Key Insights

The Indian Engineering, Procurement, and Construction (EPC) industry is experiencing robust growth, driven by significant investments in infrastructure development, particularly within the power generation sector. The market, valued at approximately $XX million in 2025 (assuming a logical estimation based on the provided CAGR of >3.00% and a stated market size of XX million - the exact figure is needed to provide a precise calculation, we'll assume a starting point for illustration), is projected to expand considerably over the forecast period (2025-2033). Key drivers include government initiatives promoting renewable energy sources, the increasing demand for electricity, and large-scale projects in transportation and industrial infrastructure. The thermal power segment currently holds a significant share, but the non-hydro renewable segment is experiencing the fastest growth, fueled by policy support and decreasing technology costs. This shift towards cleaner energy sources presents significant opportunities for EPC companies specializing in solar, wind, and other renewable technologies. While challenges remain, such as land acquisition issues and regulatory hurdles, the long-term outlook for the Indian EPC industry remains positive, with continued growth expected throughout the forecast period.

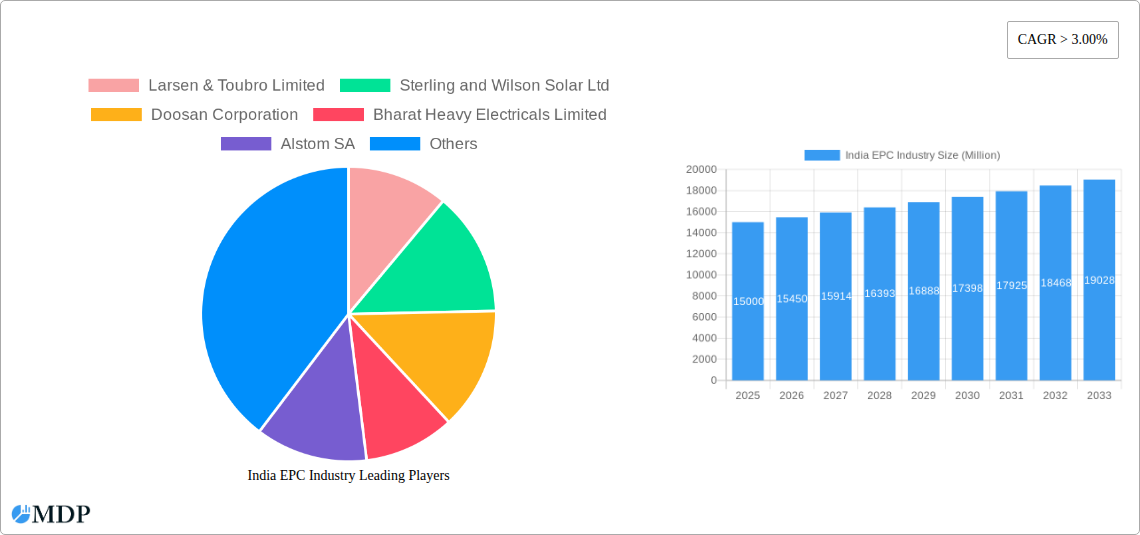

The competitive landscape is characterized by a mix of large multinational corporations and domestic players. Companies like Larsen & Toubro, Sterling and Wilson Solar, and Bharat Heavy Electricals are key market participants, leveraging their expertise and established presence. However, the sector is also witnessing increased competition from emerging players, particularly in the renewable energy segment. Regional variations exist within India, with certain areas experiencing faster growth due to higher investment activity and favorable policy environments. This regional disparity presents opportunities for companies to target specific areas based on their strengths and capabilities. Successful companies will likely focus on developing specialized expertise, building strong project management capabilities, and adapting to the evolving regulatory environment to secure a competitive advantage in this dynamic market. A thorough risk mitigation strategy factoring potential supply chain disruptions and fluctuating commodity prices is also crucial for sustainable success in this growing market.

India EPC Industry Report: 2019-2033 - A Comprehensive Market Analysis

This comprehensive report provides an in-depth analysis of the India EPC (Engineering, Procurement, and Construction) industry from 2019 to 2033. It delves into market dynamics, key trends, leading players, and future growth opportunities, offering invaluable insights for industry stakeholders, investors, and strategic decision-makers. The report covers key segments within power generation (Thermal, Hydro, Nuclear, Non-Hydro Renewables) and examines the impact of technological advancements, regulatory changes, and competitive landscapes on market growth. The base year for this analysis is 2025, with forecasts extending to 2033. The report utilizes a wealth of data and insights to provide a robust and actionable understanding of this dynamic sector. Estimated market value in 2025 is projected to be at xx Million.

India EPC Industry Market Dynamics & Concentration

The Indian EPC industry exhibits a moderately concentrated market structure, dominated by large players like Larsen & Toubro Limited, Sterling and Wilson Solar Ltd, Doosan Corporation, Bharat Heavy Electricals Limited, and Alstom SA. However, the presence of numerous mid-sized and smaller players fosters competition. Market share analysis reveals that the top 5 players hold approximately xx% of the market in 2025, indicating moderate concentration.

Innovation is a key driver, spurred by the need for efficient and sustainable solutions. Government regulations, including those promoting renewable energy and infrastructure development, significantly influence market dynamics. Product substitutes, such as decentralized energy generation models, pose a growing challenge. End-user trends, reflecting a rising demand for renewable energy and improved grid infrastructure, shape industry growth. M&A activity has been moderate in recent years, with approximately xx deals recorded between 2019 and 2024, primarily focused on expanding capabilities and market reach. Further consolidation is expected as larger players seek to strengthen their positions.

- Market Concentration: Top 5 players hold approximately xx% market share in 2025.

- M&A Activity: Approximately xx deals between 2019 and 2024.

- Key Drivers: Innovation, government regulations, end-user demand.

- Challenges: Competition from substitute products, evolving technological landscape.

India EPC Industry Industry Trends & Analysis

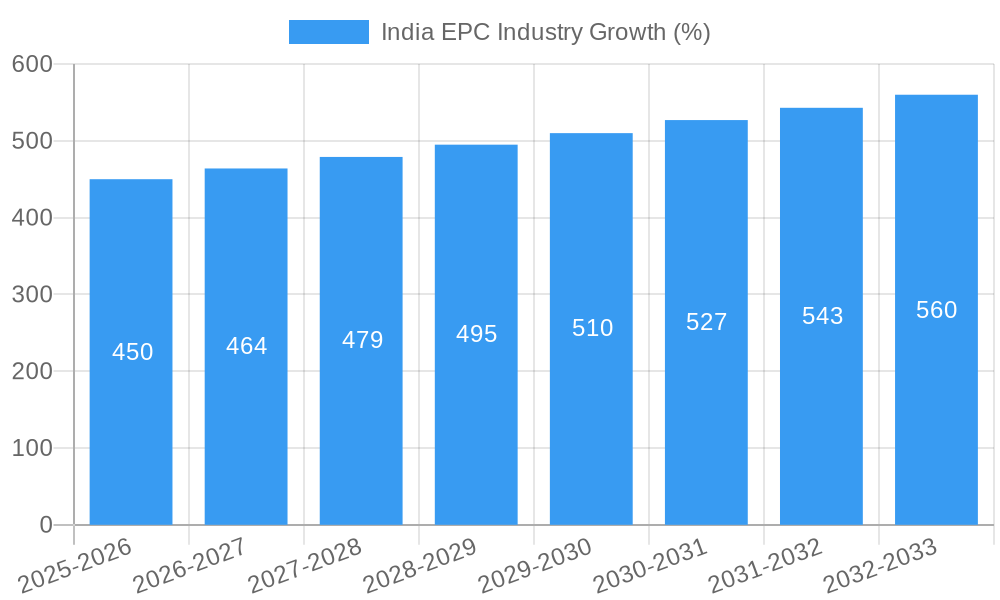

The Indian EPC industry is experiencing robust growth, driven by increasing investments in infrastructure development, particularly in power generation and transmission. The CAGR during the forecast period (2025-2033) is estimated at xx%. This growth is fueled by government initiatives focused on renewable energy targets and smart grid modernization. Technological disruptions, such as the rise of digital technologies in project management and automation, are transforming industry practices, enhancing efficiency and reducing costs. Consumer preferences are increasingly oriented towards sustainable and technologically advanced solutions, creating new market opportunities. Competitive dynamics are characterized by intense competition among large players and emerging specialized EPC companies catering to specific market segments. Market penetration of renewable energy EPC projects is expected to reach xx% by 2033, signaling significant growth in this sector.

Leading Markets & Segments in India EPC Industry

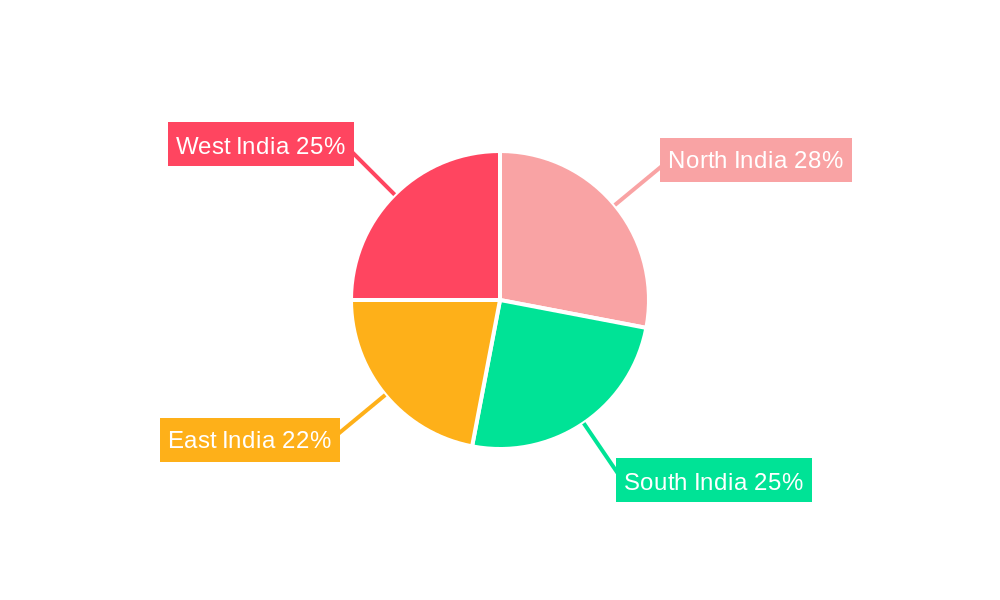

The thermal power generation segment remains the dominant market segment within the India EPC industry due to its continued importance in meeting the nation’s energy needs. However, the non-hydro renewable energy segment is experiencing rapid growth, driven by aggressive government targets for renewable energy integration and supportive policies. While the Hydro and Nuclear segments contribute significantly, they are comparatively less dominant than Thermal and Non-Hydro Renewables. Geographically, the growth is largely concentrated across several states with robust infrastructure plans.

- Thermal Power: Continued demand for electricity and existing infrastructure contribute to its dominance.

- Non-Hydro Renewables (Solar & Wind): Rapid growth driven by government policies and falling technology costs.

- Hydro Power: Relatively slower growth due to environmental concerns and project complexities.

- Nuclear Power: Steady growth with a focus on safety and regulatory compliance.

India EPC Industry Product Developments

Recent product innovations focus on enhancing efficiency, sustainability, and digital integration. This includes advanced project management software, automated construction techniques, and the adoption of Building Information Modeling (BIM). These innovations offer competitive advantages by improving project delivery timelines, reducing costs, and enhancing project quality. The market is witnessing a growing demand for solutions that integrate renewable energy sources and support smart grid infrastructure.

Key Drivers of India EPC Industry Growth

Government policies promoting renewable energy, infrastructure development, and "Make in India" initiatives are key drivers of growth. Technological advancements, such as improved energy storage solutions and digital project management tools, are significantly increasing efficiency and competitiveness. Economic growth and rising energy demand are fueling the need for expanded power generation and transmission capacity.

Challenges in the India EPC Industry Market

Regulatory hurdles, including complex approval processes and land acquisition challenges, can delay project implementation. Supply chain disruptions, particularly in procuring critical components and materials, can impact project timelines and costs. Intense competition among EPC players and the pressure to maintain profitability represent significant challenges. For example, fluctuating commodity prices may impact profitability for many companies.

Emerging Opportunities in India EPC Industry

Emerging technologies, such as advanced energy storage, smart grids, and AI-powered project management, present significant long-term growth opportunities. Strategic partnerships between EPC companies and technology providers will be crucial for leveraging these advancements. Expanding into new markets within the renewable energy sector and abroad could boost revenue streams.

Leading Players in the India EPC Industry Sector

- Larsen & Toubro Limited

- Sterling and Wilson Solar Ltd

- Doosan Corporation

- Bharat Heavy Electricals Limited

- Alstom SA

- Reliance Infrastructure Ltd (Reliance Group)

- Tata Group

- MECON Limited

- BGR Energy Systems Ltd

- Sterlite Power Transmission Limited

Key Milestones in India EPC Industry Industry

- 2020: Government announces ambitious renewable energy targets.

- 2021: Several significant M&A deals reshape the market landscape.

- 2022: Launch of new digital project management platforms by major EPC players.

- 2023: Increased focus on sustainable and environmentally friendly EPC practices.

Strategic Outlook for India EPC Industry Market

The Indian EPC industry is poised for sustained growth, driven by continued infrastructure investment and the transition towards renewable energy. Strategic partnerships, technological innovation, and the adoption of sustainable practices will be crucial for success. Expansion into new market segments and international markets will be vital for maintaining a competitive edge. The industry's future success hinges on adaptability, innovation, and a focus on sustainable and environmentally responsible development.

India EPC Industry Segmentation

-

1. Power Generation

- 1.1. Thermal

- 1.2. Hydro

- 1.3. Nuclear

- 1.4. Non-Hydro Renewables

- 2. Power Transmission and Distribution

India EPC Industry Segmentation By Geography

- 1. India

India EPC Industry REPORT HIGHLIGHTS

| Aspects | Details |

|---|---|

| Study Period | 2019-2033 |

| Base Year | 2024 |

| Estimated Year | 2025 |

| Forecast Period | 2025-2033 |

| Historical Period | 2019-2024 |

| Growth Rate | CAGR of > 3.00% from 2019-2033 |

| Segmentation |

|

Table of Contents

- 1. Introduction

- 1.1. Research Scope

- 1.2. Market Segmentation

- 1.3. Research Methodology

- 1.4. Definitions and Assumptions

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. 4.; Increase in Prices of Electricity Procured from Conventional Mechanisms 4.; Decline in Cost of Solar Energy Infrastructure

- 3.3. Market Restrains

- 3.3.1. 4.; Competition from Other Alternative Energy Sources

- 3.4. Market Trends

- 3.4.1. Conventional Thermal Segment Expected to Dominate the Market

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. India EPC Industry Analysis, Insights and Forecast, 2019-2031

- 5.1. Market Analysis, Insights and Forecast - by Power Generation

- 5.1.1. Thermal

- 5.1.2. Hydro

- 5.1.3. Nuclear

- 5.1.4. Non-Hydro Renewables

- 5.2. Market Analysis, Insights and Forecast - by Power Transmission and Distribution

- 5.3. Market Analysis, Insights and Forecast - by Region

- 5.3.1. India

- 5.1. Market Analysis, Insights and Forecast - by Power Generation

- 6. North India India EPC Industry Analysis, Insights and Forecast, 2019-2031

- 7. South India India EPC Industry Analysis, Insights and Forecast, 2019-2031

- 8. East India India EPC Industry Analysis, Insights and Forecast, 2019-2031

- 9. West India India EPC Industry Analysis, Insights and Forecast, 2019-2031

- 10. Competitive Analysis

- 10.1. Market Share Analysis 2024

- 10.2. Company Profiles

- 10.2.1 Larsen & Toubro Limited

- 10.2.1.1. Overview

- 10.2.1.2. Products

- 10.2.1.3. SWOT Analysis

- 10.2.1.4. Recent Developments

- 10.2.1.5. Financials (Based on Availability)

- 10.2.2 Sterling and Wilson Solar Ltd

- 10.2.2.1. Overview

- 10.2.2.2. Products

- 10.2.2.3. SWOT Analysis

- 10.2.2.4. Recent Developments

- 10.2.2.5. Financials (Based on Availability)

- 10.2.3 Doosan Corporation

- 10.2.3.1. Overview

- 10.2.3.2. Products

- 10.2.3.3. SWOT Analysis

- 10.2.3.4. Recent Developments

- 10.2.3.5. Financials (Based on Availability)

- 10.2.4 Bharat Heavy Electricals Limited

- 10.2.4.1. Overview

- 10.2.4.2. Products

- 10.2.4.3. SWOT Analysis

- 10.2.4.4. Recent Developments

- 10.2.4.5. Financials (Based on Availability)

- 10.2.5 Alstom SA

- 10.2.5.1. Overview

- 10.2.5.2. Products

- 10.2.5.3. SWOT Analysis

- 10.2.5.4. Recent Developments

- 10.2.5.5. Financials (Based on Availability)

- 10.2.6 Reliance Infrastructure Ltd (Reliance Group)

- 10.2.6.1. Overview

- 10.2.6.2. Products

- 10.2.6.3. SWOT Analysis

- 10.2.6.4. Recent Developments

- 10.2.6.5. Financials (Based on Availability)

- 10.2.7 Tata Group

- 10.2.7.1. Overview

- 10.2.7.2. Products

- 10.2.7.3. SWOT Analysis

- 10.2.7.4. Recent Developments

- 10.2.7.5. Financials (Based on Availability)

- 10.2.8 MECON Limited*List Not Exhaustive

- 10.2.8.1. Overview

- 10.2.8.2. Products

- 10.2.8.3. SWOT Analysis

- 10.2.8.4. Recent Developments

- 10.2.8.5. Financials (Based on Availability)

- 10.2.9 BGR Energy Systems Ltd

- 10.2.9.1. Overview

- 10.2.9.2. Products

- 10.2.9.3. SWOT Analysis

- 10.2.9.4. Recent Developments

- 10.2.9.5. Financials (Based on Availability)

- 10.2.10 Sterlite Power Transmission Limited

- 10.2.10.1. Overview

- 10.2.10.2. Products

- 10.2.10.3. SWOT Analysis

- 10.2.10.4. Recent Developments

- 10.2.10.5. Financials (Based on Availability)

- 10.2.1 Larsen & Toubro Limited

List of Figures

- Figure 1: India EPC Industry Revenue Breakdown (Million, %) by Product 2024 & 2032

- Figure 2: India EPC Industry Share (%) by Company 2024

List of Tables

- Table 1: India EPC Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 2: India EPC Industry Revenue Million Forecast, by Power Generation 2019 & 2032

- Table 3: India EPC Industry Revenue Million Forecast, by Power Transmission and Distribution 2019 & 2032

- Table 4: India EPC Industry Revenue Million Forecast, by Region 2019 & 2032

- Table 5: India EPC Industry Revenue Million Forecast, by Country 2019 & 2032

- Table 6: North India India EPC Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 7: South India India EPC Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 8: East India India EPC Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 9: West India India EPC Industry Revenue (Million) Forecast, by Application 2019 & 2032

- Table 10: India EPC Industry Revenue Million Forecast, by Power Generation 2019 & 2032

- Table 11: India EPC Industry Revenue Million Forecast, by Power Transmission and Distribution 2019 & 2032

- Table 12: India EPC Industry Revenue Million Forecast, by Country 2019 & 2032

Frequently Asked Questions

1. What is the projected Compound Annual Growth Rate (CAGR) of the India EPC Industry?

The projected CAGR is approximately > 3.00%.

2. Which companies are prominent players in the India EPC Industry?

Key companies in the market include Larsen & Toubro Limited, Sterling and Wilson Solar Ltd, Doosan Corporation, Bharat Heavy Electricals Limited, Alstom SA, Reliance Infrastructure Ltd (Reliance Group), Tata Group, MECON Limited*List Not Exhaustive, BGR Energy Systems Ltd, Sterlite Power Transmission Limited.

3. What are the main segments of the India EPC Industry?

The market segments include Power Generation , Power Transmission and Distribution.

4. Can you provide details about the market size?

The market size is estimated to be USD XX Million as of 2022.

5. What are some drivers contributing to market growth?

4.; Increase in Prices of Electricity Procured from Conventional Mechanisms 4.; Decline in Cost of Solar Energy Infrastructure.

6. What are the notable trends driving market growth?

Conventional Thermal Segment Expected to Dominate the Market.

7. Are there any restraints impacting market growth?

4.; Competition from Other Alternative Energy Sources.

8. Can you provide examples of recent developments in the market?

N/A

9. What pricing options are available for accessing the report?

Pricing options include single-user, multi-user, and enterprise licenses priced at USD 3800, USD 4500, and USD 5800 respectively.

10. Is the market size provided in terms of value or volume?

The market size is provided in terms of value, measured in Million.

11. Are there any specific market keywords associated with the report?

Yes, the market keyword associated with the report is "India EPC Industry," which aids in identifying and referencing the specific market segment covered.

12. How do I determine which pricing option suits my needs best?

The pricing options vary based on user requirements and access needs. Individual users may opt for single-user licenses, while businesses requiring broader access may choose multi-user or enterprise licenses for cost-effective access to the report.

13. Are there any additional resources or data provided in the India EPC Industry report?

While the report offers comprehensive insights, it's advisable to review the specific contents or supplementary materials provided to ascertain if additional resources or data are available.

14. How can I stay updated on further developments or reports in the India EPC Industry?

To stay informed about further developments, trends, and reports in the India EPC Industry, consider subscribing to industry newsletters, following relevant companies and organizations, or regularly checking reputable industry news sources and publications.

Methodology

Step 1 - Identification of Relevant Samples Size from Population Database

Step 2 - Approaches for Defining Global Market Size (Value, Volume* & Price*)

Note*: In applicable scenarios

Step 3 - Data Sources

Primary Research

- Web Analytics

- Survey Reports

- Research Institute

- Latest Research Reports

- Opinion Leaders

Secondary Research

- Annual Reports

- White Paper

- Latest Press Release

- Industry Association

- Paid Database

- Investor Presentations

Step 4 - Data Triangulation

Involves using different sources of information in order to increase the validity of a study

These sources are likely to be stakeholders in a program - participants, other researchers, program staff, other community members, and so on.

Then we put all data in single framework & apply various statistical tools to find out the dynamic on the market.

During the analysis stage, feedback from the stakeholder groups would be compared to determine areas of agreement as well as areas of divergence