Key Insights

The aerospace materials market, currently valued at approximately $XX million (estimated based on provided CAGR and market size), is projected to experience robust growth, exceeding an 8% CAGR from 2025 to 2033. This expansion is fueled by several key drivers: the increasing demand for lightweight and high-performance materials in aircraft manufacturing, particularly within the burgeoning commercial aviation and space exploration sectors; advancements in composite materials technology leading to improved fuel efficiency and structural integrity; and rising military and defense spending globally, driving demand for advanced materials in military aircraft and spacecraft. Significant trends include the adoption of sustainable and bio-based materials to reduce environmental impact, a growing focus on additive manufacturing for faster prototyping and production, and the increasing integration of smart materials with embedded sensors for enhanced performance monitoring and predictive maintenance. However, challenges remain, including the high cost of advanced materials, stringent regulatory requirements for aerospace applications, and supply chain complexities impacting material availability and pricing.

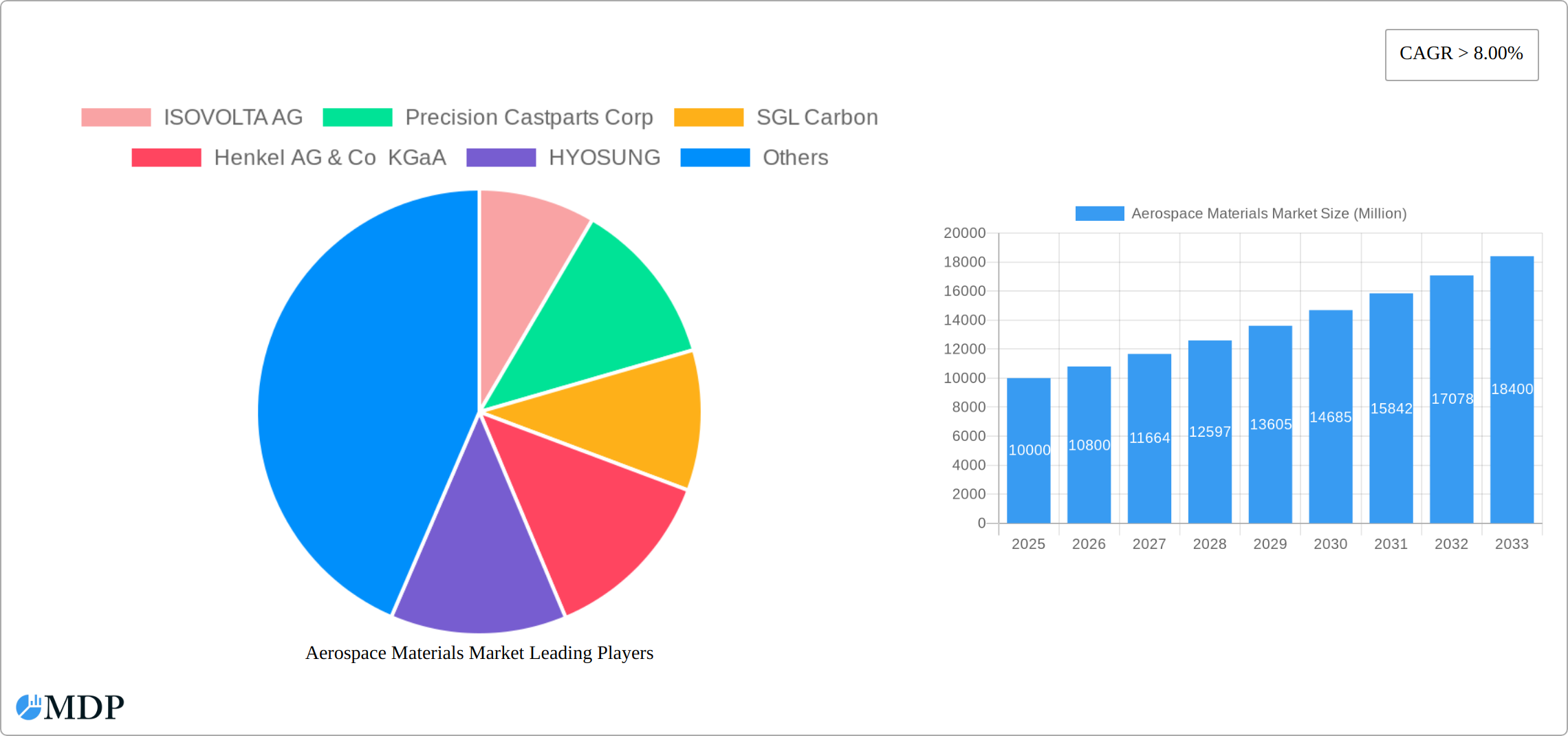

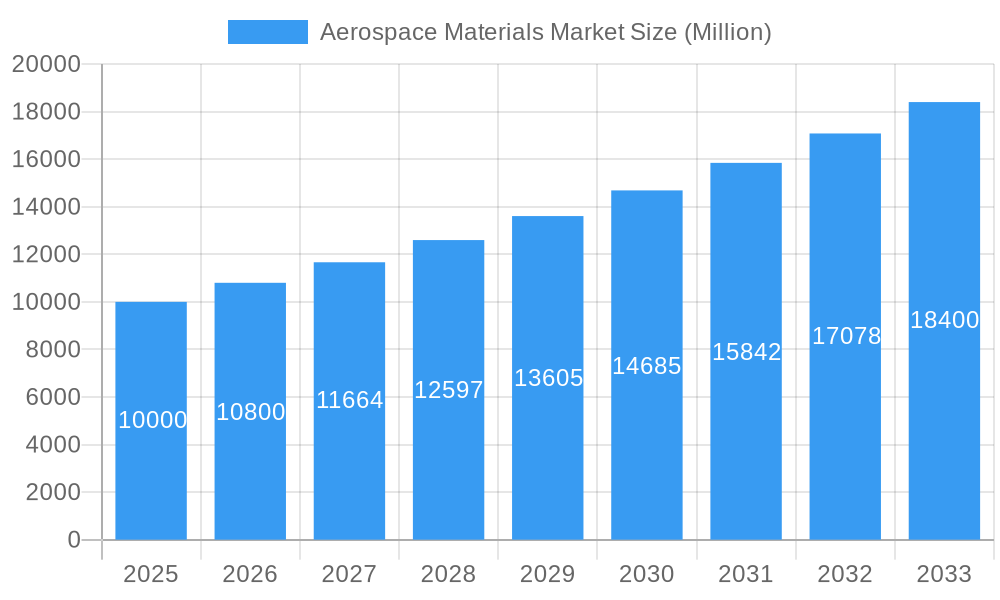

Aerospace Materials Market Market Size (In Billion)

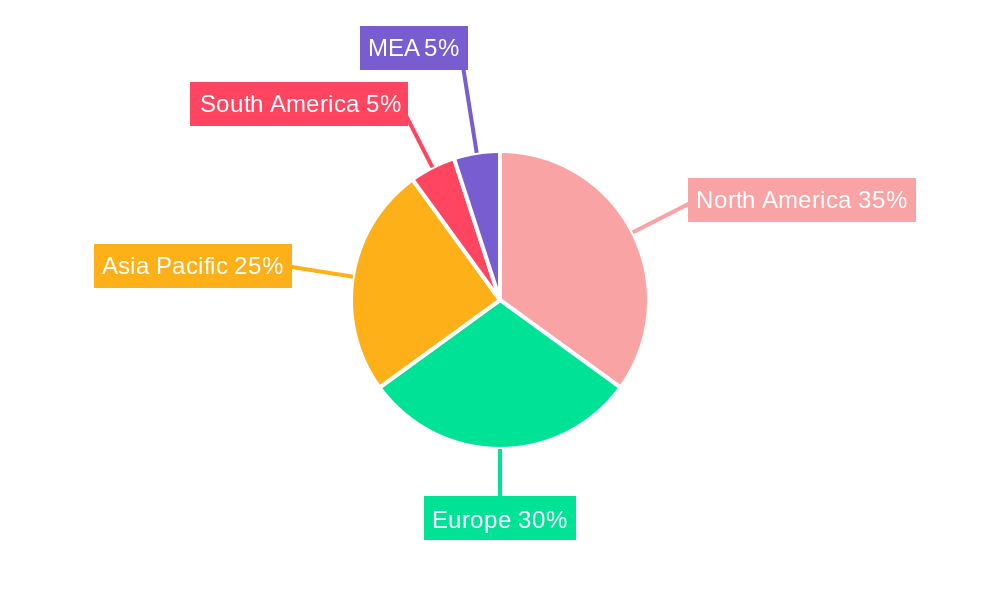

The market segmentation reveals significant opportunities across various material types. Alloys, particularly titanium, aluminum, and steel, dominate the market due to their established application in structural components. However, the increasing adoption of composites, such as carbon fiber and glass fiber, is driving significant growth, particularly in lightweight applications. The adhesives and sealants segment is also experiencing substantial growth, driven by the need for reliable bonding and sealing in aircraft structures. Regional variations exist, with North America and Europe currently holding significant market shares, driven by established aerospace manufacturing bases. However, the Asia-Pacific region, particularly China and India, is expected to experience rapid growth due to increased domestic aerospace production and investments in infrastructure. The competitive landscape is characterized by a mix of established global players and regional specialists, each focusing on specific material types and applications. Continued innovation, strategic partnerships, and mergers & acquisitions will likely shape the market dynamics in the coming years.

Aerospace Materials Market Company Market Share

Aerospace Materials Market Report: 2019-2033 Forecast

This comprehensive report provides a detailed analysis of the Aerospace Materials Market, offering valuable insights for industry stakeholders, investors, and researchers. Covering the period from 2019 to 2033, with a focus on 2025, this report meticulously examines market dynamics, leading players, and future trends. The market is projected to reach xx Million by 2033, exhibiting a CAGR of xx% during the forecast period (2025-2033).

Aerospace Materials Market Market Dynamics & Concentration

The aerospace materials market exhibits a moderately concentrated competitive landscape, dominated by several key players holding substantial market share. However, a vibrant ecosystem of smaller, specialized companies fuels innovation and ensures a dynamic competitive environment. Market concentration is significantly shaped by technological breakthroughs, stringent regulatory compliance, and the escalating demand for high-performance materials. The combined market share of the top five players is projected to be approximately [Insert Updated Percentage]% in 2025.

Innovation Drivers:

- Significant advancements in composite materials, encompassing carbon fiber, glass fiber, and novel hybrid composites, are revolutionizing aircraft design and performance.

- The development of lightweight, high-strength alloys, including Titanium, Aluminum, and Magnesium, along with innovative metal matrix composites, addresses the ongoing need for reduced weight and enhanced structural integrity.

- Continuous innovation in adhesives and sealants, focusing on improved bonding strength, durability, and resistance to harsh environmental conditions, is crucial for aircraft assembly and maintenance.

- A growing emphasis on sustainable and environmentally friendly materials, including bio-based composites and recyclable materials, is reshaping the industry's commitment to reducing its environmental impact.

- The exploration and implementation of smart materials, with capabilities like self-healing or embedded structural health monitoring, holds considerable promise for future aircraft design and maintenance.

Regulatory Frameworks: Stringent safety and quality standards enforced by aviation authorities such as the FAA and EASA exert a considerable influence on material selection and manufacturing processes. These regulations not only drive innovation but also mandate rigorous testing and certification procedures throughout the entire lifecycle of aerospace materials.

Product Substitutes & Competition: The emergence of alternative materials, such as bio-based composites and advanced polymer systems, presents both a potential challenge and a significant opportunity for innovation and market diversification. Competition is fierce, with companies constantly striving for superior performance, cost-effectiveness, and sustainable manufacturing processes.

End-User Trends: The persistent rise in global air travel demand, coupled with the increasing adoption of advanced aircraft designs (like blended wing bodies and more electric aircraft), is a primary driver shaping material requirements and fostering innovation in the aerospace materials sector. The demand for fuel-efficient aircraft is also a key factor.

M&A Activities: The aerospace materials market has experienced substantial merger and acquisition (M&A) activity in recent years, with [Insert Updated Number] deals recorded between 2019 and 2024. This consolidation trend reflects strategic efforts by industry players to expand their product portfolios, enhance their technological capabilities, and secure a stronger market position. A notable example is ISOVOLTA AG's acquisition of Gurit Holding AG's Aviation and Aerospace business unit, which significantly broadened its presence in the market. [Add other relevant examples if available]

Aerospace Materials Market Industry Trends & Analysis

The aerospace materials market is experiencing robust growth, fueled by several key factors. The continuous increase in global air travel demand necessitates a substantial rise in aircraft manufacturing, thereby significantly increasing the demand for advanced materials. Technological advancements, particularly in composites and lightweight alloys, are pivotal in enabling the development of more fuel-efficient and durable aircraft. Furthermore, the persistent rise in defense spending across numerous countries provides considerable impetus to market expansion.

The market demonstrates a strong preference for high-performance materials that deliver superior strength-to-weight ratios, enhanced durability, and improved resistance to the extreme environmental conditions encountered during flight. This trend is further amplified by the growing adoption of sustainable aviation practices, which includes a focus on developing bio-based and recyclable aerospace materials.

Competitive dynamics are shaped by relentless innovation, strategic partnerships, and intense competition amongst both established industry leaders and emerging companies. Market leaders are making significant investments in research and development (R&D) to pioneer next-generation materials and broaden their product portfolios, fostering a dynamic and competitive landscape.

The market is projected to experience a compound annual growth rate (CAGR) of [Insert Updated CAGR]% during the forecast period (2025-2033), reaching a market value of [Insert Updated Market Value] Million by 2033. Market penetration of advanced composites is anticipated to increase from [Insert Updated Percentage]% in 2025 to [Insert Updated Percentage]% by 2033, driven by their superior performance characteristics and the ongoing trend towards lighter and more fuel-efficient aircraft.

Leading Markets & Segments in Aerospace Materials Market

The North American region dominates the Aerospace Materials market, followed by Europe and Asia-Pacific. This dominance stems from the presence of major aircraft manufacturers and a strong aerospace industry ecosystem in these regions.

Key Drivers:

- North America: Strong domestic aerospace industry, high R&D spending, and advanced technological capabilities.

- Europe: Significant presence of aircraft manufacturers (Airbus), strong regulatory frameworks, and a focus on sustainable aviation.

- Asia-Pacific: Rapid growth in air travel demand, increasing domestic aerospace manufacturing, and government support for industry development.

Dominant Segments:

Alloys: Titanium alloys continue to hold a significant market share due to their high strength-to-weight ratio, particularly in high-performance aircraft applications. Aluminum alloys remain prevalent in airframe construction due to their cost-effectiveness and ease of manufacturing.

Composites: Carbon fiber composites are experiencing rapid growth, driven by their superior strength, lightweight properties, and design flexibility. Glass fiber composites remain important in less demanding applications.

Adhesives and Sealants: Epoxy and polyurethane-based adhesives and sealants dominate the market, due to their excellent bonding properties and durability.

Aircraft Type: The commercial aircraft segment holds the largest market share, followed by the military and defense segment. The space vehicle segment shows significant growth potential driven by increasing space exploration activities.

Aerospace Materials Market Product Developments

Recent innovations in aerospace materials are primarily focused on achieving significant weight reduction, enhanced durability, and improved sustainability. Advanced composites such as carbon nanotube-reinforced polymers and various bio-based composites are gaining significant traction within the industry. These advancements are specifically aimed at enhancing aircraft fuel efficiency, minimizing emissions, and improving overall structural performance. New adhesives and sealants are constantly being developed, demonstrating superior environmental resistance and extended service life. The incorporation of smart materials, offering capabilities like self-healing or continuous structural health monitoring, presents immense potential for future applications in the aerospace industry.

Key Drivers of Aerospace Materials Market Growth

The robust growth trajectory of the aerospace materials market is propelled by a confluence of factors:

- Technological Advancements: Continuous breakthroughs in materials science are consistently yielding lighter, stronger, and more durable materials, enabling significant improvements in aircraft design and performance.

- Increasing Air Travel Demand: The persistently rising number of air passengers globally necessitates a corresponding increase in aircraft production, directly fueling the demand for advanced materials.

- Stringent Safety Regulations: Governments worldwide are implementing increasingly stringent safety regulations, mandating the use of high-quality, reliable, and thoroughly tested aerospace materials.

- Rising Defense Spending: Significant and sustained investments in military aviation and defense systems across various nations represent a crucial driver of demand for advanced and specialized aerospace materials.

- Sustainability Concerns: Growing environmental awareness is driving the adoption of sustainable and recyclable materials in the aerospace industry, creating new opportunities and challenges for material providers.

Challenges in the Aerospace Materials Market Market

The market faces challenges including:

- High material costs: Advanced materials like titanium alloys and carbon fiber composites can be expensive.

- Supply chain disruptions: Geopolitical factors and pandemics can cause supply chain disruptions, affecting availability.

- Stringent certification processes: The need to meet rigorous industry standards and certification procedures can delay product launches.

- Competition: Intense competition among established and new players necessitates continuous innovation and cost optimization.

Emerging Opportunities in Aerospace Materials Market

Long-term growth is driven by several factors:

- Development of advanced composites: Further advancements in carbon fiber and other composite materials will lead to lightweight, high-strength structures.

- Sustainable aviation initiatives: Increasing focus on reducing aircraft emissions is driving the development of eco-friendly materials.

- Strategic partnerships: Collaborations between material suppliers and aircraft manufacturers will facilitate the development and integration of novel materials.

- Expansion into new applications: The growth of space exploration and unmanned aerial vehicles will provide new market opportunities.

Leading Players in the Aerospace Materials Market Sector

- ISOVOLTA AG

- Precision Castparts Corp

- SGL Carbon

- Henkel AG & Co KGaA

- HYOSUNG

- Arkema

- Beacon Adhesives Inc

- The Sherwin-Williams Company

- Jiangsu Hengshen Co Ltd

- Reliance Industries Ltd

- Solvay

- Mitsubishi Chemical Corporation

- Akzo Nobel NV

- Aluminum Corporation of China Limited (Chalco)

- Rogers Corporation

- Evonik Industries AG

- 3M

- PPG Industries Inc

- ATI

- Corporation VSMPO-AVISMA

- BASF SE

- Socomore

- Huntsman International LLC

- Axalta Coating Systems

- Howmet Aerospace

- Toray Industries Inc

- Mankiewicz Gebr & Co

- Greiner AG

- Hexcel Corporation

- Carpenter Technology Corporation

- NIPPON STEEL CORPORATION

- DELO Industrie Klebstoffe GmbH & Co KGaA

- Tata Steel (Corus)

- Acerinox SA (VDM Metals)

- Nanjing Yunhai Special Metal Co Ltd

- Hentzen Coatings Inc

Key Milestones in Aerospace Materials Market Industry

- October 2022: Toray Composite Materials America partnered with SpecialityMaterials to develop next-generation aerospace materials.

- July 2022: Hexcel partnered with Dassault to supply carbon fiber prepreg for the Falcon 10X program.

- April 2022: ISOVOLTA AG acquired Gurit Holding AG's Aviation and Aerospace business unit.

Strategic Outlook for Aerospace Materials Market Market

The aerospace materials market presents substantial growth opportunities for companies with innovative technologies and strategic foresight. Continuous innovation in material science, coupled with the relentless demand for fuel-efficient and sustainable aircraft, will remain a powerful catalyst for market expansion. Strategic partnerships and collaborations among industry players will be essential for accelerating technological advancements and facilitating the timely introduction of innovative materials into the market. The unwavering emphasis on lightweighting, durability, and sustainability will fundamentally shape future material selection and significantly drive market growth, creating a dynamic and competitive landscape for years to come.

Aerospace Materials Market Segmentation

-

1. Type

-

1.1. Structural

-

1.1.1. Composites

- 1.1.1.1. Glass Fiber

- 1.1.1.2. Carbon Fiber

- 1.1.1.3. Aramid Fiber

- 1.1.1.4. Other Composites

- 1.1.2. Plastics

-

1.1.3. Alloys

- 1.1.3.1. Titanium

- 1.1.3.2. Aluminium

- 1.1.3.3. Steel

- 1.1.3.4. Super

- 1.1.3.5. Magnesium

- 1.1.3.6. Other Alloys

-

1.1.1. Composites

-

1.2. Non-structural

- 1.2.1. Coatings

-

1.2.2. Adhesives and Sealants

- 1.2.2.1. Epoxy

- 1.2.2.2. Polyurethane

- 1.2.2.3. Silicone

- 1.2.2.4. Other Adhesives and Sealants

-

1.2.3. Foams

- 1.2.3.1. Polyethylene

- 1.2.3.2. Other Foams

- 1.2.4. Seals

-

1.1. Structural

-

2. Aircraft Type

- 2.1. General and Commercial

- 2.2. Military and Defense

- 2.3. Space Vehicles

Aerospace Materials Market Segmentation By Geography

-

1. Asia Pacific

- 1.1. China

- 1.2. India

- 1.3. Japan

- 1.4. South Korea

- 1.5. Rest of Asia Pacific

-

2. North America

- 2.1. United States

- 2.2. Canada

- 2.3. Mexico

-

3. Europe

- 3.1. Germany

- 3.2. United Kingdom

- 3.3. France

- 3.4. Italy

- 3.5. Spain

- 3.6. Russia

- 3.7. Rest of Europe

-

4. Rest of the World

- 4.1. South America

- 4.2. Middle East and Africa

Aerospace Materials Market Regional Market Share

Geographic Coverage of Aerospace Materials Market

Aerospace Materials Market REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2020-2034 |

| Base Year | 2025 |

| Estimated Year | 2026 |

| Forecast Period | 2026-2034 |

| Historical Period | 2020-2025 |

| Growth Rate | CAGR of 8.3% from 2020-2034 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Increasing Use of Composites in Aircraft Manufacturing; Growing Space Industry; Increasing Government Spending on Defense in the United States and European Countries

- 3.3. Market Restrains

- 3.3.1. High Manufacturing Cost of Carbon Fibers; Declining Usage of Alloys

- 3.4. Market Trends

- 3.4.1. Increasing Demand for General and Commercial Aircraft

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Aerospace Materials Market Analysis, Insights and Forecast, 2020-2032

- 5.1. Market Analysis, Insights and Forecast - by Type

- 5.1.1. Structural

- 5.1.1.1. Composites

- 5.1.1.1.1. Glass Fiber

- 5.1.1.1.2. Carbon Fiber

- 5.1.1.1.3. Aramid Fiber

- 5.1.1.1.4. Other Composites

- 5.1.1.2. Plastics

- 5.1.1.3. Alloys

- 5.1.1.3.1. Titanium

- 5.1.1.3.2. Aluminium

- 5.1.1.3.3. Steel

- 5.1.1.3.4. Super

- 5.1.1.3.5. Magnesium

- 5.1.1.3.6. Other Alloys

- 5.1.1.1. Composites

- 5.1.2. Non-structural

- 5.1.2.1. Coatings

- 5.1.2.2. Adhesives and Sealants

- 5.1.2.2.1. Epoxy

- 5.1.2.2.2. Polyurethane

- 5.1.2.2.3. Silicone

- 5.1.2.2.4. Other Adhesives and Sealants

- 5.1.2.3. Foams

- 5.1.2.3.1. Polyethylene

- 5.1.2.3.2. Other Foams

- 5.1.2.4. Seals

- 5.1.1. Structural

- 5.2. Market Analysis, Insights and Forecast - by Aircraft Type

- 5.2.1. General and Commercial

- 5.2.2. Military and Defense

- 5.2.3. Space Vehicles

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. Asia Pacific

- 5.3.2. North America

- 5.3.3. Europe

- 5.3.4. Rest of the World

- 5.1. Market Analysis, Insights and Forecast - by Type

- 6. Asia Pacific Aerospace Materials Market Analysis, Insights and Forecast, 2020-2032

- 6.1. Market Analysis, Insights and Forecast - by Type

- 6.1.1. Structural

- 6.1.1.1. Composites

- 6.1.1.1.1. Glass Fiber

- 6.1.1.1.2. Carbon Fiber

- 6.1.1.1.3. Aramid Fiber

- 6.1.1.1.4. Other Composites

- 6.1.1.2. Plastics

- 6.1.1.3. Alloys

- 6.1.1.3.1. Titanium

- 6.1.1.3.2. Aluminium

- 6.1.1.3.3. Steel

- 6.1.1.3.4. Super

- 6.1.1.3.5. Magnesium

- 6.1.1.3.6. Other Alloys

- 6.1.1.1. Composites

- 6.1.2. Non-structural

- 6.1.2.1. Coatings

- 6.1.2.2. Adhesives and Sealants

- 6.1.2.2.1. Epoxy

- 6.1.2.2.2. Polyurethane

- 6.1.2.2.3. Silicone

- 6.1.2.2.4. Other Adhesives and Sealants

- 6.1.2.3. Foams

- 6.1.2.3.1. Polyethylene

- 6.1.2.3.2. Other Foams

- 6.1.2.4. Seals

- 6.1.1. Structural

- 6.2. Market Analysis, Insights and Forecast - by Aircraft Type

- 6.2.1. General and Commercial

- 6.2.2. Military and Defense

- 6.2.3. Space Vehicles

- 6.1. Market Analysis, Insights and Forecast - by Type

- 7. North America Aerospace Materials Market Analysis, Insights and Forecast, 2020-2032

- 7.1. Market Analysis, Insights and Forecast - by Type

- 7.1.1. Structural

- 7.1.1.1. Composites

- 7.1.1.1.1. Glass Fiber

- 7.1.1.1.2. Carbon Fiber

- 7.1.1.1.3. Aramid Fiber

- 7.1.1.1.4. Other Composites

- 7.1.1.2. Plastics

- 7.1.1.3. Alloys

- 7.1.1.3.1. Titanium

- 7.1.1.3.2. Aluminium

- 7.1.1.3.3. Steel

- 7.1.1.3.4. Super

- 7.1.1.3.5. Magnesium

- 7.1.1.3.6. Other Alloys

- 7.1.1.1. Composites

- 7.1.2. Non-structural

- 7.1.2.1. Coatings

- 7.1.2.2. Adhesives and Sealants

- 7.1.2.2.1. Epoxy

- 7.1.2.2.2. Polyurethane

- 7.1.2.2.3. Silicone

- 7.1.2.2.4. Other Adhesives and Sealants

- 7.1.2.3. Foams

- 7.1.2.3.1. Polyethylene

- 7.1.2.3.2. Other Foams

- 7.1.2.4. Seals

- 7.1.1. Structural

- 7.2. Market Analysis, Insights and Forecast - by Aircraft Type

- 7.2.1. General and Commercial

- 7.2.2. Military and Defense

- 7.2.3. Space Vehicles

- 7.1. Market Analysis, Insights and Forecast - by Type

- 8. Europe Aerospace Materials Market Analysis, Insights and Forecast, 2020-2032

- 8.1. Market Analysis, Insights and Forecast - by Type

- 8.1.1. Structural

- 8.1.1.1. Composites

- 8.1.1.1.1. Glass Fiber

- 8.1.1.1.2. Carbon Fiber

- 8.1.1.1.3. Aramid Fiber

- 8.1.1.1.4. Other Composites

- 8.1.1.2. Plastics

- 8.1.1.3. Alloys

- 8.1.1.3.1. Titanium

- 8.1.1.3.2. Aluminium

- 8.1.1.3.3. Steel

- 8.1.1.3.4. Super

- 8.1.1.3.5. Magnesium

- 8.1.1.3.6. Other Alloys

- 8.1.1.1. Composites

- 8.1.2. Non-structural

- 8.1.2.1. Coatings

- 8.1.2.2. Adhesives and Sealants

- 8.1.2.2.1. Epoxy

- 8.1.2.2.2. Polyurethane

- 8.1.2.2.3. Silicone

- 8.1.2.2.4. Other Adhesives and Sealants

- 8.1.2.3. Foams

- 8.1.2.3.1. Polyethylene

- 8.1.2.3.2. Other Foams

- 8.1.2.4. Seals

- 8.1.1. Structural

- 8.2. Market Analysis, Insights and Forecast - by Aircraft Type

- 8.2.1. General and Commercial

- 8.2.2. Military and Defense

- 8.2.3. Space Vehicles

- 8.1. Market Analysis, Insights and Forecast - by Type

- 9. Rest of the World Aerospace Materials Market Analysis, Insights and Forecast, 2020-2032

- 9.1. Market Analysis, Insights and Forecast - by Type

- 9.1.1. Structural

- 9.1.1.1. Composites

- 9.1.1.1.1. Glass Fiber

- 9.1.1.1.2. Carbon Fiber

- 9.1.1.1.3. Aramid Fiber

- 9.1.1.1.4. Other Composites

- 9.1.1.2. Plastics

- 9.1.1.3. Alloys

- 9.1.1.3.1. Titanium

- 9.1.1.3.2. Aluminium

- 9.1.1.3.3. Steel

- 9.1.1.3.4. Super

- 9.1.1.3.5. Magnesium

- 9.1.1.3.6. Other Alloys

- 9.1.1.1. Composites

- 9.1.2. Non-structural

- 9.1.2.1. Coatings

- 9.1.2.2. Adhesives and Sealants

- 9.1.2.2.1. Epoxy

- 9.1.2.2.2. Polyurethane

- 9.1.2.2.3. Silicone

- 9.1.2.2.4. Other Adhesives and Sealants

- 9.1.2.3. Foams

- 9.1.2.3.1. Polyethylene

- 9.1.2.3.2. Other Foams

- 9.1.2.4. Seals

- 9.1.1. Structural

- 9.2. Market Analysis, Insights and Forecast - by Aircraft Type

- 9.2.1. General and Commercial

- 9.2.2. Military and Defense

- 9.2.3. Space Vehicles

- 9.1. Market Analysis, Insights and Forecast - by Type

- 10. Competitive Analysis

- 10.1. Global Market Share Analysis 2025

- 10.2. Company Profiles

- 10.2.1 ISOVOLTA AG

- 10.2.1.1. Overview

- 10.2.1.2. Products

- 10.2.1.3. SWOT Analysis

- 10.2.1.4. Recent Developments

- 10.2.1.5. Financials (Based on Availability)

- 10.2.2 Precision Castparts Corp

- 10.2.2.1. Overview

- 10.2.2.2. Products

- 10.2.2.3. SWOT Analysis

- 10.2.2.4. Recent Developments

- 10.2.2.5. Financials (Based on Availability)

- 10.2.3 SGL Carbon

- 10.2.3.1. Overview

- 10.2.3.2. Products

- 10.2.3.3. SWOT Analysis

- 10.2.3.4. Recent Developments

- 10.2.3.5. Financials (Based on Availability)

- 10.2.4 Henkel AG & Co KGaA

- 10.2.4.1. Overview

- 10.2.4.2. Products

- 10.2.4.3. SWOT Analysis

- 10.2.4.4. Recent Developments

- 10.2.4.5. Financials (Based on Availability)

- 10.2.5 HYOSUNG

- 10.2.5.1. Overview

- 10.2.5.2. Products

- 10.2.5.3. SWOT Analysis

- 10.2.5.4. Recent Developments

- 10.2.5.5. Financials (Based on Availability)

- 10.2.6 Arkema

- 10.2.6.1. Overview

- 10.2.6.2. Products

- 10.2.6.3. SWOT Analysis

- 10.2.6.4. Recent Developments

- 10.2.6.5. Financials (Based on Availability)

- 10.2.7 Beacon Adhesives Inc

- 10.2.7.1. Overview

- 10.2.7.2. Products

- 10.2.7.3. SWOT Analysis

- 10.2.7.4. Recent Developments

- 10.2.7.5. Financials (Based on Availability)

- 10.2.8 The Sherwin-Williams Company

- 10.2.8.1. Overview

- 10.2.8.2. Products

- 10.2.8.3. SWOT Analysis

- 10.2.8.4. Recent Developments

- 10.2.8.5. Financials (Based on Availability)

- 10.2.9 Jiangsu Hengshen Co Ltd

- 10.2.9.1. Overview

- 10.2.9.2. Products

- 10.2.9.3. SWOT Analysis

- 10.2.9.4. Recent Developments

- 10.2.9.5. Financials (Based on Availability)

- 10.2.10 Reliance Industries Ltd

- 10.2.10.1. Overview

- 10.2.10.2. Products

- 10.2.10.3. SWOT Analysis

- 10.2.10.4. Recent Developments

- 10.2.10.5. Financials (Based on Availability)

- 10.2.11 Solvay

- 10.2.11.1. Overview

- 10.2.11.2. Products

- 10.2.11.3. SWOT Analysis

- 10.2.11.4. Recent Developments

- 10.2.11.5. Financials (Based on Availability)

- 10.2.12 Mitsubishi Chemical Corporation

- 10.2.12.1. Overview

- 10.2.12.2. Products

- 10.2.12.3. SWOT Analysis

- 10.2.12.4. Recent Developments

- 10.2.12.5. Financials (Based on Availability)

- 10.2.13 Akzo Nobel NV

- 10.2.13.1. Overview

- 10.2.13.2. Products

- 10.2.13.3. SWOT Analysis

- 10.2.13.4. Recent Developments

- 10.2.13.5. Financials (Based on Availability)

- 10.2.14 Aluminum Corporation of China Limited (Chalco)

- 10.2.14.1. Overview

- 10.2.14.2. Products

- 10.2.14.3. SWOT Analysis

- 10.2.14.4. Recent Developments

- 10.2.14.5. Financials (Based on Availability)

- 10.2.15 Rogers Corporation

- 10.2.15.1. Overview

- 10.2.15.2. Products

- 10.2.15.3. SWOT Analysis

- 10.2.15.4. Recent Developments

- 10.2.15.5. Financials (Based on Availability)

- 10.2.16 Evonik Industries AG

- 10.2.16.1. Overview

- 10.2.16.2. Products

- 10.2.16.3. SWOT Analysis

- 10.2.16.4. Recent Developments

- 10.2.16.5. Financials (Based on Availability)

- 10.2.17 3M

- 10.2.17.1. Overview

- 10.2.17.2. Products

- 10.2.17.3. SWOT Analysis

- 10.2.17.4. Recent Developments

- 10.2.17.5. Financials (Based on Availability)

- 10.2.18 PPG Industries Inc

- 10.2.18.1. Overview

- 10.2.18.2. Products

- 10.2.18.3. SWOT Analysis

- 10.2.18.4. Recent Developments

- 10.2.18.5. Financials (Based on Availability)

- 10.2.19 ATI

- 10.2.19.1. Overview

- 10.2.19.2. Products

- 10.2.19.3. SWOT Analysis

- 10.2.19.4. Recent Developments

- 10.2.19.5. Financials (Based on Availability)

- 10.2.20 Corporation VSMPO-AVISMA

- 10.2.20.1. Overview

- 10.2.20.2. Products

- 10.2.20.3. SWOT Analysis

- 10.2.20.4. Recent Developments

- 10.2.20.5. Financials (Based on Availability)

- 10.2.21 BASF SE

- 10.2.21.1. Overview

- 10.2.21.2. Products

- 10.2.21.3. SWOT Analysis

- 10.2.21.4. Recent Developments

- 10.2.21.5. Financials (Based on Availability)

- 10.2.22 Socomore

- 10.2.22.1. Overview

- 10.2.22.2. Products

- 10.2.22.3. SWOT Analysis

- 10.2.22.4. Recent Developments

- 10.2.22.5. Financials (Based on Availability)

- 10.2.23 Huntsman International LLC

- 10.2.23.1. Overview

- 10.2.23.2. Products

- 10.2.23.3. SWOT Analysis

- 10.2.23.4. Recent Developments

- 10.2.23.5. Financials (Based on Availability)

- 10.2.24 Axalta Coating Systems

- 10.2.24.1. Overview

- 10.2.24.2. Products

- 10.2.24.3. SWOT Analysis

- 10.2.24.4. Recent Developments

- 10.2.24.5. Financials (Based on Availability)

- 10.2.25 Howmet Aerospace

- 10.2.25.1. Overview

- 10.2.25.2. Products

- 10.2.25.3. SWOT Analysis

- 10.2.25.4. Recent Developments

- 10.2.25.5. Financials (Based on Availability)

- 10.2.26 Toray Industries Inc *List Not Exhaustive

- 10.2.26.1. Overview

- 10.2.26.2. Products

- 10.2.26.3. SWOT Analysis

- 10.2.26.4. Recent Developments

- 10.2.26.5. Financials (Based on Availability)

- 10.2.27 Mankiewicz Gebr & Co

- 10.2.27.1. Overview

- 10.2.27.2. Products

- 10.2.27.3. SWOT Analysis

- 10.2.27.4. Recent Developments

- 10.2.27.5. Financials (Based on Availability)

- 10.2.28 Greiner AG

- 10.2.28.1. Overview

- 10.2.28.2. Products

- 10.2.28.3. SWOT Analysis

- 10.2.28.4. Recent Developments

- 10.2.28.5. Financials (Based on Availability)

- 10.2.29 Hexcel Corporation

- 10.2.29.1. Overview

- 10.2.29.2. Products

- 10.2.29.3. SWOT Analysis

- 10.2.29.4. Recent Developments

- 10.2.29.5. Financials (Based on Availability)

- 10.2.30 Carpenter Technology Corporation

- 10.2.30.1. Overview

- 10.2.30.2. Products

- 10.2.30.3. SWOT Analysis

- 10.2.30.4. Recent Developments

- 10.2.30.5. Financials (Based on Availability)

- 10.2.31 NIPPON STEEL CORPORATION

- 10.2.31.1. Overview

- 10.2.31.2. Products

- 10.2.31.3. SWOT Analysis

- 10.2.31.4. Recent Developments

- 10.2.31.5. Financials (Based on Availability)

- 10.2.32 DELO Industrie Klebstoffe GmbH & Co KGaA

- 10.2.32.1. Overview

- 10.2.32.2. Products

- 10.2.32.3. SWOT Analysis

- 10.2.32.4. Recent Developments

- 10.2.32.5. Financials (Based on Availability)

- 10.2.33 Tata Steel (Corus)

- 10.2.33.1. Overview

- 10.2.33.2. Products

- 10.2.33.3. SWOT Analysis

- 10.2.33.4. Recent Developments

- 10.2.33.5. Financials (Based on Availability)

- 10.2.34 Acerinox SA (VDM Metals)

- 10.2.34.1. Overview

- 10.2.34.2. Products

- 10.2.34.3. SWOT Analysis

- 10.2.34.4. Recent Developments

- 10.2.34.5. Financials (Based on Availability)

- 10.2.35 Nanjing Yunhai Special Metal Co Ltd

- 10.2.35.1. Overview

- 10.2.35.2. Products

- 10.2.35.3. SWOT Analysis

- 10.2.35.4. Recent Developments

- 10.2.35.5. Financials (Based on Availability)

- 10.2.36 Hentzen Coatings Inc

- 10.2.36.1. Overview

- 10.2.36.2. Products

- 10.2.36.3. SWOT Analysis

- 10.2.36.4. Recent Developments

- 10.2.36.5. Financials (Based on Availability)

- 10.2.1 ISOVOLTA AG

List of Figures

- Figure 1: Global Aerospace Materials Market Revenue Breakdown (undefined, %) by Region 2025 & 2033

- Figure 2: Asia Pacific Aerospace Materials Market Revenue (undefined), by Type 2025 & 2033

- Figure 3: Asia Pacific Aerospace Materials Market Revenue Share (%), by Type 2025 & 2033

- Figure 4: Asia Pacific Aerospace Materials Market Revenue (undefined), by Aircraft Type 2025 & 2033

- Figure 5: Asia Pacific Aerospace Materials Market Revenue Share (%), by Aircraft Type 2025 & 2033

- Figure 6: Asia Pacific Aerospace Materials Market Revenue (undefined), by Country 2025 & 2033

- Figure 7: Asia Pacific Aerospace Materials Market Revenue Share (%), by Country 2025 & 2033

- Figure 8: North America Aerospace Materials Market Revenue (undefined), by Type 2025 & 2033

- Figure 9: North America Aerospace Materials Market Revenue Share (%), by Type 2025 & 2033

- Figure 10: North America Aerospace Materials Market Revenue (undefined), by Aircraft Type 2025 & 2033

- Figure 11: North America Aerospace Materials Market Revenue Share (%), by Aircraft Type 2025 & 2033

- Figure 12: North America Aerospace Materials Market Revenue (undefined), by Country 2025 & 2033

- Figure 13: North America Aerospace Materials Market Revenue Share (%), by Country 2025 & 2033

- Figure 14: Europe Aerospace Materials Market Revenue (undefined), by Type 2025 & 2033

- Figure 15: Europe Aerospace Materials Market Revenue Share (%), by Type 2025 & 2033

- Figure 16: Europe Aerospace Materials Market Revenue (undefined), by Aircraft Type 2025 & 2033

- Figure 17: Europe Aerospace Materials Market Revenue Share (%), by Aircraft Type 2025 & 2033

- Figure 18: Europe Aerospace Materials Market Revenue (undefined), by Country 2025 & 2033

- Figure 19: Europe Aerospace Materials Market Revenue Share (%), by Country 2025 & 2033

- Figure 20: Rest of the World Aerospace Materials Market Revenue (undefined), by Type 2025 & 2033

- Figure 21: Rest of the World Aerospace Materials Market Revenue Share (%), by Type 2025 & 2033

- Figure 22: Rest of the World Aerospace Materials Market Revenue (undefined), by Aircraft Type 2025 & 2033

- Figure 23: Rest of the World Aerospace Materials Market Revenue Share (%), by Aircraft Type 2025 & 2033

- Figure 24: Rest of the World Aerospace Materials Market Revenue (undefined), by Country 2025 & 2033

- Figure 25: Rest of the World Aerospace Materials Market Revenue Share (%), by Country 2025 & 2033

List of Tables

- Table 1: Global Aerospace Materials Market Revenue undefined Forecast, by Type 2020 & 2033

- Table 2: Global Aerospace Materials Market Revenue undefined Forecast, by Aircraft Type 2020 & 2033

- Table 3: Global Aerospace Materials Market Revenue undefined Forecast, by Region 2020 & 2033

- Table 4: Global Aerospace Materials Market Revenue undefined Forecast, by Type 2020 & 2033

- Table 5: Global Aerospace Materials Market Revenue undefined Forecast, by Aircraft Type 2020 & 2033

- Table 6: Global Aerospace Materials Market Revenue undefined Forecast, by Country 2020 & 2033

- Table 7: China Aerospace Materials Market Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 8: India Aerospace Materials Market Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 9: Japan Aerospace Materials Market Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 10: South Korea Aerospace Materials Market Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 11: Rest of Asia Pacific Aerospace Materials Market Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 12: Global Aerospace Materials Market Revenue undefined Forecast, by Type 2020 & 2033

- Table 13: Global Aerospace Materials Market Revenue undefined Forecast, by Aircraft Type 2020 & 2033

- Table 14: Global Aerospace Materials Market Revenue undefined Forecast, by Country 2020 & 2033

- Table 15: United States Aerospace Materials Market Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 16: Canada Aerospace Materials Market Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 17: Mexico Aerospace Materials Market Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 18: Global Aerospace Materials Market Revenue undefined Forecast, by Type 2020 & 2033

- Table 19: Global Aerospace Materials Market Revenue undefined Forecast, by Aircraft Type 2020 & 2033

- Table 20: Global Aerospace Materials Market Revenue undefined Forecast, by Country 2020 & 2033

- Table 21: Germany Aerospace Materials Market Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 22: United Kingdom Aerospace Materials Market Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 23: France Aerospace Materials Market Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 24: Italy Aerospace Materials Market Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 25: Spain Aerospace Materials Market Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 26: Russia Aerospace Materials Market Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 27: Rest of Europe Aerospace Materials Market Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 28: Global Aerospace Materials Market Revenue undefined Forecast, by Type 2020 & 2033

- Table 29: Global Aerospace Materials Market Revenue undefined Forecast, by Aircraft Type 2020 & 2033

- Table 30: Global Aerospace Materials Market Revenue undefined Forecast, by Country 2020 & 2033

- Table 31: South America Aerospace Materials Market Revenue (undefined) Forecast, by Application 2020 & 2033

- Table 32: Middle East and Africa Aerospace Materials Market Revenue (undefined) Forecast, by Application 2020 & 2033

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the Aerospace Materials Market?

The projected CAGR is approximately 8.3%.

2. Which companies are prominent players in the Aerospace Materials Market?

Key companies in the market include ISOVOLTA AG, Precision Castparts Corp, SGL Carbon, Henkel AG & Co KGaA, HYOSUNG, Arkema, Beacon Adhesives Inc, The Sherwin-Williams Company, Jiangsu Hengshen Co Ltd, Reliance Industries Ltd, Solvay, Mitsubishi Chemical Corporation, Akzo Nobel NV, Aluminum Corporation of China Limited (Chalco), Rogers Corporation, Evonik Industries AG, 3M, PPG Industries Inc, ATI, Corporation VSMPO-AVISMA, BASF SE, Socomore, Huntsman International LLC, Axalta Coating Systems, Howmet Aerospace, Toray Industries Inc *List Not Exhaustive, Mankiewicz Gebr & Co, Greiner AG, Hexcel Corporation, Carpenter Technology Corporation, NIPPON STEEL CORPORATION, DELO Industrie Klebstoffe GmbH & Co KGaA, Tata Steel (Corus), Acerinox SA (VDM Metals), Nanjing Yunhai Special Metal Co Ltd, Hentzen Coatings Inc.

3. What are the main segments of the Aerospace Materials Market?

The market segments include Type, Aircraft Type.

4. Can you provide details about the market size?

The market size is estimated to be USD XXX N/A as of 2022.

5. What are some drivers contributing to market growth?

Increasing Use of Composites in Aircraft Manufacturing; Growing Space Industry; Increasing Government Spending on Defense in the United States and European Countries.

6. What are the notable trends driving market growth?

Increasing Demand for General and Commercial Aircraft.

7. Are there any restraints impacting market growth?

High Manufacturing Cost of Carbon Fibers; Declining Usage of Alloys.

8. Can you provide examples of recent developments in the market?

In October 2022, Toray Composite Materials America partnered with SpecialityMaterials, a boron fiber manufacturer, to develop advanced next-generation aerospace materials with functional properties. This move will strengthen Toray's position in the aerospace materials market.

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 4750, USD 5250, and USD 8750 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in N/A.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "Aerospace Materials Market," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the Aerospace Materials Market report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the Aerospace Materials Market?

To stay informed about further developments, trends, and reports in the Aerospace Materials Market, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence