Key Insights

The dairy products packaging market, currently valued at approximately $XX million (assuming a logical estimation based on the provided CAGR and market trends), is experiencing robust growth, projected to maintain a Compound Annual Growth Rate (CAGR) of 4.61% from 2025 to 2033. This expansion is driven by several key factors. Firstly, the increasing demand for convenient and shelf-stable dairy products fuels the need for innovative packaging solutions. Consumers are increasingly seeking on-the-go options and extended product lifespans, leading to higher adoption of aseptic packaging and modified atmosphere packaging (MAP). Secondly, the growing focus on sustainability and eco-friendly packaging materials is driving the shift towards recyclable and biodegradable options, like paperboard and plant-based plastics, pushing manufacturers to adapt their supply chains. Finally, technological advancements in packaging materials and design are creating opportunities for enhanced product protection, improved functionality, and enhanced branding, further contributing to market growth.

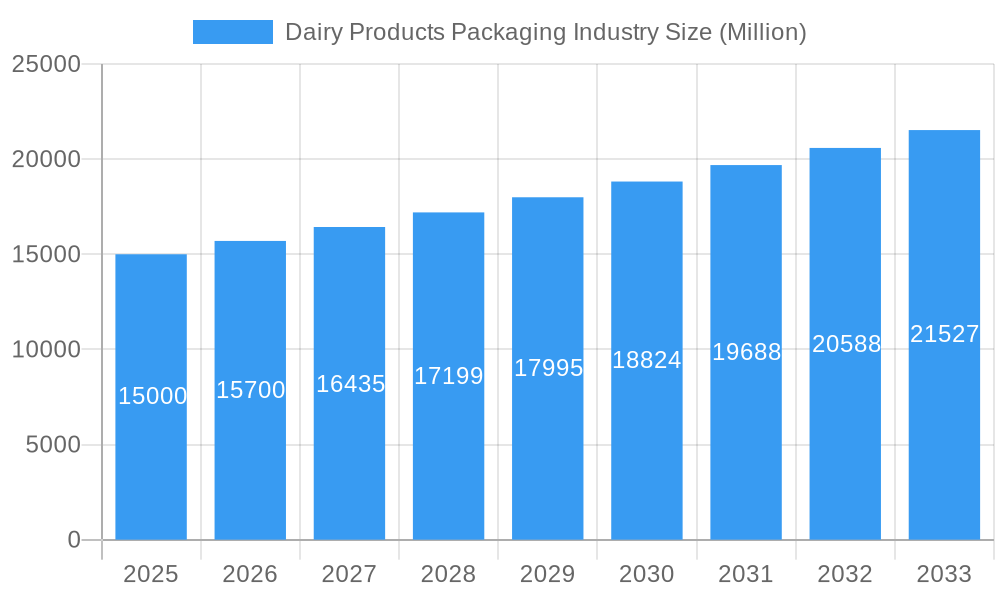

Dairy Products Packaging Industry Market Size (In Billion)

However, the market faces certain challenges. Fluctuations in raw material prices, particularly for plastics and resins, can impact profitability. Stringent regulatory requirements regarding food safety and environmental sustainability also impose constraints on manufacturers. Furthermore, the competitive landscape, with established players like Amcor PLC and Berry Global Group Inc. alongside regional competitors, necessitates continuous innovation and cost optimization strategies to maintain market share. Segment-wise, the plastic segment currently holds a significant market share due to its versatility and cost-effectiveness, but the increasing consumer preference for sustainable alternatives is driving growth in paperboard and other eco-friendly packaging options. The milk and cheese segments dominate product-wise, although frozen foods and yogurt are expected to witness significant growth due to changing consumer preferences and product innovations. Geographic regions show varied growth rates, with North America and Europe expected to maintain substantial market share driven by strong consumer demand and advanced packaging technologies, while Asia-Pacific is predicted to show significant growth potential due to increasing per capita income and changing lifestyles.

Dairy Products Packaging Industry Company Market Share

Dairy Products Packaging Industry: A Comprehensive Market Report (2019-2033)

This in-depth report provides a comprehensive analysis of the Dairy Products Packaging Industry, covering market dynamics, trends, leading players, and future outlook. With a study period spanning 2019-2033, a base year of 2025, and a forecast period of 2025-2033, this report is an indispensable resource for industry stakeholders seeking actionable insights and strategic guidance. The report covers a market valued at xx Million in 2025 and projects a value of xx Million by 2033, representing a significant CAGR of xx%.

Dairy Products Packaging Industry Market Dynamics & Concentration

The Dairy Products Packaging market is experiencing dynamic shifts driven by several factors. Market concentration is moderate, with key players like Amcor PLC, Berry Global Group Inc, and Tetra Pak (not explicitly listed but a significant player) holding substantial market share, estimated collectively at around xx%. However, the market exhibits significant fragmentation, especially in regional niche markets. Innovation is a crucial driver, fueled by the demand for sustainable and convenient packaging solutions. Stringent regulatory frameworks concerning material recyclability and food safety are shaping industry practices. The rise of eco-friendly alternatives, such as plant-based materials and biodegradable packaging, is challenging traditional materials like plastic. Consumer preferences for convenience, extended shelf life, and sustainable options are influencing packaging design and material selection. Furthermore, mergers and acquisitions (M&A) are reshaping the competitive landscape, with an estimated xx M&A deals recorded between 2019 and 2024.

- Market Concentration: Moderate, with top players holding xx% market share.

- Innovation Drivers: Sustainability, convenience, and food safety regulations.

- Regulatory Frameworks: Increasing focus on recyclability and reduced environmental impact.

- Product Substitutes: Growing adoption of biodegradable and plant-based materials.

- End-User Trends: Demand for convenient, sustainable, and tamper-proof packaging.

- M&A Activities: xx deals between 2019 and 2024, reshaping the competitive landscape.

Dairy Products Packaging Industry Industry Trends & Analysis

The Dairy Products Packaging market is characterized by robust growth, driven primarily by increasing dairy consumption globally and evolving consumer preferences. Technological advancements, such as improved barrier films, lightweight packaging, and active packaging solutions, are significantly enhancing product shelf life and quality. The demand for sustainable packaging is rapidly accelerating, prompting companies to invest in eco-friendly materials and recyclable designs. The shift towards e-commerce is influencing packaging needs, with a focus on tamper-proof and durable solutions for online deliveries. Intense competition among packaging manufacturers is leading to innovation, cost optimization, and strategic partnerships. The market is projected to experience a CAGR of xx% during the forecast period, with significant market penetration gains expected in emerging economies. Consumer preference for sustainable packaging is a key driver of innovation in the industry; approximately xx% of consumers are willing to pay a premium for sustainable dairy product packaging.

Leading Markets & Segments in Dairy Products Packaging Industry

The global dairy packaging market is experiencing dynamic growth, with the Asia-Pacific region currently leading the charge. This dominance is fueled by a confluence of factors, including rapid economic expansion, a continuously growing population, and increasing disposable incomes across a broad consumer base. Within this vibrant region, nations such as India and China are at the forefront, exhibiting some of the highest growth trajectories in dairy consumption and, consequently, packaging demand.

By Material:

- Plastic: Remains the undisputed leader, commanding the largest market share. Its widespread adoption is attributable to its exceptional versatility, cost-effectiveness for mass production, and crucial barrier properties that protect dairy products from spoilage and contamination. Innovations are continually enhancing its performance and sustainability profile.

- Paper and Paperboard: This segment is witnessing significant expansion, driven by a global imperative towards sustainability. Manufacturers are increasingly opting for these materials for their recyclability and reduced environmental footprint, making them attractive for a variety of dairy applications, especially for fresh milk and ice cream.

- Glass: While a niche segment, glass packaging is highly valued for its premium aesthetic, perceived purity, and excellent recyclability. It's often chosen for artisanal cheeses, specialty yogurts, and premium milk products where a sophisticated presentation is paramount.

- Metal: Occupying a smaller but important segment, metal packaging (primarily aluminum) is employed for specific applications that demand the highest level of barrier protection. This is particularly relevant for products with extended shelf-life requirements or those sensitive to light and oxygen.

By Product:

- Milk: Continues to be the largest segment by volume, propelled by its status as a daily staple in households worldwide. The demand for milk packaging is vast and consistent, driving innovation in both traditional and convenience formats.

- Yogurt and Cultured Products: This segment is experiencing robust growth, largely influenced by escalating health consciousness and the growing popularity of functional and probiotic-rich dairy options. Packaging for yogurt increasingly emphasizes convenience, portion control, and attractive in-store presentation.

- Cheese: A significant and diverse segment, cheese packaging requires specialized solutions tailored to the unique properties of different cheese types. Demand spans from flexible wraps for soft cheeses to rigid containers for aged varieties, with a growing emphasis on extended shelf life and leak-proof designs.

- Frozen Dairy Foods: This segment is on an upward trajectory, necessitating packaging materials with specific properties to maintain product quality and prevent freezer burn. Innovations focus on improving thermal insulation, moisture resistance, and ease of opening for frozen desserts and ice cream.

By Package Type:

- Bottles: Maintain their dominance, particularly for liquid dairy products like milk and yogurt. Modern bottle designs increasingly incorporate features like ergonomic grips, tamper-evident seals, and improved material efficiency.

- Cartons and Boxes: Widely adopted for their excellent protection, stackability, and branding opportunities, cartons and boxes remain a cornerstone for packaging milk, yogurt, and a variety of other dairy products. Innovations are focusing on multi-layer structures for enhanced barrier properties and sustainability.

- Pouches: Their popularity is on a significant rise due to their inherent convenience, reduced material usage, and lower transportation costs. Stand-up pouches and spouted pouches are gaining traction for a range of dairy products, offering ease of use and portion control.

- Bags and Wraps: These flexible packaging solutions are indispensable for products like cheese and butter, where adaptability and form-fitting protection are key. Advances in material science are enabling better seal integrity, clarity, and barrier performance in these formats.

Key drivers for the dominance of certain regions and segments include supportive economic policies, sophisticated logistics and distribution networks, and a deep-rooted and growing consumer demand for diverse dairy products. The industry is also being shaped by evolving consumer preferences for convenience, health, and sustainability.

Dairy Products Packaging Industry Product Developments

The dairy products packaging industry is currently experiencing a surge of innovation, with a primary focus on sustainability and enhanced convenience. Companies are aggressively investing in the research and development of recyclable, compostable, and lightweight packaging solutions. This includes the increased utilization of advanced materials such as post-consumer recycled plastics (PCR), innovative paperboard formulations, and emerging plant-based alternatives derived from sources like corn starch and sugarcane. Concurrently, significant technological advancements are being made in high-barrier films. These films are crucial for extending product shelf life, thereby minimizing food waste, and ensuring that dairy products reach consumers in their freshest, most optimal condition. The industry is also embracing the integration of smart packaging features. These include technologies for enhanced traceability through QR codes, RFID tags for inventory management, and even indicators that signal product freshness, all aimed at providing greater transparency and an improved consumer experience. Furthermore, there is a palpable growing demand for packaging that is specifically designed to cater to the unique requirements of a widening array of specialized dairy products, from artisanal cheeses to plant-based alternatives, and for diverse distribution channels, including the rapidly expanding online retail and direct-to-consumer (DTC) models.

Key Drivers of Dairy Products Packaging Growth

Several factors are driving growth in the Dairy Products Packaging industry. Technological advancements in materials science and packaging technology offer improved barrier properties, lighter weight, and enhanced recyclability. Economic growth in developing economies is increasing dairy consumption and demand for packaging. Stringent food safety and environmental regulations are pushing manufacturers towards sustainable and compliant packaging solutions. The increasing focus on convenience and the rise of e-commerce demand better packaging for delivery and preservation.

Challenges in the Dairy Products Packaging Industry Market

The industry faces challenges such as fluctuating raw material prices, which impact profitability. Meeting stringent environmental regulations and consumer demands for sustainable packaging requires significant investment in R&D and new technologies. Intense competition among established players and new entrants creates price pressures. Supply chain disruptions and logistical complexities, especially in the wake of global events, can impact timely delivery and production. The estimated cost of compliance with new sustainability regulations is projected at approximately xx Million annually.

Emerging Opportunities in Dairy Products Packaging Industry

The unwavering global shift towards environmental consciousness presents a fertile ground for significant opportunities within the dairy products packaging industry. The increasing consumer and regulatory demand for eco-friendly and innovative packaging solutions is creating a substantial market for biodegradable, compostable, and highly recyclable materials. Strategic collaborations and partnerships between packaging manufacturers and dairy producers are becoming increasingly vital. These alliances enable the co-creation of tailored, cost-effective, and performance-optimized packaging options that meet specific product needs and sustainability goals. Expansion into new and emerging markets, particularly in developing economies with rapidly growing middle classes and increasing dairy consumption, offers substantial untapped growth potential. Moreover, continuous advancements in active and intelligent packaging technologies are poised to be a major market growth driver. These sophisticated packaging solutions are capable of extending product shelf life through controlled release mechanisms or by actively inhibiting spoilage, and can also enhance product safety and consumer engagement through features like tamper-evidence and freshness indicators.

Leading Players in the Dairy Products Packaging Industry Sector

Key Milestones in Dairy Products Packaging Industry Industry

- May 2021: Stora Enso partnered with Pulpex to produce fiber-based bottles, offering a sustainable alternative to plastic and glass.

- August 2021: Huhtamaki acquired Elif Holding A.S., expanding its presence in sustainable flexible packaging markets in Africa, the Middle East, and Europe.

- September 2021: Greiner Packaging announced its chemically recycled polypropylene would be used by Emmi CAFFÈ LATTE, showcasing the adoption of sustainable materials in prominent brands.

Strategic Outlook for Dairy Products Packaging Industry Market

The Dairy Products Packaging market is poised for substantial growth, driven by continued demand for sustainable and innovative packaging solutions. Strategic partnerships, technological advancements, and expansion into new markets will be crucial for success. Companies that prioritize sustainability, invest in R&D, and adapt to evolving consumer preferences are expected to capture significant market share and drive future growth. The market's future is bright, with projections indicating continued robust growth and the emergence of innovative packaging materials and technologies.

Dairy Products Packaging Industry Segmentation

-

1. Material

- 1.1. Plastic

- 1.2. Paper and Paperboard

- 1.3. Glass

- 1.4. Metal

-

2. Product

- 2.1. Milk

- 2.2. Cheese

- 2.3. Frozen Foods

- 2.4. Yogurt

- 2.5. Cultured Products

-

3. Package Type

- 3.1. Bottles

- 3.2. Pouches

- 3.3. Cartons and Boxes

- 3.4. Bags and Wraps

- 3.5. Other Package Types

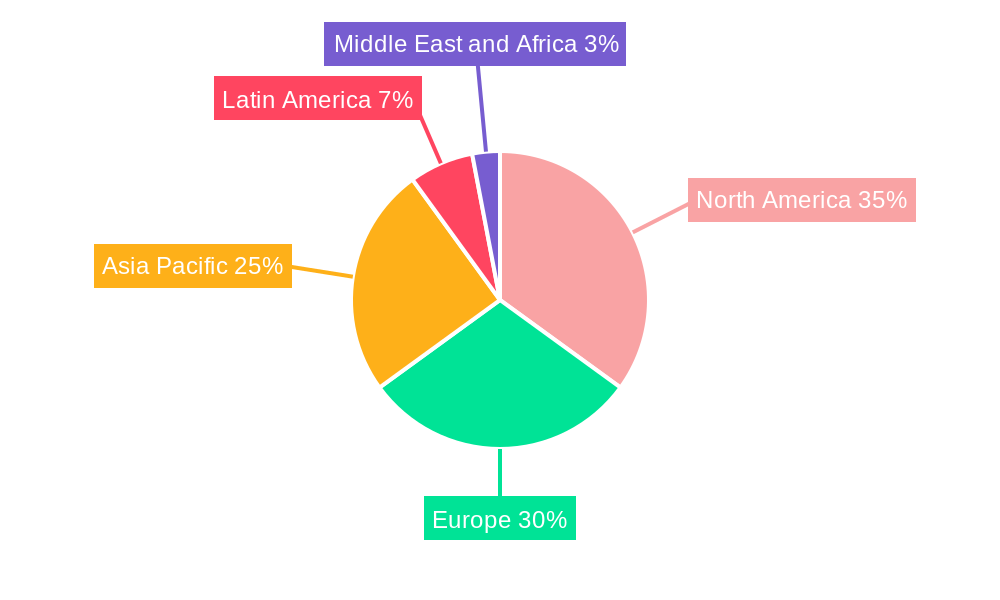

Dairy Products Packaging Industry Segmentation By Geography

- 1. North America

- 2. Europe

- 3. Asia Pacific

- 4. Latin America

- 5. Middle East and Africa

Dairy Products Packaging Industry Regional Market Share

Geographic Coverage of Dairy Products Packaging Industry

Dairy Products Packaging Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 4.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Consumer Preference Towards Protein-based Products; Increasing Adoption of Packages Incorporating Small Portion Size

- 3.3. Market Restrains

- 3.3.1. ; Greenhouse Gas Emission due to Dairy Activities Leading to Legislative Issues

- 3.4. Market Trends

- 3.4.1. Milk Occupies the Largest Market Share

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Dairy Products Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Material

- 5.1.1. Plastic

- 5.1.2. Paper and Paperboard

- 5.1.3. Glass

- 5.1.4. Metal

- 5.2. Market Analysis, Insights and Forecast - by Product

- 5.2.1. Milk

- 5.2.2. Cheese

- 5.2.3. Frozen Foods

- 5.2.4. Yogurt

- 5.2.5. Cultured Products

- 5.3. Market Analysis, Insights and Forecast - by Package Type

- 5.3.1. Bottles

- 5.3.2. Pouches

- 5.3.3. Cartons and Boxes

- 5.3.4. Bags and Wraps

- 5.3.5. Other Package Types

- 5.4. Market Analysis, Insights and Forecast - by Region

- 5.4.1. North America

- 5.4.2. Europe

- 5.4.3. Asia Pacific

- 5.4.4. Latin America

- 5.4.5. Middle East and Africa

- 5.1. Market Analysis, Insights and Forecast - by Material

- 6. North America Dairy Products Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Material

- 6.1.1. Plastic

- 6.1.2. Paper and Paperboard

- 6.1.3. Glass

- 6.1.4. Metal

- 6.2. Market Analysis, Insights and Forecast - by Product

- 6.2.1. Milk

- 6.2.2. Cheese

- 6.2.3. Frozen Foods

- 6.2.4. Yogurt

- 6.2.5. Cultured Products

- 6.3. Market Analysis, Insights and Forecast - by Package Type

- 6.3.1. Bottles

- 6.3.2. Pouches

- 6.3.3. Cartons and Boxes

- 6.3.4. Bags and Wraps

- 6.3.5. Other Package Types

- 6.1. Market Analysis, Insights and Forecast - by Material

- 7. Europe Dairy Products Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Material

- 7.1.1. Plastic

- 7.1.2. Paper and Paperboard

- 7.1.3. Glass

- 7.1.4. Metal

- 7.2. Market Analysis, Insights and Forecast - by Product

- 7.2.1. Milk

- 7.2.2. Cheese

- 7.2.3. Frozen Foods

- 7.2.4. Yogurt

- 7.2.5. Cultured Products

- 7.3. Market Analysis, Insights and Forecast - by Package Type

- 7.3.1. Bottles

- 7.3.2. Pouches

- 7.3.3. Cartons and Boxes

- 7.3.4. Bags and Wraps

- 7.3.5. Other Package Types

- 7.1. Market Analysis, Insights and Forecast - by Material

- 8. Asia Pacific Dairy Products Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Material

- 8.1.1. Plastic

- 8.1.2. Paper and Paperboard

- 8.1.3. Glass

- 8.1.4. Metal

- 8.2. Market Analysis, Insights and Forecast - by Product

- 8.2.1. Milk

- 8.2.2. Cheese

- 8.2.3. Frozen Foods

- 8.2.4. Yogurt

- 8.2.5. Cultured Products

- 8.3. Market Analysis, Insights and Forecast - by Package Type

- 8.3.1. Bottles

- 8.3.2. Pouches

- 8.3.3. Cartons and Boxes

- 8.3.4. Bags and Wraps

- 8.3.5. Other Package Types

- 8.1. Market Analysis, Insights and Forecast - by Material

- 9. Latin America Dairy Products Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Material

- 9.1.1. Plastic

- 9.1.2. Paper and Paperboard

- 9.1.3. Glass

- 9.1.4. Metal

- 9.2. Market Analysis, Insights and Forecast - by Product

- 9.2.1. Milk

- 9.2.2. Cheese

- 9.2.3. Frozen Foods

- 9.2.4. Yogurt

- 9.2.5. Cultured Products

- 9.3. Market Analysis, Insights and Forecast - by Package Type

- 9.3.1. Bottles

- 9.3.2. Pouches

- 9.3.3. Cartons and Boxes

- 9.3.4. Bags and Wraps

- 9.3.5. Other Package Types

- 9.1. Market Analysis, Insights and Forecast - by Material

- 10. Middle East and Africa Dairy Products Packaging Industry Analysis, Insights and Forecast, 2020-2032

- 10.1. Market Analysis, Insights and Forecast - by Material

- 10.1.1. Plastic

- 10.1.2. Paper and Paperboard

- 10.1.3. Glass

- 10.1.4. Metal

- 10.2. Market Analysis, Insights and Forecast - by Product

- 10.2.1. Milk

- 10.2.2. Cheese

- 10.2.3. Frozen Foods

- 10.2.4. Yogurt

- 10.2.5. Cultured Products

- 10.3. Market Analysis, Insights and Forecast - by Package Type

- 10.3.1. Bottles

- 10.3.2. Pouches

- 10.3.3. Cartons and Boxes

- 10.3.4. Bags and Wraps

- 10.3.5. Other Package Types

- 10.1. Market Analysis, Insights and Forecast - by Material

- 11. Competitive Analysis

- 11.1. Global Market Share Analysis 2025

- 11.2. Company Profiles

- 11.2.1 Consolidated Container Company LLC

- 11.2.1.1. Overview

- 11.2.1.2. Products

- 11.2.1.3. SWOT Analysis

- 11.2.1.4. Recent Developments

- 11.2.1.5. Financials (Based on Availability)

- 11.2.2 Stora Enso Oyj

- 11.2.2.1. Overview

- 11.2.2.2. Products

- 11.2.2.3. SWOT Analysis

- 11.2.2.4. Recent Developments

- 11.2.2.5. Financials (Based on Availability)

- 11.2.3 Ball Corporation

- 11.2.3.1. Overview

- 11.2.3.2. Products

- 11.2.3.3. SWOT Analysis

- 11.2.3.4. Recent Developments

- 11.2.3.5. Financials (Based on Availability)

- 11.2.4 Greiner Packaging international Gmb

- 11.2.4.1. Overview

- 11.2.4.2. Products

- 11.2.4.3. SWOT Analysis

- 11.2.4.4. Recent Developments

- 11.2.4.5. Financials (Based on Availability)

- 11.2.5 Berry Global Group Inc

- 11.2.5.1. Overview

- 11.2.5.2. Products

- 11.2.5.3. SWOT Analysis

- 11.2.5.4. Recent Developments

- 11.2.5.5. Financials (Based on Availability)

- 11.2.6 Huhtamaki Group

- 11.2.6.1. Overview

- 11.2.6.2. Products

- 11.2.6.3. SWOT Analysis

- 11.2.6.4. Recent Developments

- 11.2.6.5. Financials (Based on Availability)

- 11.2.7 Winpak Ltd

- 11.2.7.1. Overview

- 11.2.7.2. Products

- 11.2.7.3. SWOT Analysis

- 11.2.7.4. Recent Developments

- 11.2.7.5. Financials (Based on Availability)

- 11.2.8 Amcor PLC

- 11.2.8.1. Overview

- 11.2.8.2. Products

- 11.2.8.3. SWOT Analysis

- 11.2.8.4. Recent Developments

- 11.2.8.5. Financials (Based on Availability)

- 11.2.9 International Paper Company

- 11.2.9.1. Overview

- 11.2.9.2. Products

- 11.2.9.3. SWOT Analysis

- 11.2.9.4. Recent Developments

- 11.2.9.5. Financials (Based on Availability)

- 11.2.10 Sealed Air Corporation

- 11.2.10.1. Overview

- 11.2.10.2. Products

- 11.2.10.3. SWOT Analysis

- 11.2.10.4. Recent Developments

- 11.2.10.5. Financials (Based on Availability)

- 11.2.11 Saudi Basic Industries Corporation

- 11.2.11.1. Overview

- 11.2.11.2. Products

- 11.2.11.3. SWOT Analysis

- 11.2.11.4. Recent Developments

- 11.2.11.5. Financials (Based on Availability)

- 11.2.1 Consolidated Container Company LLC

List of Figures

- Figure 1: Global Dairy Products Packaging Industry Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: North America Dairy Products Packaging Industry Revenue (undefined), by Material 2025 & 2033

- Figure 3: North America Dairy Products Packaging Industry Revenue Share (%), by Material 2025 & 2033

- Figure 4: North America Dairy Products Packaging Industry Revenue (undefined), by Product 2025 & 2033

- Figure 5: North America Dairy Products Packaging Industry Revenue Share (%), by Product 2025 & 2033

- Figure 6: North America Dairy Products Packaging Industry Revenue (undefined), by Package Type 2025 & 2033

- Figure 7: North America Dairy Products Packaging Industry Revenue Share (%), by Package Type 2025 & 2033

- Figure 8: North America Dairy Products Packaging Industry Revenue (undefined), by Country 2025 & 2033

- Figure 9: North America Dairy Products Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 10: Europe Dairy Products Packaging Industry Revenue (undefined), by Material 2025 & 2033

- Figure 11: Europe Dairy Products Packaging Industry Revenue Share (%), by Material 2025 & 2033

- Figure 12: Europe Dairy Products Packaging Industry Revenue (undefined), by Product 2025 & 2033

- Figure 13: Europe Dairy Products Packaging Industry Revenue Share (%), by Product 2025 & 2033

- Figure 14: Europe Dairy Products Packaging Industry Revenue (undefined), by Package Type 2025 & 2033

- Figure 15: Europe Dairy Products Packaging Industry Revenue Share (%), by Package Type 2025 & 2033

- Figure 16: Europe Dairy Products Packaging Industry Revenue (undefined), by Country 2025 & 2033

- Figure 17: Europe Dairy Products Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 18: Asia Pacific Dairy Products Packaging Industry Revenue (undefined), by Material 2025 & 2033

- Figure 19: Asia Pacific Dairy Products Packaging Industry Revenue Share (%), by Material 2025 & 2033

- Figure 20: Asia Pacific Dairy Products Packaging Industry Revenue (undefined), by Product 2025 & 2033

- Figure 21: Asia Pacific Dairy Products Packaging Industry Revenue Share (%), by Product 2025 & 2033

- Figure 22: Asia Pacific Dairy Products Packaging Industry Revenue (undefined), by Package Type 2025 & 2033

- Figure 23: Asia Pacific Dairy Products Packaging Industry Revenue Share (%), by Package Type 2025 & 2033

- Figure 24: Asia Pacific Dairy Products Packaging Industry Revenue (undefined), by Country 2025 & 2033

- Figure 25: Asia Pacific Dairy Products Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 26: Latin America Dairy Products Packaging Industry Revenue (undefined), by Material 2025 & 2033

- Figure 27: Latin America Dairy Products Packaging Industry Revenue Share (%), by Material 2025 & 2033

- Figure 28: Latin America Dairy Products Packaging Industry Revenue (undefined), by Product 2025 & 2033

- Figure 29: Latin America Dairy Products Packaging Industry Revenue Share (%), by Product 2025 & 2033

- Figure 30: Latin America Dairy Products Packaging Industry Revenue (undefined), by Package Type 2025 & 2033

- Figure 31: Latin America Dairy Products Packaging Industry Revenue Share (%), by Package Type 2025 & 2033

- Figure 32: Latin America Dairy Products Packaging Industry Revenue (undefined), by Country 2025 & 2033

- Figure 33: Latin America Dairy Products Packaging Industry Revenue Share (%), by Country 2025 & 2033

- Figure 34: Middle East and Africa Dairy Products Packaging Industry Revenue (undefined), by Material 2025 & 2033

- Figure 35: Middle East and Africa Dairy Products Packaging Industry Revenue Share (%), by Material 2025 & 2033

- Figure 36: Middle East and Africa Dairy Products Packaging Industry Revenue (undefined), by Product 2025 & 2033

- Figure 37: Middle East and Africa Dairy Products Packaging Industry Revenue Share (%), by Product 2025 & 2033

- Figure 38: Middle East and Africa Dairy Products Packaging Industry Revenue (undefined), by Package Type 2025 & 2033

- Figure 39: Middle East and Africa Dairy Products Packaging Industry Revenue Share (%), by Package Type 2025 & 2033

- Figure 40: Middle East and Africa Dairy Products Packaging Industry Revenue (undefined), by Country 2025 & 2033

- Figure 41: Middle East and Africa Dairy Products Packaging Industry Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Dairy Products Packaging Industry Revenue undefined Forecast, by Material 2020 & 2033

- Table 2: Global Dairy Products Packaging Industry Revenue undefined Forecast, by Product 2020 & 2033

- Table 3: Global Dairy Products Packaging Industry Revenue undefined Forecast, by Package Type 2020 & 2033

- Table 4: Global Dairy Products Packaging Industry Revenue undefined Forecast, by Region 2020 & 2033

- Table 5: Global Dairy Products Packaging Industry Revenue undefined Forecast, by Material 2020 & 2033

- Table 6: Global Dairy Products Packaging Industry Revenue undefined Forecast, by Product 2020 & 2033

- Table 7: Global Dairy Products Packaging Industry Revenue undefined Forecast, by Package Type 2020 & 2033

- Table 8: Global Dairy Products Packaging Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 9: Global Dairy Products Packaging Industry Revenue undefined Forecast, by Material 2020 & 2033

- Table 10: Global Dairy Products Packaging Industry Revenue undefined Forecast, by Product 2020 & 2033

- Table 11: Global Dairy Products Packaging Industry Revenue undefined Forecast, by Package Type 2020 & 2033

- Table 12: Global Dairy Products Packaging Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 13: Global Dairy Products Packaging Industry Revenue undefined Forecast, by Material 2020 & 2033

- Table 14: Global Dairy Products Packaging Industry Revenue undefined Forecast, by Product 2020 & 2033

- Table 15: Global Dairy Products Packaging Industry Revenue undefined Forecast, by Package Type 2020 & 2033

- Table 16: Global Dairy Products Packaging Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 17: Global Dairy Products Packaging Industry Revenue undefined Forecast, by Material 2020 & 2033

- Table 18: Global Dairy Products Packaging Industry Revenue undefined Forecast, by Product 2020 & 2033

- Table 19: Global Dairy Products Packaging Industry Revenue undefined Forecast, by Package Type 2020 & 2033

- Table 20: Global Dairy Products Packaging Industry Revenue undefined Forecast, by Country 2020 & 2033

- Table 21: Global Dairy Products Packaging Industry Revenue undefined Forecast, by Material 2020 & 2033

- Table 22: Global Dairy Products Packaging Industry Revenue undefined Forecast, by Product 2020 & 2033

- Table 23: Global Dairy Products Packaging Industry Revenue undefined Forecast, by Package Type 2020 & 2033

- Table 24: Global Dairy Products Packaging Industry Revenue undefined Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Dairy Products Packaging Industry?

The projected CAGR is approximately 4.3%.

2. Which companies are prominent players in the Dairy Products Packaging Industry?

Key companies in the market include Consolidated Container Company LLC, Stora Enso Oyj, Ball Corporation, Greiner Packaging international Gmb, Berry Global Group Inc, Huhtamaki Group, Winpak Ltd, Amcor PLC, International Paper Company, Sealed Air Corporation, Saudi Basic Industries Corporation.

3. What are the main segments of the Dairy Products Packaging Industry?

The market segments include Material, Product, Package Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

Increasing Consumer Preference Towards Protein-based Products; Increasing Adoption of Packages Incorporating Small Portion Size.

6. What are the notable trends driving market growth?

Milk Occupies the Largest Market Share.

7. Are there any restraints impacting market growth?

; Greenhouse Gas Emission due to Dairy Activities Leading to Legislative Issues.

8. Can you provide examples of recent developments in the market?

September 2021 - Greiner Packaging announced Emmi CAFFÈ LATTE, Europe's leading ready-to-drink iced coffee brand, will start incorporating its new chemically recycled polypropylene into packaging. Greiner Packaging makes these cups from chemically recycled material that comes from Borealis.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Dairy Products Packaging Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Dairy Products Packaging Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Dairy Products Packaging Industry?

To stay informed about further developments, trends, and reports in the Dairy Products Packaging Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence