Key Insights

The Australian dairy alternatives market, valued at 601.39 million in 2025, is projected to experience substantial growth at a Compound Annual Growth Rate (CAGR) of 12.1% from 2025 to 2033. This expansion is propelled by increasing consumer awareness of plant-based diets' health benefits, including reduced saturated fat and cholesterol. The rising popularity of vegan and vegetarian lifestyles, alongside growing concerns for animal welfare and environmental sustainability, further fuels demand. Continuous product innovation, enhancing taste, texture, and nutritional profiles, also drives consumer acceptance and market penetration. The off-trade distribution channel, encompassing supermarkets and retail stores, leads the market due to the accessibility and convenience of dairy alternatives. Key players such as Nestlé SA, Danone SA, and Califia Farms are capitalizing on their brand recognition and distribution networks, while specialized companies focus on niche segments. The market is segmented into non-dairy milk, ice cream, cheese, and butter, each exhibiting distinct growth patterns influenced by consumer preferences and product innovations. Emerging segments like warehouse clubs and gas stations present growing opportunities.

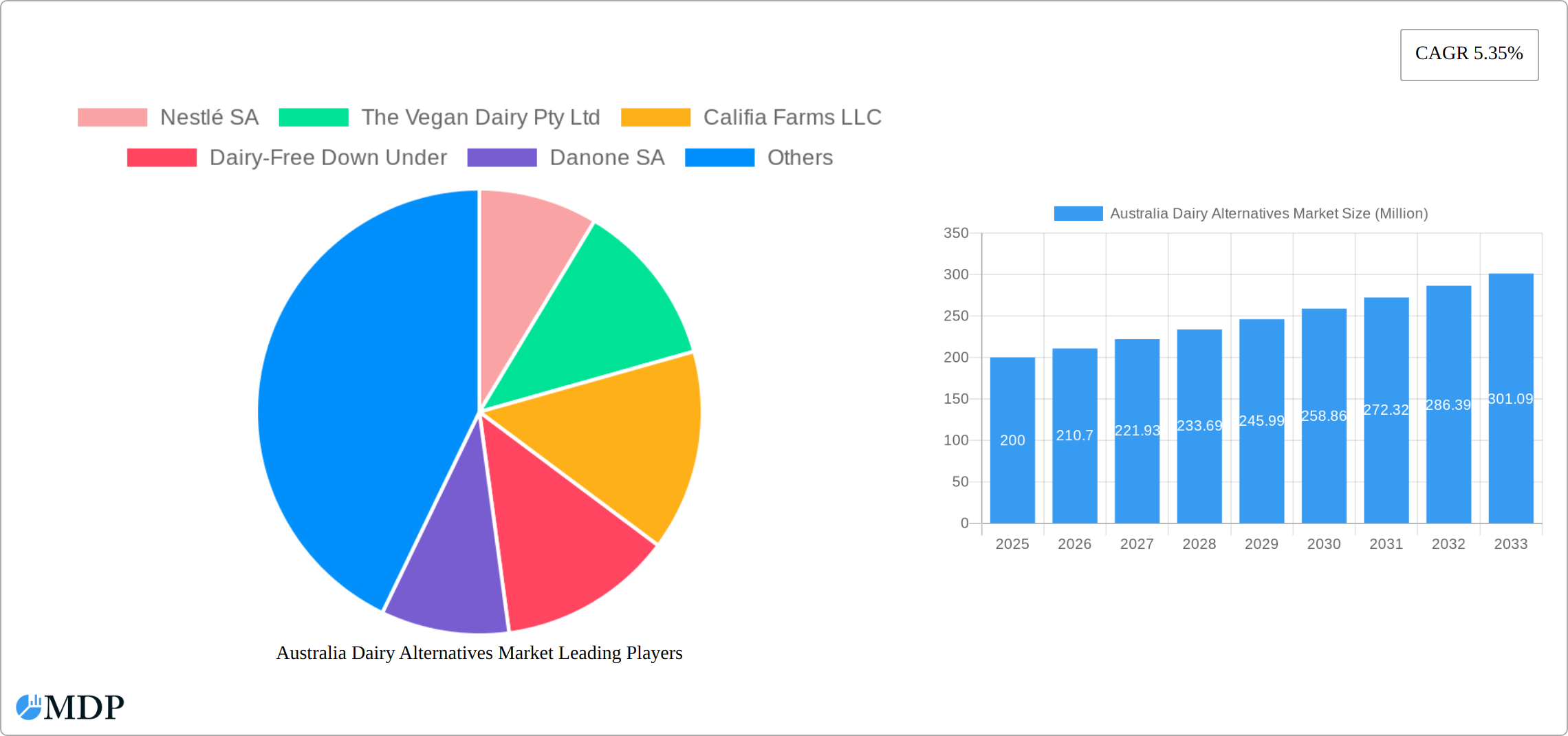

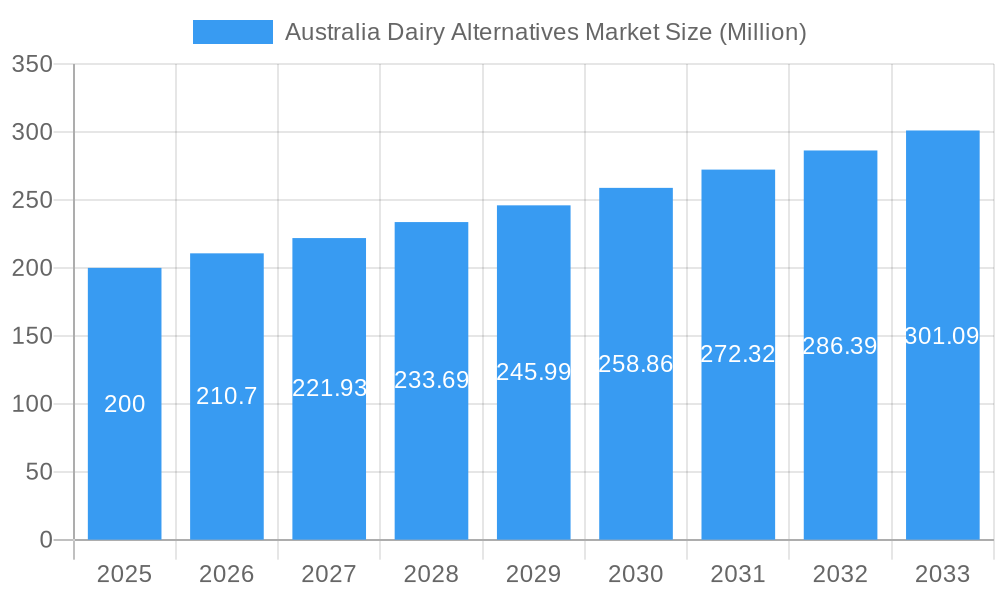

Australia Dairy Alternatives Market Market Size (In Million)

Market growth faces challenges including raw material price volatility and competition from established dairy producers. Consumer perceptions regarding the taste and texture of some alternatives also remain a barrier. Overcoming these challenges necessitates ongoing product innovation, effective marketing emphasizing taste and health benefits, and robust supply chain management for consistent availability and affordability. Future growth hinges on addressing these challenges while leveraging trends such as functional dairy alternatives fortified with vitamins and minerals. The Australian market offers significant opportunities for both established and emerging dairy alternative players.

Australia Dairy Alternatives Market Company Market Share

Australia Dairy Alternatives Market Report: 2019-2033

This comprehensive report provides an in-depth analysis of the burgeoning Australia Dairy Alternatives Market, offering invaluable insights for industry stakeholders, investors, and businesses seeking to capitalize on this rapidly expanding sector. Covering the period from 2019 to 2033, with a focus on 2025, this report meticulously examines market dynamics, leading players, emerging trends, and future growth potential. The report leverages detailed data analysis and expert insights to present a clear, actionable roadmap for navigating the complexities of this dynamic market. The market is expected to reach xx Million by 2033.

Australia Dairy Alternatives Market Market Dynamics & Concentration

The Australian dairy alternatives market is experiencing robust and dynamic growth, propelled by a significant surge in consumer demand for plant-based products. This upward trend is further amplified by heightened health consciousness, with consumers actively seeking healthier alternatives, and a growing awareness of the environmental sustainability benefits associated with plant-based diets. The market's concentration is characterized as moderately competitive. A few key players command a substantial portion of the market share, while a vibrant ecosystem of smaller, innovative companies also contributes significantly to the overall market volume and diversity.

Innovation is a critical engine driving this market forward. Continuous product diversification is evident in the expanding range of ingredients (such as oat, almond, soy, coconut, and newer sources like fava bean and pea protein), an array of appealing flavors, and the development of functional benefits tailored to specific consumer needs. Regulatory frameworks, particularly concerning labeling transparency and product standards, play an influential role in shaping market operations and ensuring consumer trust. The accelerating adoption of veganism and vegetarianism, alongside the persistent challenges of lactose intolerance and dairy allergies, are fundamental factors fueling sustained demand for dairy alternatives.

While traditional dairy products remain a substitute, the dairy alternatives sector is steadily expanding its market share by offering unique value propositions centered on health, ethics, and environmental impact. The market is also witnessing considerable Mergers and Acquisitions (M&A) activity, reflecting ongoing consolidation efforts and strategic expansion by key players. For instance, the number of M&A deals recorded between 2020 and 2024 totaled approximately [Insert Number Here]. The market share held by the top 5 players in 2024 was estimated at approximately [Insert Percentage Here]%.

- Key Market Drivers: Escalating consumer preference for plant-based diets, growing health concerns related to traditional dairy products, and increasing environmental consciousness regarding agricultural practices.

- Competitive Landscape: A moderately concentrated market featuring a blend of well-established multinational corporations and agile, specialized brands actively competing for consumer attention.

- Regulatory Landscape: Stringent government regulations and food safety standards critically influence product formulation, ingredient sourcing, and consumer-facing labeling.

- Innovation: Persistent and ambitious product development, including the introduction of novel ingredients and advanced processing techniques to enhance taste, texture, nutritional profiles, and overall functionality.

- M&A Activity: Notable M&A activity underscores ongoing industry consolidation, strategic partnerships, and ambitious expansion strategies by market leaders.

Australia Dairy Alternatives Market Industry Trends & Analysis

The Australian dairy alternatives market is exhibiting a strong, upward trajectory, underpinned by a dynamic interplay of evolving consumer behaviors and industry advancements. A significant shift in consumer preferences towards plant-based options is a dominant trend, driven by a confluence of health-conscious decisions and ethical considerations. Technological innovations are at the forefront, enabling the development of increasingly sophisticated products that closely mimic the desirable taste and texture of traditional dairy, thereby broadening their appeal to a wider consumer base.

The market's growth is further amplified by enhanced retail availability, the expansion of diverse distribution channels, and highly targeted marketing campaigns executed by key industry players. The Compound Annual Growth Rate (CAGR) for the market during the historical period (2019-2024) was approximately [Insert Percentage Here]%, with market penetration reaching an estimated [Insert Percentage Here]% in 2024. This impressive growth is projected to continue robustly during the forecast period (2025-2033), with an anticipated CAGR of [Insert Percentage Here]%. The competitive dynamics are characterized by a lively interplay between established market leaders and emerging new entrants, all vying for market share, which in turn fuels continuous innovation and price competitiveness.

Leading Markets & Segments in Australia Dairy Alternatives Market

The Australian dairy alternatives market showcases strong growth across various segments and distribution channels. The Off-Trade channel (supermarkets, grocery stores, etc.) currently dominates, accounting for approximately xx% of the market share in 2024. Non-Dairy Milk is the leading product category, with a market share of approximately xx% in 2024. The key drivers for this dominance include:

Non-Dairy Milk: High consumer adoption, wide availability, and continuous product innovation driving growth.

Off-Trade Channel: Ease of access and established distribution networks in supermarkets and grocery stores.

Regional Variations: Market growth is consistently strong across most regions in Australia, reflecting broad national consumer trends.

Key Drivers for Non-Dairy Milk Segment Dominance:

- Widespread availability in retail outlets.

- Versatile applications in various culinary preparations.

- Growing consumer preference for plant-based alternatives.

- Health-conscious consumers seeking lactose-free options.

Key Drivers for Off-Trade Channel Dominance:

- Extensive retail network providing easy access to consumers.

- Well-established supply chain infrastructure facilitating smooth distribution.

- Strategic partnerships between manufacturers and retailers bolster market presence.

Australia Dairy Alternatives Market Product Developments

Recent years have witnessed remarkable product innovation within the Australian dairy alternatives market. Companies are constantly developing new products with improved taste, texture, and nutritional profiles to better satisfy consumer preferences. This includes using novel ingredients, exploring various plant-based sources (like oats, almonds, soy), and focusing on creating functional products with added health benefits. The focus on improving the "dairy-like" experience through technological advancements is leading to a significant expansion of product applications across diverse food and beverage categories. This ongoing innovation allows companies to differentiate themselves and enhance their competitive positions in a growing market.

Key Drivers of Australia Dairy Alternatives Market Growth

The sustained growth of the Australian dairy alternatives market is propelled by a powerful combination of converging factors. The accelerating adoption of vegan and vegetarian lifestyles stands as a primary driver, deeply intertwined with an increasing awareness and concern regarding the environmental footprint of traditional dairy farming practices. Health considerations, particularly the prevalence of lactose intolerance and concerns about cholesterol levels, are compelling a significant segment of consumers to transition towards plant-based dairy alternatives.

Furthermore, supportive government policies that champion sustainable agriculture and encourage the production and consumption of plant-based foods play a vital role in fostering market expansion. Technological advancements are also critical, leading to demonstrably improved product quality, enhanced taste profiles, and superior textures, all of which significantly contribute to higher consumer acceptance and market penetration.

Challenges in the Australia Dairy Alternatives Market Market

Despite the market's robust growth, several challenges remain. Fluctuations in raw material prices can affect production costs, impacting profitability. Ensuring a consistent and reliable supply chain is crucial, particularly for niche ingredients. Intense competition among numerous players necessitates ongoing innovation and effective marketing strategies to retain and attract customers. Regulatory hurdles and evolving food safety standards require continuous adaptation and compliance. The premium pricing of some dairy alternatives compared to traditional dairy products presents a barrier for price-sensitive consumers.

Emerging Opportunities in Australia Dairy Alternatives Market

The Australian dairy alternatives market is ripe with exciting long-term growth opportunities, offering fertile ground for innovation and expansion. Technological breakthroughs in developing more sustainable, efficient, and cost-effective production processes are poised to drive industry advancements and potentially lower consumer prices. Strategic collaborations and partnerships between dairy alternative manufacturers and the food service sector, including cafes, restaurants, and catering businesses, represent a significant avenue for expanding market reach and introducing products to new consumer touchpoints.

Moreover, the continuously growing consumer awareness and escalating demand for healthier, ethically produced, and environmentally friendly food options create a highly conducive environment for further market expansion. This trend is expected to foster the emergence of new, specialized product lines catering to niche dietary needs and preferences, further diversifying and strengthening the market.

Leading Players in the Australia Dairy Alternatives Market Sector

- Nestlé SA

- The Vegan Dairy Pty Ltd

- Califia Farms LLC

- Dairy-Free Down Under

- Danone SA

- PureHarvest

- Blue Diamond Growers

- Vitasoy International Holdings Lt

- Namyang Dairy Products Co Ltd

- Spiral Foods

- Sanitarium Health and Wellbeing Company

Key Milestones in Australia Dairy Alternatives Market Industry

- August 2022: Califia Farms launched its Oat Barista Blend, strengthening its presence in the coffee market.

- August 2022: Sanitarium launched a new master brand campaign for its 'So Good' plant-based milk.

- October 2022: Vitasoy International Holdings Ltd planned to expand its dairy alternative business through an acquisition.

Strategic Outlook for Australia Dairy Alternatives Market Market

The future of the Australian dairy alternatives market looks promising. Continued innovation in product development, focusing on enhanced taste, texture, and nutritional value, will be crucial for sustained growth. Strategic partnerships and collaborations, particularly with food service providers and retailers, will be key to expanding market reach and driving adoption. Companies that effectively leverage technological advancements to improve efficiency, sustainability, and product quality are poised to capture a larger share of this rapidly expanding market. Furthermore, addressing consumer concerns about pricing and ensuring supply chain stability will be critical factors for success in the years to come.

Australia Dairy Alternatives Market Segmentation

-

1. Category

- 1.1. Non-Dairy Butter

- 1.2. Non-Dairy Cheese

- 1.3. Non-Dairy Ice Cream

-

1.4. Non-Dairy Milk

-

1.4.1. By Product Type

- 1.4.1.1. Almond Milk

- 1.4.1.2. Cashew Milk

- 1.4.1.3. Coconut Milk

- 1.4.1.4. Hazelnut Milk

- 1.4.1.5. Oat Milk

- 1.4.1.6. Soy Milk

-

1.4.1. By Product Type

- 1.5. Non-Dairy Yogurt

-

2. Distribution Channel

-

2.1. Off-Trade

- 2.1.1. Convenience Stores

- 2.1.2. Online Retail

- 2.1.3. Specialist Retailers

- 2.1.4. Supermarkets and Hypermarkets

- 2.1.5. Others (Warehouse clubs, gas stations, etc.)

- 2.2. On-Trade

-

2.1. Off-Trade

Australia Dairy Alternatives Market Segmentation By Geography

- 1. Australia

Australia Dairy Alternatives Market Regional Market Share

Geographic Coverage of Australia Dairy Alternatives Market

Australia Dairy Alternatives Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 12.1% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Growing Inclination Towards Vegan/Plant-based Protein Sources; Increasing Demand for Functional Protein Beverages

- 3.3. Market Restrains

- 3.3.1. Competition from Substitute Products

- 3.4. Market Trends

- 3.4.1. OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Australia Dairy Alternatives Market Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Category

- 5.1.1. Non-Dairy Butter

- 5.1.2. Non-Dairy Cheese

- 5.1.3. Non-Dairy Ice Cream

- 5.1.4. Non-Dairy Milk

- 5.1.4.1. By Product Type

- 5.1.4.1.1. Almond Milk

- 5.1.4.1.2. Cashew Milk

- 5.1.4.1.3. Coconut Milk

- 5.1.4.1.4. Hazelnut Milk

- 5.1.4.1.5. Oat Milk

- 5.1.4.1.6. Soy Milk

- 5.1.4.1. By Product Type

- 5.1.5. Non-Dairy Yogurt

- 5.2. Market Analysis, Insights and Forecast - by Distribution Channel

- 5.2.1. Off-Trade

- 5.2.1.1. Convenience Stores

- 5.2.1.2. Online Retail

- 5.2.1.3. Specialist Retailers

- 5.2.1.4. Supermarkets and Hypermarkets

- 5.2.1.5. Others (Warehouse clubs, gas stations, etc.)

- 5.2.2. On-Trade

- 5.2.1. Off-Trade

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Australia

- 5.1. Market Analysis, Insights and Forecast - by Category

- 6. Competitive Analysis

- 6.1. Market Share Analysis 2025

- 6.2. Company Profiles

- 6.2.1 Nestlé SA

- 6.2.1.1. Overview

- 6.2.1.2. Products

- 6.2.1.3. SWOT Analysis

- 6.2.1.4. Recent Developments

- 6.2.1.5. Financials (Based on Availability)

- 6.2.2 The Vegan Dairy Pty Ltd

- 6.2.2.1. Overview

- 6.2.2.2. Products

- 6.2.2.3. SWOT Analysis

- 6.2.2.4. Recent Developments

- 6.2.2.5. Financials (Based on Availability)

- 6.2.3 Califia Farms LLC

- 6.2.3.1. Overview

- 6.2.3.2. Products

- 6.2.3.3. SWOT Analysis

- 6.2.3.4. Recent Developments

- 6.2.3.5. Financials (Based on Availability)

- 6.2.4 Dairy-Free Down Under

- 6.2.4.1. Overview

- 6.2.4.2. Products

- 6.2.4.3. SWOT Analysis

- 6.2.4.4. Recent Developments

- 6.2.4.5. Financials (Based on Availability)

- 6.2.5 Danone SA

- 6.2.5.1. Overview

- 6.2.5.2. Products

- 6.2.5.3. SWOT Analysis

- 6.2.5.4. Recent Developments

- 6.2.5.5. Financials (Based on Availability)

- 6.2.6 PureHarvest

- 6.2.6.1. Overview

- 6.2.6.2. Products

- 6.2.6.3. SWOT Analysis

- 6.2.6.4. Recent Developments

- 6.2.6.5. Financials (Based on Availability)

- 6.2.7 Blue Diamond Growers

- 6.2.7.1. Overview

- 6.2.7.2. Products

- 6.2.7.3. SWOT Analysis

- 6.2.7.4. Recent Developments

- 6.2.7.5. Financials (Based on Availability)

- 6.2.8 Vitasoy International Holdings Lt

- 6.2.8.1. Overview

- 6.2.8.2. Products

- 6.2.8.3. SWOT Analysis

- 6.2.8.4. Recent Developments

- 6.2.8.5. Financials (Based on Availability)

- 6.2.9 Namyang Dairy Products Co Ltd

- 6.2.9.1. Overview

- 6.2.9.2. Products

- 6.2.9.3. SWOT Analysis

- 6.2.9.4. Recent Developments

- 6.2.9.5. Financials (Based on Availability)

- 6.2.10 Spiral Foods

- 6.2.10.1. Overview

- 6.2.10.2. Products

- 6.2.10.3. SWOT Analysis

- 6.2.10.4. Recent Developments

- 6.2.10.5. Financials (Based on Availability)

- 6.2.11 Sanitarium Health and Wellbeing Company

- 6.2.11.1. Overview

- 6.2.11.2. Products

- 6.2.11.3. SWOT Analysis

- 6.2.11.4. Recent Developments

- 6.2.11.5. Financials (Based on Availability)

- 6.2.1 Nestlé SA

List of Figures

- Figure 1: Australia Dairy Alternatives Market Revenue Breakdown (million, %) by Product 2025 & 2033

- Figure 2: Australia Dairy Alternatives Market Share (%) by Company 2025

List of Tables

- Table 1: Australia Dairy Alternatives Market Revenue million Forecast, by Category 2020 & 2033

- Table 2: Australia Dairy Alternatives Market Revenue million Forecast, by Distribution Channel 2020 & 2033

- Table 3: Australia Dairy Alternatives Market Revenue million Forecast, by Region 2020 & 2033

- Table 4: Australia Dairy Alternatives Market Revenue million Forecast, by Category 2020 & 2033

- Table 5: Australia Dairy Alternatives Market Revenue million Forecast, by Distribution Channel 2020 & 2033

- Table 6: Australia Dairy Alternatives Market Revenue million Forecast, by Country 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Australia Dairy Alternatives Market?

The projected CAGR is approximately 12.1%.

2. Which companies are prominent players in the Australia Dairy Alternatives Market?

Key companies in the market include Nestlé SA, The Vegan Dairy Pty Ltd, Califia Farms LLC, Dairy-Free Down Under, Danone SA, PureHarvest, Blue Diamond Growers, Vitasoy International Holdings Lt, Namyang Dairy Products Co Ltd, Spiral Foods, Sanitarium Health and Wellbeing Company.

3. What are the main segments of the Australia Dairy Alternatives Market?

The market segments include Category, Distribution Channel.

4. Can you provide details about the market size?

The market size is estimated to be USD 601.39 million as of 2022.

5. What are some drivers contributing to market growth?

Growing Inclination Towards Vegan/Plant-based Protein Sources; Increasing Demand for Functional Protein Beverages.

6. What are the notable trends driving market growth?

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT.

7. Are there any restraints impacting market growth?

Competition from Substitute Products.

8. Can you provide examples of recent developments in the market?

October 2022: Vitasoy International Holdings Ltd planned to expand its dairy alternative business by acquiring the shares from its joint venture Bega Cheese subsidiary National Food Holdings Ltd.August 2022: The addition of the new Oat Barista Blend to Califia Farms' already well-liked Original and Unsweetened Almondmilk Barista Blends demonstrated the company's commitment to quality coffee while bolstering its relationships with both old and new coffee shops.August 2022: Sanitarium launched a new master brand campaign for its plant-based milk 'So Good' brand.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Australia Dairy Alternatives Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Australia Dairy Alternatives Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Australia Dairy Alternatives Market?

To stay informed about further developments, trends, and reports in the Australia Dairy Alternatives Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence