Key Insights

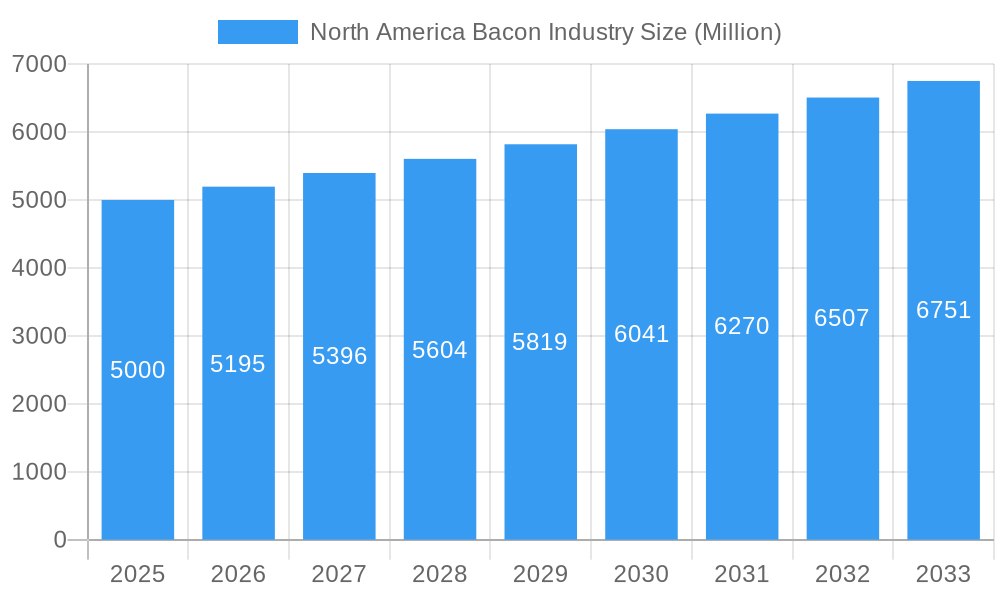

The North American bacon market, valued at approximately $5 billion in 2025, is projected to experience steady growth, driven primarily by increasing consumer demand for convenient ready-to-eat options and the enduring popularity of bacon in various culinary applications. The 3.90% CAGR indicates a consistent expansion, with the market expected to reach approximately $6.5 billion by 2033. This growth is fueled by several factors, including the rising disposable incomes in North America leading to increased spending on premium food products, innovative product launches like flavored bacons and organic options catering to health-conscious consumers, and robust growth in the food service sector, particularly restaurants and cafes integrating bacon into a wider range of menu items. The retail channel continues to be a significant contributor, with supermarkets and grocery stores offering various bacon types and sizes, contributing to market accessibility.

North America Bacon Industry Market Size (In Billion)

However, factors such as fluctuating pork prices, concerns regarding saturated fat content, and increasing competition from alternative protein sources (e.g., plant-based bacon) pose potential restraints to market growth. To mitigate these challenges, major players are focusing on strategies such as diversification of product offerings, strategic partnerships, and increased investment in marketing and branding to highlight the unique attributes of their bacon products. The market segmentation clearly indicates a strong preference for ready-to-eat bacon, a trend likely to continue as consumers prioritize convenience. The dominance of established players like Hormel Foods, Tyson Foods, and Kraft Heinz, coupled with the emergence of smaller regional producers, underscores a dynamic competitive landscape. Geographical focus remains on the United States, with Canada and Mexico contributing significantly to the overall North American market.

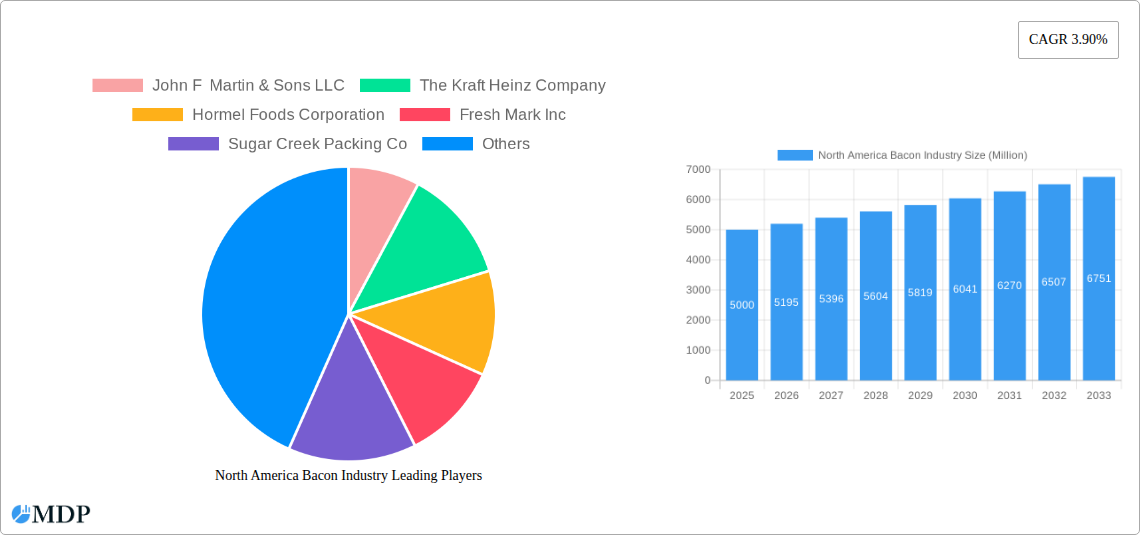

North America Bacon Industry Company Market Share

North America Bacon Industry Report: 2019-2033

Dive into the sizzling world of the North American bacon industry with this comprehensive market report, covering the period 2019-2033. This in-depth analysis provides critical insights into market dynamics, key players, emerging trends, and future growth opportunities, equipping you with the knowledge to navigate this dynamic sector. With a focus on key segments (Standard Bacon, Ready-to-Eat Bacon, Food Service, and Retail Channels), this report offers actionable intelligence for strategic decision-making.

This report is your essential guide, incorporating data from 2019-2024 (Historical Period), 2025 (Base and Estimated Year), and projecting to 2033 (Forecast Period).

North America Bacon Industry Market Dynamics & Concentration

The North American bacon market, valued at xx Million in 2024, exhibits a moderately concentrated structure with several dominant players controlling a significant market share. Market concentration is influenced by factors such as economies of scale in production, strong brand recognition, and established distribution networks. Key players like Hormel Foods Corporation and Tyson Foods hold substantial shares, while smaller regional players cater to niche markets.

Market Dynamics:

- Innovation Drivers: The industry is driven by innovation in product formats (e.g., ready-to-eat, organic, flavored bacons), packaging, and production technologies to enhance efficiency and appeal to diverse consumer preferences.

- Regulatory Frameworks: Food safety regulations, labeling requirements, and animal welfare standards significantly impact the industry's operational landscape. Compliance costs and changing regulations represent ongoing challenges.

- Product Substitutes: Plant-based bacon alternatives are emerging as a significant competitive pressure, impacting market share of traditional bacon products. The recent launch of Umaro Foods' seaweed bacon illustrates this trend.

- End-User Trends: Health-conscious consumers are driving demand for leaner bacon options, reduced sodium versions, and sustainably sourced products.

- M&A Activities: The past five years have seen xx M&A deals, mainly focused on consolidating market share and expanding product portfolios. Major players are actively engaged in strategic acquisitions to enhance their competitive positioning. For example, while specific numbers are not available, the acquisition of smaller regional players by large corporations is a common occurrence.

North America Bacon Industry Industry Trends & Analysis

The North American bacon market is experiencing a CAGR of xx% during the forecast period (2025-2033). Market penetration is high in established markets, but growth is being fuelled by expansion into newer segments and channels.

- Market Growth Drivers: Rising disposable incomes, increasing demand for convenience foods (ready-to-eat bacon), and expanding food service sectors contribute significantly to market expansion.

- Technological Disruptions: Automation in production processes is transforming efficiency and reducing labor costs, as evidenced by Tyson Foods’ USD 1.3 Billion investment in automation. This trend is expected to continue driving cost reduction and increased production capacity.

- Consumer Preferences: Consumers increasingly value natural and organic options, along with products that align with health and wellness trends. This shifts demand towards low-sodium, reduced-fat, and minimally processed bacon variants.

- Competitive Dynamics: Intense competition among established players and the emergence of new players (particularly in the plant-based bacon segment) are shaping market dynamics. Price competitiveness and product differentiation remain crucial factors.

Leading Markets & Segments in North America Bacon Industry

The United States dominates the North American bacon market, driven by high per capita consumption and well-established distribution networks. The retail channel remains the largest distribution segment, although the food service channel exhibits high growth potential due to increasing demand from restaurants and other food service establishments.

Dominant Segments:

- Product Type: Standard bacon accounts for the majority of market share, although ready-to-eat bacon is experiencing robust growth driven by convenience and ease of preparation.

- Distribution Channel: The retail channel maintains its dominant position, benefiting from widespread availability in supermarkets and grocery stores. However, the food service channel is a key growth area, driven by demand from fast-casual restaurants and quick-service eateries.

Key Drivers:

- Strong consumer demand for bacon products, across both retail and food service channels

- High per capita consumption of pork products in North America.

- Extensive retail infrastructure and distribution networks

- Favorable economic conditions and increasing disposable incomes

North America Bacon Industry Product Developments

Recent product innovations focus on enhancing convenience (ready-to-cook and microwaveable options), catering to health-conscious consumers (lean bacon, reduced-sodium options), and exploring alternative protein sources (plant-based and seaweed bacon). These innovations are aimed at broadening market appeal and responding to evolving consumer preferences. Technological advancements in processing and preservation techniques are also driving improvements in product quality and shelf life.

Key Drivers of North America Bacon Industry Growth

Several factors are driving growth in the North American bacon market. These include: rising disposable incomes boosting consumer spending on convenient and premium food items, the expanding food service sector increasing demand for bacon in restaurants, and technological advancements like automation enhancing production efficiency and lowering costs. The growing popularity of bacon in diverse cuisines and dishes also contributes significantly to market expansion.

Challenges in the North America Bacon Industry Market

The industry faces challenges such as increasing input costs (pork prices, packaging materials), stringent food safety regulations requiring substantial investments in compliance, and fluctuating consumer demand affected by economic cycles. The growing popularity of plant-based meat alternatives poses a further competitive challenge, potentially reducing market share of traditional bacon. Supply chain disruptions are also a source of concern.

Emerging Opportunities in North America Bacon Industry

Significant opportunities exist for innovation in bacon products, particularly within the health-conscious segment with reduced-sodium, leaner, and plant-based alternatives. Strategic partnerships and collaborations within the food service sector can help expand market reach. Exploring new flavor profiles and packaging formats presents opportunities to attract diverse consumer segments. Expansion into emerging markets within North America (e.g., underserved geographic areas) also provides potential for growth.

Leading Players in the North America Bacon Industry Sector

- John F Martin & Sons LLC

- The Kraft Heinz Company

- Hormel Foods Corporation

- Fresh Mark Inc

- Sugar Creek Packing Co

- Maple Leaf Foods

- JBS SA

- Tyson Foods

- Seaboard Foods

Key Milestones in North America Bacon Industry Industry

- February 2022: Tyson Foods announces a USD 1.3 Billion investment in automation to boost production capacity and efficiency. This signifies a significant shift towards automation within the industry.

- March 2022: Seaboard Foods launches its "top tier" Prairie Fresh USA Prime bacon, expanding its product portfolio to target premium market segments.

- June 2022: Umaro Foods launches seaweed bacon in several US restaurants, marking the entry of a novel plant-based protein into the bacon market and highlighting competitive pressure from alternative protein sources. This event reflects consumer interest in alternative protein sources and growing competition in the industry.

Strategic Outlook for North America Bacon Industry Market

The North American bacon market is poised for continued growth, driven by evolving consumer preferences, technological innovations, and strategic initiatives by leading players. Focus on product diversification, particularly in healthy and convenient options, will be crucial for maintaining competitive advantage. Expansion into new channels and markets, along with strategic partnerships, will further fuel market expansion throughout the forecast period. The increasing adoption of sustainable and ethical sourcing practices will also play a significant role in shaping the industry's future.

North America Bacon Industry Segmentation

-

1. Product Type

- 1.1. Standard Bacon

- 1.2. Ready-to-Eat Bacon (Includes Microwavable)

-

2. Distribution Channel

-

2.1. Food Service Channel

- 2.1.1. Full-Service Restaurants

- 2.1.2. Quick-Service Restaurants

- 2.1.3. Cafes and Bars

- 2.1.4. Other Food Service Channels

-

2.2. Retail Channel

- 2.2.1. Supermarkets/Hypermarkets

- 2.2.2. Specialty Stores

- 2.2.3. Online Stores

- 2.2.4. Other Retail Channels

-

2.3. By Geography

- 2.3.1. United States

- 2.3.2. Canada

- 2.3.3. Mexico

- 2.3.4. Rest of North America

-

2.1. Food Service Channel

North America Bacon Industry Segmentation By Geography

-

1. United States

- 1.1. Canada

- 1.2. Mexico

- 1.3. Rest of North America

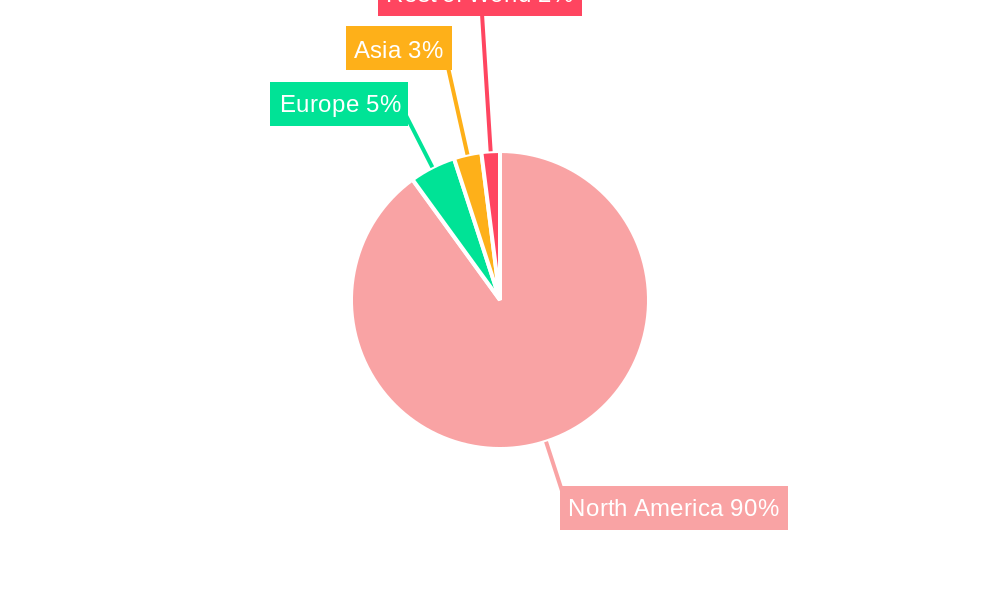

North America Bacon Industry Regional Market Share

Geographic Coverage of North America Bacon Industry

North America Bacon Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 2.9% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing consumer Demand for Convenience Foods; Innovation in Bacon Varieties

- 3.3. Market Restrains

- 3.3.1. High fat and sodium content in bacon can lead to health issues impacting consumer preference

- 3.4. Market Trends

- 3.4.1. Increasing Preference for Premium Bacon Products as Breakfast Option

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. North America Bacon Industry Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 5.1.1. Standard Bacon

- 5.1.2. Ready-to-Eat Bacon (Includes Microwavable)

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Food Service Channel

- 5.2.1.1. Full-Service Restaurants

- 5.2.1.2. Quick-Service Restaurants

- 5.2.1.3. Cafes and Bars

- 5.2.1.4. Other Food Service Channels

- 5.2.2. Retail Channel

- 5.2.2.1. Supermarkets/Hypermarkets

- 5.2.2.2. Specialty Stores

- 5.2.2.3. Online Stores

- 5.2.2.4. Other Retail Channels

- 5.2.3. By Geography

- 5.2.3.1. United States

- 5.2.3.2. Canada

- 5.2.3.3. Mexico

- 5.2.3.4. Rest of North America

- 5.2.1. Food Service Channel

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. United States

- 5.1. Market Analysis, Insights and Forecast - by Product Type

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2025

- 6.2. Company Profiles

- 6.2.1 John F Martin & Sons LLC

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 The Kraft Heinz Company

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Hormel Foods Corporation

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Fresh Mark Inc

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Sugar Creek Packing Co

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 Maple Leaf Foods

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 JBS SA

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Tyson Foods

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Seaboard Foods

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.1 John F Martin & Sons LLC

List of Figures

- Figure 1: North America Bacon Industry Revenue Breakdown (undefined, %) by Product 2025 & 2033

- Figure 2: North America Bacon Industry Share (%) by Company 2025

List of Tables

- Table 1: North America Bacon Industry Revenue undefined Forecast, by Product Type 2020 & 2033

- Table 2: North America Bacon Industry Revenue undefined Forecast, by Distribution Channel 2020 & 2033

- Table 3: North America Bacon Industry Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: North America Bacon Industry Revenue undefined Forecast, by Product Type 2020 & 2033

- Table 5: North America Bacon Industry Revenue undefined Forecast, by Distribution Channel 2020 & 2033

- Table 6: North America Bacon Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: Canada North America Bacon Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: Mexico North America Bacon Industry Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Rest of North America North America Bacon Industry Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the North America Bacon Industry?

The projected CAGR is approximately 2.9%.

2. Which companies are prominent players in the North America Bacon Industry?

Key companies in the market include John F Martin & Sons LLC, The Kraft Heinz Company, Hormel Foods Corporation, Fresh Mark Inc, Sugar Creek Packing Co, Maple Leaf Foods, JBS SA, Tyson Foods, Seaboard Foods.

3. What are the main segments of the North America Bacon Industry?

The market segments include Product Type, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

Increasing consumer Demand for Convenience Foods; Innovation in Bacon Varieties.

6. What are the notable trends driving market growth?

Increasing Preference for Premium Bacon Products as Breakfast Option.

7. Are there any restraints impacting market growth?

High fat and sodium content in bacon can lead to health issues impacting consumer preference.

8. Can you provide examples of recent developments in the market?

June 2022: Umaro Foods' novel seaweed bacon was launched in several renowned United States restaurants. Umaro Foods introduced seaweed-based bacon into three US restaurants for the first time, allowing customers to try the brand's novel protein. UMARO bacon was featured in various specialty dishes at San Francisco's Michelin-starred Sorrel Restaurant, New York City's Egg Shop, and Nashville's D'Andrews Bakery and Cafe. The company intends to expand into more restaurants in the Bay Area, Los Angeles, and elsewhere.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "North America Bacon Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the North America Bacon Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the North America Bacon Industry?

To stay informed about further developments, trends, and reports in the North America Bacon Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence