Key Insights

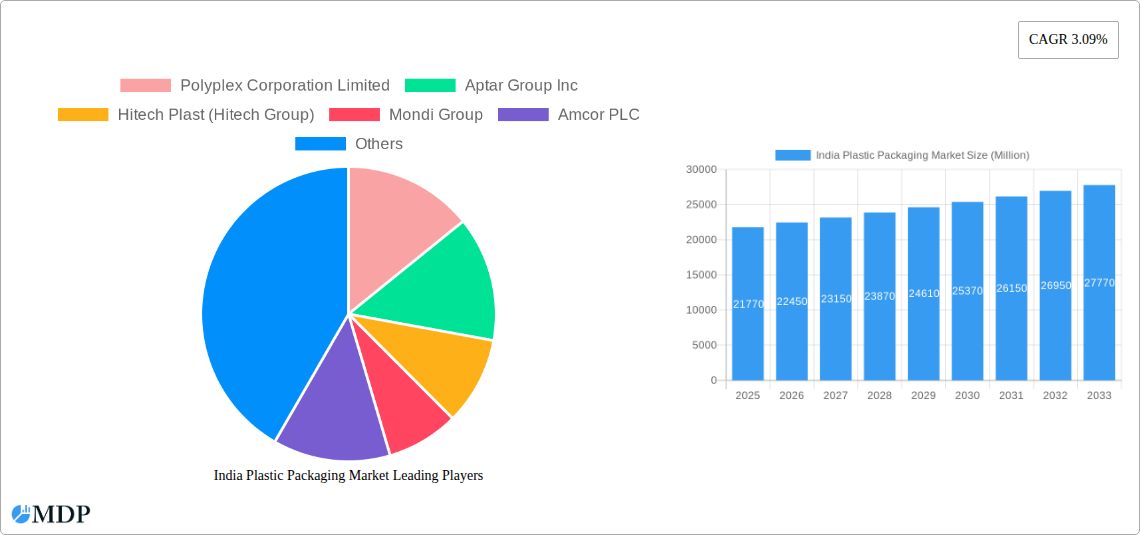

The India plastic packaging market, valued at $21.77 billion in 2025, is projected to experience robust growth, driven by a burgeoning food and beverage sector, rising consumer spending, and the increasing adoption of e-commerce. The market's Compound Annual Growth Rate (CAGR) of 3.09% from 2025 to 2033 reflects a steady expansion, although this rate is likely influenced by various factors. The significant growth in packaged food and beverage consumption, fueled by a growing population and changing lifestyles, is a primary driver. Furthermore, the expanding healthcare sector, with its demand for safe and effective packaging solutions, contributes to market growth. However, the market faces constraints such as stringent government regulations regarding plastic waste management and increasing environmental concerns pushing for sustainable alternatives like biodegradable packaging. The market is segmented by product type (bottles & jars, trays & containers, pouches, bags, films & wraps, others), packaging type (flexible and rigid), and end-user industries (food, beverage, healthcare, personal care, household, others). Regional variations exist, with potential higher growth in urban centers and more developed regions. Leading players such as Amcor PLC, Berry Global Inc., and others are strategically expanding their production capacities and exploring innovative packaging solutions to capitalize on the market's potential.

The competitive landscape is characterized by both domestic and international players, vying for market share through product diversification, technological advancements, and strategic partnerships. The increasing adoption of advanced plastic packaging materials with improved barrier properties and enhanced shelf life contributes to market expansion. However, the push towards sustainability necessitates the development and adoption of eco-friendly alternatives, including recyclable and biodegradable packaging materials, thus presenting both opportunities and challenges to the industry. The increasing awareness of environmental impact necessitates a shift towards sustainable packaging solutions. Companies are focusing on recycling initiatives and investing in research and development of bio-plastics and other environmentally friendly materials to address growing concerns about plastic waste. This shift towards sustainability will play a crucial role in shaping the future trajectory of the Indian plastic packaging market.

India Plastic Packaging Market: A Comprehensive Report (2019-2033)

This insightful report provides a detailed analysis of the burgeoning India plastic packaging market, offering crucial data and forecasts for informed decision-making. Covering the period from 2019 to 2033, with a base year of 2025, this study examines market dynamics, leading players, emerging trends, and future growth prospects. The report is invaluable for industry stakeholders, investors, and strategic planners seeking to navigate this dynamic sector. The market is expected to reach xx Million by 2033, exhibiting a CAGR of xx% during the forecast period (2025-2033).

India Plastic Packaging Market Market Dynamics & Concentration

The Indian plastic packaging market is characterized by a moderately concentrated landscape, with several large players and a multitude of smaller firms. Market share is distributed across multinational corporations and domestic manufacturers, with intense competition driving innovation and efficiency gains. Key dynamics shaping the market include:

- Innovation Drivers: Sustainable packaging solutions, lightweighting technologies, and improved barrier properties are major innovation drivers, responding to environmental concerns and consumer demands.

- Regulatory Frameworks: Government regulations concerning plastic waste management, such as the ban on single-use plastics, are reshaping market strategies, pushing companies to adopt eco-friendly alternatives. This has resulted in a notable increase in the adoption of recycled content.

- Product Substitutes: Growing awareness of environmental impact is leading to increased adoption of biodegradable and compostable packaging materials, creating a competitive pressure on traditional plastic packaging.

- End-User Trends: The burgeoning food and beverage sector, coupled with rising disposable incomes and changing lifestyles, fuels the demand for convenient and attractive packaging. The healthcare sector also shows robust growth in demand for specialized plastic packaging, owing to its protective and barrier properties.

- M&A Activities: The market has witnessed a moderate level of mergers and acquisitions, with larger players consolidating their market position and expanding their product portfolios. The estimated number of M&A deals in the last 5 years is xx. Market share consolidation is evident, with top 5 players holding approximately xx% of market share in 2024.

India Plastic Packaging Market Industry Trends & Analysis

The Indian plastic packaging market is experiencing robust growth, driven by several factors. The increasing demand for packaged goods across diverse sectors, particularly food and beverages, personal care, and pharmaceuticals, fuels this expansion. Technological advancements in material science and manufacturing processes are improving product performance, efficiency, and sustainability. The shift towards e-commerce and online retail further contributes to the growth of the market, requiring efficient and cost-effective packaging solutions. Consumer preferences increasingly favor convenient, attractive, and eco-friendly packaging. However, the industry faces competitive pressures, with both domestic and international players vying for market share. The market is expected to grow at a significant CAGR of xx% from 2025 to 2033, achieving a market penetration of xx% by 2033.

Leading Markets & Segments in India Plastic Packaging Market

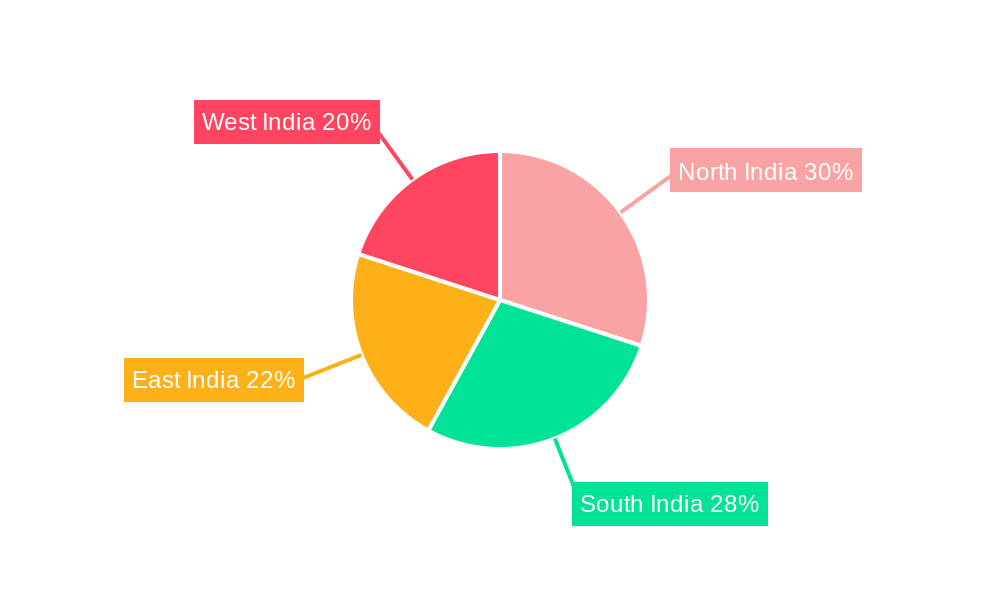

The Indian plastic packaging market is geographically diverse, with significant regional variations in demand and growth rates. Metropolitan areas and major industrial hubs demonstrate higher consumption rates. Within the segmentation:

By Product Type: Bags and films are currently the dominant segment, driven by their versatility and widespread application in multiple industries, followed by bottles and jars.

- Key Drivers for Bottles and Jars: Increasing demand from the food and beverage sector, particularly for packaged water and beverages.

- Key Drivers for Bags: Widespread use in food and grocery packaging and retail.

- Key Drivers for Flexible Packaging: Its cost-effectiveness and ease of transport.

- Key Drivers for Rigid Packaging: Demand for high-barrier packaging in food and pharmaceuticals.

By Packaging Type: Flexible plastic packaging holds a larger market share compared to rigid packaging due to lower cost and wider applications.

By End User: The food and beverage sector is the largest end-user segment, contributing to xx% of the total market share, closely followed by the healthcare sector. Rapid growth in the personal care segment is also a major factor.

- Key Drivers for Food and Beverage: Rising disposable incomes and changing consumption patterns.

- Key Drivers for Healthcare: Growing demand for pharmaceuticals and medical devices.

India Plastic Packaging Market Product Developments

The Indian plastic packaging market is witnessing significant product innovation, driven by the need for sustainability and enhanced functionality. Developments include lightweighting technologies to reduce material usage, the incorporation of recycled content (rPET), and the development of biodegradable and compostable alternatives. These developments respond to both environmental concerns and shifting consumer preferences, allowing manufacturers to meet the changing demands of the market while offering competitive advantages. This includes increasing use of barrier films in flexible packaging for longer shelf life and tamper-evident packaging in the pharmaceutical segment.

Key Drivers of India Plastic Packaging Market Growth

Several factors are driving the growth of the India plastic packaging market. These include:

- Technological advancements: Innovations in materials and manufacturing processes are producing more sustainable and efficient packaging solutions.

- Economic growth: Rising disposable incomes and expanding middle class are increasing demand for packaged goods.

- Favorable government policies: Although there are restrictions on single-use plastics, government initiatives aimed at promoting manufacturing and infrastructure development are also indirectly contributing to the market.

Challenges in the India Plastic Packaging Market

The industry faces several challenges, including:

- Stringent environmental regulations: The ban on certain types of plastics and the push for sustainable alternatives are creating compliance costs for manufacturers.

- Fluctuating raw material prices: The volatility of crude oil prices significantly impacts the cost of plastic resin, affecting profitability and pricing strategies.

- Intense competition: The market is highly competitive, particularly in the flexible packaging segment, making it difficult for smaller players to compete. This has led to xx% decrease in profit margins for some smaller players.

Emerging Opportunities in India Plastic Packaging Market

The long-term growth of the Indian plastic packaging market hinges on several factors. The development of sustainable packaging solutions and the increasing demand for e-commerce packaging present major opportunities. Strategic partnerships and collaborations across the value chain, along with investments in advanced manufacturing technologies, are crucial for capitalizing on this potential. Furthermore, expanding into rural markets with appropriate packaging solutions offers significant expansion opportunities.

Leading Players in the India Plastic Packaging Market Sector

- Polyplex Corporation Limited

- Aptar Group Inc

- Hitech Plast (Hitech Group)

- Mondi Group

- Amcor PLC

- TCPL Packaging Ltd

- Jindal Poly Films Limited

- Constantia Flexibles

- Berry Global Inc

- Cosmo Films Ltd (Cosmo First Limited)

- Sealed Air Corporation

- Manjushree Tecnopack Ltd

Key Milestones in India Plastic Packaging Market Industry

- October 2023: Coca-Cola India launched 100% recycled polyethylene terephthalate (rPET)-made bottles, showcasing a commitment to sustainability and influencing industry practices.

- January 2024: Coca-Cola India and Reliance Retail launched the 'Bhool na Jana, Plastic Bottles Lautana' initiative, highlighting a significant step towards improved plastic waste management and recycling infrastructure in India. This initiative signals a positive shift towards circular economy models in the packaging sector.

Strategic Outlook for India Plastic Packaging Market Market

The future of the Indian plastic packaging market is promising, driven by economic growth, evolving consumer preferences, and the increasing focus on sustainable packaging solutions. Companies that invest in innovation, sustainable practices, and efficient supply chains will be best positioned for long-term success. Strategic partnerships, mergers, and acquisitions will play a key role in shaping the market landscape, while the adoption of advanced technologies will enhance efficiency and competitiveness. The market presents attractive opportunities for both domestic and international players willing to embrace sustainability and adapt to changing market dynamics.

India Plastic Packaging Market Segmentation

-

1. Packaging Type

- 1.1. Flexible Plastic Packaging

- 1.2. Rigid Plastic Pacakaging

-

2. End User

- 2.1. Food

- 2.2. Beverage

- 2.3. Healthcare

- 2.4. Personal Care and Household

- 2.5. Other End Users

-

3. Product Type

- 3.1. Bottles and Jars

- 3.2. Trays and Containers

- 3.3. Pouches

- 3.4. Bags

- 3.5. Films and Wraps

- 3.6. Other Product Types

India Plastic Packaging Market Segmentation By Geography

- 1. India

India Plastic Packaging Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of 3.09% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Adoption of Lightweight-packaging Methods; Increased Eco-friendly Packaging and Recycled Plastic; Growing E-commerc Industry is Expected to Drive Growth

- 3.3. Market Restrains

- 3.3.1. High Price of Raw Material (Plastic Resin); Government Regulations and Environmental Concerns

- 3.4. Market Trends

- 3.4.1. Food Segment to Hold a Significant Share

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. India Plastic Packaging Market Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Packaging Type

- 5.1.1. Flexible Plastic Packaging

- 5.1.2. Rigid Plastic Pacakaging

- 5.2. Market Analysis, Insights and Forecast - by End User

- 5.2.1. Food

- 5.2.2. Beverage

- 5.2.3. Healthcare

- 5.2.4. Personal Care and Household

- 5.2.5. Other End Users

- 5.3. Market Analysis, Insights and Forecast - by Product Type

- 5.3.1. Bottles and Jars

- 5.3.2. Trays and Containers

- 5.3.3. Pouches

- 5.3.4. Bags

- 5.3.5. Films and Wraps

- 5.3.6. Other Product Types

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. India

- 5.1. Market Analysis, Insights and Forecast - by Packaging Type

- 6. North India India Plastic Packaging Market Analysis, Insights and Forecast, 2019-2031

- 7. South India India Plastic Packaging Market Analysis, Insights and Forecast, 2019-2031

- 8. East India India Plastic Packaging Market Analysis, Insights and Forecast, 2019-2031

- 9. West India India Plastic Packaging Market Analysis, Insights and Forecast, 2019-2031

- 10. Competitive Analysis

- 10.1. Market Share Analysis 2024

- 10.2. Company Profiles

- 10.2.1 Polyplex Corporation Limited

- 10.2.1.1. Overview

- 10.2.1.2. Products

- 10.2.1.3. SWOT Analysis

- 10.2.1.4. Recent Developments

- 10.2.1.5. Financials (Based on Availability)

- 10.2.2 Aptar Group Inc

- 10.2.2.1. Overview

- 10.2.2.2. Products

- 10.2.2.3. SWOT Analysis

- 10.2.2.4. Recent Developments

- 10.2.2.5. Financials (Based on Availability)

- 10.2.3 Hitech Plast (Hitech Group)

- 10.2.3.1. Overview

- 10.2.3.2. Products

- 10.2.3.3. SWOT Analysis

- 10.2.3.4. Recent Developments

- 10.2.3.5. Financials (Based on Availability)

- 10.2.4 Mondi Group

- 10.2.4.1. Overview

- 10.2.4.2. Products

- 10.2.4.3. SWOT Analysis

- 10.2.4.4. Recent Developments

- 10.2.4.5. Financials (Based on Availability)

- 10.2.5 Amcor PLC

- 10.2.5.1. Overview

- 10.2.5.2. Products

- 10.2.5.3. SWOT Analysis

- 10.2.5.4. Recent Developments

- 10.2.5.5. Financials (Based on Availability)

- 10.2.6 TCPL Packaging Ltd

- 10.2.6.1. Overview

- 10.2.6.2. Products

- 10.2.6.3. SWOT Analysis

- 10.2.6.4. Recent Developments

- 10.2.6.5. Financials (Based on Availability)

- 10.2.7 Jindal Poly Films Limited

- 10.2.7.1. Overview

- 10.2.7.2. Products

- 10.2.7.3. SWOT Analysis

- 10.2.7.4. Recent Developments

- 10.2.7.5. Financials (Based on Availability)

- 10.2.8 Constantia Flexibles*List Not Exhaustive

- 10.2.8.1. Overview

- 10.2.8.2. Products

- 10.2.8.3. SWOT Analysis

- 10.2.8.4. Recent Developments

- 10.2.8.5. Financials (Based on Availability)

- 10.2.9 Berry Global Inc

- 10.2.9.1. Overview

- 10.2.9.2. Products

- 10.2.9.3. SWOT Analysis

- 10.2.9.4. Recent Developments

- 10.2.9.5. Financials (Based on Availability)

- 10.2.10 Cosmo Films Ltd (Cosmo First Limited)

- 10.2.10.1. Overview

- 10.2.10.2. Products

- 10.2.10.3. SWOT Analysis

- 10.2.10.4. Recent Developments

- 10.2.10.5. Financials (Based on Availability)

- 10.2.11 Sealed Air Corporation

- 10.2.11.1. Overview

- 10.2.11.2. Products

- 10.2.11.3. SWOT Analysis

- 10.2.11.4. Recent Developments

- 10.2.11.5. Financials (Based on Availability)

- 10.2.12 Manjushree Tecnopack Ltd

- 10.2.12.1. Overview

- 10.2.12.2. Products

- 10.2.12.3. SWOT Analysis

- 10.2.12.4. Recent Developments

- 10.2.12.5. Financials (Based on Availability)

- 10.2.1 Polyplex Corporation Limited

List of Figures

- Figure 1: India Plastic Packaging Market Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: India Plastic Packaging Market Share (%) by Company 2024

List of Tables

- Table 1: India Plastic Packaging Market Revenue Million Forecast, by Region 2019 & 2032

- Table 2: India Plastic Packaging Market Revenue Million Forecast, by Packaging Type 2019 & 2032

- Table 3: India Plastic Packaging Market Revenue Million Forecast, by End User 2019 & 2032

- Table 4: India Plastic Packaging Market Revenue Million Forecast, by Product Type 2019 & 2032

- Table 5: India Plastic Packaging Market Revenue Million Forecast, by Region 2019 & 2032

- Table 6: India Plastic Packaging Market Revenue Million Forecast, by Country 2019 & 2032

- Table 7: North India India Plastic Packaging Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: South India India Plastic Packaging Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: East India India Plastic Packaging Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: West India India Plastic Packaging Market Revenue (Million) Forecast, by Application 2019 & 2032

- Table 11: India Plastic Packaging Market Revenue Million Forecast, by Packaging Type 2019 & 2032

- Table 12: India Plastic Packaging Market Revenue Million Forecast, by End User 2019 & 2032

- Table 13: India Plastic Packaging Market Revenue Million Forecast, by Product Type 2019 & 2032

- Table 14: India Plastic Packaging Market Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the India Plastic Packaging Market?

The projected CAGR is approximately 3.09%.

2. Which companies are prominent players in the India Plastic Packaging Market?

Key companies in the market include Polyplex Corporation Limited, Aptar Group Inc, Hitech Plast (Hitech Group), Mondi Group, Amcor PLC, TCPL Packaging Ltd, Jindal Poly Films Limited, Constantia Flexibles*List Not Exhaustive, Berry Global Inc, Cosmo Films Ltd (Cosmo First Limited), Sealed Air Corporation, Manjushree Tecnopack Ltd.

3. What are the main segments of the India Plastic Packaging Market?

The market segments include Packaging Type, End User, Product Type.

4. Can you provide details about the market size?

The market size is estimated to be USD 21.77 Million as of 2022.

5. What are some drivers contributing to market growth?

Increasing Adoption of Lightweight-packaging Methods; Increased Eco-friendly Packaging and Recycled Plastic; Growing E-commerc Industry is Expected to Drive Growth.

6. What are the notable trends driving market growth?

Food Segment to Hold a Significant Share.

7. Are there any restraints impacting market growth?

High Price of Raw Material (Plastic Resin); Government Regulations and Environmental Concerns.

8. Can you provide examples of recent developments in the market?

January 2024: Coca-Cola India and Reliance Retail, the retail arm of India-based conglomerate Reliance Industries Limited (RIL), launched a new polyethylene terephthalate (PET) collection and recycling initiative. The initiative, called 'Bhool na Jana, Plastic Bottles Lautana,' will feature reverse vending machines and collection bins in Coca-Cola India's and Reliance Retail's stores in Mumbai and Delhi, with plans to roll it out nationwide. The initiative, part of the Indian government's larger 'Swachh Bharat' Mission, started with 36 stores, including those in Mumbai, Delhi's Smart Bazaar, and Sahara Bhandar.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "India Plastic Packaging Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the India Plastic Packaging Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the India Plastic Packaging Market?

To stay informed about further developments, trends, and reports in the India Plastic Packaging Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence