Key Insights

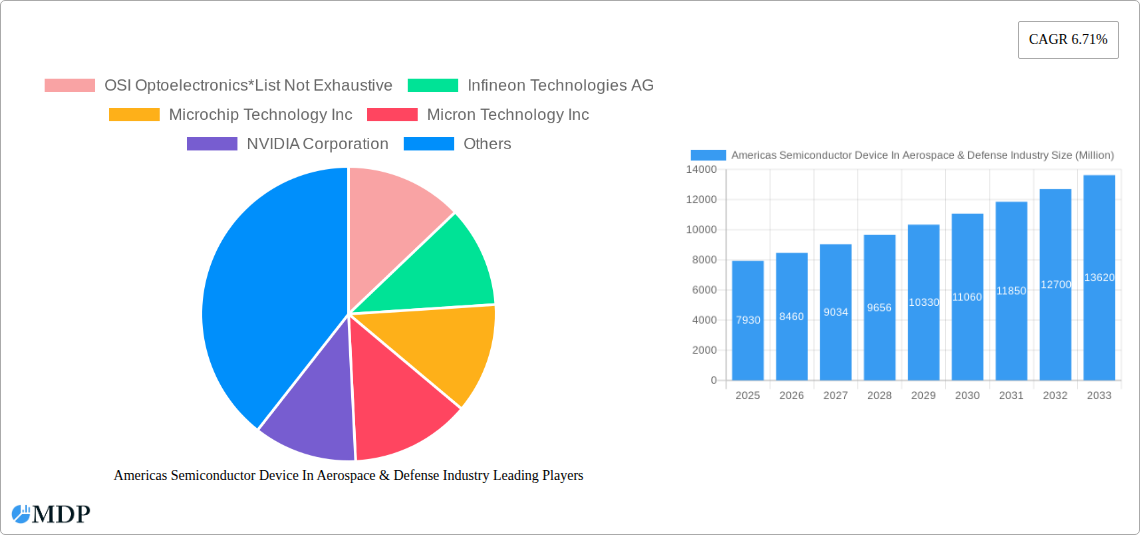

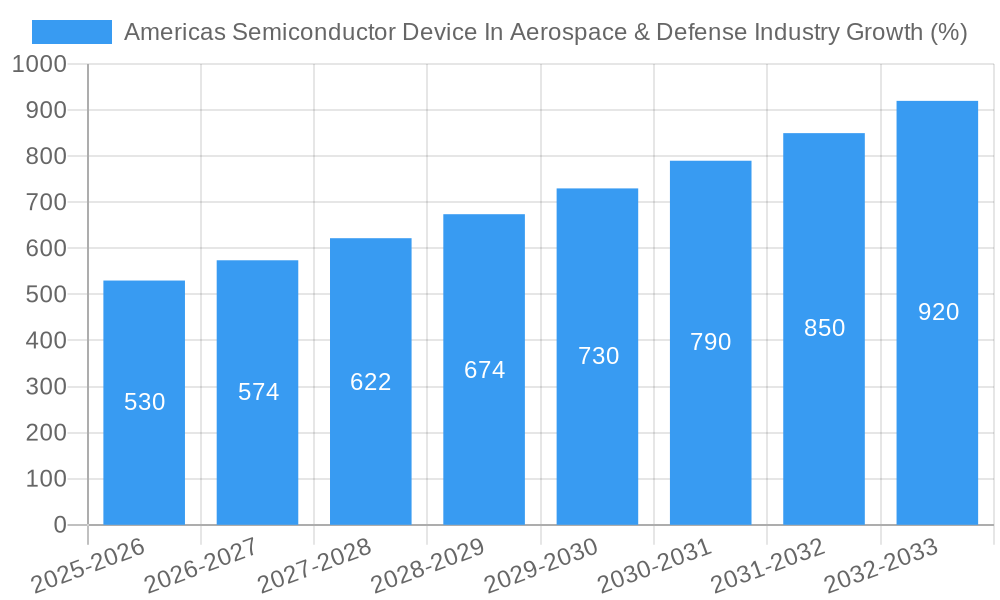

The Americas semiconductor device market within the aerospace and defense industry exhibits robust growth, projected to reach $7.93 billion in 2025 and maintain a Compound Annual Growth Rate (CAGR) of 6.71% from 2025 to 2033. This expansion is driven by several key factors. Firstly, increasing demand for advanced technologies in military and commercial aircraft, including improved navigation systems, sensor integration, and sophisticated communication capabilities, fuels the need for higher-performing and more reliable semiconductor devices. Secondly, the ongoing development of unmanned aerial vehicles (UAVs) and autonomous systems presents significant growth opportunities, necessitating miniaturized, energy-efficient semiconductors for diverse applications. Finally, government investments in defense modernization initiatives across North and South America contribute significantly to market expansion. The market is segmented by device type (discrete semiconductors, optoelectronics, sensors, and integrated circuits) and geography (United States, Canada, Brazil, and Mexico). Leading companies like Infineon, Texas Instruments, and Analog Devices are strategically positioned to capitalize on these trends, focusing on innovation and partnerships to meet the stringent reliability and performance requirements of the aerospace and defense sector. The market's growth is expected to be most pronounced in North America, driven primarily by the United States' significant investments in defense spending and technological advancements.

While the market displays strong growth potential, several challenges exist. Supply chain disruptions, particularly concerning specialized components, pose a significant risk. Furthermore, the stringent regulatory environment and stringent quality control measures required in the aerospace and defense sector necessitate substantial investments in research, development, and testing, potentially affecting profitability. Competitive pressures from established players and emerging entrants also pose a challenge. However, the long-term outlook remains positive, with consistent innovation in semiconductor technology and escalating demand for advanced defense systems expected to propel market growth in the coming years. The integration of artificial intelligence and machine learning into aerospace and defense applications will further drive demand for sophisticated semiconductor solutions in the forecast period.

Americas Semiconductor Device in Aerospace & Defense Industry: Market Report 2019-2033

This comprehensive report provides an in-depth analysis of the Americas semiconductor device market within the aerospace and defense industry, covering the period 2019-2033. Uncover key trends, growth drivers, challenges, and opportunities shaping this dynamic sector, with a focus on market size, leading players, and future projections. This report is essential for industry stakeholders, investors, and strategic decision-makers seeking actionable insights into this high-growth market.

Americas Semiconductor Device In Aerospace & Defense Industry Market Dynamics & Concentration

The Americas semiconductor market for aerospace and defense applications demonstrates a complex interplay of factors driving both growth and consolidation. Market concentration is moderate, with several major players holding significant shares, but also a healthy ecosystem of smaller, specialized companies. Innovation is a critical driver, fueled by the constant demand for improved performance, miniaturization, and enhanced reliability in military and space technologies. Stringent regulatory frameworks, particularly concerning quality, security, and export controls, shape the competitive landscape. Product substitution is gradual, with new technologies often coexisting with established ones, dependent on application-specific needs. End-user trends favour increased automation, AI integration, and improved sensor capabilities, driving demand for advanced semiconductor devices. Mergers and acquisitions (M&A) activity is notable, with larger companies strategically acquiring smaller firms to expand their product portfolios and technological expertise.

- Market Share: The top 5 companies hold approximately 65% of the market share in 2025, with the remainder dispersed among numerous smaller players.

- M&A Deal Counts: An average of xx M&A deals per year were recorded during the historical period (2019-2024), with an expected increase to xx per year during the forecast period.

Americas Semiconductor Device In Aerospace & Defense Industry Industry Trends & Analysis

The Americas aerospace and defense semiconductor market is experiencing robust growth, driven by increasing defense budgets, modernization initiatives, and technological advancements. The Compound Annual Growth Rate (CAGR) is estimated to be xx% during the forecast period (2025-2033). This expansion is fueled by a growing demand for high-performance computing, advanced sensors, and improved communication systems. Technological disruptions, such as the rise of AI and machine learning, are reshaping product design and application. The preference for smaller, more energy-efficient devices is a significant factor, driving innovation in miniaturization and power management. Competitive dynamics are characterized by intense rivalry among major semiconductor manufacturers, focusing on product differentiation, technological leadership, and supply chain security. Market penetration of advanced technologies, such as GaN and SiC, is steadily increasing, driven by their superior performance characteristics.

Leading Markets & Segments in Americas Semiconductor Device In Aerospace & Defense Industry

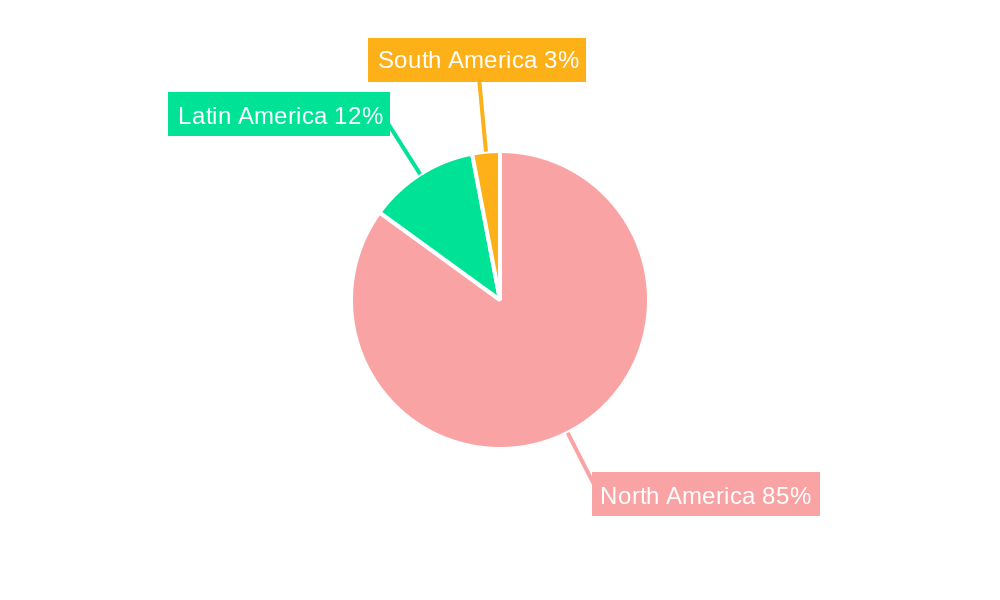

The United States dominates the Americas semiconductor device market for aerospace and defense, accounting for approximately xx% of the total market value in 2025. This leadership is attributed to the significant investments in defense and space exploration, a strong domestic semiconductor industry, and favorable government policies supporting technological innovation.

- United States: Strong defense spending, robust R&D, well-established semiconductor ecosystem.

- Canada: Growing aerospace sector, investments in defense modernization, proximity to US market.

- Mexico: Increasing manufacturing capabilities, proximity to the US market, cost-effective manufacturing.

- Brazil: Growing investments in defense and aerospace sectors.

By Device Type: Integrated Circuits hold the largest segment share in 2025, reflecting the increasing complexity and sophistication of aerospace and defense systems. This is followed by sensors, discrete semiconductors, and optoelectronics.

Americas Semiconductor Device In Aerospace & Defense Industry Product Developments

Recent product innovations focus on delivering higher performance, improved radiation hardness, and enhanced reliability in harsh environments. Applications range from navigation and guidance systems to advanced sensors and communication networks. Competitive advantages are primarily derived from superior performance, smaller form factors, and improved power efficiency. The market is seeing a growing trend toward the adoption of advanced materials and packaging technologies to meet demanding specifications.

Key Drivers of Americas Semiconductor Device In Aerospace & Defense Industry Growth

The growth of the Americas aerospace and defense semiconductor market is propelled by several key factors:

- Increased defense spending: Governments in the Americas are investing heavily in modernizing their military capabilities.

- Technological advancements: Innovations in semiconductor technology are leading to improved performance and functionality.

- Stringent regulatory requirements: Regulations driving improved safety and reliability.

Challenges in the Americas Semiconductor Device In Aerospace & Defense Industry Market

The market faces challenges including:

- Supply chain disruptions: Geopolitical factors and production bottlenecks can impact the availability of semiconductor devices.

- High manufacturing costs: Producing advanced semiconductor devices requires significant capital investment.

- Intense competition: The market is characterized by fierce competition among major semiconductor manufacturers.

Emerging Opportunities in Americas Semiconductor Device In Aerospace & Defense Industry

Significant opportunities exist for growth through:

- Advancements in AI and machine learning: These technologies are driving demand for high-performance computing.

- Development of new materials and packaging technologies: These advancements will enhance device performance and reliability.

- Strategic partnerships: Collaboration between semiconductor manufacturers and aerospace/defense companies can accelerate innovation.

Leading Players in the Americas Semiconductor Device In Aerospace & Defense Industry Sector

- OSI Optoelectronics

- Infineon Technologies AG

- Microchip Technology Inc

- Micron Technology Inc

- NVIDIA Corporation

- Texas Instruments Inc

- NXP Semiconductors

- STMicroelectronics NV

- Analog Devices Inc

- On Semiconductor Corporation

- Intel Corporation

Key Milestones in Americas Semiconductor Device In Aerospace & Defense Industry Industry

- December 2023: The USPTO launched the Semiconductor Technology Pilot Program, aiming to expedite patent reviews for semiconductor innovations, bolstering the domestic supply chain.

- February 2024: Joint launch of two HBTSS satellite sets by the Space Development Agency and Missile Defense Agency, demonstrating advancements in hypersonic threat detection.

Strategic Outlook for Americas Semiconductor Device In Aerospace & Defense Industry Market

The Americas semiconductor device market for aerospace and defense is poised for continued growth. Strategic opportunities include focusing on advanced technologies, strengthening supply chain resilience, and developing innovative solutions that meet the increasing demands of military and space applications. The market’s expansion is projected to be driven by sustained government investment, technological progress, and the rising need for sophisticated defense systems. The total market value is expected to reach xx Million by 2033.

Americas Semiconductor Device In Aerospace & Defense Industry Segmentation

-

1. Device Type

- 1.1. Discrete Semiconductors

- 1.2. Optoelectronics

- 1.3. Sensors

-

1.4. Integrated Circuits

- 1.4.1. Analog

- 1.4.2. Logic

- 1.4.3. Memory

- 1.4.4. Micro (MCU, MPU, Digital Signal Processor)

Americas Semiconductor Device In Aerospace & Defense Industry Segmentation By Geography

-

1. Americas

- 1.1. United States

- 1.2. Canada

- 1.3. Mexico

- 1.4. Brazil

- 1.5. Argentina

- 1.6. Chile

- 1.7. Colombia

- 1.8. Peru

Americas Semiconductor Device In Aerospace & Defense Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 6.71% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Rising Military Expenditure; Growing Adoption of Advanced Electronic & Semiconductor Devices

- 3.3. Market Restrains

- 3.3.1. Semiconductor Chip Shortage Issue

- 3.4. Market Trends

- 3.4.1. Rising Military Expenditure to Drive the Market's Growth

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Americas Semiconductor Device In Aerospace & Defense Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Device Type

- 5.1.1. Discrete Semiconductors

- 5.1.2. Optoelectronics

- 5.1.3. Sensors

- 5.1.4. Integrated Circuits

- 5.1.4.1. Analog

- 5.1.4.2. Logic

- 5.1.4.3. Memory

- 5.1.4.4. Micro (MCU, MPU, Digital Signal Processor)

- 5.2. Market Analysis, Insights and Forecast - by Region

- 5.2.1. Americas

- 5.1. Market Analysis, Insights and Forecast - by Device Type

- 6. Latin America Americas Semiconductor Device In Aerospace & Defense Industry Analysis, Insights and Forecast, 2019-2031

- 6.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 6.1.1 Mexico

- 6.1.2 Brazil

- 7. North America Americas Semiconductor Device In Aerospace & Defense Industry Analysis, Insights and Forecast, 2019-2031

- 7.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 7.1.1 United States

- 7.1.2 Canada

- 7.1.3 Mexico

- 8. South America Americas Semiconductor Device In Aerospace & Defense Industry Analysis, Insights and Forecast, 2019-2031

- 8.1. Market Analysis, Insights and Forecast - By Country/Sub-region

- 8.1.1 Brazil

- 8.1.2 Argentina

- 8.1.3 Rest of South America

- 9. Competitive Analysis

- 9.1. Market Share Analysis 2024

- 9.2. Company Profiles

- 9.2.1 OSI Optoelectronics*List Not Exhaustive

- 9.2.1.1. Overview

- 9.2.1.2. Products

- 9.2.1.3. SWOT Analysis

- 9.2.1.4. Recent Developments

- 9.2.1.5. Financials (Based on Availability)

- 9.2.2 Infineon Technologies AG

- 9.2.2.1. Overview

- 9.2.2.2. Products

- 9.2.2.3. SWOT Analysis

- 9.2.2.4. Recent Developments

- 9.2.2.5. Financials (Based on Availability)

- 9.2.3 Microchip Technology Inc

- 9.2.3.1. Overview

- 9.2.3.2. Products

- 9.2.3.3. SWOT Analysis

- 9.2.3.4. Recent Developments

- 9.2.3.5. Financials (Based on Availability)

- 9.2.4 Micron Technology Inc

- 9.2.4.1. Overview

- 9.2.4.2. Products

- 9.2.4.3. SWOT Analysis

- 9.2.4.4. Recent Developments

- 9.2.4.5. Financials (Based on Availability)

- 9.2.5 NVIDIA Corporation

- 9.2.5.1. Overview

- 9.2.5.2. Products

- 9.2.5.3. SWOT Analysis

- 9.2.5.4. Recent Developments

- 9.2.5.5. Financials (Based on Availability)

- 9.2.6 Texas Instruments Inc

- 9.2.6.1. Overview

- 9.2.6.2. Products

- 9.2.6.3. SWOT Analysis

- 9.2.6.4. Recent Developments

- 9.2.6.5. Financials (Based on Availability)

- 9.2.7 NXP Semiconductors

- 9.2.7.1. Overview

- 9.2.7.2. Products

- 9.2.7.3. SWOT Analysis

- 9.2.7.4. Recent Developments

- 9.2.7.5. Financials (Based on Availability)

- 9.2.8 STMicroelectronics NV

- 9.2.8.1. Overview

- 9.2.8.2. Products

- 9.2.8.3. SWOT Analysis

- 9.2.8.4. Recent Developments

- 9.2.8.5. Financials (Based on Availability)

- 9.2.9 Analog Devices Inc

- 9.2.9.1. Overview

- 9.2.9.2. Products

- 9.2.9.3. SWOT Analysis

- 9.2.9.4. Recent Developments

- 9.2.9.5. Financials (Based on Availability)

- 9.2.10 On Semiconductor Corporation

- 9.2.10.1. Overview

- 9.2.10.2. Products

- 9.2.10.3. SWOT Analysis

- 9.2.10.4. Recent Developments

- 9.2.10.5. Financials (Based on Availability)

- 9.2.11 Intel Corporation

- 9.2.11.1. Overview

- 9.2.11.2. Products

- 9.2.11.3. SWOT Analysis

- 9.2.11.4. Recent Developments

- 9.2.11.5. Financials (Based on Availability)

- 9.2.1 OSI Optoelectronics*List Not Exhaustive

List of Figures

- Figure 1: Americas Semiconductor Device In Aerospace & Defense Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: Americas Semiconductor Device In Aerospace & Defense Industry Share (%) by Company 2024

List of Tables

- Table 1: Americas Semiconductor Device In Aerospace & Defense Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: Americas Semiconductor Device In Aerospace & Defense Industry Revenue Million Forecast, by Device Type 2019 & 2032

- Table 3: Americas Semiconductor Device In Aerospace & Defense Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 4: Americas Semiconductor Device In Aerospace & Defense Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 5: Mexico Americas Semiconductor Device In Aerospace & Defense Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 6: Brazil Americas Semiconductor Device In Aerospace & Defense Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: Americas Semiconductor Device In Aerospace & Defense Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 8: United States Americas Semiconductor Device In Aerospace & Defense Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: Canada Americas Semiconductor Device In Aerospace & Defense Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: Mexico Americas Semiconductor Device In Aerospace & Defense Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: Americas Semiconductor Device In Aerospace & Defense Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 12: Brazil Americas Semiconductor Device In Aerospace & Defense Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 13: Argentina Americas Semiconductor Device In Aerospace & Defense Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 14: Rest of South America Americas Semiconductor Device In Aerospace & Defense Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 15: Americas Semiconductor Device In Aerospace & Defense Industry Revenue Million Forecast, by Device Type 2019 & 2032

- Table 16: Americas Semiconductor Device In Aerospace & Defense Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 17: United States Americas Semiconductor Device In Aerospace & Defense Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 18: Canada Americas Semiconductor Device In Aerospace & Defense Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 19: Mexico Americas Semiconductor Device In Aerospace & Defense Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 20: Brazil Americas Semiconductor Device In Aerospace & Defense Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 21: Argentina Americas Semiconductor Device In Aerospace & Defense Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 22: Chile Americas Semiconductor Device In Aerospace & Defense Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 23: Colombia Americas Semiconductor Device In Aerospace & Defense Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 24: Peru Americas Semiconductor Device In Aerospace & Defense Industry Revenue (Million) Forecast, by Application 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Americas Semiconductor Device In Aerospace & Defense Industry?

The projected CAGR is approximately 6.71%.

2. Which companies are prominent players in the Americas Semiconductor Device In Aerospace & Defense Industry?

Key companies in the market include OSI Optoelectronics*List Not Exhaustive, Infineon Technologies AG, Microchip Technology Inc, Micron Technology Inc, NVIDIA Corporation, Texas Instruments Inc, NXP Semiconductors, STMicroelectronics NV, Analog Devices Inc, On Semiconductor Corporation, Intel Corporation.

3. What are the main segments of the Americas Semiconductor Device In Aerospace & Defense Industry?

The market segments include Device Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 7.93 Million as of 2022.

5. What are some drivers contributing to market growth?

Rising Military Expenditure; Growing Adoption of Advanced Electronic & Semiconductor Devices.

6. What are the notable trends driving market growth?

Rising Military Expenditure to Drive the Market's Growth.

7. Are there any restraints impacting market growth?

Semiconductor Chip Shortage Issue.

8. Can you provide examples of recent developments in the market?

February 2024 - The Space Development Agency and Missile Defense Agency jointly launched two satellite sets, showcasing their intent to enhance capabilities for detecting and tracking adversaries' hypersonic weapons and other advanced threats. In tandem, the agencies deployed two Hypersonic and Ballistic Tracking Space Sensor (HBTSS) platforms, crafted by L3harris and Northrop Grumman, respectively, for the Missile Defense Agency.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 4950, and USD 6800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Americas Semiconductor Device In Aerospace & Defense Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Americas Semiconductor Device In Aerospace & Defense Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Americas Semiconductor Device In Aerospace & Defense Industry?

To stay informed about further developments, trends, and reports in the Americas Semiconductor Device In Aerospace & Defense Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence