Key Insights

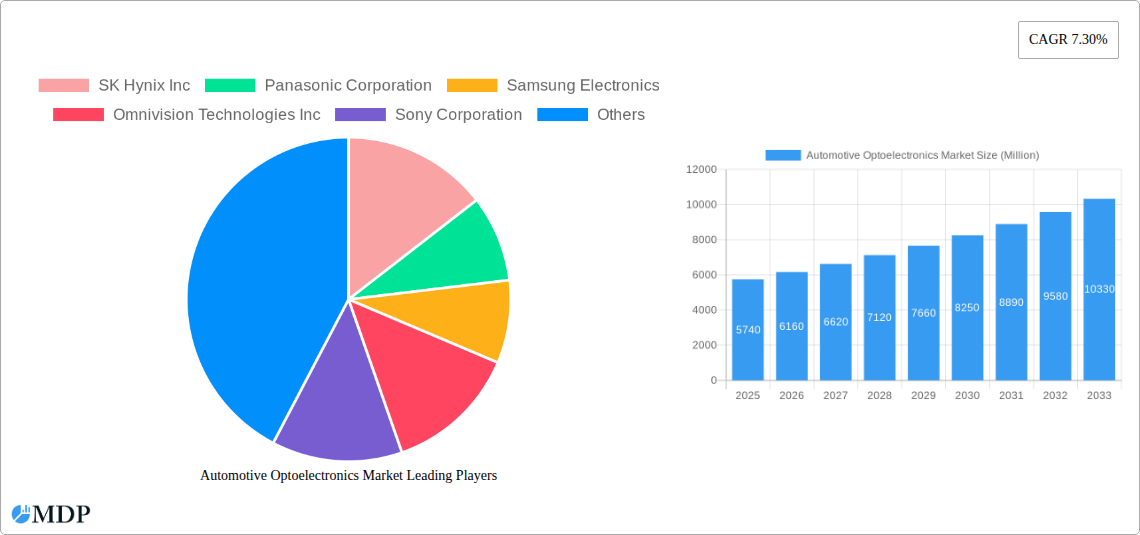

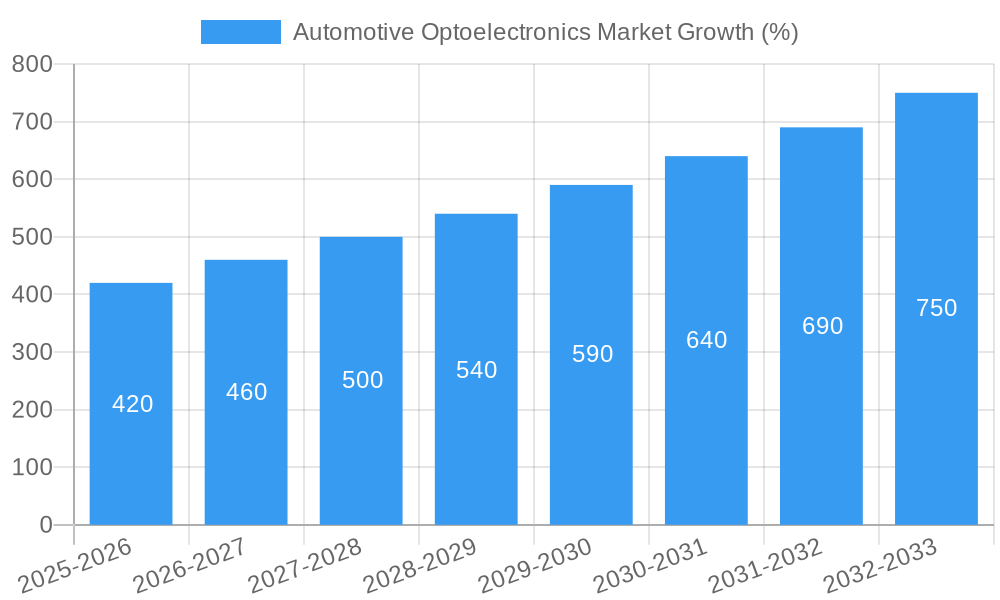

The automotive optoelectronics market, valued at $5.74 billion in 2025, is projected to experience robust growth, driven by the increasing adoption of advanced driver-assistance systems (ADAS) and the rising demand for autonomous vehicles. The market's Compound Annual Growth Rate (CAGR) of 7.30% from 2025 to 2033 indicates a significant expansion, fueled by technological advancements in lighting systems, sensors, and displays. Key growth drivers include the increasing integration of LEDs in automotive lighting, the proliferation of LiDAR and camera-based sensor technologies for ADAS functionalities like lane keeping assist and adaptive cruise control, and the rising popularity of head-up displays (HUDs) and digital instrument clusters enhancing driver experience and safety. Furthermore, stringent government regulations mandating advanced safety features in new vehicles are accelerating market adoption. While supply chain constraints and the cost associated with implementing these advanced technologies pose some challenges, the long-term outlook remains positive, particularly with continued innovation in areas like micro-LEDs and improved sensor performance. Competition among major players like SK Hynix, Panasonic, Samsung Electronics, and others is intensifying, driving innovation and affordability. This competitive landscape is further fostering market expansion through continuous product development and strategic partnerships. The market segmentation, while not fully detailed, suggests a diverse range of applications driving growth across various vehicle types and geographic regions.

The forecast period of 2025-2033 anticipates continued market expansion, with a projected market size exceeding $10 billion by 2033. This growth will be influenced by the maturity of existing technologies and the emergence of new applications, like in-cabin sensing for driver monitoring and occupant comfort. Regional variations in market growth will be influenced by factors such as vehicle production rates, adoption of advanced technologies, and government regulations. The continued focus on enhancing vehicle safety and improving driver experience will drive increased integration of optoelectronic components across all vehicle segments, leading to sustainable long-term market growth.

Automotive Optoelectronics Market: A Comprehensive Report (2019-2033)

This in-depth report provides a comprehensive analysis of the Automotive Optoelectronics Market, offering invaluable insights for stakeholders across the automotive and semiconductor industries. From market dynamics and leading players to emerging opportunities and future trends, this report unveils the key factors shaping the future of this rapidly evolving sector. With a meticulous study period spanning from 2019 to 2033 (base year 2025, forecast period 2025-2033), this analysis is an essential resource for strategic decision-making. The report also leverages high-impact keywords such as automotive lighting, LED technology, automotive sensors, semiconductor market, and ADAS to ensure maximum visibility within search engine results. Estimated market value is pegged at xx Million by 2033.

Automotive Optoelectronics Market Market Dynamics & Concentration

The automotive optoelectronics market is characterized by a moderately concentrated landscape, with a handful of major players holding significant market share. Innovation in LED technology, particularly in areas like micro-LEDs and advanced lighting systems, is a primary growth driver. Stringent regulatory frameworks concerning vehicle safety and fuel efficiency further fuel market expansion. The rise of ADAS (Advanced Driver-Assistance Systems) and autonomous driving technologies is creating substantial demand for sophisticated sensors and lighting systems. Product substitutes, such as traditional incandescent bulbs, are gradually losing market share due to their lower efficiency and performance. End-user trends reflect a growing preference for enhanced vehicle aesthetics and safety features.

- Market Concentration: The top 5 players hold approximately xx% of the global market share (2024).

- Innovation Drivers: Miniaturization of components, higher luminous efficacy, and integration of smart functionalities.

- Regulatory Frameworks: Stringent safety and emission standards, promoting adoption of energy-efficient technologies.

- M&A Activities: An estimated xx M&A deals were concluded within the last five years, driven by strategic consolidation and expansion.

Automotive Optoelectronics Market Industry Trends & Analysis

The automotive optoelectronics market is experiencing robust growth, driven by the increasing adoption of advanced driver-assistance systems (ADAS), autonomous driving technologies, and the growing demand for enhanced vehicle aesthetics. The market is witnessing a technological shift from traditional incandescent and halogen lighting to energy-efficient LEDs and other advanced technologies. This transition is fueled by stricter government regulations and the rising consumer preference for enhanced safety and fuel economy. Consumer preferences are shifting towards feature-rich vehicles with sophisticated lighting and sensing systems. The CAGR for the forecast period (2025-2033) is estimated at xx%, with market penetration rates steadily increasing across all key regions. Competitive dynamics are intense, with leading players investing heavily in R&D to develop innovative and cost-effective solutions.

Leading Markets & Segments in Automotive Optoelectronics Market

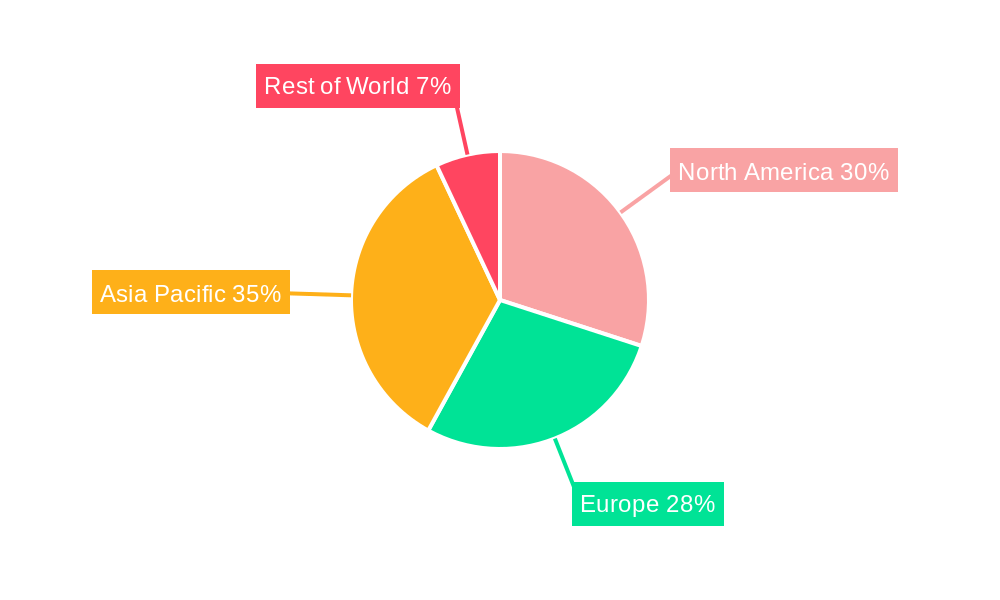

The Asia-Pacific region currently dominates the global automotive optoelectronics market, driven by factors such as rapid economic growth, booming automotive production, and significant government support for technological advancements. Within the region, China and Japan represent significant markets, with supportive infrastructure and robust automotive industries propelling growth.

- Key Drivers in Asia-Pacific:

- Strong automotive manufacturing base

- High demand for advanced safety features

- Favorable government policies supporting technological innovation

- Increasing disposable incomes and consumer preference for advanced vehicles

The detailed dominance analysis indicates Asia-Pacific's lead is expected to continue throughout the forecast period. This is largely due to the region’s substantial automotive production volume, expanding middle-class population, and proactive government incentives to improve vehicle safety standards. Other regions like North America and Europe, while mature, continue to show consistent growth, driven by the adoption of new vehicle technologies and stringent emission regulations.

Automotive Optoelectronics Market Product Developments

Recent product innovations include the development of highly integrated LED modules incorporating multiple functionalities such as headlamps, taillights, and turn signals. Advanced sensor technologies utilizing laser and infrared (IR) are becoming increasingly crucial for ADAS and autonomous driving systems. These advancements offer improved performance, reduced costs, and better integration into vehicle designs, resulting in a competitive advantage for manufacturers.

Key Drivers of Automotive Optoelectronics Market Growth

Several factors contribute to the growth of the automotive optoelectronics market:

- Technological advancements: Miniaturization, increased efficiency, and enhanced functionalities of LEDs and sensors.

- Stringent safety regulations: Governments are mandating advanced safety features, boosting demand for automotive optoelectronics.

- Rising consumer demand: Consumers increasingly prefer vehicles with advanced lighting, sensing, and display technologies.

- Increased adoption of ADAS and autonomous driving: Self-driving cars rely heavily on optoelectronic components for navigation and safety.

Challenges in the Automotive Optoelectronics Market Market

The automotive optoelectronics market faces several challenges:

- High initial investment costs: Developing and manufacturing advanced components requires significant capital expenditure.

- Supply chain disruptions: Global events and geopolitical uncertainties can impact the availability of raw materials and components.

- Intense competition: The market is dominated by a large number of companies vying for market share, putting pressure on pricing.

Emerging Opportunities in Automotive Optoelectronics Market

The market presents significant long-term opportunities through the integration of new technologies such as LiDAR, advanced camera systems, and next-generation LED lighting. Strategic partnerships and collaborations between automotive manufacturers and component suppliers will play a critical role in driving innovation and accelerating market growth. Expansion into developing economies presents significant untapped potential for market expansion.

Leading Players in the Automotive Optoelectronics Market Sector

- SK Hynix Inc

- Panasonic Corporation

- Samsung Electronics

- Omnivision Technologies Inc

- Sony Corporation

- Ams Osram AG

- Signify Holding

- Vishay Intertechnology Inc

- Texas Instruments Inc

- LITE-ON Technology Corporation

- Rohm Company Limited

- Mitsubishi Electric Corporation

- Broadcom Inc

- Sharp Corporation

Key Milestones in Automotive Optoelectronics Market Industry

- February 2024: TSMC, Sony Semiconductor Solutions Corporation, DENSO Corporation, and Toyota Motor Corporation invested significantly in Japan Advanced Semiconductor Manufacturing Inc. (JASM), signaling a major commitment to expanding semiconductor production capacity in Japan, which will ultimately increase the availability of components vital to the automotive optoelectronics sector. This investment will surpass USD 20 Billion.

- January 2024: Osram Licht AG launched SYNIOS P1515 side-looker LEDs, offering streamlined design and improved aesthetics for automotive rear lighting, potentially driving adoption across the industry.

Strategic Outlook for Automotive Optoelectronics Market Market

The automotive optoelectronics market is poised for sustained growth, driven by technological innovation, increasing demand for advanced safety features, and the expansion of electric and autonomous vehicles. Strategic partnerships and collaborations will be crucial for players seeking to capitalize on emerging opportunities and consolidate their market positions. Further investments in R&D and capacity expansion will be critical in meeting the growing demand for sophisticated and cost-effective solutions.

Automotive Optoelectronics Market Segmentation

-

1. Device Type

- 1.1. LED

- 1.2. Laser Diode

- 1.3. Image Sensors

- 1.4. Optocouplers

- 1.5. Photovoltaic cells

- 1.6. Other Device Types

Automotive Optoelectronics Market Segmentation By Geography

- 1. United States

- 2. Europe

- 3. Japan

- 4. China

- 5. South Korea

- 6. Taiwan

Automotive Optoelectronics Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 7.30% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1 Technology Advancements

- 3.2.2 and AI Developments will Drive the Growth; Growing Demand for Electric Vehicles

- 3.3. Market Restrains

- 3.3.1 Technology Advancements

- 3.3.2 and AI Developments will Drive the Growth; Growing Demand for Electric Vehicles

- 3.4. Market Trends

- 3.4.1. Image Sensors are Expected to Hold Major Market Share

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Automotive Optoelectronics Market Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Device Type

- 5.1.1. LED

- 5.1.2. Laser Diode

- 5.1.3. Image Sensors

- 5.1.4. Optocouplers

- 5.1.5. Photovoltaic cells

- 5.1.6. Other Device Types

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. United States

- 5.2.2. Europe

- 5.2.3. Japan

- 5.2.4. China

- 5.2.5. South Korea

- 5.2.6. Taiwan

- 5.1. Market Analysis, Insights and Forecast - by Device Type

- 6. United States Automotive Optoelectronics Market Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - by Device Type

- 6.1.1. LED

- 6.1.2. Laser Diode

- 6.1.3. Image Sensors

- 6.1.4. Optocouplers

- 6.1.5. Photovoltaic cells

- 6.1.6. Other Device Types

- 6.1. Market Analysis, Insights and Forecast - by Device Type

- 7. Europe Automotive Optoelectronics Market Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - by Device Type

- 7.1.1. LED

- 7.1.2. Laser Diode

- 7.1.3. Image Sensors

- 7.1.4. Optocouplers

- 7.1.5. Photovoltaic cells

- 7.1.6. Other Device Types

- 7.1. Market Analysis, Insights and Forecast - by Device Type

- 8. Japan Automotive Optoelectronics Market Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - by Device Type

- 8.1.1. LED

- 8.1.2. Laser Diode

- 8.1.3. Image Sensors

- 8.1.4. Optocouplers

- 8.1.5. Photovoltaic cells

- 8.1.6. Other Device Types

- 8.1. Market Analysis, Insights and Forecast - by Device Type

- 9. China Automotive Optoelectronics Market Analysis, Insights and Forecast, 2019-2031

- 9.1. Market Analysis, Insights and Forecast - by Device Type

- 9.1.1. LED

- 9.1.2. Laser Diode

- 9.1.3. Image Sensors

- 9.1.4. Optocouplers

- 9.1.5. Photovoltaic cells

- 9.1.6. Other Device Types

- 9.1. Market Analysis, Insights and Forecast - by Device Type

- 10. South Korea Automotive Optoelectronics Market Analysis, Insights and Forecast, 2019-2031

- 10.1. Market Analysis, Insights and Forecast - by Device Type

- 10.1.1. LED

- 10.1.2. Laser Diode

- 10.1.3. Image Sensors

- 10.1.4. Optocouplers

- 10.1.5. Photovoltaic cells

- 10.1.6. Other Device Types

- 10.1. Market Analysis, Insights and Forecast - by Device Type

- 11. Taiwan Automotive Optoelectronics Market Analysis, Insights and Forecast, 2019-2031

- 11.1. Market Analysis, Insights and Forecast - by Device Type

- 11.1.1. LED

- 11.1.2. Laser Diode

- 11.1.3. Image Sensors

- 11.1.4. Optocouplers

- 11.1.5. Photovoltaic cells

- 11.1.6. Other Device Types

- 11.1. Market Analysis, Insights and Forecast - by Device Type

- 12. Competitive Analysis

- 12.1. Global Market Share Analysis 2024

- 12.2. Company Profiles

- 12.2.1 SK Hynix Inc

- 12.2.1.1. Overview

- 12.2.1.2. Products

- 12.2.1.3. SWOT Analysis

- 12.2.1.4. Recent Developments

- 12.2.1.5. Financials (Based on Availability)

- 12.2.2 Panasonic Corporation

- 12.2.2.1. Overview

- 12.2.2.2. Products

- 12.2.2.3. SWOT Analysis

- 12.2.2.4. Recent Developments

- 12.2.2.5. Financials (Based on Availability)

- 12.2.3 Samsung Electronics

- 12.2.3.1. Overview

- 12.2.3.2. Products

- 12.2.3.3. SWOT Analysis

- 12.2.3.4. Recent Developments

- 12.2.3.5. Financials (Based on Availability)

- 12.2.4 Omnivision Technologies Inc

- 12.2.4.1. Overview

- 12.2.4.2. Products

- 12.2.4.3. SWOT Analysis

- 12.2.4.4. Recent Developments

- 12.2.4.5. Financials (Based on Availability)

- 12.2.5 Sony Corporation

- 12.2.5.1. Overview

- 12.2.5.2. Products

- 12.2.5.3. SWOT Analysis

- 12.2.5.4. Recent Developments

- 12.2.5.5. Financials (Based on Availability)

- 12.2.6 Ams Osram AG

- 12.2.6.1. Overview

- 12.2.6.2. Products

- 12.2.6.3. SWOT Analysis

- 12.2.6.4. Recent Developments

- 12.2.6.5. Financials (Based on Availability)

- 12.2.7 Signify Holding

- 12.2.7.1. Overview

- 12.2.7.2. Products

- 12.2.7.3. SWOT Analysis

- 12.2.7.4. Recent Developments

- 12.2.7.5. Financials (Based on Availability)

- 12.2.8 Vishay Intertechnology Inc

- 12.2.8.1. Overview

- 12.2.8.2. Products

- 12.2.8.3. SWOT Analysis

- 12.2.8.4. Recent Developments

- 12.2.8.5. Financials (Based on Availability)

- 12.2.9 Texas Instruments Inc

- 12.2.9.1. Overview

- 12.2.9.2. Products

- 12.2.9.3. SWOT Analysis

- 12.2.9.4. Recent Developments

- 12.2.9.5. Financials (Based on Availability)

- 12.2.10 LITE-ON Technology Corporation

- 12.2.10.1. Overview

- 12.2.10.2. Products

- 12.2.10.3. SWOT Analysis

- 12.2.10.4. Recent Developments

- 12.2.10.5. Financials (Based on Availability)

- 12.2.11 Rohm Company Limited

- 12.2.11.1. Overview

- 12.2.11.2. Products

- 12.2.11.3. SWOT Analysis

- 12.2.11.4. Recent Developments

- 12.2.11.5. Financials (Based on Availability)

- 12.2.12 Mitsubishi Electric Corporation

- 12.2.12.1. Overview

- 12.2.12.2. Products

- 12.2.12.3. SWOT Analysis

- 12.2.12.4. Recent Developments

- 12.2.12.5. Financials (Based on Availability)

- 12.2.13 Broadcom Inc

- 12.2.13.1. Overview

- 12.2.13.2. Products

- 12.2.13.3. SWOT Analysis

- 12.2.13.4. Recent Developments

- 12.2.13.5. Financials (Based on Availability)

- 12.2.14 Sharp Corporatio

- 12.2.14.1. Overview

- 12.2.14.2. Products

- 12.2.14.3. SWOT Analysis

- 12.2.14.4. Recent Developments

- 12.2.14.5. Financials (Based on Availability)

- 12.2.1 SK Hynix Inc

List of Figures

- Figure 1: Global Automotive Optoelectronics Market Revenue Breakdown (Million, %) by Region 2024 & 2032

- Figure 2: Global Automotive Optoelectronics Market Volume Breakdown (Billion, %) by Region 2024 & 2032

- Figure 3: United States Automotive Optoelectronics Market Revenue (Million), by Device Type 2024 & 2032

- Figure 4: United States Automotive Optoelectronics Market Volume (Billion), by Device Type 2024 & 2032

- Figure 5: United States Automotive Optoelectronics Market Revenue Share (%), by Device Type 2024 & 2032

- Figure 6: United States Automotive Optoelectronics Market Volume Share (%), by Device Type 2024 & 2032

- Figure 7: United States Automotive Optoelectronics Market Revenue (Million), by Country 2024 & 2032

- Figure 8: United States Automotive Optoelectronics Market Volume (Billion), by Country 2024 & 2032

- Figure 9: United States Automotive Optoelectronics Market Revenue Share (%), by Country 2024 & 2032

- Figure 10: United States Automotive Optoelectronics Market Volume Share (%), by Country 2024 & 2032

- Figure 11: Europe Automotive Optoelectronics Market Revenue (Million), by Device Type 2024 & 2032

- Figure 12: Europe Automotive Optoelectronics Market Volume (Billion), by Device Type 2024 & 2032

- Figure 13: Europe Automotive Optoelectronics Market Revenue Share (%), by Device Type 2024 & 2032

- Figure 14: Europe Automotive Optoelectronics Market Volume Share (%), by Device Type 2024 & 2032

- Figure 15: Europe Automotive Optoelectronics Market Revenue (Million), by Country 2024 & 2032

- Figure 16: Europe Automotive Optoelectronics Market Volume (Billion), by Country 2024 & 2032

- Figure 17: Europe Automotive Optoelectronics Market Revenue Share (%), by Country 2024 & 2032

- Figure 18: Europe Automotive Optoelectronics Market Volume Share (%), by Country 2024 & 2032

- Figure 19: Japan Automotive Optoelectronics Market Revenue (Million), by Device Type 2024 & 2032

- Figure 20: Japan Automotive Optoelectronics Market Volume (Billion), by Device Type 2024 & 2032

- Figure 21: Japan Automotive Optoelectronics Market Revenue Share (%), by Device Type 2024 & 2032

- Figure 22: Japan Automotive Optoelectronics Market Volume Share (%), by Device Type 2024 & 2032

- Figure 23: Japan Automotive Optoelectronics Market Revenue (Million), by Country 2024 & 2032

- Figure 24: Japan Automotive Optoelectronics Market Volume (Billion), by Country 2024 & 2032

- Figure 25: Japan Automotive Optoelectronics Market Revenue Share (%), by Country 2024 & 2032

- Figure 26: Japan Automotive Optoelectronics Market Volume Share (%), by Country 2024 & 2032

- Figure 27: China Automotive Optoelectronics Market Revenue (Million), by Device Type 2024 & 2032

- Figure 28: China Automotive Optoelectronics Market Volume (Billion), by Device Type 2024 & 2032

- Figure 29: China Automotive Optoelectronics Market Revenue Share (%), by Device Type 2024 & 2032

- Figure 30: China Automotive Optoelectronics Market Volume Share (%), by Device Type 2024 & 2032

- Figure 31: China Automotive Optoelectronics Market Revenue (Million), by Country 2024 & 2032

- Figure 32: China Automotive Optoelectronics Market Volume (Billion), by Country 2024 & 2032

- Figure 33: China Automotive Optoelectronics Market Revenue Share (%), by Country 2024 & 2032

- Figure 34: China Automotive Optoelectronics Market Volume Share (%), by Country 2024 & 2032

- Figure 35: South Korea Automotive Optoelectronics Market Revenue (Million), by Device Type 2024 & 2032

- Figure 36: South Korea Automotive Optoelectronics Market Volume (Billion), by Device Type 2024 & 2032

- Figure 37: South Korea Automotive Optoelectronics Market Revenue Share (%), by Device Type 2024 & 2032

- Figure 38: South Korea Automotive Optoelectronics Market Volume Share (%), by Device Type 2024 & 2032

- Figure 39: South Korea Automotive Optoelectronics Market Revenue (Million), by Country 2024 & 2032

- Figure 40: South Korea Automotive Optoelectronics Market Volume (Billion), by Country 2024 & 2032

- Figure 41: South Korea Automotive Optoelectronics Market Revenue Share (%), by Country 2024 & 2032

- Figure 42: South Korea Automotive Optoelectronics Market Volume Share (%), by Country 2024 & 2032

- Figure 43: Taiwan Automotive Optoelectronics Market Revenue (Million), by Device Type 2024 & 2032

- Figure 44: Taiwan Automotive Optoelectronics Market Volume (Billion), by Device Type 2024 & 2032

- Figure 45: Taiwan Automotive Optoelectronics Market Revenue Share (%), by Device Type 2024 & 2032

- Figure 46: Taiwan Automotive Optoelectronics Market Volume Share (%), by Device Type 2024 & 2032

- Figure 47: Taiwan Automotive Optoelectronics Market Revenue (Million), by Country 2024 & 2032

- Figure 48: Taiwan Automotive Optoelectronics Market Volume (Billion), by Country 2024 & 2032

- Figure 49: Taiwan Automotive Optoelectronics Market Revenue Share (%), by Country 2024 & 2032

- Figure 50: Taiwan Automotive Optoelectronics Market Volume Share (%), by Country 2024 & 2032

List of Tables

- Table 1: Global Automotive Optoelectronics Market Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Global Automotive Optoelectronics Market Volume Billion Forecast, by Region 2019 & 2032

- Table 3: Global Automotive Optoelectronics Market Revenue Million Forecast, by Device Type 2019 & 2032

- Table 4: Global Automotive Optoelectronics Market Volume Billion Forecast, by Device Type 2019 & 2032

- Table 5: Global Automotive Optoelectronics Market Revenue Million Forecast, by Region 2019 & 2032

- Table 6: Global Automotive Optoelectronics Market Volume Billion Forecast, by Region 2019 & 2032

- Table 7: Global Automotive Optoelectronics Market Revenue Million Forecast, by Device Type 2019 & 2032

- Table 8: Global Automotive Optoelectronics Market Volume Billion Forecast, by Device Type 2019 & 2032

- Table 9: Global Automotive Optoelectronics Market Revenue Million Forecast, by Country 2019 & 2032

- Table 10: Global Automotive Optoelectronics Market Volume Billion Forecast, by Country 2019 & 2032

- Table 11: Global Automotive Optoelectronics Market Revenue Million Forecast, by Device Type 2019 & 2032

- Table 12: Global Automotive Optoelectronics Market Volume Billion Forecast, by Device Type 2019 & 2032

- Table 13: Global Automotive Optoelectronics Market Revenue Million Forecast, by Country 2019 & 2032

- Table 14: Global Automotive Optoelectronics Market Volume Billion Forecast, by Country 2019 & 2032

- Table 15: Global Automotive Optoelectronics Market Revenue Million Forecast, by Device Type 2019 & 2032

- Table 16: Global Automotive Optoelectronics Market Volume Billion Forecast, by Device Type 2019 & 2032

- Table 17: Global Automotive Optoelectronics Market Revenue Million Forecast, by Country 2019 & 2032

- Table 18: Global Automotive Optoelectronics Market Volume Billion Forecast, by Country 2019 & 2032

- Table 19: Global Automotive Optoelectronics Market Revenue Million Forecast, by Device Type 2019 & 2032

- Table 20: Global Automotive Optoelectronics Market Volume Billion Forecast, by Device Type 2019 & 2032

- Table 21: Global Automotive Optoelectronics Market Revenue Million Forecast, by Country 2019 & 2032

- Table 22: Global Automotive Optoelectronics Market Volume Billion Forecast, by Country 2019 & 2032

- Table 23: Global Automotive Optoelectronics Market Revenue Million Forecast, by Device Type 2019 & 2032

- Table 24: Global Automotive Optoelectronics Market Volume Billion Forecast, by Device Type 2019 & 2032

- Table 25: Global Automotive Optoelectronics Market Revenue Million Forecast, by Country 2019 & 2032

- Table 26: Global Automotive Optoelectronics Market Volume Billion Forecast, by Country 2019 & 2032

- Table 27: Global Automotive Optoelectronics Market Revenue Million Forecast, by Device Type 2019 & 2032

- Table 28: Global Automotive Optoelectronics Market Volume Billion Forecast, by Device Type 2019 & 2032

- Table 29: Global Automotive Optoelectronics Market Revenue Million Forecast, by Country 2019 & 2032

- Table 30: Global Automotive Optoelectronics Market Volume Billion Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Automotive Optoelectronics Market?

The projected CAGR is approximately 7.30%.

2. Which companies are prominent players in the Automotive Optoelectronics Market?

Key companies in the market include SK Hynix Inc, Panasonic Corporation, Samsung Electronics, Omnivision Technologies Inc, Sony Corporation, Ams Osram AG, Signify Holding, Vishay Intertechnology Inc, Texas Instruments Inc, LITE-ON Technology Corporation, Rohm Company Limited, Mitsubishi Electric Corporation, Broadcom Inc, Sharp Corporatio.

3. What are the main segments of the Automotive Optoelectronics Market?

The market segments include Device Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 5.74 Million as of 2022.

5. What are some drivers contributing to market growth?

Technology Advancements. and AI Developments will Drive the Growth; Growing Demand for Electric Vehicles.

6. What are the notable trends driving market growth?

Image Sensors are Expected to Hold Major Market Share.

7. Are there any restraints impacting market growth?

Technology Advancements. and AI Developments will Drive the Growth; Growing Demand for Electric Vehicles.

8. Can you provide examples of recent developments in the market?

February 2024: TSMC, Sony Semiconductor Solutions Corporation, DENSO Corporation, and Toyota Motor Corporation bolstered their investment in Japan Advanced Semiconductor Manufacturing Inc. ("JASM"), a subsidiary primarily owned by TSMC in Kumamoto Prefecture, Japan. This investment aims to establish a second fab, slated to commence operations by the end of 2027. Coupled with JASM's first fab, set to launch in 2024, the collective investment in JASM will surpass USD 20 billion, backed by substantial support from the Japanese government.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million and volume, measured in Billion.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Automotive Optoelectronics Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Automotive Optoelectronics Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Automotive Optoelectronics Market?

To stay informed about further developments, trends, and reports in the Automotive Optoelectronics Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence