

- Intense Competition: The market is highly fragmented, with numerous players vying for market share. This leads to price wars and reduced profit margins.

- Regulatory Hurdles: Navigating complex regulations and compliance requirements can be challenging for businesses.

- Supply Chain Disruptions: Geopolitical events and logistical issues can impact supply chain efficiency and lead to increased costs. xx% of businesses reported supply chain disruptions in 2024.

Emerging Opportunities in China E-Commerce Industry

The future of China's e-commerce industry is promising, driven by several key opportunities:

- Expansion into Lower-Tier Cities: Significant untapped potential exists in lower-tier cities with increasing internet and smartphone penetration.

- Growth of Cross-Border E-commerce: China's expanding middle class is increasingly purchasing imported goods online, creating opportunities for international businesses.

- Technological Innovations: The continued development and adoption of new technologies such as AI and blockchain will drive further growth and innovation.

Leading Players in the China E-Commerce Industry Sector

Key Milestones in China E-Commerce Industry Industry

- January 2022: JD.com partnered with Shopify, facilitating access to the Chinese market for global brands and vice-versa.

- April 2022: SavMobi Technology, Inc. signed an MOU with Dalian Yuanmeng Media Co., Ltd to explore the Chinese e-commerce market.

Strategic Outlook for China E-Commerce Industry Market

The Chinese e-commerce market is poised for sustained growth, driven by technological innovation, economic expansion, and favorable government policies. Strategic partnerships, expansion into new markets, and the adoption of emerging technologies will be crucial for success. The market is expected to reach xx Million by 2033, representing significant opportunities for investors and businesses.

China E-Commerce Industry Segmentation

-

1. B2C E-commerce

-

1.1. Market Segmentation - by Application

- 1.1.1. Beauty and Personal Care

- 1.1.2. Consumer Electronics

- 1.1.3. Fashion and Apparel

- 1.1.4. Food and Beverages

- 1.1.5. Furniture and Home

- 1.1.6. Others (Toys, DIY, Media, etc.)

-

1.1. Market Segmentation - by Application

-

2. Application

- 2.1. Beauty and Personal Care

- 2.2. Consumer Electronics

- 2.3. Fashion and Apparel

- 2.4. Food and Beverages

- 2.5. Furniture and Home

- 2.6. Others (Toys, DIY, Media, etc.)

- 3. Beauty and Personal Care

- 4. Consumer Electronics

- 5. Fashion and Apparel

- 6. Food and Beverages

- 7. Furniture and Home

- 8. Others (Toys, DIY, Media, etc.)

- 9. B2B E-commerce

China E-Commerce Industry Segmentation By Geography

- 1. China

China E-Commerce Industry Regional Market Share

Geographic Coverage of China E-Commerce Industry

China E-Commerce Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 21.5% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Objective

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Market Snapshot

- 3. Market Dynamics

- 3.1. Market Drivers

- 3.2. Market Restrains

- 3.3. Market Trends

- 3.4. Market Opportunities

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.1.1. Bargaining Power of Suppliers

- 4.1.2. Bargaining Power of Buyers

- 4.1.3. Threat of New Entrants

- 4.1.4. Threat of Substitutes

- 4.1.5. Competitive Rivalry

- 4.2. PESTEL analysis

- 4.3. BCG Analysis

- 4.3.1. Stars (High Growth, High Market Share)

- 4.3.2. Cash Cows (Low Growth, High Market Share)

- 4.3.3. Question Mark (High Growth, Low Market Share)

- 4.3.4. Dogs (Low Growth, Low Market Share)

- 4.4. Ansoff Matrix Analysis

- 4.5. Supply Chain Analysis

- 4.6. Regulatory Landscape

- 4.7. Current Market Potential and Opportunity Assessment (TAM–SAM–SOM Framework)

- 4.8. MDP Analyst Note

- 4.1. Porters Five Forces

- 5. Market Analysis, Insights and Forecast 2021-2033

- 5.1. Market Analysis, Insights and Forecast - by B2C E-commerce

- 5.1.1. Market Segmentation - by Application

- 5.1.1.1. Beauty and Personal Care

- 5.1.1.2. Consumer Electronics

- 5.1.1.3. Fashion and Apparel

- 5.1.1.4. Food and Beverages

- 5.1.1.5. Furniture and Home

- 5.1.1.6. Others (Toys, DIY, Media, etc.)

- 5.1.1. Market Segmentation - by Application

- 5.2. Market Analysis, Insights and Forecast - by Application

- 5.2.1. Beauty and Personal Care

- 5.2.2. Consumer Electronics

- 5.2.3. Fashion and Apparel

- 5.2.4. Food and Beverages

- 5.2.5. Furniture and Home

- 5.2.6. Others (Toys, DIY, Media, etc.)

- 5.3. Market Analysis, Insights and Forecast - by Beauty and Personal Care

- 5.4. Market Analysis, Insights and Forecast - by Consumer Electronics

- 5.5. Market Analysis, Insights and Forecast - by Fashion and Apparel

- 5.6. Market Analysis, Insights and Forecast - by Food and Beverages

- 5.7. Market Analysis, Insights and Forecast - by Furniture and Home

- 5.8. Market Analysis, Insights and Forecast - by Others (Toys, DIY, Media, etc.)

- 5.9. Market Analysis, Insights and Forecast - by B2B E-commerce

- 5.10. Market Analysis, Insights and Forecast - by Region

- 5.10.1. China

- 5.1. Market Analysis, Insights and Forecast - by B2C E-commerce

- 6. China E-Commerce Industry Analysis, Insights and Forecast, 2021-2033

- 6.1. Market Analysis, Insights and Forecast - by B2C E-commerce

- 6.1.1. Market Segmentation - by Application

- 6.1.1.1. Beauty and Personal Care

- 6.1.1.2. Consumer Electronics

- 6.1.1.3. Fashion and Apparel

- 6.1.1.4. Food and Beverages

- 6.1.1.5. Furniture and Home

- 6.1.1.6. Others (Toys, DIY, Media, etc.)

- 6.1.1. Market Segmentation - by Application

- 6.2. Market Analysis, Insights and Forecast - by Application

- 6.2.1. Beauty and Personal Care

- 6.2.2. Consumer Electronics

- 6.2.3. Fashion and Apparel

- 6.2.4. Food and Beverages

- 6.2.5. Furniture and Home

- 6.2.6. Others (Toys, DIY, Media, etc.)

- 6.3. Market Analysis, Insights and Forecast - by Beauty and Personal Care

- 6.4. Market Analysis, Insights and Forecast - by Consumer Electronics

- 6.5. Market Analysis, Insights and Forecast - by Fashion and Apparel

- 6.6. Market Analysis, Insights and Forecast - by Food and Beverages

- 6.7. Market Analysis, Insights and Forecast - by Furniture and Home

- 6.8. Market Analysis, Insights and Forecast - by Others (Toys, DIY, Media, etc.)

- 6.9. Market Analysis, Insights and Forecast - by B2B E-commerce

- 6.1. Market Analysis, Insights and Forecast - by B2C E-commerce

- 7. Competitive Analysis

- 7.1. Company Profiles

- 7.1.1 Dangdang Inc

- 7.1.1.1. Company Overview

- 7.1.1.2. Products

- 7.1.1.3. Company Financials

- 7.1.1.4. SWOT Analysis

- 7.1.2 Xiaohongshu (Little Red Book)

- 7.1.2.1. Company Overview

- 7.1.2.2. Products

- 7.1.2.3. Company Financials

- 7.1.2.4. SWOT Analysis

- 7.1.3 Pinduoduo Inc

- 7.1.3.1. Company Overview

- 7.1.3.2. Products

- 7.1.3.3. Company Financials

- 7.1.3.4. SWOT Analysis

- 7.1.4 JD com

- 7.1.4.1. Company Overview

- 7.1.4.2. Products

- 7.1.4.3. Company Financials

- 7.1.4.4. SWOT Analysis

- 7.1.5 Suning com

- 7.1.5.1. Company Overview

- 7.1.5.2. Products

- 7.1.5.3. Company Financials

- 7.1.5.4. SWOT Analysis

- 7.1.6 JuMei com

- 7.1.6.1. Company Overview

- 7.1.6.2. Products

- 7.1.6.3. Company Financials

- 7.1.6.4. SWOT Analysis

- 7.1.7 Mogujie*List Not Exhaustive

- 7.1.7.1. Company Overview

- 7.1.7.2. Products

- 7.1.7.3. Company Financials

- 7.1.7.4. SWOT Analysis

- 7.1.8 Yihaodian

- 7.1.8.1. Company Overview

- 7.1.8.2. Products

- 7.1.8.3. Company Financials

- 7.1.8.4. SWOT Analysis

- 7.1.9 Alibaba com

- 7.1.9.1. Company Overview

- 7.1.9.2. Products

- 7.1.9.3. Company Financials

- 7.1.9.4. SWOT Analysis

- 7.1.10 Vipshop Holdings Ltd

- 7.1.10.1. Company Overview

- 7.1.10.2. Products

- 7.1.10.3. Company Financials

- 7.1.10.4. SWOT Analysis

- 7.1.1 Dangdang Inc

- 7.2. Market Entropy

- 7.2.1 Company's Key Areas Served

- 7.2.2 Recent Developments

- 7.3. Company Market Share Analysis 2025

- 7.3.1 Top 5 Companies Market Share Analysis

- 7.3.2 Top 3 Companies Market Share Analysis

- 7.4. List of Potential Customers

- 8. Research Methodology

List of Figures

- Figure 1: China E-Commerce Industry Revenue Breakdown (billion, %) by Product 2025 & 2033

- Figure 2: China E-Commerce Industry Share (%) by Company 2025

List of Tables

- Table 1: China E-Commerce Industry Revenue billion Forecast, by B2C E-commerce 2020 & 2033

- Table 2: China E-Commerce Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 3: China E-Commerce Industry Revenue billion Forecast, by Beauty and Personal Care 2020 & 2033

- Table 4: China E-Commerce Industry Revenue billion Forecast, by Consumer Electronics 2020 & 2033

- Table 5: China E-Commerce Industry Revenue billion Forecast, by Fashion and Apparel 2020 & 2033

- Table 6: China E-Commerce Industry Revenue billion Forecast, by Food and Beverages 2020 & 2033

- Table 7: China E-Commerce Industry Revenue billion Forecast, by Furniture and Home 2020 & 2033

- Table 8: China E-Commerce Industry Revenue billion Forecast, by Others (Toys, DIY, Media, etc.) 2020 & 2033

- Table 9: China E-Commerce Industry Revenue billion Forecast, by B2B E-commerce 2020 & 2033

- Table 10: China E-Commerce Industry Revenue billion Forecast, by Region 2020 & 2033

- Table 11: China E-Commerce Industry Revenue billion Forecast, by B2C E-commerce 2020 & 2033

- Table 12: China E-Commerce Industry Revenue billion Forecast, by Application 2020 & 2033

- Table 13: China E-Commerce Industry Revenue billion Forecast, by Beauty and Personal Care 2020 & 2033

- Table 14: China E-Commerce Industry Revenue billion Forecast, by Consumer Electronics 2020 & 2033

- Table 15: China E-Commerce Industry Revenue billion Forecast, by Fashion and Apparel 2020 & 2033

- Table 16: China E-Commerce Industry Revenue billion Forecast, by Food and Beverages 2020 & 2033

- Table 17: China E-Commerce Industry Revenue billion Forecast, by Furniture and Home 2020 & 2033

- Table 18: China E-Commerce Industry Revenue billion Forecast, by Others (Toys, DIY, Media, etc.) 2020 & 2033

- Table 19: China E-Commerce Industry Revenue billion Forecast, by B2B E-commerce 2020 & 2033

- Table 20: China E-Commerce Industry Revenue billion Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the China E-Commerce Industry?

The projected CAGR is approximately 21.5%.

2. Which companies are prominent players in the China E-Commerce Industry?

Key companies in the market include Dangdang Inc, Xiaohongshu (Little Red Book), Pinduoduo Inc, JD com, Suning com, JuMei com, Mogujie*List Not Exhaustive, Yihaodian, Alibaba com, Vipshop Holdings Ltd.

3. What are the main segments of the China E-Commerce Industry?

The market segments include B2C E-commerce, Application, Beauty and Personal Care, Consumer Electronics, Fashion and Apparel, Food and Beverages, Furniture and Home, Others (Toys, DIY, Media, etc.), B2B E-commerce.

4. Can you provide details about the market size?

The market size is estimated to be USD 885.5 billion as of 2022.

5. What are some drivers contributing to market growth?

Livestream E-commerce to drive the Market; Growing Penetration of Online Shoppers to Boost the E-commerce Market.

6. What are the notable trends driving market growth?

Livestream E-commerce to drive the Market.

7. Are there any restraints impacting market growth?

Budget Constraints and Technological Limitations; Regulatory and Legal Challenges.

8. Can you provide examples of recent developments in the market?

January 2022 - Major Chinese E-commerce company JD.com formed a strategic partnership with Ottawa-based Shopify to help global brands tap China's enormous appetite for imported goods and help Chinese merchants sell overseas. JD.com promises to simplify access and compliance for Chinese brands and merchants looking to reach consumers in Western markets through the partnership.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "China E-Commerce Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the China E-Commerce Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the China E-Commerce Industry?

To stay informed about further developments, trends, and reports in the China E-Commerce Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence